AMD Q1’25: Beats Expectations, Navigates China Challenges

Earnings beat, AI momentum, Export controls, Market share gains in Data Center and PC

AMD reported a robust start to 2025, with its first-quarter earnings surpassing analyst expectations for both revenue and profitability. However, new export restrictions clouded the outlook, weighing on stock sentiment.

The company showcased significant year-over-year growth, primarily fueled by the strong performance of its Data Center and Client segments, driven by demand for its Instinct AI accelerators, EPYC server processors, and Ryzen CPUs.

1. Results

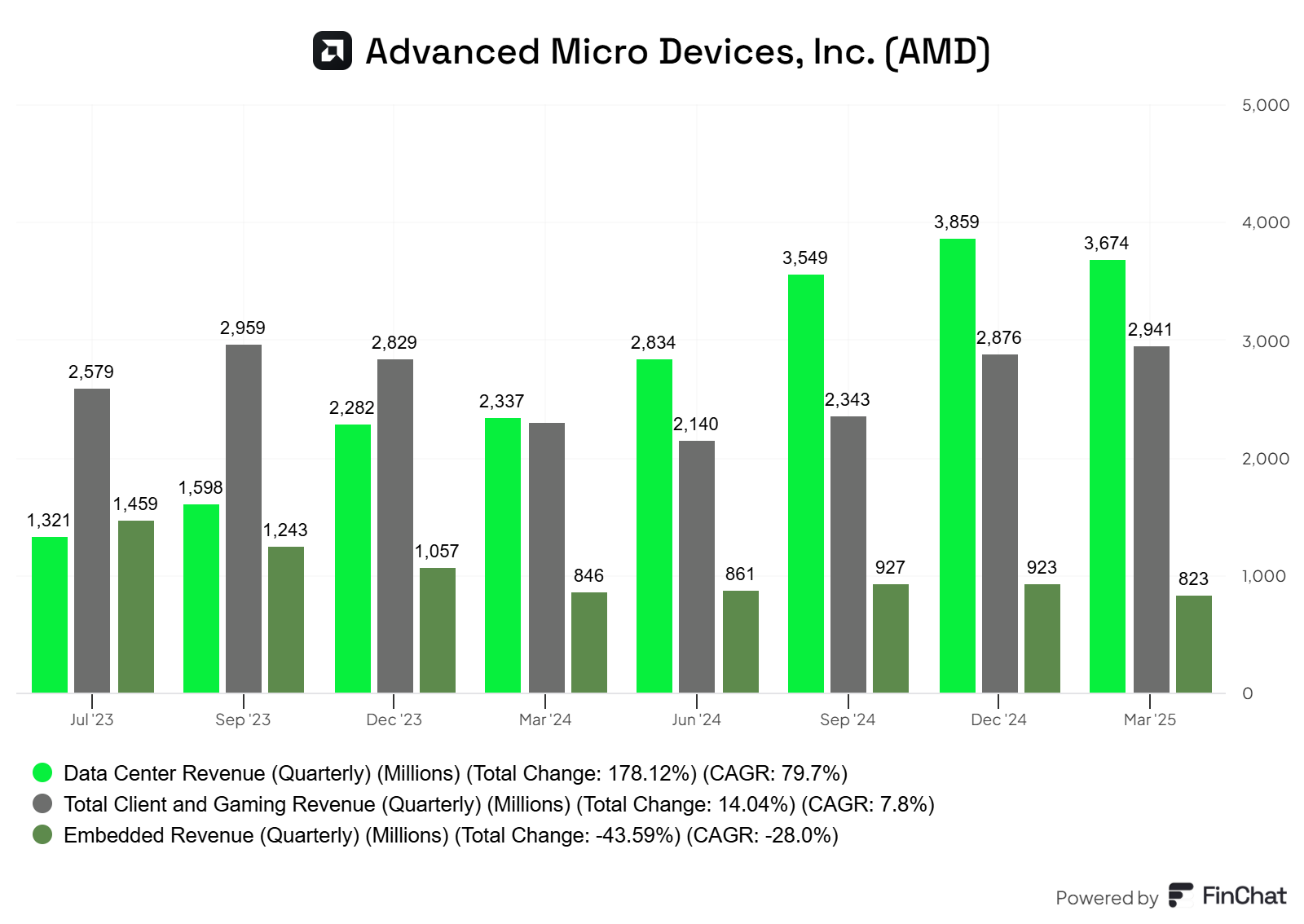

Revenue for the year increased 36% YoY to $7.44 billion, outperforming the consensus estimate of $7.12 billion. Non-GAAP EPS of $0.96, up 55% YoY and exceeding analysts' projections of $0.93.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

Gross margin expanded to 54%, an increase of 140 basis points YoY. Non-GAAP operating income was $1.78 billion, translating to an operating margin of 24%. This improved profitability was attributed to a higher mix of Data Center sales and a higher mix of Ryzen processors in the Client segment.

