ABNB 0.00%↑ reported its Q3’22 results on 1st November 2022 where it met the higher end of its revenue guidance ($2.88B) and exceeded its targeted Adjusted EBITDA margin of +49% (50.5%). It has also beaten GAAP EPS by $0.29 ($1.79 Vs $1.50) and non-GAAP EPS by $0.24 ($1.79 Vs $1.55).

Key results

In the current quarter, $ABNB had a record revenue of $2.9B (up 29% or 36% ex-FX) and record net income and Adjusted EBITDA of $1.2B (up 46%) and $1.5B (up 32%), respectively.

Source: Airbnb 10-Q reports, Airbnb Shareholder letters, StockOpine analysis

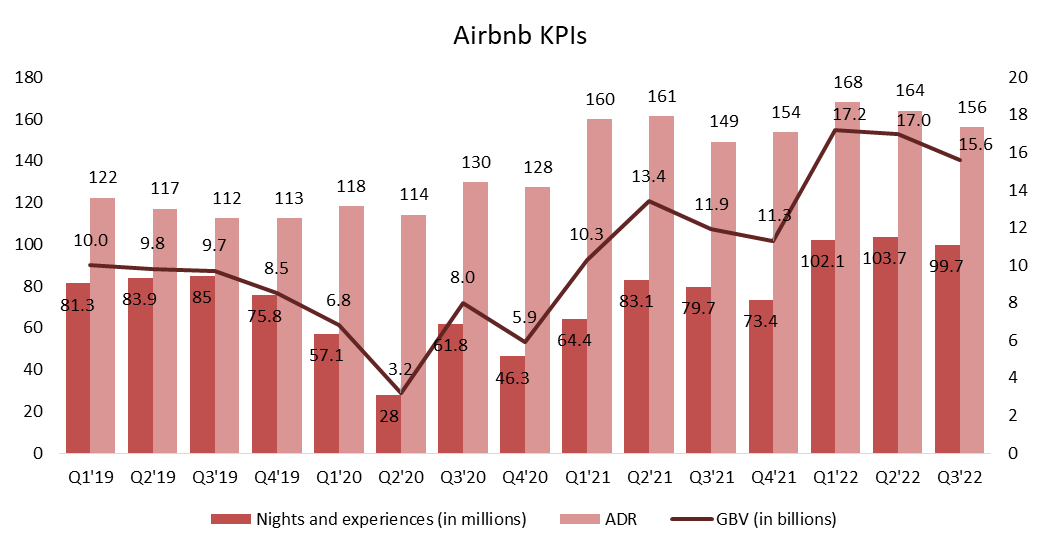

GBV of $15.6B, up 31% Y/Y (40% ex-FX) driven by increase in Nights and Experiences Booked combined with the continued strength in ADR (Average Daily Rate).

ADR of $156, 5% higher than Q3’21 (12% ex-FX) due to price appreciation offset by FX and mix changes.

Nights and Experiences booked increased by 25% Y/Y with strong growth across all regions, especially APAC (65% increase but still below pre-pandemic).

Record quarter guest arrivals exceeding 90 million.

Active listings excluding China grew by 15% in Q3’22.

Improvement in margins with Adjusted EBITDA margin of 50.5% (Vs 49.2% in Q3’21) and Profit margin of 42.1% (Vs 37.3%) driven by growth and expense discipline. One reason of margin improvement is marketing.

“We've been incredibly effective at that 90% of our traffic remains direct or unpaid which is driving a great return on investment for kind of new active bookers.” David Stephenson, CFO

The company each and every quarter proves its ability to generate cash with $960M of free cash flow (33.3% of revenue), up from $529M (23.6% of revenue) in Q3 2021. Trailing Twelve Months Free Cash Flow (“FCF”) is $3.3B (or 41.4% of revenue) whereas cash, cash equivalents, marketable securities as of September 30, 2022, stand at $9.6B compared to a Long-term debt of $2.0B.

