In this release, we will break down Alphabet’s GOOGL 0.00%↑ ROE using the 5-step DuPont analysis.

Return on Equity measures the profitability that is generated for shareholders and is one of the fundamental ratios used by investors. Ultimately if ROE is higher than cost of equity, management is creating value for the shareholders.

A higher or increasing ROE demonstrates the efficiency of the company in converting shareholder equity financing into profits.

The formula of ROE is =>

Even though the ROE is a backward looking metric one should not ignore that ROE multiplied by the retention ratio leads to the Sustainable Growth Rate, which is the maximum growth rate a company can sustain using only internally generated profits.

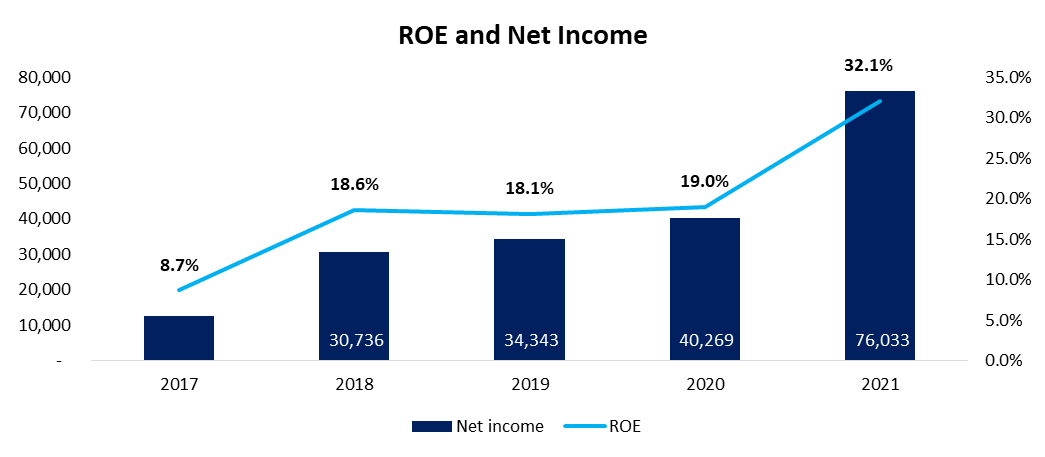

1. Alphabet’s reported ROE and Net income evolution:

Source: 10K reports, StockOpine analysis

2. ROE DuPont 5-step formula:

3. ROE analysis:

Source: 10K reports, StockOpine analysis

ROE: Alphabet’s ROE seems to be improving since 2017, increasing its ROE from 8.7% in 2017 to 32.1% in 2021.

The Net profit margin of Alphabet was relatively constant over the years 2018-2020, except for years 2017 and 2021. In 2017, the net profit margin was 11.4% because of one-off tax burden (53% effective tax rate) whereas in 2021, net profit margin increased to 29,5% mainly due to operating margin improvement.

Operating margin: Operating margin was in a declining trend from 2017 until 2019 (2020 was similar to 2019) mainly due to a contraction of the Gross Profit Margin (GPM) which decreased from 58.9% in 2017 to 55.6% in 2019. The reason for the decline in GPM was the change in revenue mix and increased investments in data center expenses, content acquisition costs and hardware costs. Revenue mix shifted from Google Search towards other segments such as Google Cloud, Google Play, hardware products and YouTube. The margins of those businesses vary significantly, and we presume that they have lower margins than Google Search business. We have elaborated in more detail about Alphabet’s Gross Profit Margin in a previous post in Commonstock.

Source: 10K reports, StockOpine analysis

Source: 10K reports, StockOpine analysis

In 2021, $GOOGL ‘s operating profit margin improved by 8 percentage points to 30.6% relative to 22.6% in 2020, mainly due to Google Search increased revenue share, improved operating loss margin of Google Cloud (see graph below) and a reduction in the depreciation expense as a result of a change in the estimated life of servers and other network equipment. It shall be noted, that during 2021 revenue grew by 41% while operating expenses increased by 20%, primarily driven by headcount growth of 16%.

Overall, we believe that the deterioration in operating margins from 2017 to 2020 was driven by investments in product offerings which are at an earlier stage of their life cycle (Cloud, Other bets, YouTube) rather than competition pressures.

As Google Cloud continues to move towards positive profitability and as Google Search gains share over Google network member properties, we can expect further operating margin improvement.

Source: 10K reports, StockOpine analysis

Interest burden is meant to account for the burden from net interest expense/income, however, in order to normalize operating margins we also included EU fines, debt & equity security gains/losses and other charges. This factor has gradually increased over 1 during the period indicating that non-operating income exceeds interest expenses. The gains on debt and equity securities for the period 2017-2021 of c. $28B far outweighed EU fines of c. $9.5B.

Tax burden was relatively constant except in 2017 when the Tax Act was enacted and resulted in a one-time transition tax on accumulated foreign subsidiary earnings.

Asset turnover was fairly stable during 2017-2020, however, in 2021 the asset efficiency improved as a result of the 41% revenue growth compared to the 14% growth in average total assets, indicating the Company’s ability to generate marginal revenues with lower incremental investments in its total assets.

The final component of the ROE formula is the Financial Leverage which has a positive effect on the ROE of Alphabet as it increased from 1.25 in 2017 to 1.43 in 2021. Taking excessive leverage could increase risk of default, however, no such threat exists for Alphabet. As of 31 December 2021, Alphabet’s cash and marketable securities amounted to $140B ($125B as at 30 June 2022) while long term debt was only $15B (unchanged as at 30 June 2022) resulting in positive net interest for the year.

4. Concluding remarks:

Alphabet consistently improved its ROE while at the same time was investing in loss making segments such as Google Cloud and Other Bets. We did not identify any signs of margin compression as a result of competition forces indicating Alphabet’s strong competitive positioning. In addition, we believe that ROE is not optimized yet and has further room for improvement as Google Cloud moves towards profitability.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.