Adobe Q2 FY26: Attractive Valuation vs Strategic Pivot Uncertainty

Record Top-line, Aggressive User Acquisition and a New Financial Lead

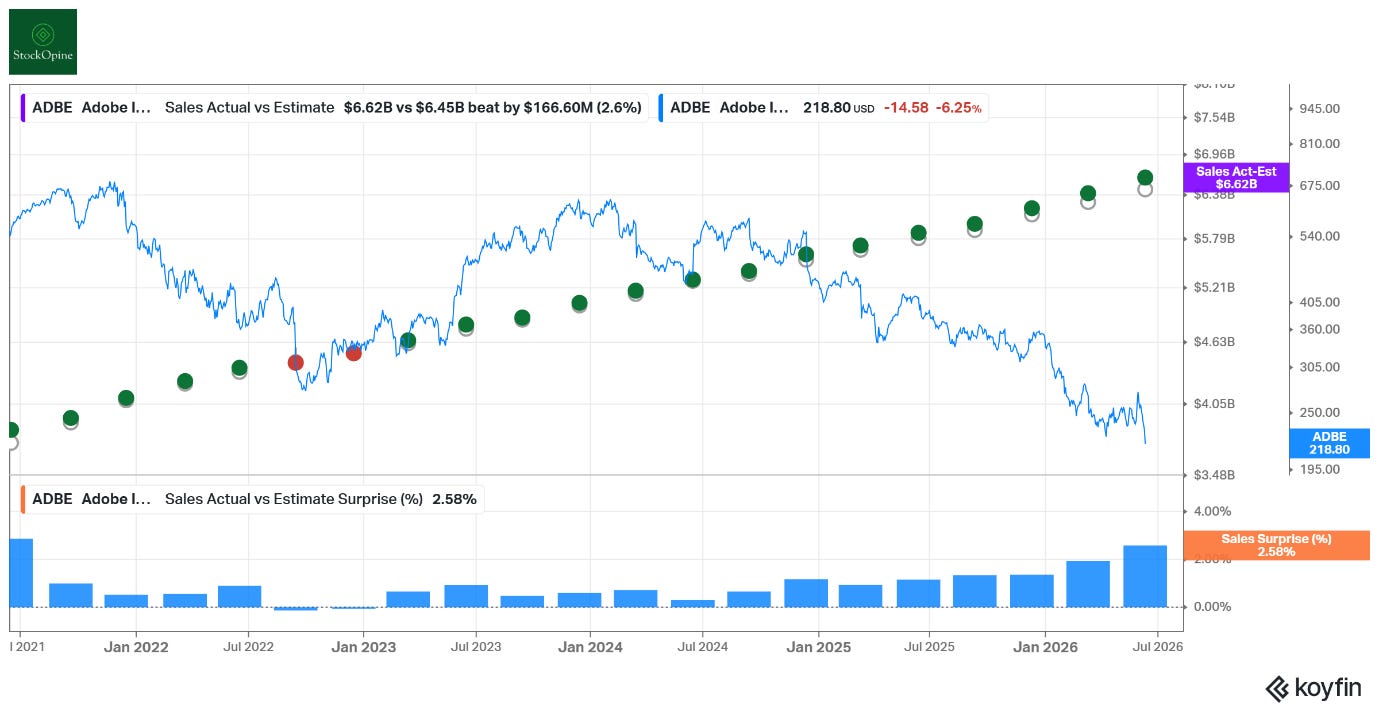

Adobe delivered a strong second quarter for fiscal 2026, achieving record revenue of $6.62 billion, representing 12.7% year-over-year growth and exceeding analyst expectations. However, the quarter was defined by more than just financial beats. Adobe is shifting toward a freemium-first acquisition model, choosing to prioritize user growth and long-term lifetime value over immediate monetization. Additionally, CFO Dan Durn is departing while the search for a new CEO continues as Shantanu Narayen prepares to transition to Board Chair.

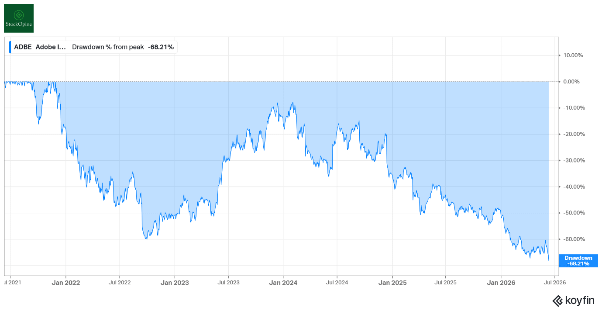

With the stock trading at a 68% drawdown from its peak and historically low multiples, the question remains: is Adobe’s AI strategy working?

