In this article, we evaluate Amazon’s performance for Q1 2025 and conclude with an updated valuation to assess whether the current price presents an attractive entry point. Despite recent volatility, Amazon’s stock jumped 8% on May 12, 2025, following the announcement of a 90-day pause on proposed US-China tariff increases, a move that eased investor concerns over global trade tensions. Even with this rally, the stock remains down 4.2% year-to-date, reflecting earlier pressure and uncertainty from tariffs.

This was a generally strong quarter, with AWS and Advertising showing solid momentum, while AI-related capex investments continued at a steady, anticipated pace.

Let’s unpack it.

Got 1–2 minutes? Help us improve StockOpine by taking this quick survey.

1. Performance

a. High level results

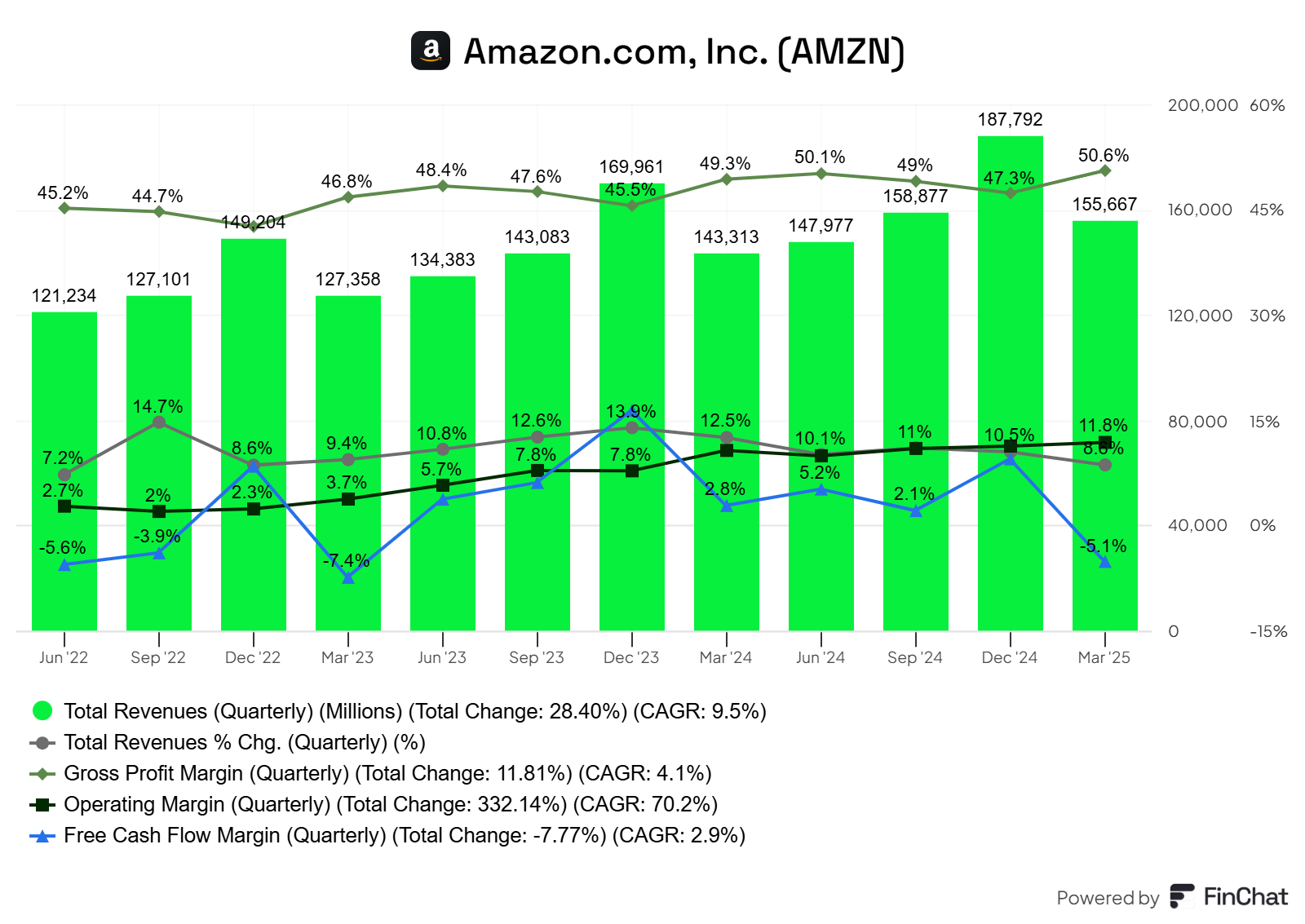

Q1’25 revenues reached $155.7 billion, surpassing the high end of guidance ($155.5 billion) and the consensus estimate ($155.12 billion), representing 9% year-over-year growth.

