Adobe’s Q1’25: Is the Post-Earnings Sell-Off an Opportunity?

Strong Execution, AI Uncertainty, and a Market Overreaction

Adobe kicked off fiscal 2025 with record revenue and operating cash flow in Q1, delivering another solid quarter. The Company beat analyst expectations and reaffirmed its full-year guidance, yet the stock plunged 14% the next day. Why? Investors weren’t excited with Adobe’s flat guidance, expecting a beat-and-raise instead of a reaffirmation.

This sharp reaction highlights growing concerns about generative AI’s impact on Adobe’s business. While management shed some light on AI-driven revenue contributions, it wasn’t enough to ease investor fears. As a result, Adobe is now sitting on a 30% drawdown, with valuation multiples nearly cut in half.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

Despite the noise, the fundamentals tell a different story. Adobe continues to grow revenue and earnings at a steady pace, extending its streak of nine consecutive earnings beats, proving its ability to execute.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

In this article, we’ll break down Adobe’s Q1’25 earnings, examine the latest AI developments that continue to be a key concern for investors, highlight key takeaways from the earnings call, and assess Adobe’s valuation in light of the recent market reaction.

1. Results Overview

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

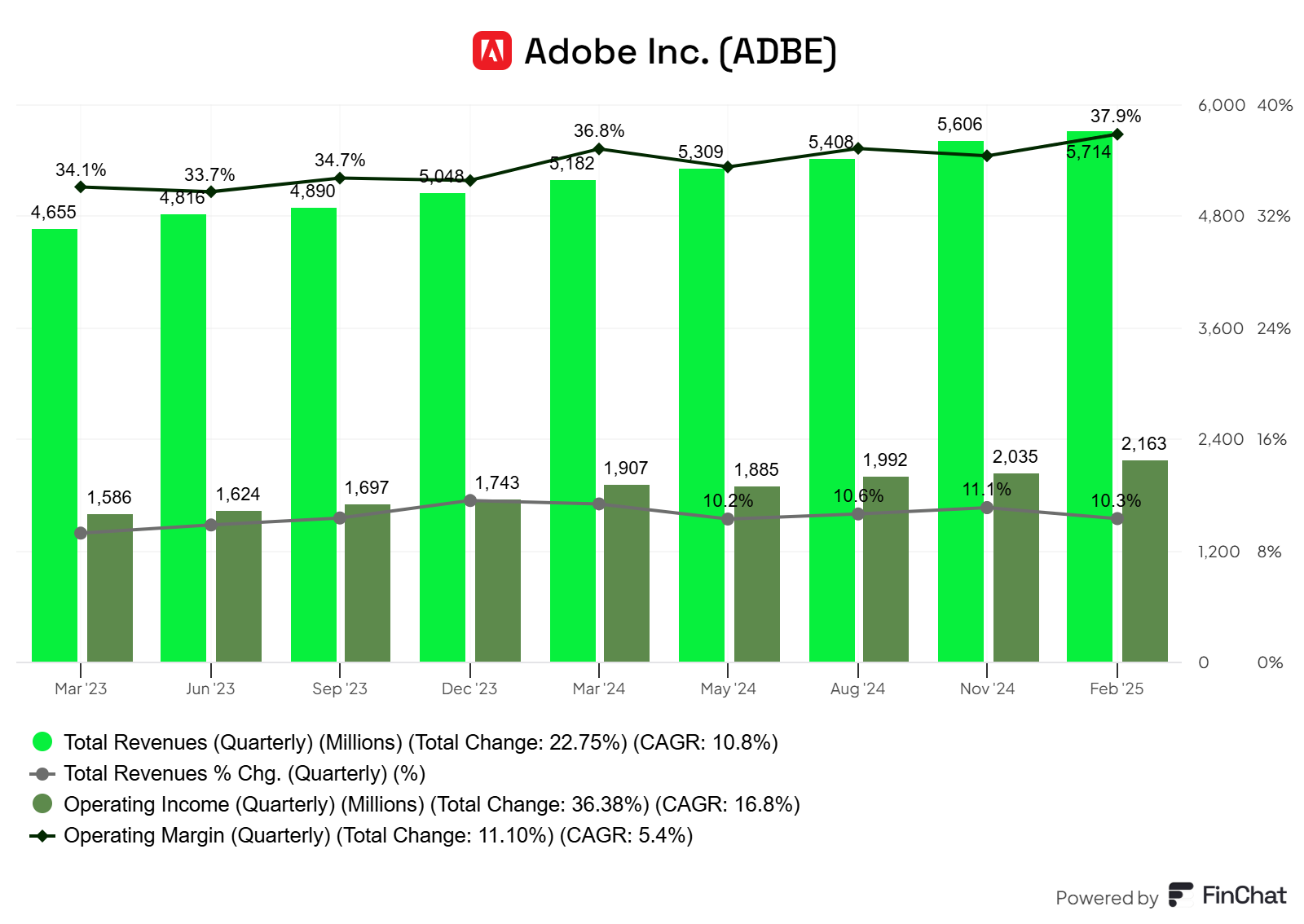

Adobe’s Q1’25 results exceeded expectations across the board, beating both analyst estimates and the guidance provided last quarter. The company continued to deliver double-digit growth, with revenue reaching $5.71 billion, up 10% year-over-year (11% in constant currency).

