Adobe: Is AI expected to kill the company or help it thrive?

Earnings Review Q4'FY24

Hi StockOpiner,

Merry Christmas! We hope you're enjoying your holidays and wish you a New Year filled with happiness, health, and joy. If you’ve forgotten about your investment geek friend, don’t worry—you can always make it up to them by gifting a subscription to StockOpine to give them access to our insights. You know best who deserves such a gift! 🎁

On another note, we want to let you know that we plan to send out an explanatory post about our valuation process (possibly in a short, educational format series). If you have any suggestions, feel free to send us a message—we welcome feedback from everyone, not just paid subscribers.

But first, a word from our sponsor!! 👇

Borsa is an earnings season tool that has become indispensable in our research routine. Don't have time to read an entire earnings call transcript? Borsa's latest AI Summary feature makes catching up on earnings calls quicker and easier than ever. Borsa provides concise summaries of the opening remarks and the Q&A portion of every earnings call.

Borsa's AI Summary includes citations that link directly to the moment in the call where the topic was discussed, providing an interactive table of contents for every earnings call. Skip to specific discussions on operational metrics, market trends, guidance, etc. with just one click.

Borsa isn’t just simple—it’s a powerful tool for finance pros. With presentation slides, earnings releases, and transcripts for every call, Borsa makes researching companies incredibly easy. Don’t miss a beat—streamline your research with Borsa (iOS | Android).

Now, back to Adobe: we first covered the company in April when it was trading around the same levels as today. Since then, the share price has been volatile but never turned into a positive return trajectory for the year. After its recent drop following the earnings report on December 11, 2024, the company sits at a negative YTD return of -25%.

In this article, we’ll assess the latest earnings report, discuss the AI developments, which remain a major concern for investors, evaluate the company’s future, update our valuation, and let you know if we are taking any action in our portfolio.

With that, let’s dive in.

1. Results Overview

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

Q4’24 results exceeded consensus estimates across the board, as well as the guidance provided by management last quarter. This marks a repeat of their performance in Q3’23, demonstrating Adobe's consistent execution.

a. Financial Performance

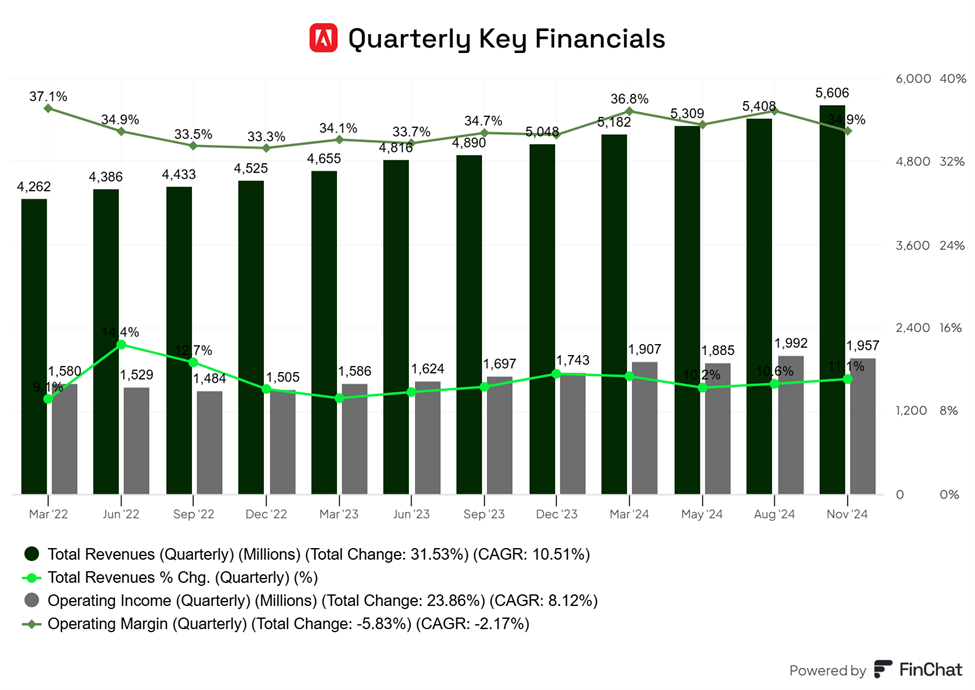

Net Revenue: $5.61 billion for Q4, up 11%. FY24 revenue reached $21.51 billion, also up 11%, with 95% derived from subscriptions, which grew by 12%.

Operating Income:

GAAP: $1.96 billion, up 12% (34.9% margin vs. 34.5% in Q4’23).

Non-GAAP: $2.6 billion, up 11% (46.3% margin vs. 46.4% in Q4’23).

Earnings Per Share (EPS):

GAAP: $3.79 for Q4, up 17%; annual EPS at $12.36, up 5%.

Non-GAAP: $4.81 for Q4, up 13%; annual EPS at $18.42, up 15%.

Remaining Performance Obligations (RPO): Total RPO reached $19.96 billion, up 16%, adding $2.745 billion year-over-year—a record high. Current RPO grew by 13%.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

b. Segments

Digital Media

Digital Media revenue reached $4.15 billion, up 12%, exceeding mid-guidance of $4.105 billion. The segment added a record $578 million in net new ARR (above guidance of $550 million), bringing annual addition to over $2 billion, driven by product innovation, social media, and AI integrations. Digital Media ARR now stands at $17.33 billion, up 13% year-over-year (FX-adjusted: $17.22 billion), while annual revenue for the segment reached $15.86 billion, up 11.6%.

Creative Cloud generated $3.3 billion in revenue (up 10%), with ARR reaching $13.85 billion (up 11%) and net new ARR of $405 million for the quarter. This growth was driven by Adobe Express integrations with platforms like ChatGPT, Google, Slack, and Webflow, expanding customer reach. Additionally, there was strong momentum in emerging markets and the adoption of Firefly Services within enterprises, further fueled growth. The rollout of Firefly Services is gaining momentum, with the Firefly Video Model set for a broader launch in 2025. The beta integration with Premiere Pro has already driven a 70% increase in beta users, reflecting strong customer interest.

Document Cloud also showed impressive growth, with revenue of $843 million (up 17%) and ARR at $3.48 billion (up 23%). This growth was driven by the accelerated adoption and monetization of AI Assistant, as well as strong performance across Reader and Acrobat on web and mobile, along with extensions like Edge and Chrome. Acrobat Web's success in expanding the free user base is evident, with MAUs up 50% year-over-year. Total Document Cloud MAUs, including both paid and free users, grew 25% year-over-year to surpass 650 million, underlining Adobe's relevance and long-term monetization potential.

Management remains optimistic, stating, “We are very effective at taking free users of Reader and converting them to paid users of Acrobat. And we continue to do that across more surfaces that used to be predominantly a focus on desktop applications. As we've noted in the past, we now have Edge integrations and Chrome integrations.”

Meanwhile, innovations such as AI Assistant, now integrated across desktop, web, mobile, and extensions like Microsoft Teams, are also driving deeper customer value.

“A recent productivity study found that users leveraging AI Assistant completed their document-related tasks four times faster on average. AI Assistant is now available in Acrobat across desktop, web and mobile and integrated into our Edge, Chrome and Microsoft Teams extensions [...] We saw AI Assistant conversations double quarter over quarter, driving deeper customer value.” David Wadhwani, President of Digital Media

Digital Media’s gross profitability remained exceptional, reaching 95.4%, up 100bps year-over-year. While Adobe continues to attract more users through its innovations, the focus remains on adding value and effectively monetizing its expanding ecosystem, reflecting the company's resilience and strategic positioning for continued growth.