2. Segments

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

a. Data Center

The Data Center segment was a key growth engine, with revenue surging 57% YoY to $3.7 billion. This growth was driven by Instinct Accelerators and gains in server CPU share with the ramp-up of the latest 5th Gen EPYC Turin processors.

Sequentially, however, Data Center revenue saw a slight decrease of 5% due to the strong last year ramp-up demand from MI300X GPUs. Management expects demand to ramp up in the second half of the year with the launch of MI350.

Operating income for this segment was $932 million, or 25% of revenue compared to 23.1% in prior year.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

EPYC Processors

EPYC CPU sales experienced a large double-digit percentage growth YoY for the seventh consecutive quarter. Continued CPU server share gains across both cloud and enterprise customers driven by the ramp of AMD's latest fifth-gen EPYC Turin processors. Management highlighted that the new 5th Gen EPYC Turin processors are seen as delivering unmatched performance, efficiency, and TCO.

Hyperscaler demand remained strong, with cloud providers like Alibaba, AWS, Google, Oracle, and Tencent expanding EPYC deployments.

Enterprise adoption also saw robust growth, with the number of EPYC-powered cloud instances activated by Forbes 2000 enterprise customers more than doubling year-over-year. AMD expects enterprise adoption to accelerate further as over 150 Turin platforms become available from partners like Dell, Cisco, HPE, Lenovo, and Super Micro.

Looking ahead, AMD passed key milestones in April to begin manufacturing 5th Gen EPYC at TSMC's new Arizona fab, with initial shipments expected in the second half of 2025. The next-generation "Venice" EPYC processors, based on TSMC's 2-nanometer process, are expected to be launched in 2026.

Instinct accelerators

Revenue from Data Center AI, primarily Instinct accelerators, grew by a significant double-digit percentage YoY, as MI325X shipments ramped up for new enterprise and cloud deployments. Management mentioned that Data Center GPU performed in line with or slightly better than expected in Q1.

Several hyperscalers expanded their use of Instinct accelerators for generative AI search, ranking, and recommendation use cases.

AMD highlighted the industry-leading memory capacity and bandwidth of its Instinct portfolio making ideal for inference of large-scale AI models and is working with customers to scale deployments from single-node to distributed inferencing clusters.

Additionally, training engagements and sovereign AI deployments also ramped in the quarter.

“Training engagements also ramped in the quarter as multiple Tier 1 hyperscale, AI and enterprise customers scaled Instinct GPU clusters to train internal and frontier models. In parallel, we're making meaningful progress with sovereign AI deployments as countries expand investments to establish domestic nation-scale AI infrastructure. In February, we announced a strategic partnership with G42 to build one of France's most powerful AI compute facilities powered by Instinct accelerators.” Lisa Su

MI350 series remain on track to begin accelerated production by midyear and customer interest is very strong and will enable broad deployment in the second half of the year.

“MI350 Series performance is very strong based on the advances in our CDNA 4 architecture. We designed CDNA 4 to deliver leadership performance across a wide range of AI workloads, increasing memory capacity and bandwidth 1.5x, adding support for new data types and improving network efficiency to deliver 35x higher throughput and performance compared to MI300x.” Lisa Su

Regarding MI400, management highlighted that it remains on track for launch next year.

