AMD Q2’25: Data Center and Client Segments Shine

Market share gains in PC and Server power another strong quarter for AMD.

Here is a look in AMD’s Q2 earnings in case you missed it. AMD delivered a strong second quarter for 2025, beating revenue estimates and demonstrating significant momentum in its Data Center and Client segments. While the transition to its next-generation AI accelerators and ongoing export restrictions presented headwinds for the Data Center AI business, the core CPU portfolio and a recovery in the Gaming segment painted a picture of robust growth and market share gains.

1. Results

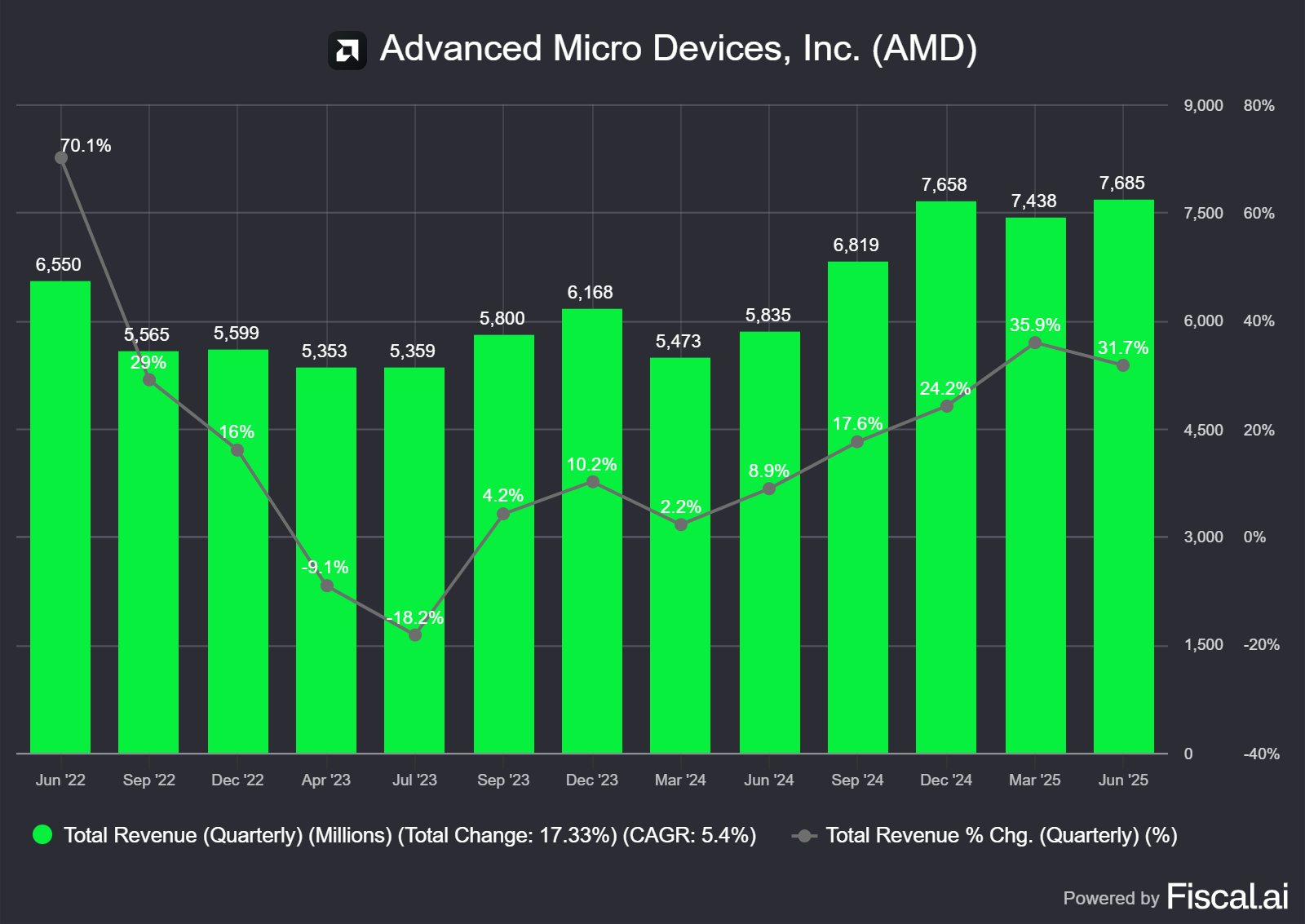

Revenue for the quarter increased 32% year-over-year to $7.68 billion, outperforming the consensus estimate of $7.43 billion and the high end of management's guidance. The strong performance was primarily driven by record sales of EPYC and Ryzen CPUs, alongside a welcome recovery in the Gaming segment.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