Other highlights

1. Strong growth in # of hosts with the accelerated increase of guests in cities and potential for a further increase

Statement on Shareholder letter “we’re seeing strong growth in the number of new Hosts on Airbnb. Just like during the Great Recession in 2008 when Airbnb started, people are especially interested in earning extra income through hosting. That’s why on November 16, we’re introducing an all-new, super easy way for millions of people to Airbnb their homes as part of our 2022 Winter Release”

“We’re also delivering a major upgrade to AirCover that provides even more top-to-bottom protection for every Host on Airbnb.” Brian Chesky, Co-Founder and CEO

2. Long-term stays

Long term stays of +28 days remain strong at 20% of gross nights booked (stable) despite the return to office trend with Asia Pacific showing an uptick in popularity. +7 days accounted for 45% of gross nights booked.

3. Cities and cross border – mix changes but still growing strong

Cross border gross nights booked increased 58% and high-density urban (cities) nights booked grew by 27% Y/Y. In Q3 2022, high-density urban nights booked was 48% of total gross nights booked (Vs 58% in Q3 2019) and cross-border was 43% (Vs 33% in Q3’21 & 48% in Q3’19).

“As the impact of the pandemic recedes but macro conditions persist, we expect a continued, albeit choppy, recovery of cross-border travel to be a further tailwind to future results.”

4. Share repurchase program

$1B out of the authorized $2B announced last quarter were utilized -> the program will enable the company to offset dilution from employee stock programs.

5. On Airbnb categories introduced on May 11

Brian Chesky, Co-Founder and CEO, “Again, we're already seeing people discover homes they never knew existed. We're seeing a lot more people engage with categories. The homes and categories have been viewed more than 300 million times, we're going to continue to be making improvements to this every single year.”

300M compares well to the number of 180M disclosed in Q2’22 earnings release (2nd August) as the whole point is “pointing demand where we have supply, bringing us top of funnel” and thus resulting to a better conversion.

6. Finally Airbnb plans to redesign (not change) pricing policy!

Brian Chesky, Co-Founder and CEO, “And so we are working on redesigning how pricing works on Airbnb, so people better understand the total price they're going to pay the moment they arrive at Airbnb, and it's not a surprise to them.”

Not knowing the total price in advance and getting a cleaning fee and a service fee as a ‘surprise’ was never the best experience for us.

Outlook for Q4’2022

Nights and Experiences Booked growth rate “will moderate slightly” in Q4 2022 relative to Q3’22 growth. What could that mean? We go for 20% growth Vs 25% in Q3’22. On another note, as at the end of Q3’22 there are $1.2B Unearned Fees (Vs $892M in Q3’21).

ADR “will face some pressure from FX headwinds and business mix”. We go for 5% decline Y/Y reaching an ADR of c. $146 and a resulting GBV growth of 13.8%.

Q4’22 revenue is expected to be between $1.8B and $1.88B, up 20.1% compared to Q4’2021 using the mid-point forecast. Revenue outlook includes a significant FX headwind of c. 6%.

Adjusted EBITDA will increase relative to Q4 2022 and margin to be “modestly higher than last year’s margin of 22%”.

Q4 guidance may have left investors buzzled but we do not think that it’s so bad to justify the recent drop in price. The growth rates are reasonable and improved profitability is always a plus.

Based on Q4 guidance, revenue will most likely close higher (at $8.34B) compared to $8.23B estimates when we run our initial valuation. Additionally, based on our calculations, a +100bps positive impact on EBITDA margin is expected and a lower Stock Based Compensation than initially anticipated (in our valuation).

Regarding 2023, David Stephenson, CFO disclosed that potential moderation in ADRs does put pressure on FCF margins but “improvements in our variable costs and the fixed cost leverage should enable us to maintain or even increase free cash flow margins over the longer term.”

Concluding Remarks

A decent quarter, meeting or beating guidance across key metrics. Airbnb business model remains strong* and despite the potential short-term macro and FX headwinds, our thesis remains intact. The improved profitability along with the potential increase in Nights and Experiences booked in the APAC region were few of the reasons why we added another 1.5% to our portfolio.

* “We're in 100,000 cities all over the world. We're not just a vacation rental business. We're also an urban business, also a cross-border business. We're not just a family business. We're also popular with millennials, Gen Z and retirees at nearly every type of price point. So I think that however travel demand changes, we'll be able to adapt.” Brian Chesky, Co-Founder and CEO

You can find us at Commonstock and on Twitter @StockOpine.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward-looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

This post may contain affiliate links, which means that we might get a commission if you decide to sign-up using any of these links. No extra cost is charged to you.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.