Despite ongoing investments in AI, Adobe managed to expand its operating margin to 37.9% in Q1’25 from 36.3% (excluding $1 billion termination fees paid for the Figma acquisition) in Q1’24, demonstrating cost efficiencies.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

Remaining Performance Obligations (RPO) grew 12% year-over-year, reaching $19.69 billion, adding $2.1 billion over the past year. However, RPO declined sequentially, reflecting a deceleration in growth. Management did not provide an explanation for the decline, making it inconclusive, especially since RPO can sometimes be a misleading indicator. The slowdown could stem from various factors, including seasonality, deal delays, fewer new contracts, or a ramp-up in deals in the previous quarter (which seems to be the case considering RPO growth in Q4’24). Without further clarification, it’s unclear whether this signals a broader trend or simply a temporary fluctuation.

Source: Adobe filings, StockOpine analysis

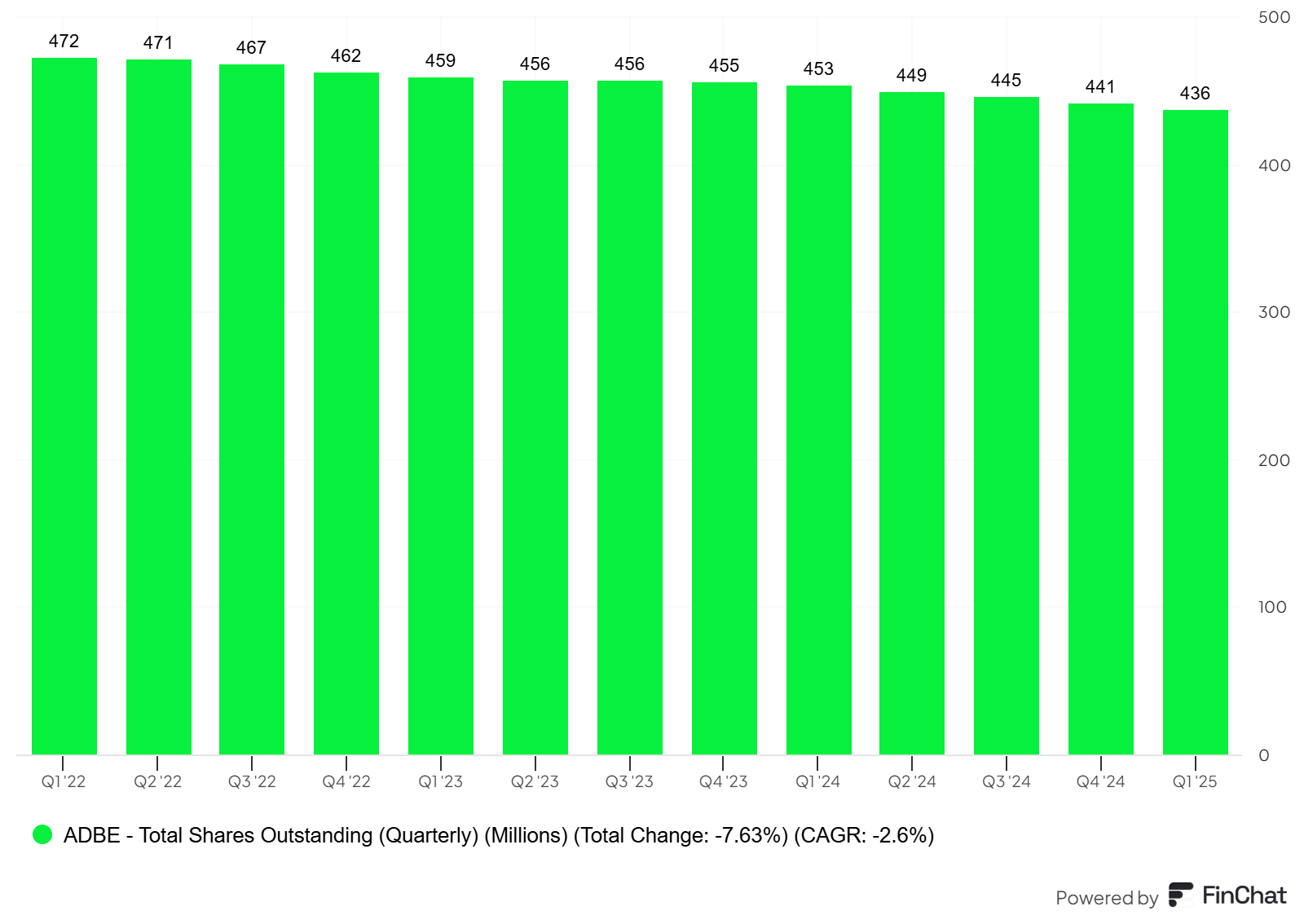

Adobe generated $2.48 billion in operating cash flow in Q1’25 and repurchased 7 million shares (approximately 1.5% of shares outstanding). The Company accelerated its buyback, spending $3.25 billion on repurchases, up from $2.6 billion in the previous quarter and $2.2 billion a year ago. The ramp-up in buybacks signals management’s confidence in Adobe’s valuation. With the stock falling below $400 post-earnings, we’d like to see further acceleration in repurchases, as it would enhance shareholder value at these lower price levels. And based on CFO Daniel Durn’s comments, it looks like that’s exactly what Adobe plans to do:

“So if I take a step back, Keith, and you think about the last 4 quarters, we've repurchased almost $11 billion. And we've always talked about if there's opportunities to be opportunistic along the way, we would take advantage of it. And I think that's what you saw play out in Q1.”

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)