Adyen H2 2025 Review: The Underlying Business Remains Strong

The Growth Engine Decelerates, The Profit Machine Returns

The market is reacting sharply. Adyen missed revenue estimates and guided for slower growth. But disciplined investors don’t trade headlines; they focus on business fundamentals.

Below is our analysis explaining why the “PayPal fear” is misplaced and the actions taken in our portfolio.

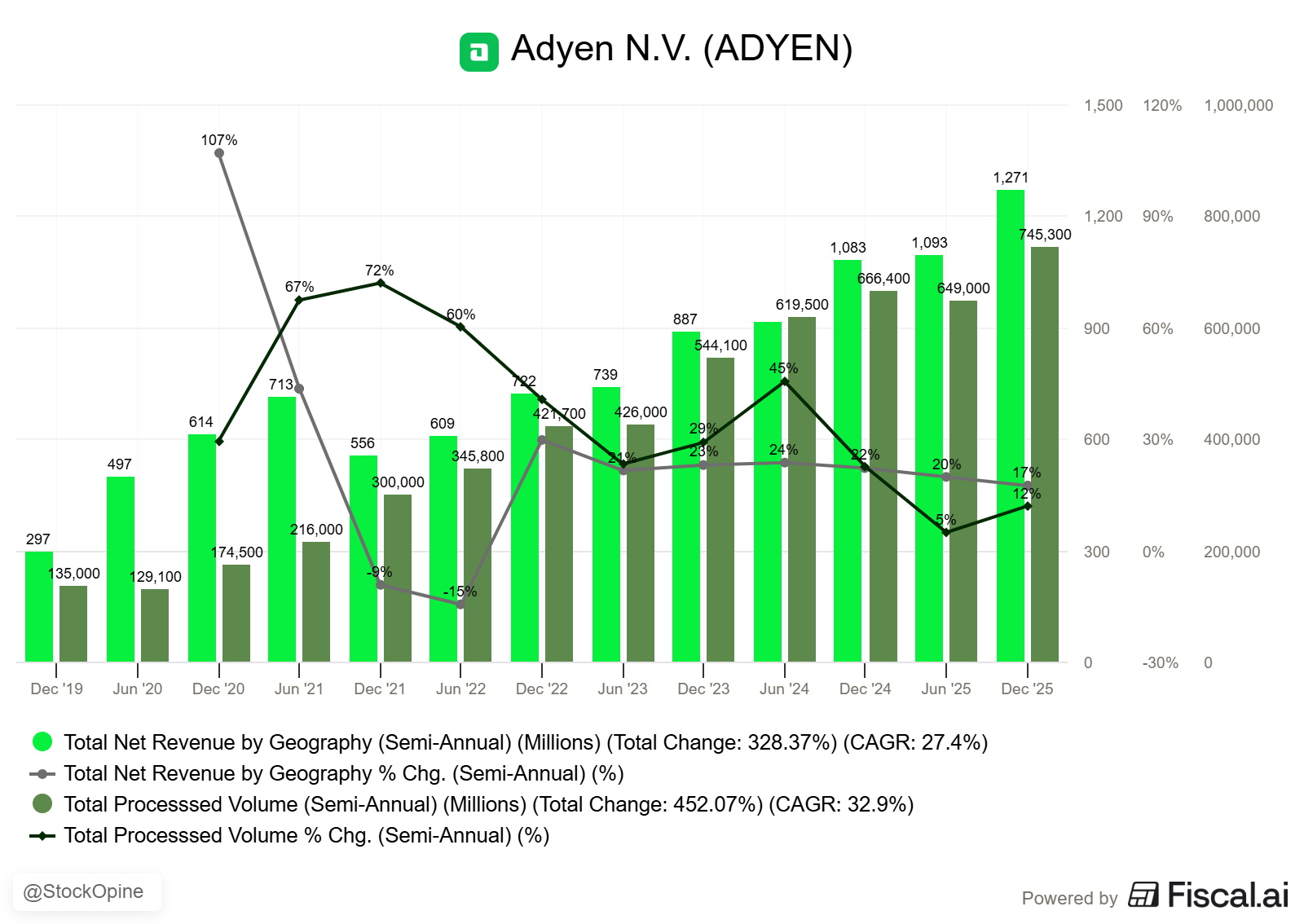

1. H2 2025 Scorecard

Net Revenue: €1.27 Billion (+17% Reported / +21% Constant Currency). Missed Consensus of €1.29B.

EBITDA: €702.1 Million (+23% YoY). Beat Consensus of €692M.

EBITDA Margin: 55%. Massive expansion of ~200 bps YoY.

Processed Volume: €745.3 Billion, up 12% (+19% YoY - excluding a single large volume customer).

EPS: €18.46 per share (+11.5% YoY).

Free Cash Flow Conversion: 86%.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

2. The “PayPal Fear” & The Take Rate Defense

The bear case today is that Adyen is becoming just another payments company like PayPal, fighting a price war it can’t win. Investors look at the Digital pillar volume (-1% reported, or +11% excluding the large customer) and compare it to Braintree’s recent +12% growth, assuming Adyen is losing share.

But if Adyen were losing a price war, their Take Rate (the cut they keep) would be collapsing. It isn’t. It’s expanding.

Digital Take Rate: Increased to 0.183% in H2 2025 (up from ~0.169% in H2 2024).

Total Take Rate: Landed at 17.1 bps, up from 16.2 bps a year ago.

This is the “anti-PayPal” signal. Adyen is effectively churning low-margin volume (likely Block’s Cash App) while winning complex, high-margin enterprise volume. The fact that Digital revenue grew 10% (Constant Currency) while volume was essentially flat proves they are extracting more value, not less.

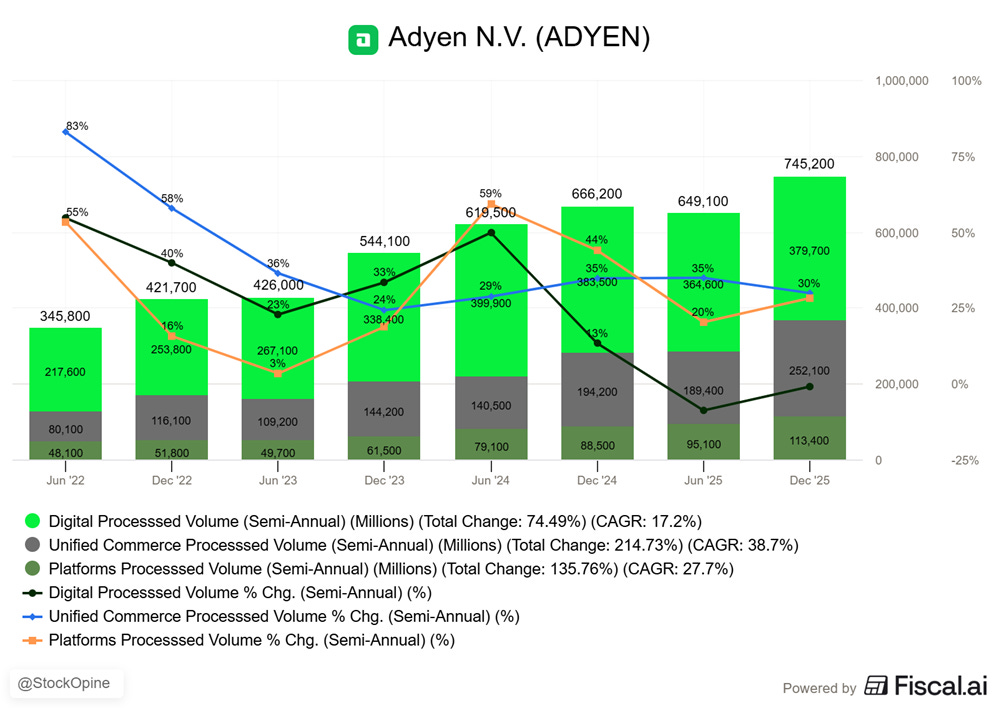

3. Dissecting the Pillars

To understand the true health of the business, we must look at the three pillars individually. The headline slowdown hides a shift towards stickier revenue.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

a. Digital: The “Optical” Weakness

Revenue: €696.1M (+10% Constant Currency, +7% reported).

Volume: -1% reported (impacted by Cash App, +11% excluding the large volume customer).

Management noted a record number of customers moving into Unified Commerce. When a Digital client opens a store, their volume often shifts pillars. This creates a “double headwind” for the Digital segment: Cash App drags the volume down, and successful upsells “steal” the growth to the Unified pillar.

However, as the CFO Ethan Tandowsky noted,

“Being able to support our customers in more sales channels means that they put more trust. We’re able to win more of their share of wallet.”

b. Unified Commerce (UC): The Crown Jewel

Revenue: €431.3M (+33% Constant Currency).

Volume: +30%.

Terminals: Adyen added 54,000 terminals in H2 alone, reaching 456k total active terminals (+92k YoY).

The ability to roll out Starbucks to 943 stores in seven weeks or expand Uber to kiosks is a moat that pure-play digital competitors cannot cross. The data supports the "omnichannel" thesis: during Black Friday (BFCM), in-store baskets were 28% higher than online ones. Adyen is capturing this market.

c. Platforms

Revenue: €143.3M (+49% Constant Currency).

Volume: +28% (or +54% excluding eBay).

While the growth looks massive, we note that the number of platforms processing >€1B dropped slightly from 32 to 31. However, the number of active business customers grew to 220k (vs 193k in H1). This suggests the drop is likely a single client falling just below the threshold due to macro factors, not a structural churn issue. Additionally, with 31% of Platforms volume now on POS (up from 25%), the stickiness of this segment is increasing.

4. Profitability: “Trust the Process” Pays Off

In 2023, Adyen crashed when they refused to stop hiring. They asked for our trust. H2 2025 is the payoff.

EBITDA Margin: Hit 55%.

The Lesson: Management shifts resources to where clients are going (Unified Commerce, Platforms) rather than chasing short-term quarterly targets.

Source: Company filings

As Ingo Uytdehaage said on the call:

“But we think that too much focus on the short term is not helping us in that long-term execution... in all the decision that we make as a management board, we only take the 3-5 years perspective and not this year’s perspective.”

We trusted them on the hiring in 22-23. We should trust them on the client strategy in 2026.