AMD Q3'25: CPUs Hit Records & AI Ramp

Record CPU sales and accelerating AI demand drive a strong beat

Here is a look at AMD’s Q3 earnings in case you missed it. AMD delivered an outstanding third quarter for 2025, beating revenue ($9.25B Vs $8.75B expected) and earnings estimates ($1.2 EPS Vs $1.17 expected). Momentum across its Data Center AI, Server, and PC businesses continued. While the Embedded segment remained soft year-over-year, it showed signs of recovery with sequential growth.

1. Results

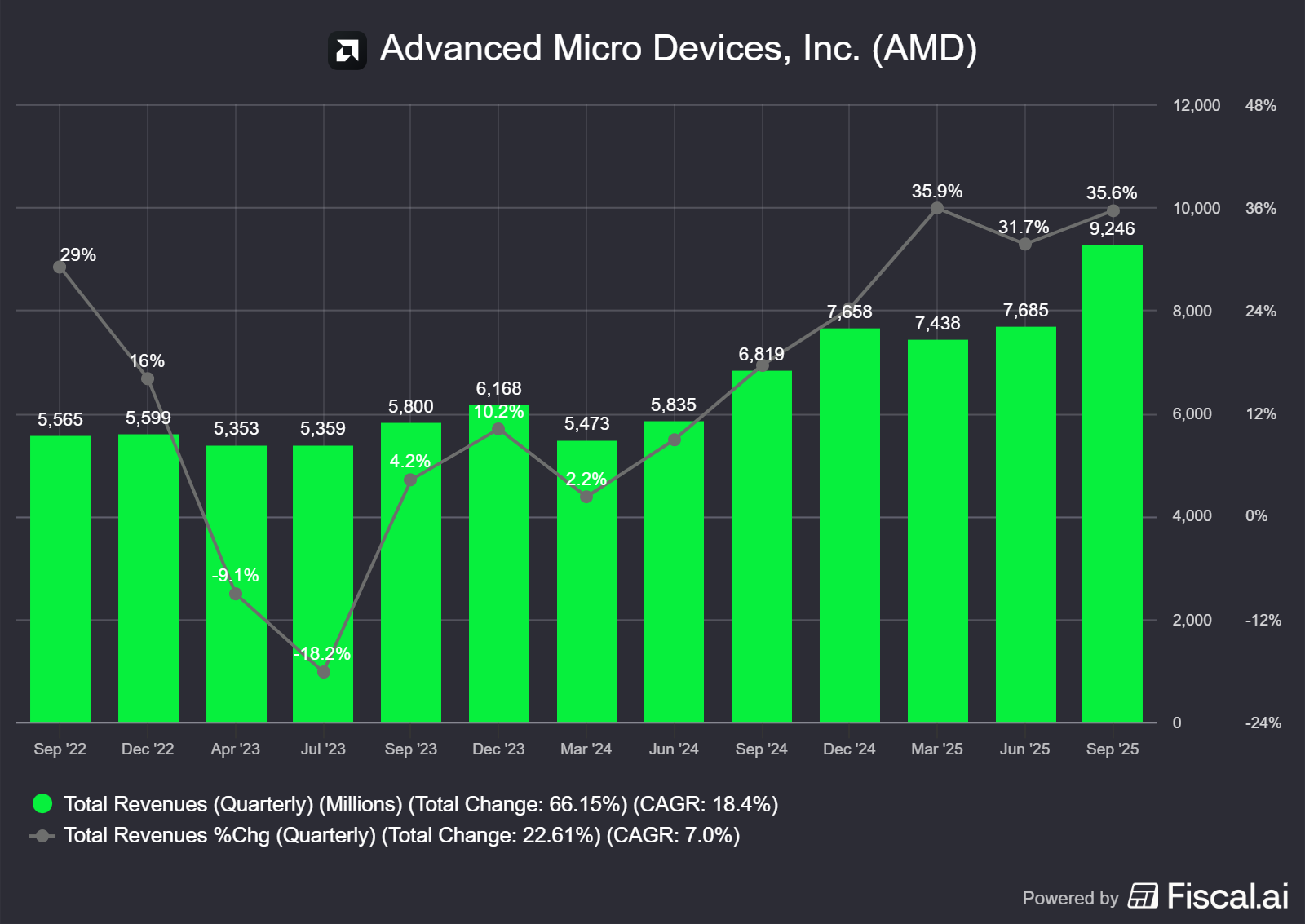

Revenue for the quarter increased 36% year-over-year to a record $9.2 billion, significantly outperforming the consensus estimate and the high end of management’s guidance (which was $8.7B +/- $300M). The strong performance was primarily driven by record sales of EPYC, Ryzen, and Instinct processors.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Profitability was also strong. Non-GAAP gross margin was 54%, flat year-over-year but a strong recovery from 43% in Q2’25 which was affected by the $800 million write-off for the MI308 inventory. Non-GAAP operating income was $2.2 billion, up 30% year-over-year. The operating margin of 24% was down slightly from 25% last year, which management attributed to higher R&D investments to capitalize on significant AI opportunities. Non-GAAP EPS was a record $1.20, up 30% Y/Y.