Q1’25 operating income was $18.4 billion (margin of 11.8%), exceeding the high end of guidance ($18 billion) and the consensus estimate ($17.4 billion). This marks a 20% increase from $15.3 billion in Q1’24 (margin of 10.7%).

Q1’25 EPS came in at $1.59, beating the consensus estimate of $1.36 and increasing 62% from $0.98 in Q1’24. Excluding the $3.3 billion gain from the conversion of a portion of Amazon's convertible notes into non-voting preferred stock in Anthropic, EPS would be $1.28, below the consensus estimate.

Free cash flow (TTM) totaled $25.9 billion, down from $50.1 billion in the TTM ending Q1’24, despite a $14.75 billion increase in operating cash flow.

The decline was driven by a sharp rise in capital expenditures, which increased from $53.4 billion (TTM as of Q1’24) — including $14.9 billion in Q1’24 — to $93.1 billion (TTM), directed toward AWS infrastructure, including data centers, custom chips like Trainium, and broader technology infrastructure to support AI and cloud growth.

This resulted in negative free cash flow of $8 billion for the quarter.

Operating cashflow was up by 15% reaching $113.9 billion on a TTM basis.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

b. Segmental analysis

North America

Amazon’s North America segment reported $92.9B in net sales (+8% YoY) and $5.8B in operating income (+16% YoY), with the operating margin expanding to 6.3%, up from 5.8% in Q1 2024. Excluding one-time charges from forward inventory purchases (to mitigate tariff risks), the margin would have reached 7.3%.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

Performance was fueled by higher unit volumes across first- and third-party sales, along with strength in advertising and subscription services. Amazon attributes this to its continued focus on price, selection, and convenience. The regionalization of its fulfillment network into regional hubs helped deliver faster Prime deliveries, often in fewer packages and at lower costs, contributing to record delivery speeds for Prime members.

Amazon also highlighted progress in adding automation and robotics to their facilities, and commitment to expand delivery stations in rural areas to better serve them. All this will result to better delivery speeds, cost efficiencies and potentially better margins.

Beyond the product range expansion, including partnerships with brands like Oura Rings and Michael Kors, and the launch of a luxury shopping experience with Saks, a standout highlight was the robust growth in everyday essentials, which grew more than twice as fast as the rest of the business and represented 1 in every 3 units sold in the US on Amazon. Amazon is one of the largest grocers in the US.

This strengthens Amazon’s relevance across both premium and day-to-day shopping categories.

Regarding tariff uncertainty, Amazon hasn’t observed a meaningful increase in average selling prices, helped by forward-buying from both its first-party business and third-party sellers. With hundreds of millions of SKUs and 2M+ global sellers, Amazon is well-positioned to offer competitive pricing and navigate supply chain challenges. Meanwhile, the recent 90-day tariff reductions from 125% to 10% by both the US (plus a 20% fentanyl-specific tariff) and China should further ease pressure.

International

The International segment delivered net sales of $33.5 billion, up 5% YoY, or 8% excluding a ~$1 billion FX headwind. Operating income increased to $1.0 billion (from $0.9 billion in Q1 2024), with a margin of 3.0%. Excluding the impact of forward inventory build-up, margins would have been 3.7%, up from 2.8% a year ago. Growth was supported by higher unit volumes, advertising strength, and improved cost efficiency, indicating steady progress towards sustainable profitability.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

