Alphabet's Q2’25: Firing on All Cylinders

Search Accelerates, Gemini Gains Momentum, Cloud's Stellar Quarter

Alphabet reported Q2 2025 and it was a strong quarter across the board. The company beat expectations on revenue and earnings, with growth accelerating in all its key segments

Revenue: $96.4B (up 14% YoY), Vs estimates of $94B.

EPS: $2.31 (up 19% YoY), Vs estimates $2.20.

This quarter provided clear signs that Alphabet's AI strategy is paying off, strengthening its core businesses like Search, YouTube, and Cloud.

Let's dive into the details.

But first, a word from our sponsor - Quiver Quantitative!

Trade Like an Insider With Quiver Quantitative

Make smarter trading decisions with Quiver’s next-generation stock research platform. We bring you data from government trades, corporate lobbying, insider transactions, and more. For a limited time, use promo code YT2025 at checkout for a 50% discount on your first year.

Now, back to the earnings.

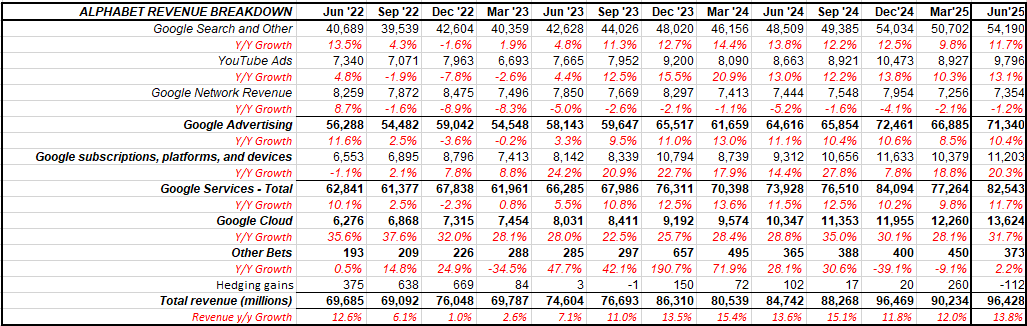

Revenue

At a high level, Alphabet’s 14% (13% on constant currency) revenue growth was a significant acceleration, driven by double-digit growth in Search, YouTube, Subscriptions, and a monster quarter from Google Cloud.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers), StockOpine Analysis

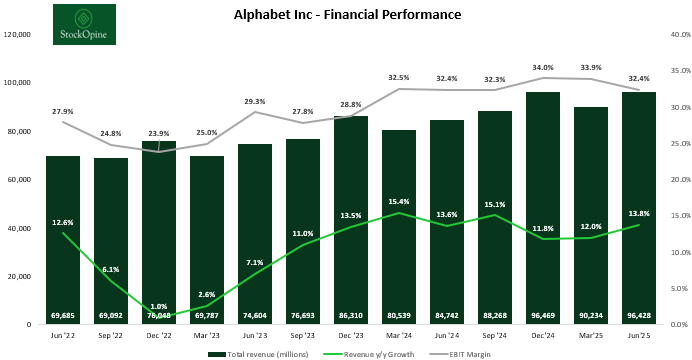

Profitability

Operating income climbed to $31.2 billion, but the operating margin was flat year-over-year at 32.4%. At first glance, you might expect some margin expansion with such strong top-line growth. However, two key items weighed on the numbers: a hefty $1.4 billion legal charge and increased depreciation from the company's aggressive CAPEX investments in AI infrastructure.

If we adjust for that one-time legal charge, the operating margin would have been 33.9%, showing that the underlying profitability of the business remains strong and in line with the prior quarter.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers), StockOpine Analysis

Google Search

The narrative that AI chatbots would divert away Google search queries has been a major overhang on the stock. We believe this quarter’s results challenge that thesis.

Search revenue growth accelerated to 11.7%, driven by strength in the retail and financial services verticals.

So, what’s going on? It seems the pie is getting bigger for everyone. As CEO Sundar Pichai noted on the call:

"Overall queries and commercial queries on Search continue to grow year-over-year."

It is possible that AI chatbots are often used for new, incremental queries rather than just replacing traditional searches. Furthermore, Google's own AI integrations are proving to be successfull in keeping users within its ecosystem and expanding Search's capabilities:

AI Overviews now reach over 2 billion monthly users (up from 1.5 billion last quarter). AI Overviews are now driving over 10% more queries globally for the types of queries that show them, indicating that users are adopting to AI Overviews.

AI Mode continues to receive positive feedback for more complex questions, and already has over 100 million monthly active users.

Google Lens visual searches grew an incredible 70% year-over-year.