2. Segments

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

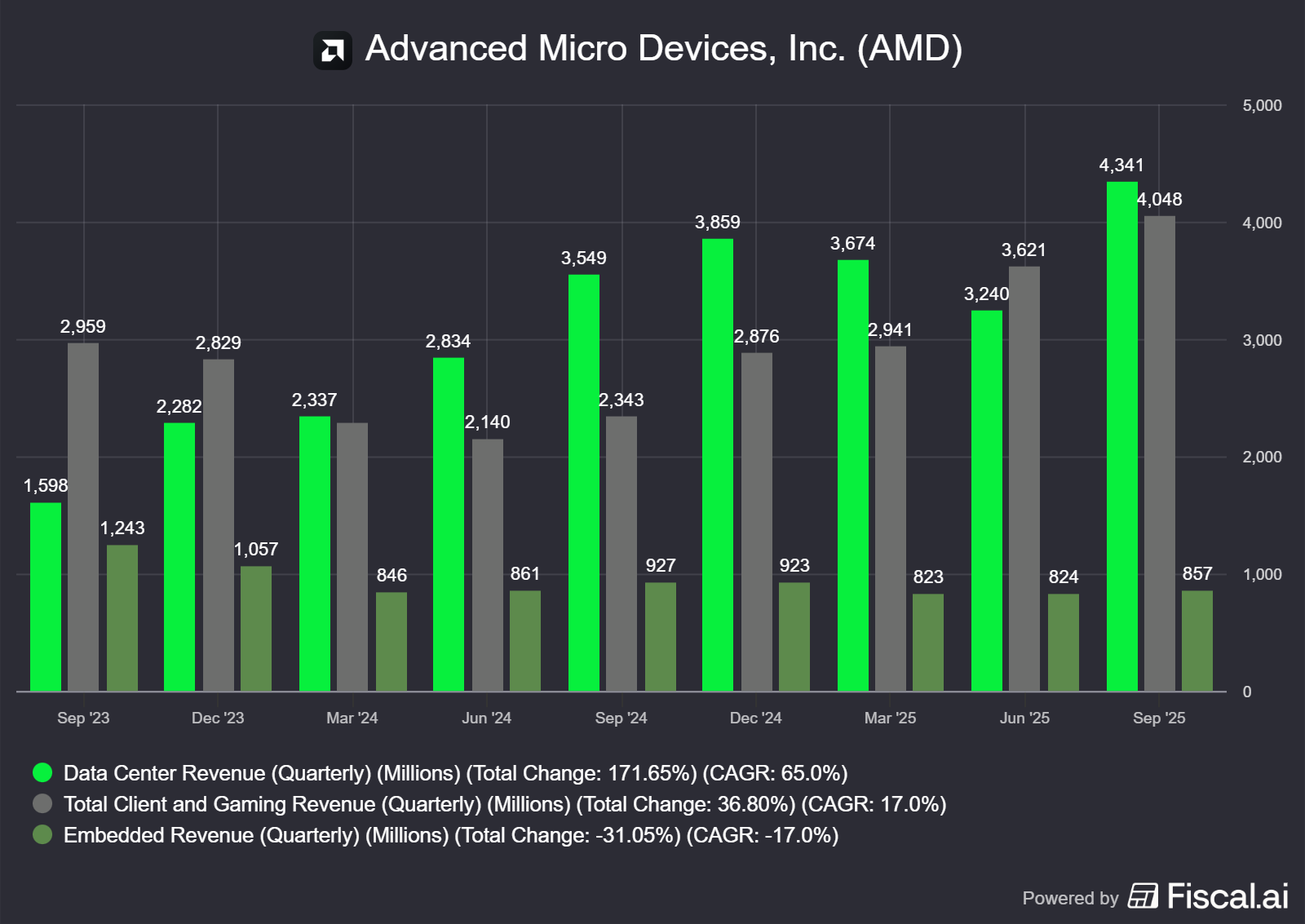

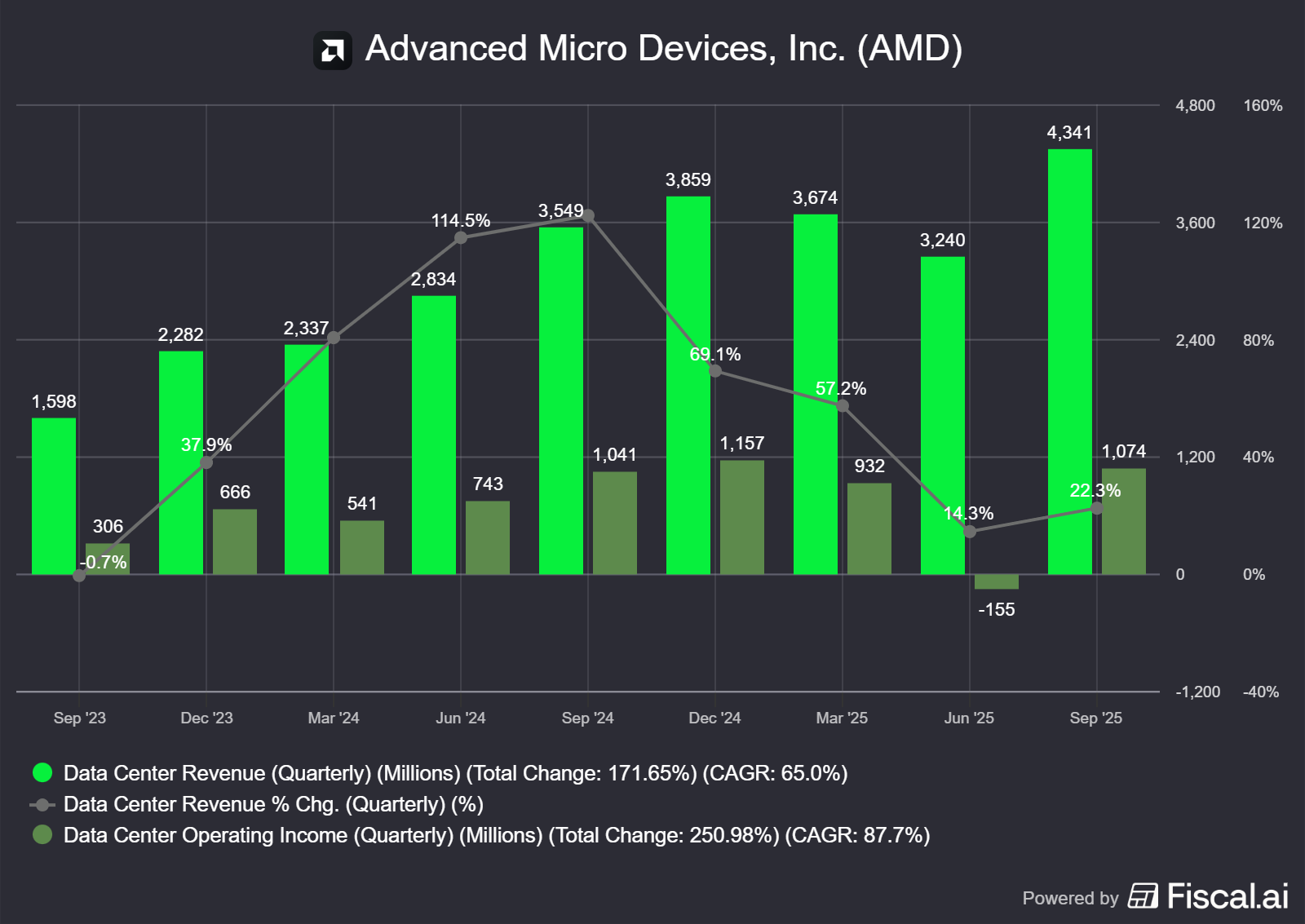

a. Data Center

The Data Center segment revenue hit a record $4.3 billion, up 22% year-over-year. This represents a significant acceleration from the 14% growth seen in Q2. The growth was driven by the sharp ramp of Instinct MI350 Series GPUs and continued share gains in server CPUs.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

The segment reported an operating income of $1.1 billion, for a 25% operating margin. This was down from 29% a year ago, primarily due to higher R&D investments in the AI roadmap.

EPYC Processors

Data center CPUs continued their phenomenal performance, reaching an all-time high in sales. Management noted once again that the ramp of AI is also boosting the need for general-purpose compute. As CEO Lisa Su explained on the earnings call:

“Many customers are now planning substantially larger CPU build-outs over the coming quarters to support increased demands from AI serving as a powerful new catalyst for our server business.”