Advertising: Gaining Momentum

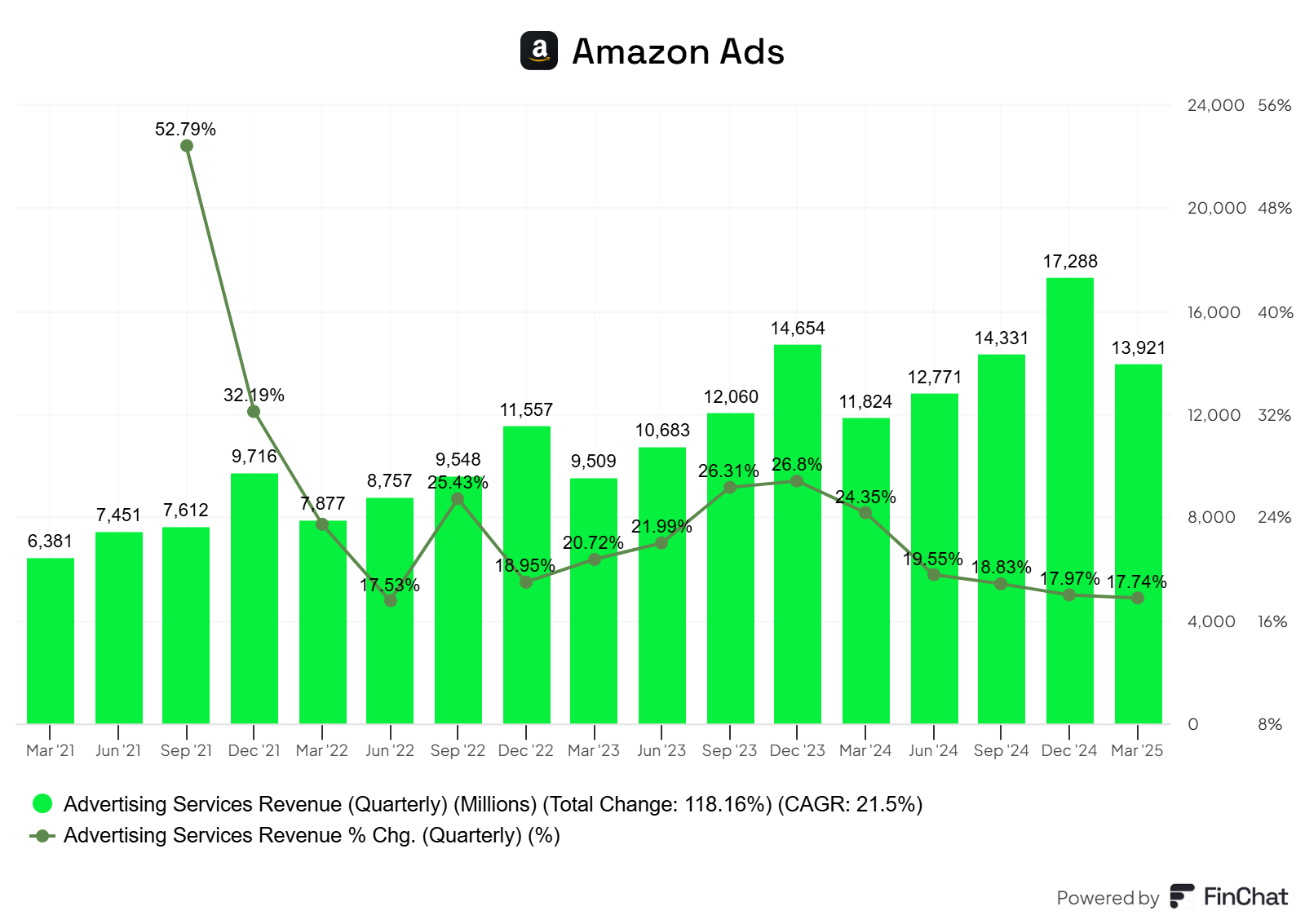

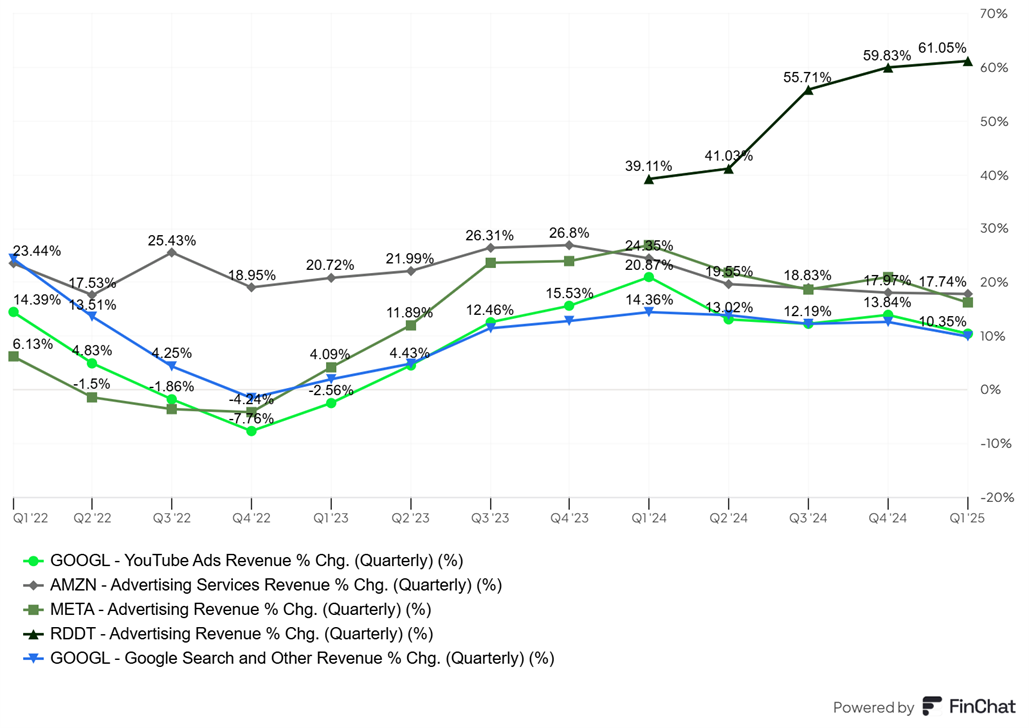

Amazon’s advertising business continues to scale impressively, generating $13.9 billion in Q1 2025, up 18% YoY which outpaced Meta’s advertising growth (+16.2%) and far exceeded Google Search (+9.9%) and YouTube ads (+10.3%), though Reddit’s 61% surge comes off a much smaller base (~40x smaller).