However, $800 million write-off for the MI308 inventory, impacted by U.S. export controls, affected profitability. Non-GAAP gross margin came in at 43%. Excluding the inventory charge, the gross margin was 54%, improving from 53% in the prior year and consistent with Q1'25. Consequently, non-GAAP operating income was $897 million, down 29% year-over-year, with an operating margin of 12% (Vs 22% in Q2’24).

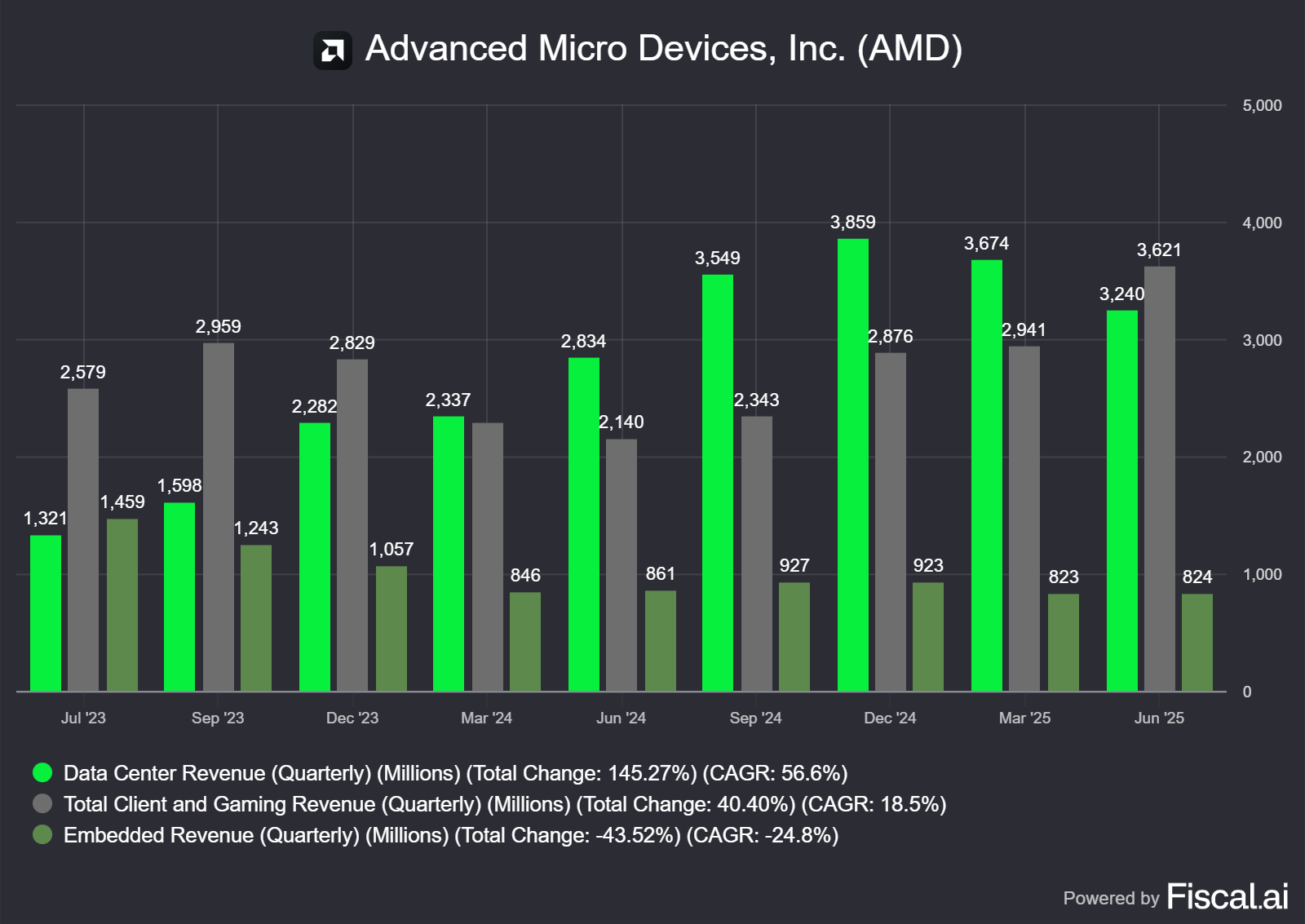

2. Segments

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

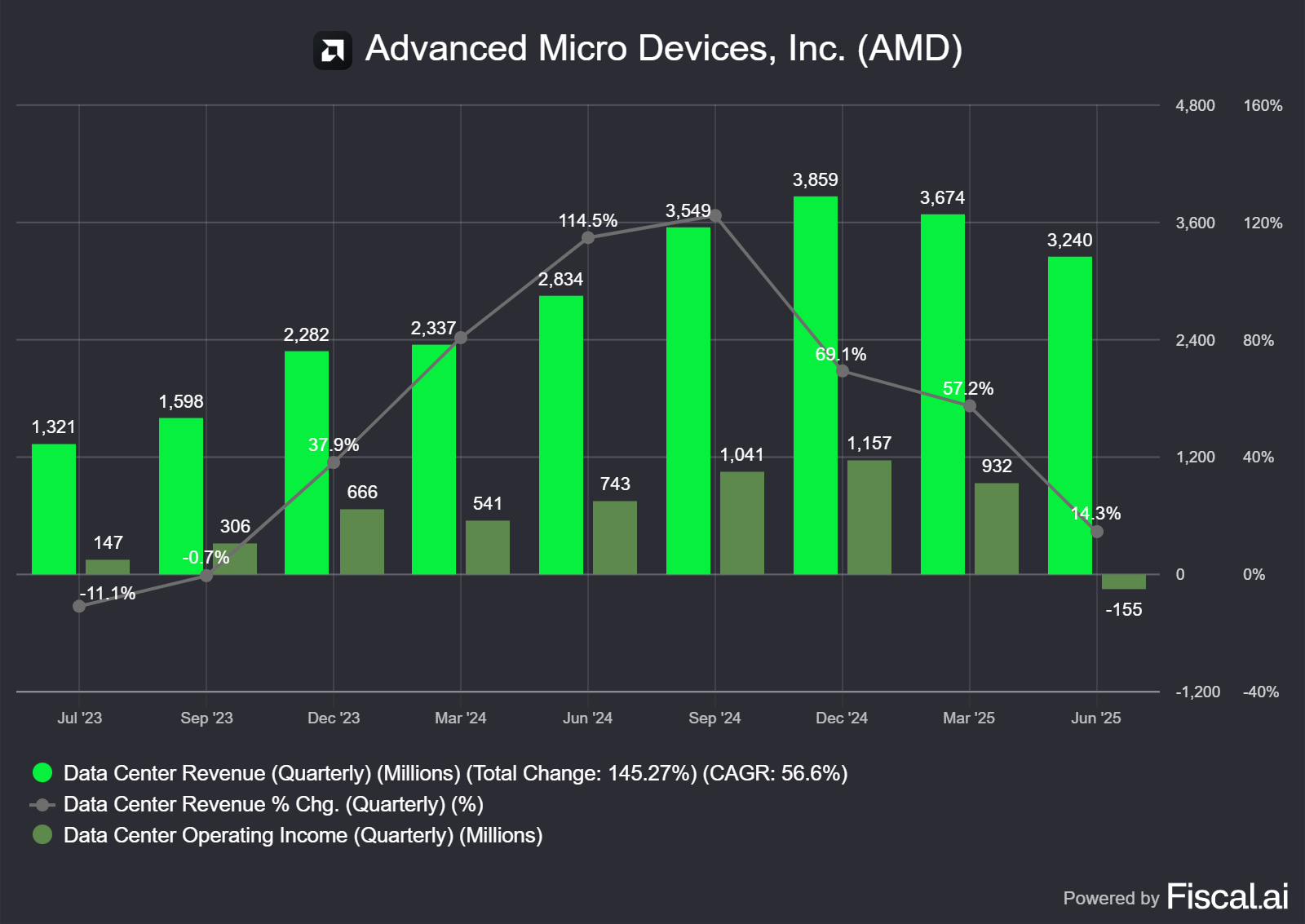

a. Data Center

The Data Center segment revenue grew 14% year-over-year to $3.2 billion. This represents a deceleration from the 57% growth seen in Q1, largely due to a decline in AI accelerator revenue. This was caused by U.S. export restrictions to China, which halted sales of the MI308, and a product cycle transition to the next-generation MI350 series, which is expected to ramp in the second half of the year.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

The segment reported an operating loss of $155 million, compared to an operating income of $743 million last year, with the MI308 inventory write-off being the primary factor.

