Adobe's Q1 FY26: Strong Execution, but Is the Market Right to Stay Sceptical?

Record Numbers, Margin Pressure, and a Historic Leadership Change

Adobe kicked off fiscal 2026 with record-breaking quarter, revenue and operating cash flow both hit all-time Q1 highs, and once again beat analyst expectations across every key metric. That said operating margins are under pressure, declining year over year but improving sequentially as AI investment ramps. The quarter’s biggest headline was the transition of its CEO Shantanu Narayen, who has led Adobe for 18 years, from CEO to Chair of the Board.

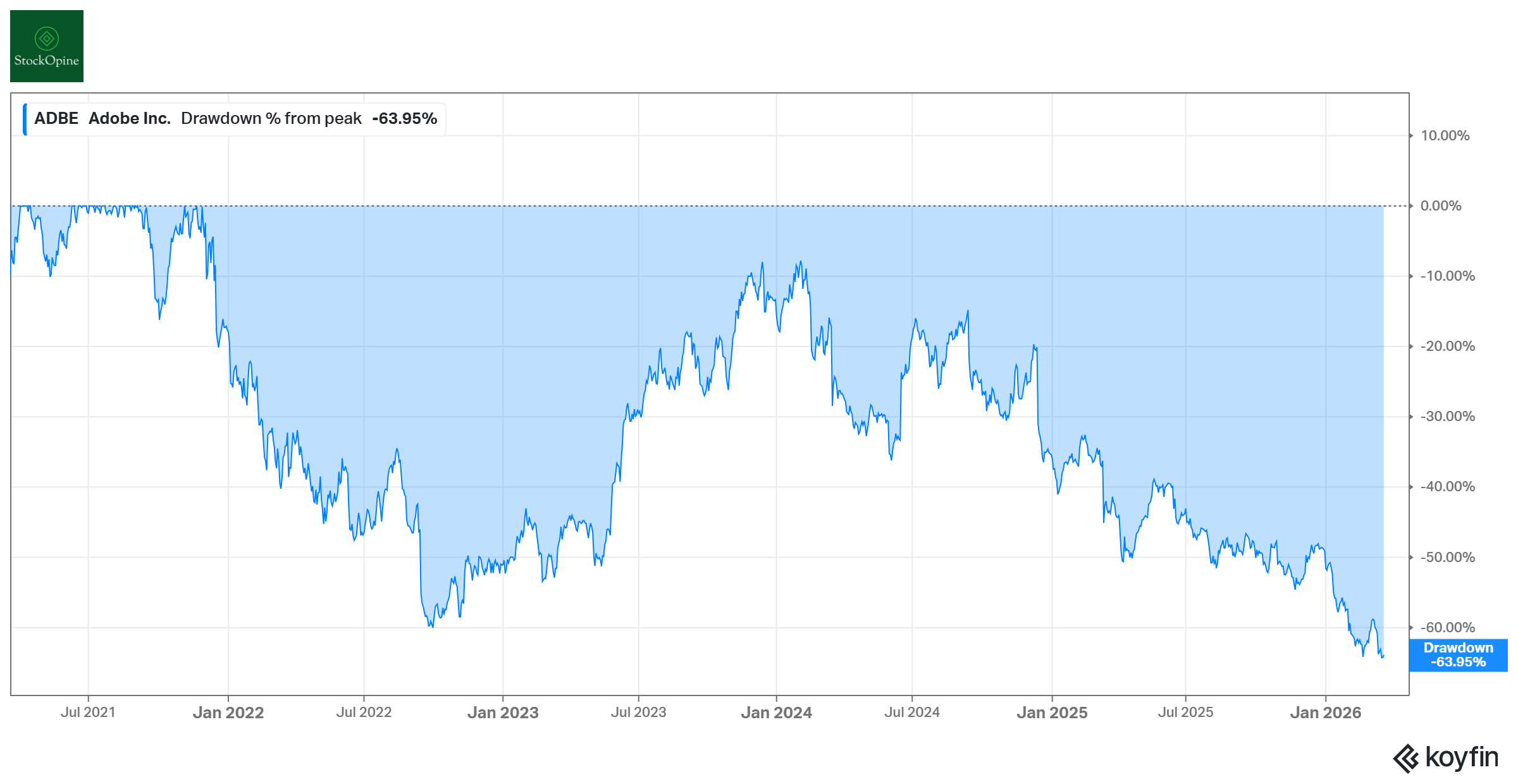

Meanwhile, the stock is selling at historically low valuation multiples and is about 64% below its peak.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