Circle to Search is now on over 300 million Android devices (up from 250 million devices in last quarter).

New Agentic Capabilities are being integrated directly into Search, such as AI-powered calling to local businesses for U.S. users.

Virtual Try-On for clothing was launched in Search Labs, allowing users to try on billions of products virtually, with very positive early engagement from Gen Z users.

YouTube

YouTube had a great quarter with ad revenue growing 13.1% to $9.8 billion. The broader "Subscriptions, Platforms, and Devices" segment grew an impressive 20%, and management cited YouTube's subscription offerings as a primary driver of revenue growth. This indicates that services like YouTube Premium and YouTube TV continue to grow at a very healthy rate.

On top of that, Shorts monetization continues to improve:

“In the U.S., shorts now earn as much revenue per watch hour as traditional in-stream on YouTube. And in some countries, it now even exceeds in-stream's rate.”

With Shorts hitting 200 billion daily views, achieving monetization parity unlocks a sustainable growth driver for the years ahead.

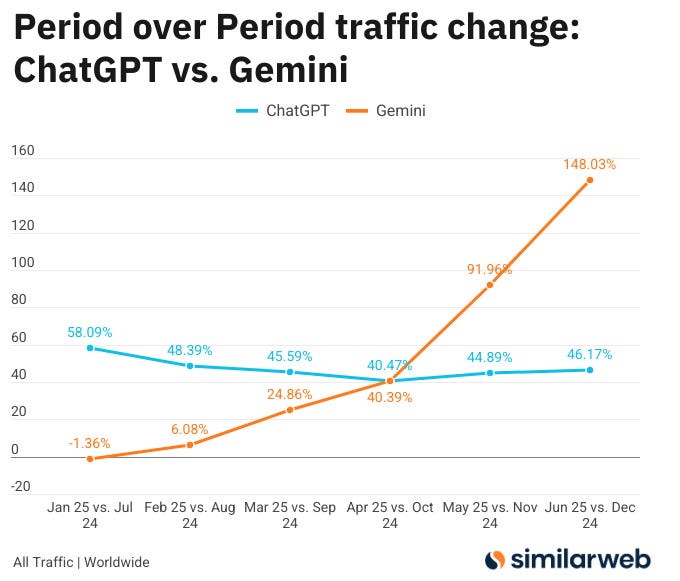

Gemini App

While ChatGPT remains the market leader in user numbers, the momentum is clearly shifting. In March, court filings revealed Gemini had 350 million monthly active users. Just three months later, that number has surged by nearly 30% to 450 million.

Even more telling is the engagement: daily requests on the app grew by over 50% since Q1. This shows that users are using the Gemini app more frequently. This engagement is also translating into revenue, as the recent launch of Google AI Pro and Ultra tiers has boosted subscriptions for Google One.

Data from Similarweb confirms this trend, showing Gemini's web traffic growth has been outpacing ChatGPT's significantly over the past six months.

Furthermore, the viral success of new features such as Veo 3 is a powerful catalyst for growth. Management noted that the video-generation model Veo 3 went viral with people sharing clips created in Gemini app, with over 70 million videos generated since May. This kind of excitement is exactly what drives users to upgrade to paid AI subscriptions.