EPYC Processors

Data center CPUs continued their phenomenal performance. Management noted that strong demand for AI is also boosting the need for general-purpose compute. As CEO Lisa Su explained on the earnings call:

“In particular, adoption of agentic AI is creating additional demand for general purpose compute infrastructure as customers quickly realize that each token generated by a GPU triggers multiple CPU-intensive tasks. Against this backdrop, fifth-gen EPYC Turin shipments ramped significantly, and we had sustained demand for our prior-generation EPYC processors.”

Both Cloud and enterprise CPU sales reached record highs, marking the 33rd consecutive quarter of year-over-year server CPU share gains for AMD. With nearly 1,200 EPYC cloud instances now available globally (up from over 900 a year ago), hyperscaler adoption remains strong.

Given that revenue from AI accelerators decreased year-over-year (more than $1 billion of sales of AI accelerators in Q2’24), it is reasonable to assume that the data center CPU business grew in excess of 20% year-over-year.

Instinct accelerators

Data Center AI revenue declined year-over-year due to the aforementioned export controls and the transition to the MI350 series. Despite the quarterly decline, management expects Instinct revenue to grow year-over-year in the third quarter, driven by the MI350 ramp.

Management emphasized the total cost of ownership (TCO) advantages of the new series:

“We launched our Instinct MI350 series with industry-leading memory bandwidth and capacity and broad adoption across hyperscalers, AI companies and OEMs. From a competitive standpoint, MI355 matches or exceeds B200 in critical training and inference workloads and delivers comparable performance to GB200 for key workloads at significantly lower cost and complexity.

For upscale inferencing, MI355 delivers up to 40% more tokens per dollar, providing leadership performance and clear TCO advantages.

With the MI350 series, we're also expanding our system-level capabilities to support deployments powered by AMD CPUs, GPUs and NICs. As one example, Oracle is building a 27,000-plus node AI cluster combining MI355X accelerators, fifth-gen EPYC Turin CPUs and Pollara 400 SmartNICs. We began volume production of the MI350 series ahead of schedule in June and expect a steep production ramp in the second half of the year to support large-scale production deployments with multiple customers.”

Looking further ahead, the company is generating significant customer interest for its next-generation MI400 series, planned for a 2026 launch.

“Looking ahead, the development of our next-generation MI400 series is progressing rapidly. These are the most advanced GPUs we have ever built with up to 40 petaflops of FP4 AI performance and 50% more memory, memory bandwidth and scale-out throughput than the competition.

With the MI400 series, we're bringing together everything we've learned across silicon, software and systems to deliver Helios, a full-stack rack scale AI platform.

Helios is purpose built for the most demanding AI workloads with each rack connecting up to 72 GPUs that can operate as a single massive AI accelerator. Helios is expected to deliver up to a 10x generational performance increase for the most advanced Frontier models, and we believe it will be the highest-performance AI system in the world when it launches. MI400 series development is progressing well towards our planned launch in 2026, with significant interest in large-scale deployments from multiple high-profile customers.”

Progress was also highlighted on the ROCm software front, a critical component for competing with Nvidia's CUDA platform. The company announced ROCm 7, delivering over 3x higher performance compared to its prior generation, and expanded developer access and native support across key frameworks.