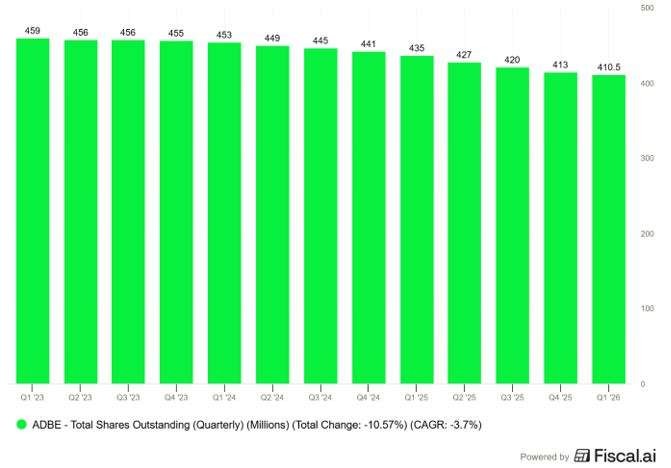

Adobe has also extended its run of earnings & sales beats over the past 5 years (it only missed sales consensus twice) by continuing to grow revenue and profitability at a consistent rate. The earnings beat magnitude has widened over the past three quarters driven both by performance and by the aggressive buyback program, reducing shares outstanding from 435 million in Q1’25 to 410 million in Q1’26 .

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

In this article, we’ll break down Adobe’s Q1’26 earnings, analyse the ongoing AI transition, highlight key takeaways from the earnings call, assess Adobe’s valuation and let you know if we are doing any changes in our portfolio.

1. Results Overview

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

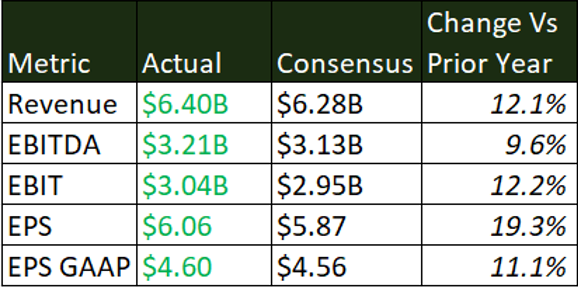

Adobe’s Q1 FY26 results exceeded expectations across the board, surpassing both analyst consensus and the guidance provided last quarter. Revenue hit $6.40 billion, growing 12% as reported and 11% in constant currency, the highest Q1 revenue in company history.

However, the top-line strength came alongside a modest operating margin contraction, as increasing AI-related investments weighed on profitability. GAAP operating margin came in at 37.8% in Q1 FY26, down from 37.9% in Q1 FY25 (a 10-basis point contraction). The underlying driver is sales & marketing ($1.71B, +14% YoY) and G&A ($463M, +26% YoY) which are growing faster than revenue.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