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

Strength remains broad-based across Amazon’s full-funnel ad offerings, reaching 275M+ ad-supported users in the U.S. alone. Ads run not only in Amazon’s online store but across its media ecosystem, including Prime Video, Twitch, IMDb, Amazon Music, and live sports (NFL, NBA, NASCAR), as well as external platforms via Amazon DSP, such as Pinterest and BuzzFeed.

Additionally, Amazon’s recent feature launches, ‘Interests’ and ‘Buy for Me,’ are further deepening user engagement and boosting the effectiveness of its advertising platform. ‘Interests’ uses AI to surface personalized product recommendations based on browsing behavior, making product discovery more intuitive and tailored. Meanwhile, ‘Buy for Me’ allows users to purchase products from third-party brand websites directly through Amazon’s app, even if Amazon doesn’t carry the item itself.

This reinforces Amazon as the default starting point for product searches. By enabling seamless transactions beyond its own inventory, Amazon increases the utility of its platform and keeps customers within its ecosystem. Consequently, it is more likely shoppers won’t look elsewhere, which in turn makes Amazon an even more attractive platform for advertisers. If brands know customers are sticking to Amazon for both discovery and purchase, the incentive to invest more ad dollars on Amazon only grows.

Advertising is a high-margin business with a long growth runway, and its accelerating momentum allows it to offset thinner retail margins while funding investments in logistics and customer experience.

AWS: The Growth and Profitability Engine

In Q1 2025, AWS net sales rose 17% year-over-year to $29.3 billion, reaching an annualized revenue run rate of $117 billion. While this growth lags behind Alphabet’s GCP at 28% ($12.3 billion) and Microsoft Azure’s 33%, AWS operates from a much larger base.

That being said, AWS operating income jumped 22.6% to $11.5 billion, driven in part by payroll cost savings and despite significant infrastructure investments. This translated into an operating margin of nearly 40% (moderation may be observed in subsequent quarters as the investment cycle progresses). The strong financial results reflect not only revenue growth but also efficiency gains from improved server capacity, custom low-cost networking gear, and better power usage in data centers.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

While growth trails peers, the $12 billion increase in backlog (or 20%) to $189 billion, maturing over 4.1 years, demonstrates a significant growth runway. This is further supported by major client wins such as Adobe, Uber, and Nasdaq.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

An interesting stat shared by management on AI is that Amazon’s AI business is already generating multi-billion-dollar annual revenues with triple-digit year-over-year growth. CEO Andy Jassy highlighted its potential:

“Before this generation of AI, we thought AWS had the chance to ultimately be a multi-hundred billion dollar revenue run rate business. We now think it could be even larger.”

Amazon is investing aggressively in AI across all operations, developing over 1,000 AI applications, enhancing Alexa to Alexa+, and integrating AI into its fulfillment networks. On Alexa+, Jassy mentioned the following to give a glimpse into its agentic use case:

“She asked me if she wanted me to make a reservation. I said yes. And she made the reservation and confirmed the time, like that. When you get into those types of routines and you have those types of experiences, they’re very, very useful. It is really like having a great personal assistant, which most people in the world don't have.”

Key to its growth strategy are AWS’s custom AI chips like Trainium2, and AI services including Amazon Bedrock, which offers various foundation models, and Amazon Nova, focused on advanced speech and action-oriented AI. Demand for these services currently outpaces capacity, but new infrastructure, including next-gen NVIDIA instances, is planned to boost capacity in coming months, supporting accelerated AWS growth.

Looking ahead, Jassy emphasizes the vast untapped opportunity: over 85% of global IT spending remains on-premises, signaling a multi-decade expansion.

Got 1–2 minutes? Help us improve StockOpine by taking this quick survey.

Outlook

Management estimates net sales of $159–164 billion (up 7–11% YoY) and operating income between $13 billion and $17.5 billion, a slight 3.7% increase at the midpoint versus last year.

Q2 operating margin is expected to decline to 9.4% from 11.8% in Q1’25 and 9.9% in Q2’24, partly due to Kuiper launch costs and stock-based compensation timing.

We believe that was enough to remind everyone what happened in Amazon’s first quarter and to give a sense of what lies ahead. With that, we’re moving on to its valuation, which is reserved exclusively for paid subscribers.