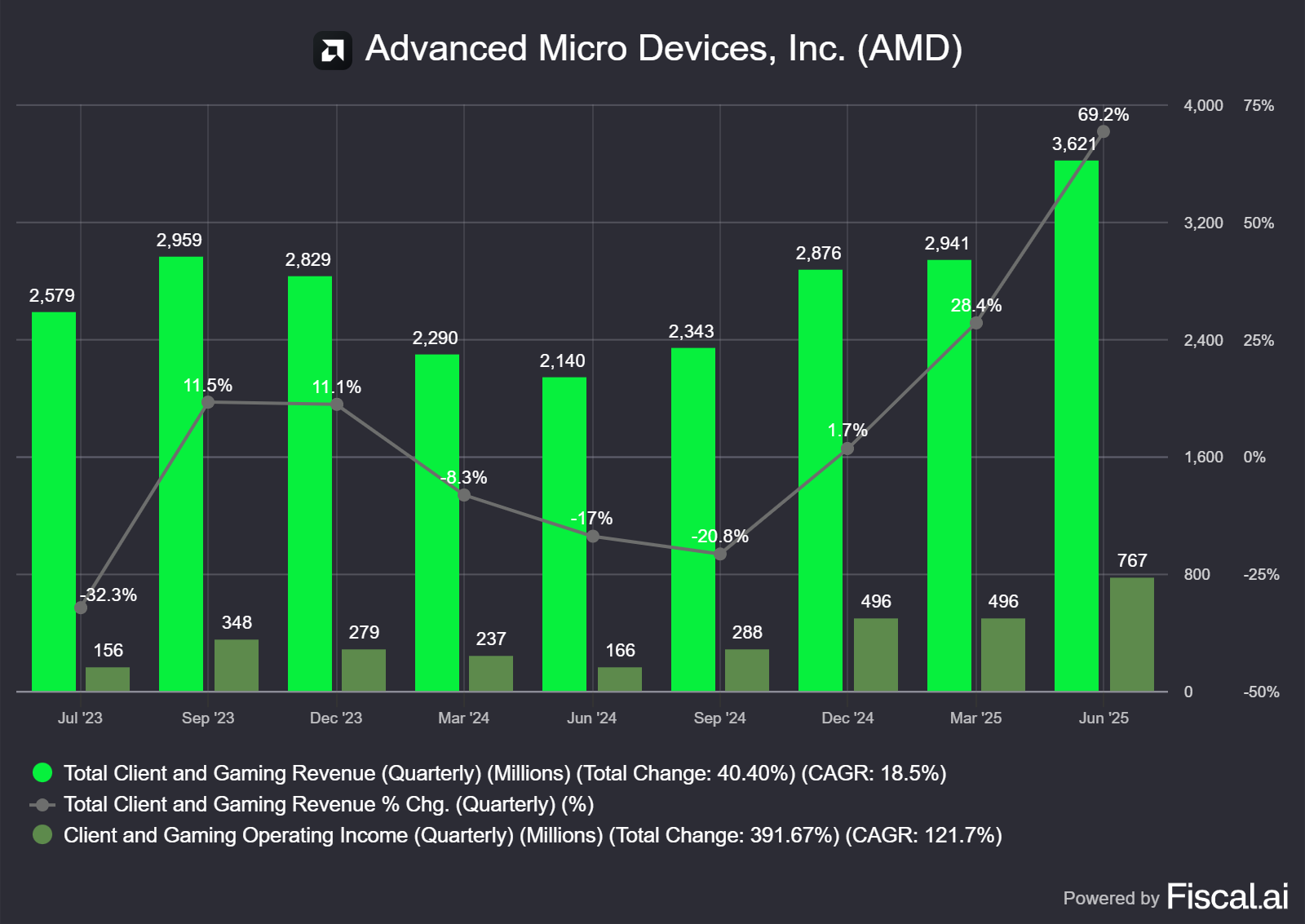

b. Client & Gaming

The combined Client & Gaming segment reported revenue of $3.6 billion, up an impressive 69% year-over-year. Operating income surged to $767 million, reflecting a 21.2% operating margin, a significant expansion from 7.8% last year.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Client

Client revenue grew 67% year-over-year to $2.5 billion, driven by record desktop CPU sales as Ryzen processors topped best-seller lists. This is the 7th consecutive quarter of revenue growth in excess of 50%.

In mobile, there was strong demand for AMD-powered notebooks, with sell-out growing by a large double-digit percentage year-over-year. A higher mix of premium AI notebooks also drove up average selling prices (ASPs).

In commercial PCs, Ryzen adoption accelerated as OEM consumption increased more than 25% year-over-year.

Looking ahead management expects to continue gaining share in the Client segment.

Gaming

After ten consecutive quarters of decline, the Gaming segment returned to growth, with revenue increasing 73% year-over-year to $1.1 billion. The growth was fueled by a large double-digit increase in semi-custom revenue as console inventories normalized ahead of the holiday season.

On PC gaming, management highlighted that demand for the latest-generation Radeon 9000 series GPUs was very strong, with desktop GPU sell-through accelerating in the quarter as demand outpaced supply.