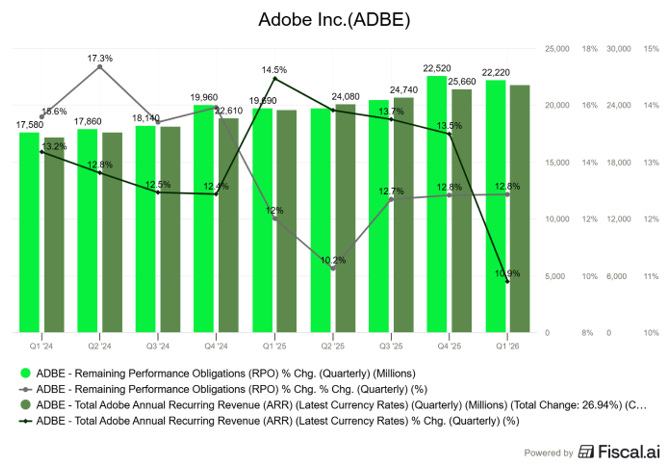

Remaining Performance Obligations (RPO) exiting Q1 stood at $22.22 billion, growing 13% year over year (12% in constant currency) while posting a sequential decline from $22.52B at Q4 FY25 end. Current RPO (cRPO) grew 12% year on year (+1.7% QoQ) and 11% in constant currency in this quarter. From FY24 to FY25, the ending cRPO coverage ratio (ending cRPO/Next 12M revenue) increased, reaching 56.32% in FY25 and edging up further to 57.26% in Q1 FY26, suggesting improving near-term revenue visibility.

Moving to ARR in Q1 it reached $26.06 billion, up 10.9% year over year.

While the YoY growth rate held steady, the sequential deceleration from 11.5% was possibly due to increasing usage of AI but slower materialization to RPO. Management reaffirmed the full-year FY26 ARR growth target of 10.2%, implying double-digit ARR growth for each of the remaining three quarters.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

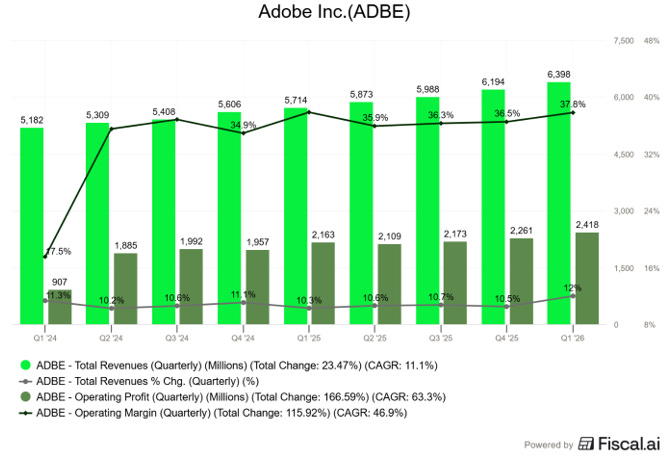

Adobe generated a Q1 record $2.96 billion in operating cash flows, up from $2.48 billion a year ago. The company repurchased 8.1 million shares (~2% of shares outstanding), with $3.89B remaining of the $25B authorization. With the stock trading at historically low multiples, management’s continued buyback pace signals strong confidence in Adobe’s long-term value.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

2. Customer Group Performance

Adobe reports two customer subscription groups. Both delivered strong double-digit growth in Q1 FY26:

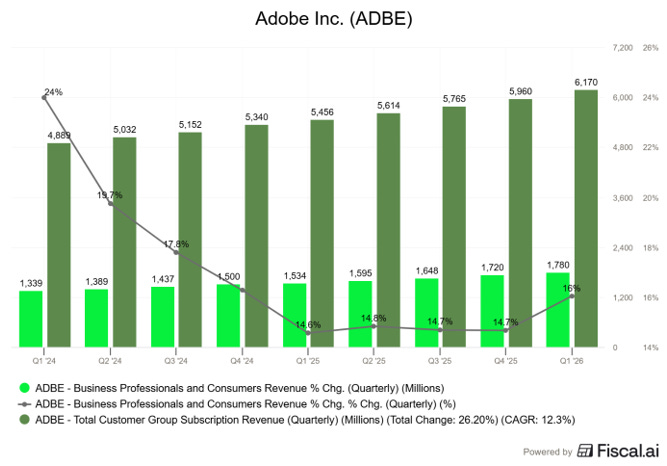

a. Business Professionals and Consumers – Revenue increased 16% YoY to $1.78 billion, contributing 29% to the total subscription revenue. With a single PDF or across documents in a PDF Space, Acrobat AI Assistant offers users conversational experiences that help them understand information more quickly and accurately. The connection between Acrobat and Express allows users to turn content they are consuming into audio summaries, infographics, presentations and more. Resonance with these features led the growth in AI Assistant MAU and ARR by 2x YoY and 3x YoY, respectively, in Q1FY26. Simultaneously, Express MAU was up 3x YoY and was integrated into 99% of U.S Fortune 500 companies.