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

In this article, we analyze the ongoing AI transition, and highlight key takeaways from the earnings call. We also assess Adobe’s valuation and let you know if we are making any changes to our portfolio.

1. Results Overview

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

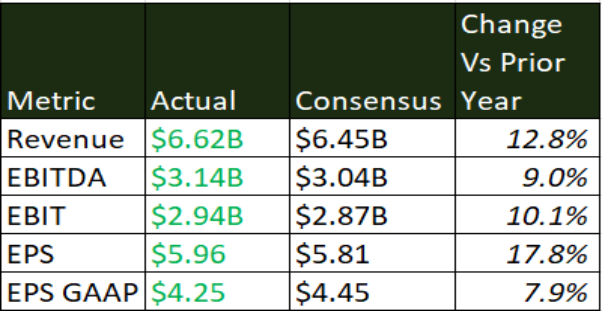

Revenue: Adobe’s revenues comfortably surpassed both Wall Street consensus and the company’s own guidance from last quarter. Total revenue reached a record-breaking $6.62 billion, marking the highest Q2 top-line performance in Adobe’s history, driven by a 13% growth rate on a reported basis and an 11% increase in constant currency. Revenue growth ex-Semrush stood at 12% year-over-year.

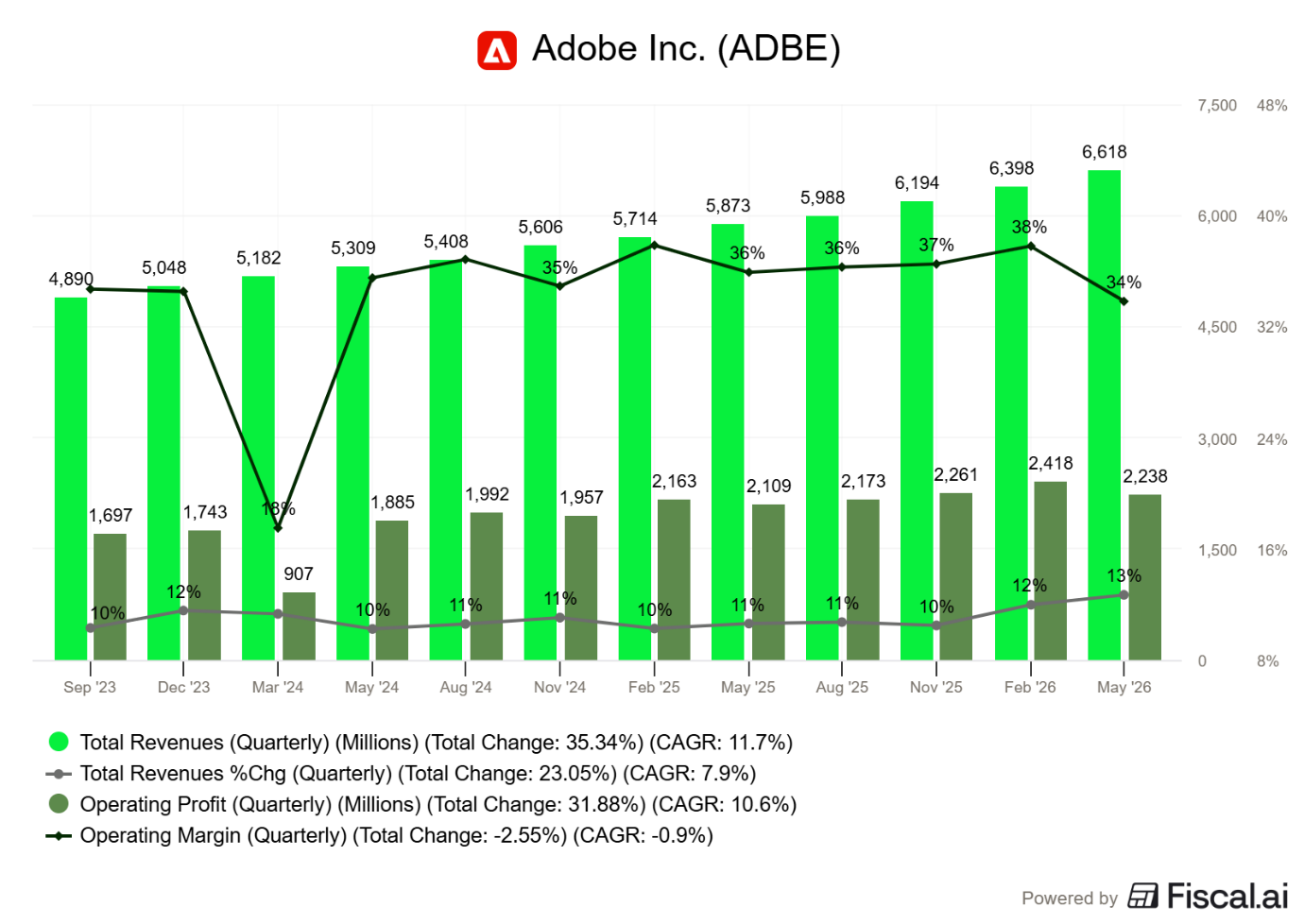

Operating Margins: This top-line strength was accompanied by a contraction in operating margin, as heavy AI-related infrastructure investments and structural costs weighed on the bottom line. GAAP operating margin compressed by 210 basis points to 33.8% in Q2 FY26, down from 35.9% in the prior year’s quarter. Operating margin ex-Semrush declined by 189 basis points to 34%. This profitability pressure was primarily driven by outsized spending in Sales & Marketing ($1.9 billion, +15.9% YoY) and G&A expenses ($546 million, +44.8% YoY), both of which outpaced Adobe’s 13% YoY revenue growth.

Earnings Per Share (EPS): Non-GAAP EPS reached $5.96, an 17.8% increase year-over-year. GAAP EPS was $4.25, impacted by a $70 million ($0.17 per share) non-cash goodwill impairment charge related to the Publishing & Advertising unit.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