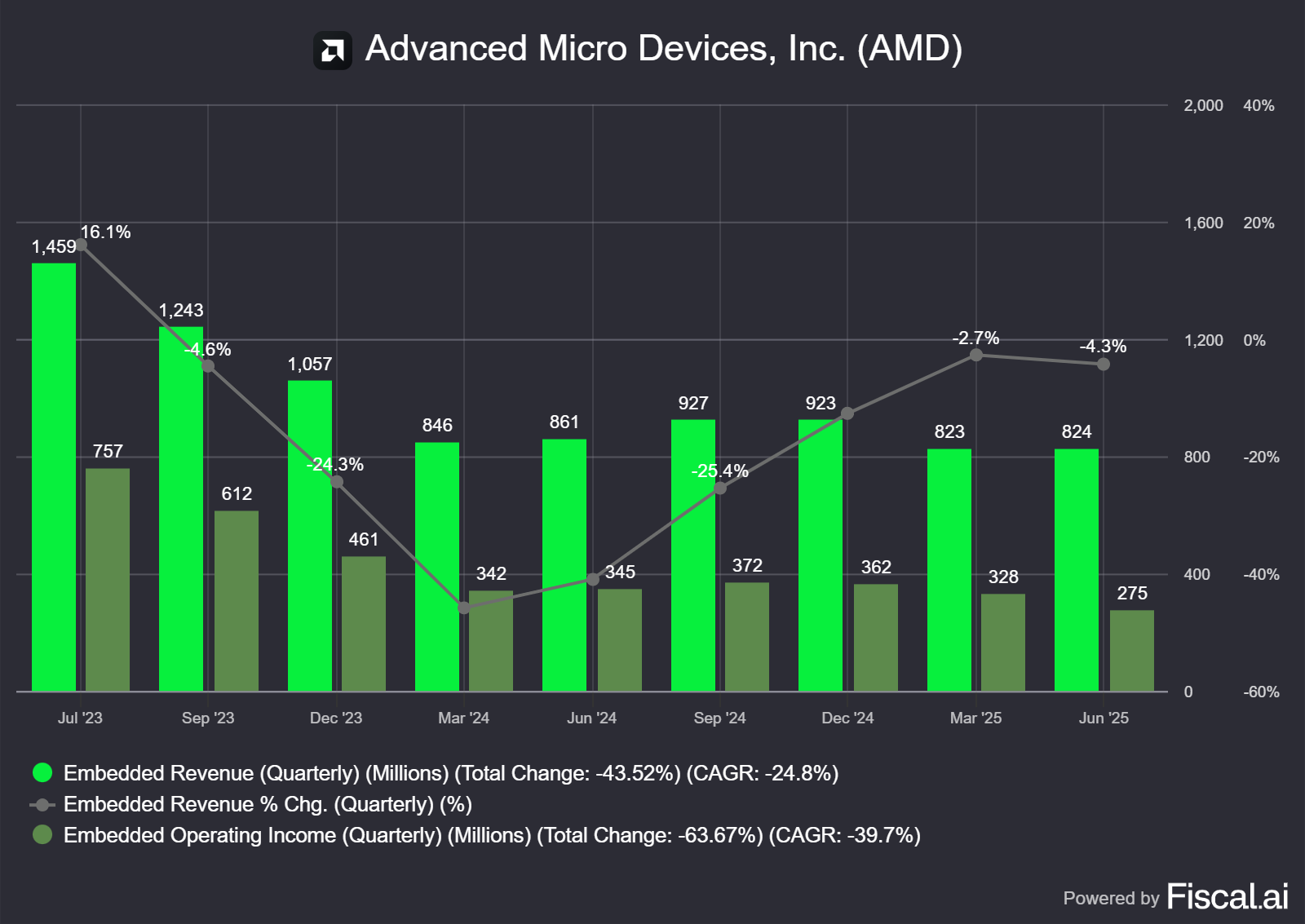

c. Embedded

The Embedded segment revenue was $824 million, down 4% year-over-year, but showed signs of a gradual recovery, with revenue flat sequentially. The decline in operating margin to 33% compared to 40% last year was attributed to product mix. Management expects improving demand in key markets to drive a return to sequential growth in the second half of 2025.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