Adoption of 5th Gen EPYC Turin processors accelerated rapidly, accounting for nearly half of all EPYC revenue in the quarter. Cloud sales hit a record as hyperscalers launched over 160 new EPYC instances, bringing the global total to over 1,350. Enterprise adoption also accelerated, with sell-through increasing sharply.

Looking ahead, the next-generation 2-nanometer Venice processors are on track to be launched in 2026.

“Customer pull and engagement for Venice are the strongest we have seen reflecting our competitive positioning and the growing demand for more data center compute. Multiple cloud OEM partners have already brought their first Venice platforms online, setting the stage for broad solution availability and cloud deployments at launch.”

Instinct accelerators

The Data Center AI business returned to growth as a result of the ramp of MI350 GPUs. The highlights on AMD’s AI strategy and collaborations were the following:

OpenAI Strategic Partnership: AMD announced a multiyear agreement with OpenAI to deploy 6 gigawatts of Instinct GPUs. The first gigawatt, using the next-gen MI450 accelerator, is scheduled to come online in the second half of 2026. Management stated this partnership has the potential to generate well over $100 billion in revenue over the next few years.

Oracle Partnership: Oracle was announced as another lead launch partner for the MI450 Series, deploying tens of thousands of GPUs starting in 2026.

Management emphasized the significance of these wins as a validation of their TCO and software stack:

“OpenAI’s decision to use AMD Instinct platforms for its most sophisticated and complex AI workloads sends a clear signal that our Instinct GPUs and ROCm open software stack deliver the performance and TCO required for the most demanding deployments.”

Software Progress: The company launched ROCm 7, its most advanced software release, delivering up to 4.6x higher inference and 3x higher training performance compared to the prior version.

Next-Gen Helios Platform: Development is progressing rapidly on the next-gen MI400 Series and the Helios rack-scale solution which is expected to launch in 2026.

Helios integrates our Instinct MI400 Series GPUs, Venice EPYC CPUs and Pensando NICs in a double-wide rack solution optimized for the performance, power, cooling and serviceability required for the next generation of AI infrastructure and supports Meta’s new open rack wide standard. Development of both our MI400 Series GPUs and Helios rack is progressing rapidly, supported by deep technical engagements across a growing set of hyperscalers, AI companies and OEM and ODM partners to enable large-scale deployments next year.