ZT Systems

AMD completed the acquisition of ZT Systems during the quarter. This move adds system design expertise, enabling AMD to offer ready-to-deploy rack-level AI solutions based on AMD CPUs, GPUs, and networking. The ZT team is already co-designing with key customers on rack-level designs for the upcoming MI400 series and working to accelerate time-to-market for the MI350 series. The ZT design team will add approximately $50 million in quarterly operating expenses.

b. Client & Gaming

The combined Client & Gaming segment reported revenue of $2.9 billion, up 28% YoY. Operating income was $496 million, reflecting 16.9% operating margin compared to 10.3% in prior year.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

Client

Client revenue saw impressive growth of 68% YoY, reaching $2.3 billion, marking the fifth consecutive quarter of revenue share gains. This growth was driven by strong sales of Ryzen processors and a richer mix of high-end desktop and mobile Ryzen processors, which contributed to record client CPU Average Selling Prices (ASPs).

Desktop channel sell-out increased by over 50% YoY. Sales of Al PC processors also ramped up, increasing by more than 50% quarter-on-quarter. Commercial PC demand was also strong, with Ryzen PRO PC sell-through growing over 30% year-over-year due to new customer wins and an 80% increase in AMD-powered commercial systems from HP, Lenovo, Dell, and Asus.

Gaming

Gaming revenue, however, decreased by 30% YoY to $647 million, primarily due to lower semi-custom SoC sales. This was partially offset by higher Radeon graphics sales.

Despite the yearly decline in semi-custom sales, console channel inventories have normalized, and demand has strengthened for 2025 with semi-custom SoC sales up quarter-over-quarter. Management expects full-year growth in the semi-custom business.

On the PC gaming front, the launch of the Radeon 9070 series, based on the new RDNA 4 architecture, saw strong demand, with record first-week sell-out (10x higher than the previous best Radeon launch). AMD also introduced FSR 4, its first machine learning-based rendering technology.

c. Embedded

Embedded segment revenue was $823 million, down 3% YoY. Demand in this segment continues a gradual recovery with Q1’25 being the fourth quarter of consecutive improvement. Operating income was $328 million reflecting operating margin of 40% (flat YoY).

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

AMD expects improving demand in the test and measurement, communications, and aerospace markets to drive a return to growth in the second half of 2025. The company completed initial shipments of its cost-optimized Spartan UltraScale+ FPGAs and second-generation Versal AI Edge SoCs to meet growing demand for AI at the edge.

3. Outlook

For the second quarter of 2025, AMD expects revenue to be approximately $7.4 billion, plus or minus $300 million. This guidance includes an estimated $700 million revenue reduction due to new export license requirements for MI308 shipments to China. Despite this headwind, the midpoint of the guidance represents 27% YoY revenue growth. Sequentially for Q2, AMD anticipates:

Client & Gaming segment revenue to increase by a double-digit percentage.

Embedded segment revenue to be flat.

Data Center segment revenue to decrease due to the exclusion of MI308 revenue. Data Center GPU revenue is also not expected to grow year-over-year in Q2 due to the export control. However it is expected to grow year-over-year in Q3 and Q4

Non-GAAP gross margin for Q2 is estimated to be around 43%, inclusive of an approximately $800 million charge for inventory primarily for MI308. Excluding this charge, the non-GAAP gross margin would be approximately 54%, which is in line with Q1’25.

Source: AMD Earnings Presentation Q1’25

For the full year 2025, AMD remains confident in delivering strong double-digit revenue growth. This confidence is based on accelerating share gains with its latest Zen 5 EPYC and Ryzen CPUs and Radeon GPUs, as well as the ramping production of MI350 in the second half of the year. The company estimates the full-year revenue impact from the export license requirement for MI308 to China to be approximately $1.5 billion. Management expects this impact to largely occur in Q2 and Q3. AMD also expects full-year growth in its semi-custom business and for the Embedded business to return to year-over-year growth in the second half.

4. Conclusion

Overall, AMD delivered a strong first quarter despite headwinds from export controls to China and the ongoing downcycle in its Embedded and Gaming segments. The Data Center and Client segments performed exceptionally well, gaining CPU market share in both data centers and PCs. While the Gaming segment experienced a decline due to lower semi-custom sales and the Embedded segment is on a gradual recovery path, the outlook for both indicates improvement in the second half of the year.

The newly imposed export controls on MI308 to China present a notable headwind. However, AMD has factored this into its guidance, and management's confidence in achieving strong double-digit revenue growth for the full year remains intact.

In essence, AMD's Q1 performance and outlook suggest a company effectively navigating current challenges, well-positioned for future growth.

If you are interested to learn more about AMD, check our deep dive published in February.