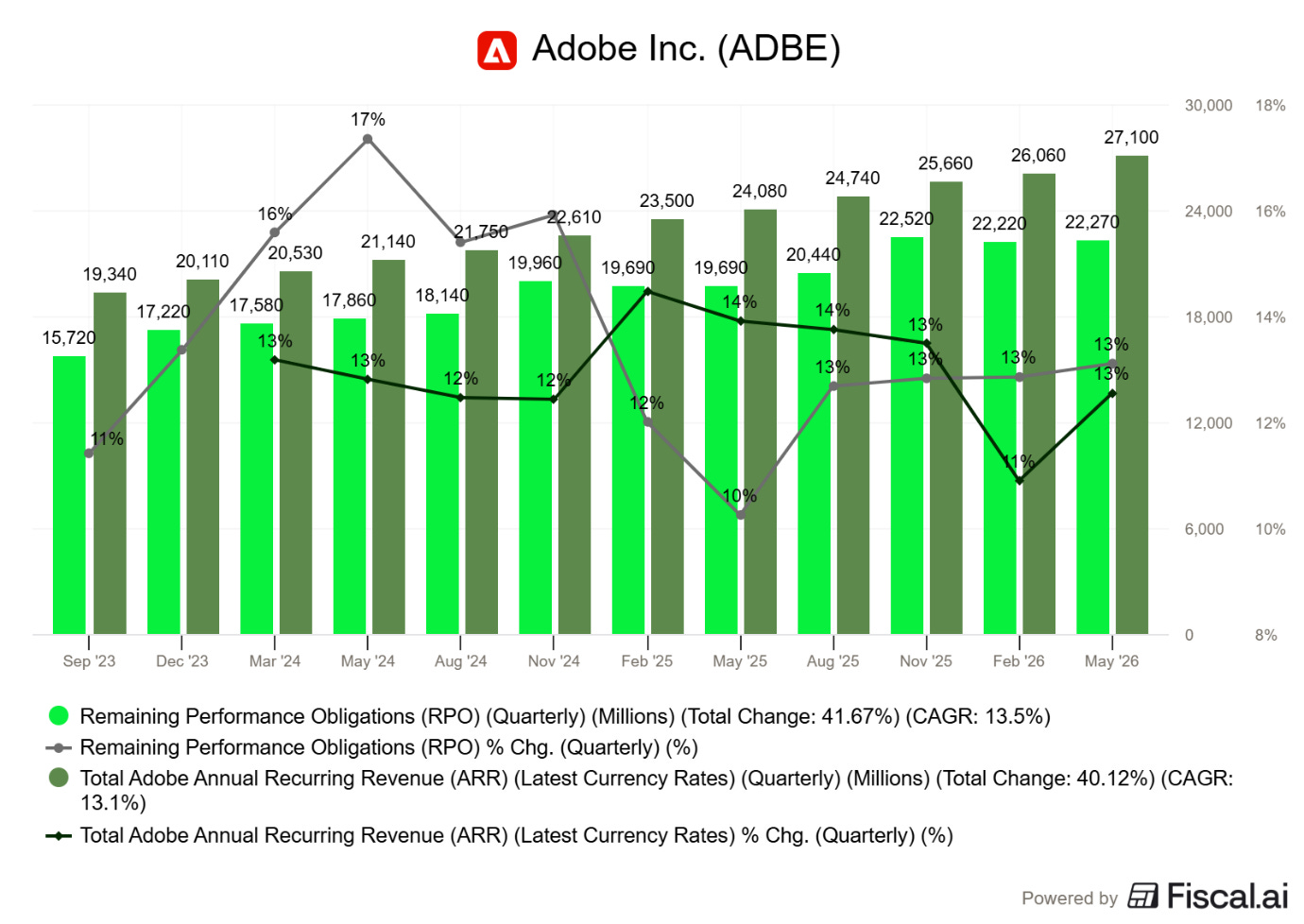

ARR & RPO: Remaining Performance Obligations exiting Q2 stood at $22.27 billion, growing 13% year over year (12% in constant currency) and a modest sequential increase from $22.22 billion at Q1FY26 end. Current RPO (cRPO) also grew 13% year-over-year and remained consistent with the previous quarter at 67%.

Moving to ARR in Q2, it reached $27.10 billion up 12.5% year over year. This re-acceleration from Q1’s 10.9% (+3.7% QoQ) growth was mainly driven by the $480 million ARR contribution from the Semrush acquisition (growth was 10.5% excluding the acquisition impact). AI-first ARR grew ~25% quarter on quarter (from +$400m in Q1) and tripled YoY to more than $500 million.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Adobe also generated $2.17 billion in operating cash flows compared to $2.19 billion in the same period last year reflecting a minor increase in working capital requirements.