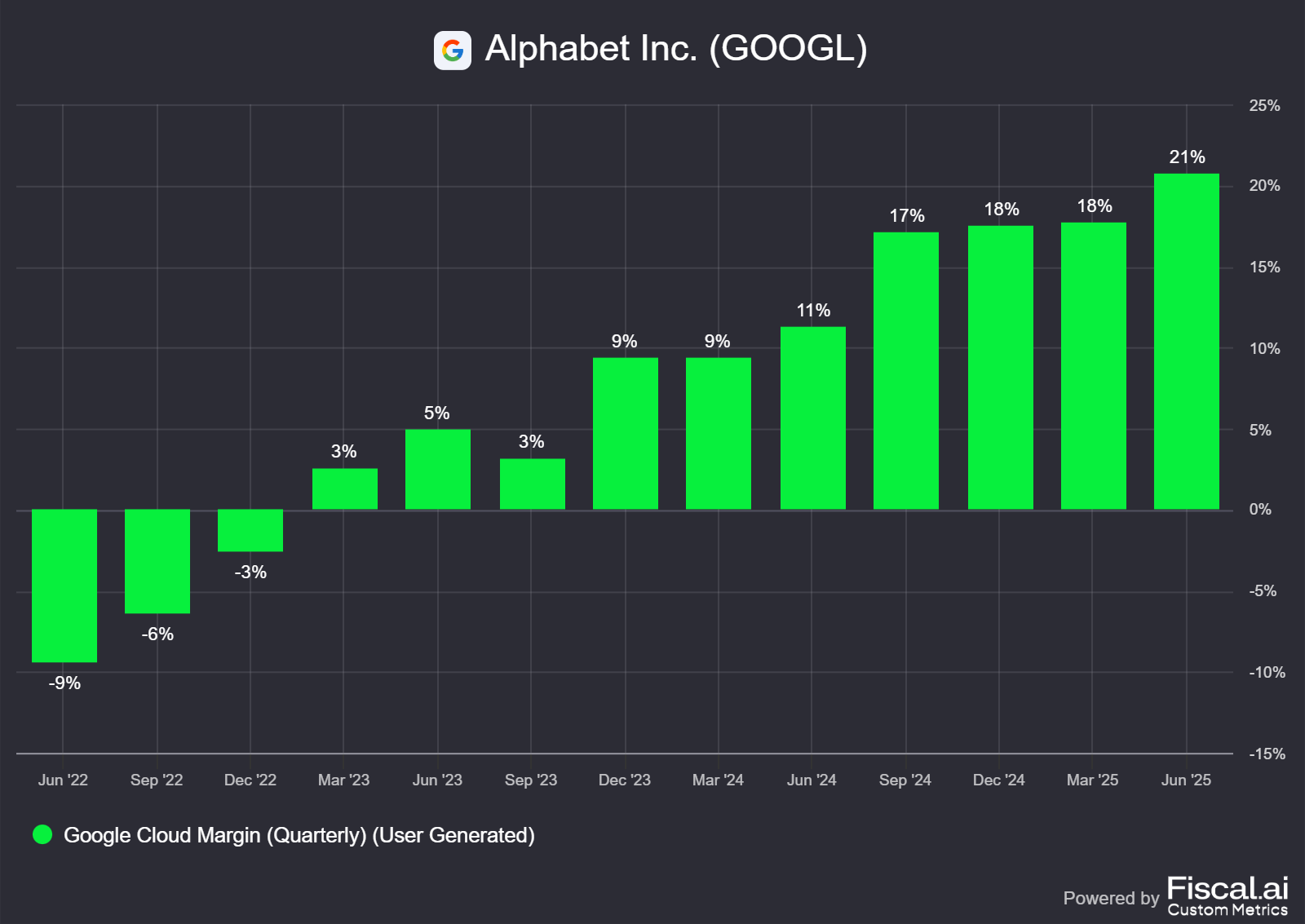

Google Cloud

Google Cloud was the north star of the quarter, with revenue growth accelerating to 32%, hitting an incredible $54 billion annual run-rate. Adding to the story, management highlighted accelerating momentum with large customers: contracts over $250 million doubled year-over-year, the number of new GCP customers increased by nearly 28% quarter-over-quarter, and impressively, they signed as many deals over $1 billion in the first half of 2025 as they did in all of 2024.

What's even more impressive is the profitability. Operating margin for Cloud hit 20.7%, up from just 11.3% a year ago.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Furthermore, management noted that nearly all GenAI unicorns use Google Cloud, suggesting a competitive edge from its AI infrastructure, including its AI-optimized data centers and TPUs.

“We operate the leading global network of AI-optimized data centers and cloud regions. We also offer the industry's widest range of TPUs and GPUs along with storage and software built on top. That's why nearly all GenAI unicorns use Google Cloud.”

Additionally, Google Cloud's backlog surged 38% to $106 billion, and management confirmed they are still supply-constrained. This should explain the decision to hike the full-year CAPEX outlook from $75 billion to $85 billion, with management signaling that spending will increase even more in FY26. They aren't just spending money; they are racing to build the infrastructure to meet demand.

Conclusion

This was a strong quarter for Alphabet. Underpinning all of this is the sheer scale of AI adoption across the ecosystem. Management revealed they are now processing over 980 trillion monthly tokens—more than double the number from just a few months ago. This explosive growth in usage is an indication that their massive AI investments are translating into real-world engagement.

Search and YouTube revenues are growing, as are Search queries, while Gemini is rapidly gaining ground and Google Cloud is cementing itself as the go-to platform for the AI revolution.

From a valuation perspective, the stock has had a great run over the last month and, in our opinion, is no longer trading at a significant discount to its intrinsic value. It currently trades at an EV/EBIT multiple of around 18.3x, which is below its 10-year average of 22x but up from the lows of approximately 15x we saw in May. As Alphabet is already our largest position, we are not looking to add here, but this quarter gives us confidence in the long-term thesis.

If you want to dive deeper into our valuation for Alphabet, we recommend reading our two previous reports which remain highly relevant today: