Airbnb - Earnings Review Q2’22

$ABNB reported its Q2’22 results on 2nd August 2022 where it marginally missed revenue guidance ($975k) but has beaten GAAP EPS ($0.56) by $0.13 and non-GAAP EPS ($0.73) by $0.21.

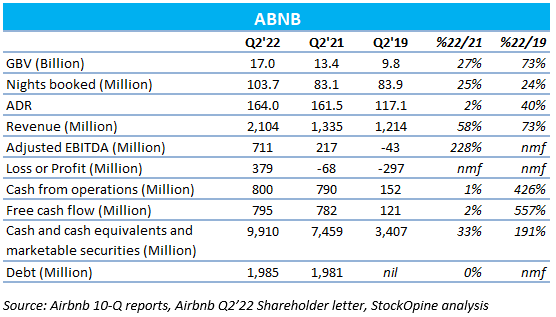

Key results

Source: Airbnb 10-Q reports, Airbnb Shareholder letters, StockOpine analysis

GBV of $17B, up 27% Y/Y and up 73% from Q2 2019. Growth driven by increase in Nights and Experiences Booked, combined with the continued strength in ADR (Average Daily Rate). Although, GBV increased on Y/Y basis, it has declined q/q from $17.2B due to a decrease in ADR.

Nights and Experiences booked a new record which surpassed 103.7m increasing 25% Y/Y and up 24% from Q2 2019 driven by North America (37%), EMEA (26%) and Latin America (64%). The only region which underperforms is Asia Pacific which was lower than Q2’2019 but at least 19% higher than prior year.

The following should also be noted: a) nearly 50% of the nights are 7 days or longer, b) active listings for the same period increased by 23% and c) all mainland Chinese listings were taken down in July but $ABNB still has over 6 million active listings.

Revenue of $2.1B, up 58% Y/Y and up by 73% from Q2 2019.

Both Net and Operating profitability demonstrate the strength of Airbnb’s model as Adjusted EBITDA (margin 34%) and Profit (margin of 18%) were higher Y/Y by $494M and $447, respectively. Although profitability is expanding the margin should not be taken as a mature margin since the company is still growing => David Stephenson, CFO added “But while we're thrilled with this margin expansion, we're heavily in growth mode. We are not in profit maximization mode. We really want to balance profitability with growth.”

The company is a cash machine generating $795M of free cash flow (38% of revenue), up from $782 million (59% of revenue) in Q2 2021 and $121 million (10% of revenue) in Q2 2019, whereas FCF over the latest 12M was $2.9B.

Brian Chesky highlighted that the main drivers of their success in improving profitability and being cash flow generating are the adaptability of the business model and the streamlining of expenses that took place during the pandemic. => “First, our business model is adaptable. We have nearly every type of space in nearly every location, so however travel changes, we are able to adapt.”

Other Call highlights

1. Share repurchase program

Brian Chesky, Co-Founder and CEO “In fact, we're so confident in our long-term growth and profitability that today, we're announcing a $2 billion share repurchase program. And this is coming only 1.5 years after our IPO.”

As per the Shareholder Letter, the program will enable the company to offset dilution from employee stock programs.

2. Long-term stays

Brian Chesky, Co-Founder and CEO “We saw long-term stays of 28 days or more remain our fastest-growing category by trip nights compared to 2019. The long-term stays has increased nearly 25% from a year ago. And actually, long-term stays have increased almost 90% since Q2 2019”.

3. Product enhancements – Airbnb Categories, AirCover for guests, I’m Flexible etc.

Brian Chesky, Co-Founder and CEO, on the below product improvements:

Airbnb Categories => “Since launch, listings in the Airbnb Categories have been viewed more than 180 million times.”

Since the release of Airbnb Categories, Airbnb has also seen the highest daily number of visitors.

AirCover for guests => “Since launch, the Net Promoter Score for guests that had an issue with their stay has already improved. And the real insulin -- instance where our host cancels, AirCover has led to 10% more rebookings.”

I’m Flexible => “I think this is a really big thing that we're going to be focusing on, and we're going to continue to be investing in this product because I think this is a bit of a paradigm shift for how people will travel.”

Hosts related => “So you're going to see some exciting new product features to recruit the next generation of host later this year.” & “We have 4 million hosts on Airbnb, and I think that millions more can turn to hosting, especially during these economic times. So that, I think, is really priority #1.”

4. Cities and non-urban stays

Brian Chesky, Co-Founder and CEO, “But we're also seeing guests returning to cities [47% of gross bookings in Q2 2022] and crossing borders above pre-pandemic levels.”

“We continue to see the strongest supply increases in areas of greatest demand, with nonurban active listings up 50% compared to Q2 2019. But as demand is returning to cities, we're also seeing an increase in total urban supply.”

5. Joe Gebbia

Brian Chesky, Co-Founder and CEO, “Last month, Joe announced that he'll be stepping back from this full-time operating role. Joe will continue to serve on the Board of Directors of both Airbnb and Airbnb.org. Airbnb is a founder-led company. So he's going to continue to take a role at Airbnb, and this will be as an adviser to me on future concepts and creative culture.”

Outlook for Q3’2022

Nights and Experiences Booked growth rate in Q3 2022 Y/Y will approximate the growth rate in Q2 2022 Y/Y, i.e., 25%.

ADR is expected to slightly increase in Q3 2022 on a Y/Y basis. Higher projected ADR in Q3 2022 combined with 25% increase in nights and experiences suggests a +25% GBV growth.

Q3 2022 revenue is expected to be the record revenue for Airbnb, i.e. between $2.78 billion and $2.88 billion, up 26.5% compared to Q3’2021 and 72% compared to Q3’2019, using the mid-point forecast. It shall be noted that revenue outlook includes a significant FX headwind.

Record Adjusted EBITDA is expected for Q3 2022 as well as a +/- margin to the all-time high of 49% in Q3 2021.

Management guidance implies high growth rates, improved profitability and above all, resilience to economic shocks. Over the call, it was indicated numerous times that Airbnb model is resilient to shocks due to the diversity of its offerings and its value proposition to guests and hosts. Its history is also there to prove it, i.e. founded during a recession, thrived in the COVID era etc.

Concluding Remarks

Satisfactory quarter with Nights and Experiences booked growing across all (almost) regions, long term stays being the fastest growing category, product innovations driving momentum across guests and hosts, exemplary profitability and potential for further upside (e.g. China outbound pent-up demand, Experiences).

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.