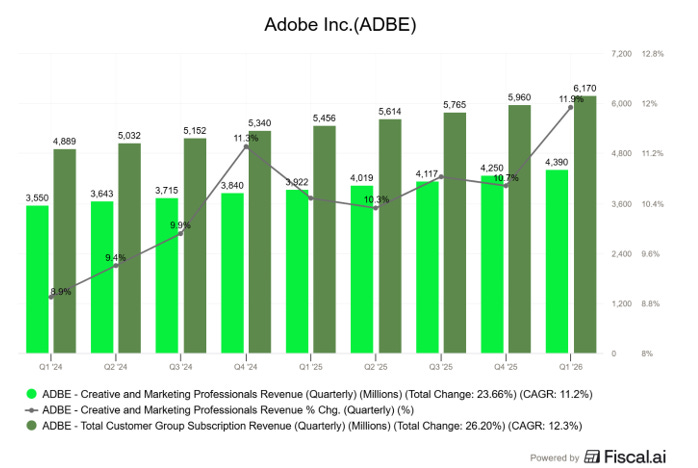

b. Creative & Marketing Professionals – Revenue rose 12% YoY to $4.39 billion, exceeding management’s guidance of $4.33 billion and accounting for 71.2% of total subscription revenue.

Creators & Creative Professionals: With over 30 AI models, including those from Google and OpenAI, sharing ideas using “Firefly Boards” and prompt-based editing capabilities with integrated photoshop and express web journeys, Firefly has changed from a basic AI tool into a professional creative hub. As a result, the total generative consumption has increased 45% QoQ in Q1FY26. The company reported rise in high value AI usage with video generative actions growing more than 8x YoY and audio generative actions expanding 2x YoY. Therefore, Adobe’s revenue from Firefly subscriptions and credit packed ending ARR jumped by 75% sequentially in Q1FY26. On the other hand, Firefly enterprise is experiencing new customer acquisition growth of 50% YoY. Tools such as Firefly services (provides API that allows creating of mass assets using automation) and Firefly foundry (allows the enterprise to train AI on their own IP without compromising on brand safety) have enabled large scale content creation at a faster pace and reduced costs.

Marketing Professionals: Adobe’s Customer Experience Orchestration (CXO) is a strategy which connects the design and marketing team through AEP and GenStudio. Adobe Experience Platform (AEP) uses AI agents to analyse customer behaviour through interactions and automate marketing campaigns. In Q1FY26, Adobe enabled the usage of these tools to AEP users through their Try and Buy program. The AEP AI Assistant is already being used by 70% of AEP customers. Subscription revenue for this platform and its apps grew 30% YoY, indicating sustained momentum. GenStudio is a one stop destination which combines separate Adobe’s tools required for digital content and manages activities right from idea to final ad. Ending ARR for the Adobe GenStudio products grew > 30% YoY as global leading brands and agencies are investing in Adobe ecosystem to power their content supply chain. If those growth rates and adoption trends suggest that AI is eating Adobe’s lunch, then we just disagree.

“In Q1, we introduced new AEP Agents along with expanded Agent Orchestrator capabilities, now available to all AEP customers, via a Try and Buy program. The scale of our platform has grown to over 35 trillion segment evaluations and more than 70 billion profile activations per day. Subscription revenue for AEP and native apps grew over 30% year over year, demonstrating continued momentum and value realization.” Anil Chakravarthy

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

In the sections below paywall we will dicuss AI developments, valuation and other highlights from the call.