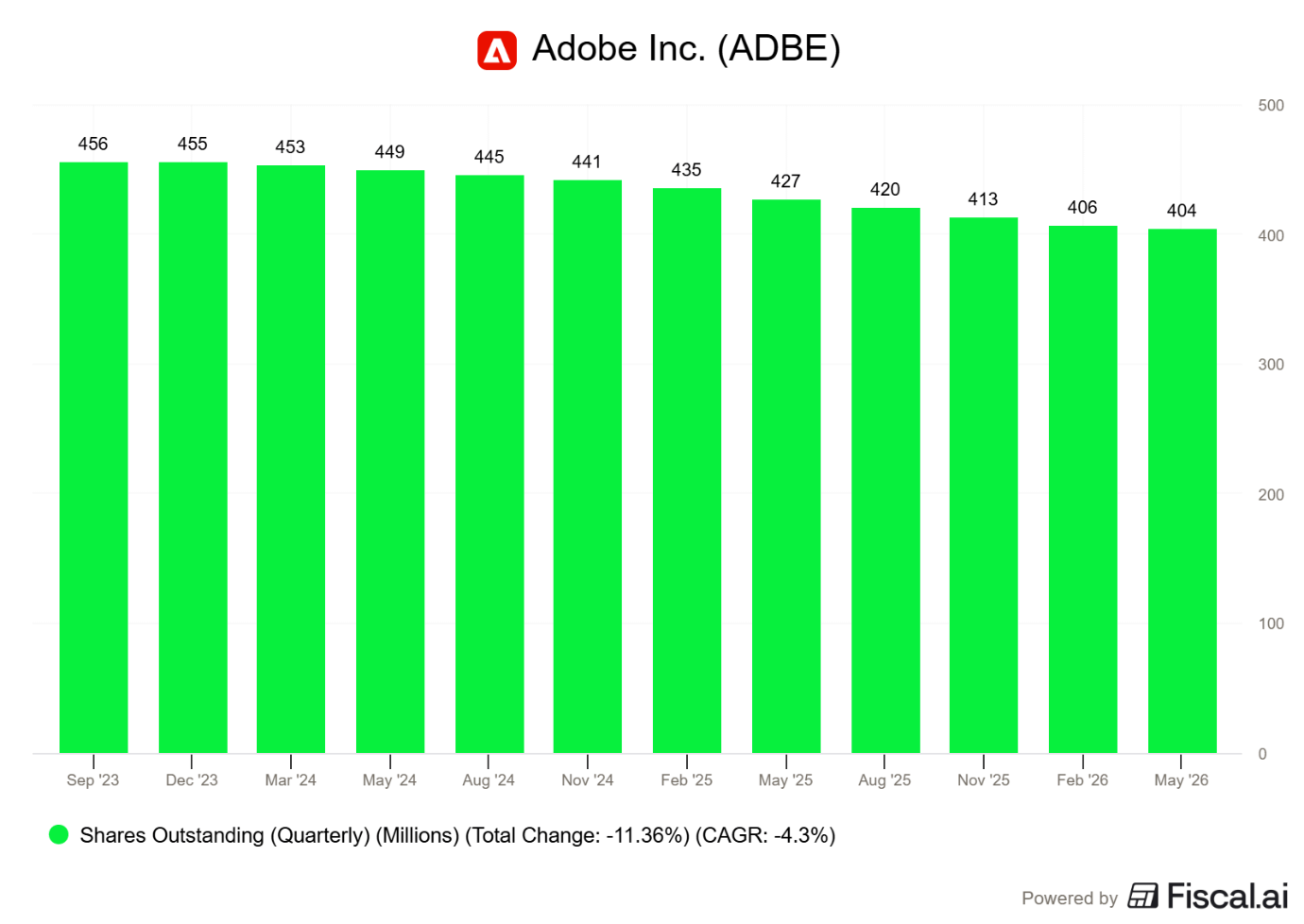

Meanwhile, the company sustained its aggressive capital return strategy, repurchasing 8.5 million shares over the quarter. Following a new 25 billion authorization in April, the company has approximately 27 billion remaining for future repurchases.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

2. Customer Group Performance

Both subscription groups showed sustained double-digit growth, even as Adobe rebalanced its funnel toward freemium onboarding.