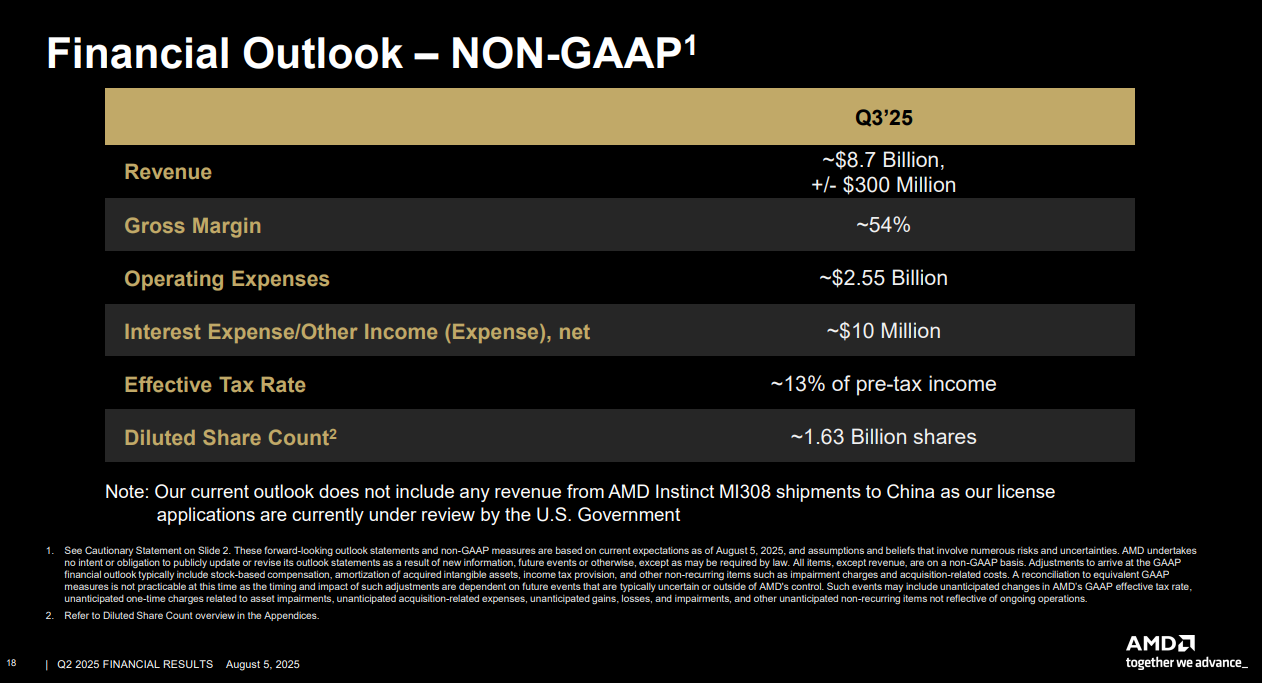

3. Outlook

For the third quarter of 2025, AMD expects revenue to be approximately $8.7 billion (+/- $300 million), implying 28% year-over-year growth at the midpoint. This growth is expected to be driven by strong double-digit increases in the Client, Gaming, and Data Center segments.

Sequentially for Q3, AMD anticipates:

strong double-digit growth in the Data Center segment with the ramp of AMD Instinct MI350

modest growth in Client and Gaming segment, with Client revenue increasing and the Gaming revenue to be flattish

Embedded segment revenue to return to growth

Notably, the guidance does not include any potential revenue from MI308 shipments to China. On this front, it was reported yesterday that the U.S. government will approve sales of AMD's MI308 and Nvidia's H20 in exchange for a 15% revenue share. While not confirmed yet, any such agreement would represent a potential upside to the current guidance.

Non-GAAP gross margin is guided to be approximately 54%. The company also guided for non-GAAP operating expenses of approximately $2.55 billion, reflecting increased investments in R&D, particularly for AI, and implying an operating margin of roughly 25%.

Source: AMD Earnings Presentation Q2’25

4. Conclusion

AMD's Q2 results demonstrate the strength of its core businesses, with the Data Center CPU and Client segments performing exceptionally well and gaining market share. While the AI accelerator business is navigating a transition period, the MI350 and MI400 series appears promising.

As Lisa Su concluded:

“Looking ahead, we see a clear path to scaling our AI business to tens of billions of dollars in annual revenue. We are very excited about our next-generation MI400 series... Customer interest for the MI400 series is very strong, and we are actively engaging with an expanding set of customers to support large-scale deployments in 2026.”