a. Business Professionals & Consumers

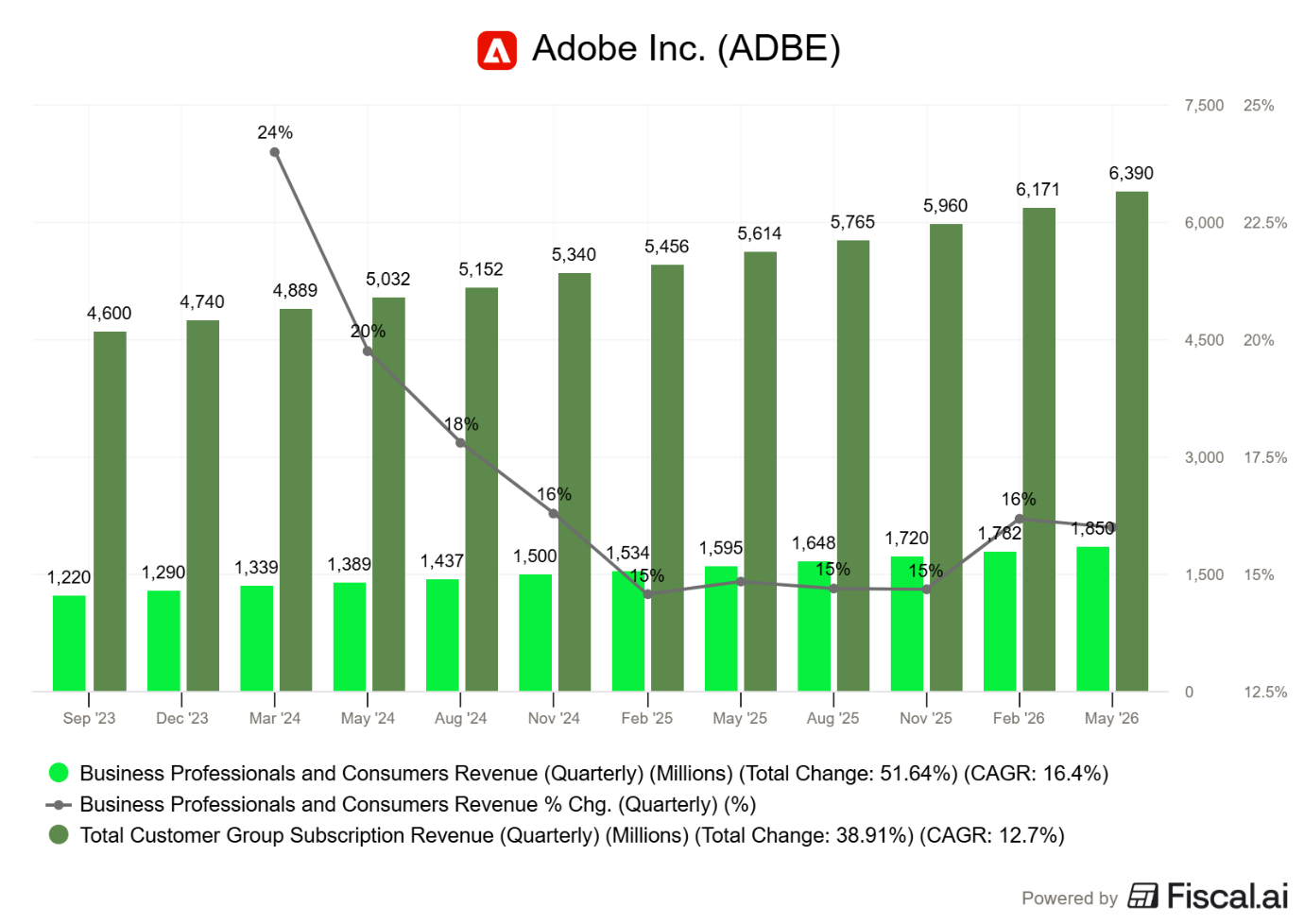

Business Professionals & Consumers subscription revenue surged 16% YoY (11% on constant currency basis) to $1.85 billion, accounting for 29% of Adobe’s total subscriptions. A key driver this quarter was the introduction of the Adobe Productivity Agent, a breakthrough AI experience embedded within Acrobat that leverages document intelligence and Adobe Express to seamlessly transform static files into dynamic assets like presentations, podcasts and social content. This strategic shift toward interactive document workflows, complemented by the ability to share branded PDF Spaces featuring customizable AI assistants, is successfully transitioning users from passive readers to active collaborators.

Rapid adoption of these capabilities fueled an approximate 3x YoY growth in Acrobat AI Assistant ARR, alongside a stellar 150%+ YoY increase in paid MAUs. Simultaneously, Express MAU expanded by more than 20% quarter-over-quarter. Together, combined Acrobat and Express Monthly Active Users (MAU) surpassed the 850 million milestone, climbing roughly 20% YoY.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

b. Creative & Marketing Professionals

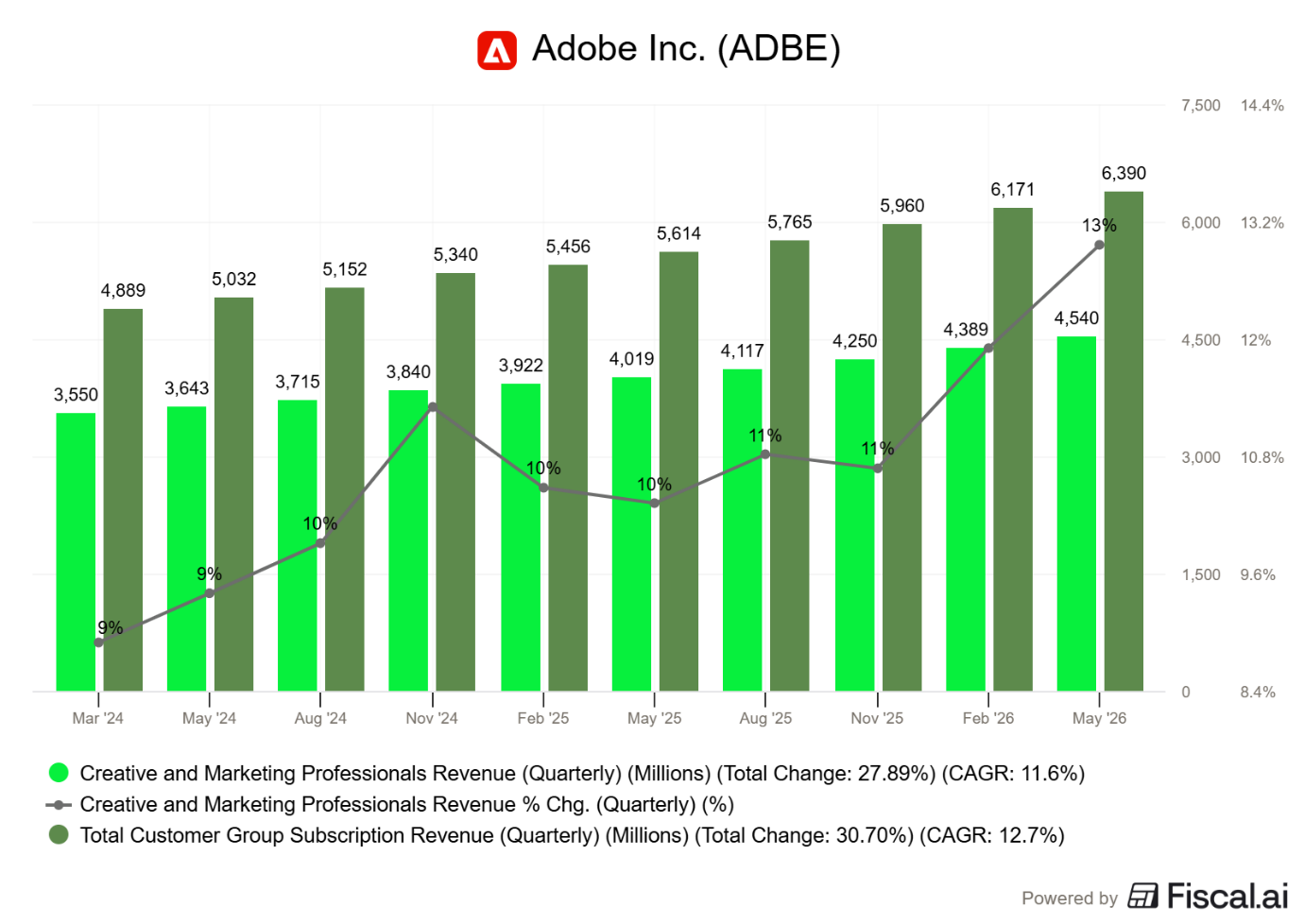

Revenue grew 13% year-over-year (11% YoY on constant currency) to $4.54 billion.

Creators & Creative Professionals: With the beta launch of the Adobe Creative Agent and the integration of third-party models like Kling 3.0, Adobe has evolved its “all-in-one creative AI studio” into an agentic production hub. This shift drove record AI usage across flagship applications like Photoshop and Illustrator, while Firefly ARR expanded approximately 50% sequentially via app subscriptions and credit packs. High-value content generation continues to scale at an impressive rate with a greater than 4x YoY surge in assets generated through Firefly Enterprise. Furthermore, solutions like Firefly Services and Firefly Foundry, now supercharged by a strategic NVIDIA partnership for accelerated computing, are empowering global enterprises to industrialize brand-safe content production at unprecedented speed while drastically lowering operational costs. Overall, the top-of-funnel remains efficient, as Creative freemium MAU (spanning Firefly, Express and mobile apps) surpassed 90 million users, reflecting a 70%+ YoY growth rate.

Marketing Professionals: Adobe’s Customer Experience Orchestration (CXO) strategy has centered on the new Adobe CX Enterprise, an end-to-end agentic architecture that seamlessly bridges design and marketing teams to govern the entire customer lifecycle. Enterprise adoption achieved a new milestone this quarter, with over 80% of AEP and AEM customers deploying integrated agentic capabilities, up from 70% in Q1. Momentum is robust, with subscription revenue for AEP and native apps jumping over 30% YoY, while the Adobe GenStudio portfolio grew its ending ARR by more than 25% YoY as multinational brands standardize their content supply chains on Adobe’s ecosystem. Additionally, the recent acquisition of Semrush extends Adobe’s competitive moat into search and brand visibility across the agentic web.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

3. Strategic Pivot: Freemium Focus and Deferred Pricing

The standout theme of the Q2 report is Adobe’s deliberate decision to prioritize user acquisition over immediate ARR.