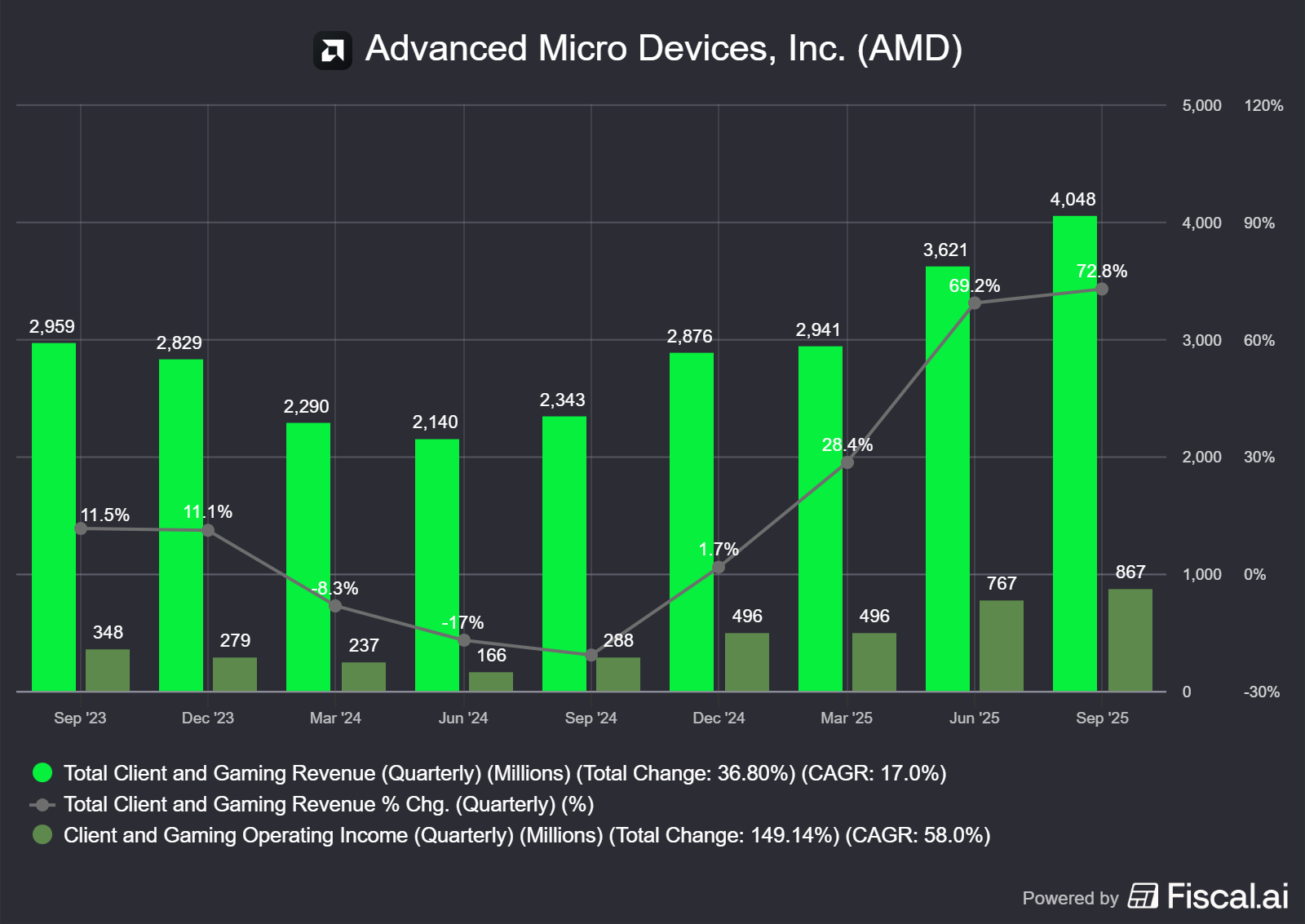

b. Client & Gaming

The combined Client & Gaming segment reported a record $4.0 billion in revenue, up 73% year-over-year. Operating income surged to $867 million, reflecting a 21% operating margin, an expansion from 12% last year.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Client

Client (PC) revenue grew 46% year-over-year to a record $2.8 billion, driven by record desktop CPU sales as Ryzen 9000 processors led demand. In the commercial market, Ryzen PRO adoption accelerated, with PC sell-through up more than 30% year-over-year.

Gaming

Gaming revenue rebounded sharply, growing 181% year-over-year to $1.3 billion. This growth was fueled by higher semi-custom revenue as Sony and Microsoft prepare for the holiday sales period. In PC gaming, demand for the Radeon 9000 series GPUs was strong, with channel sell-through growing significantly.

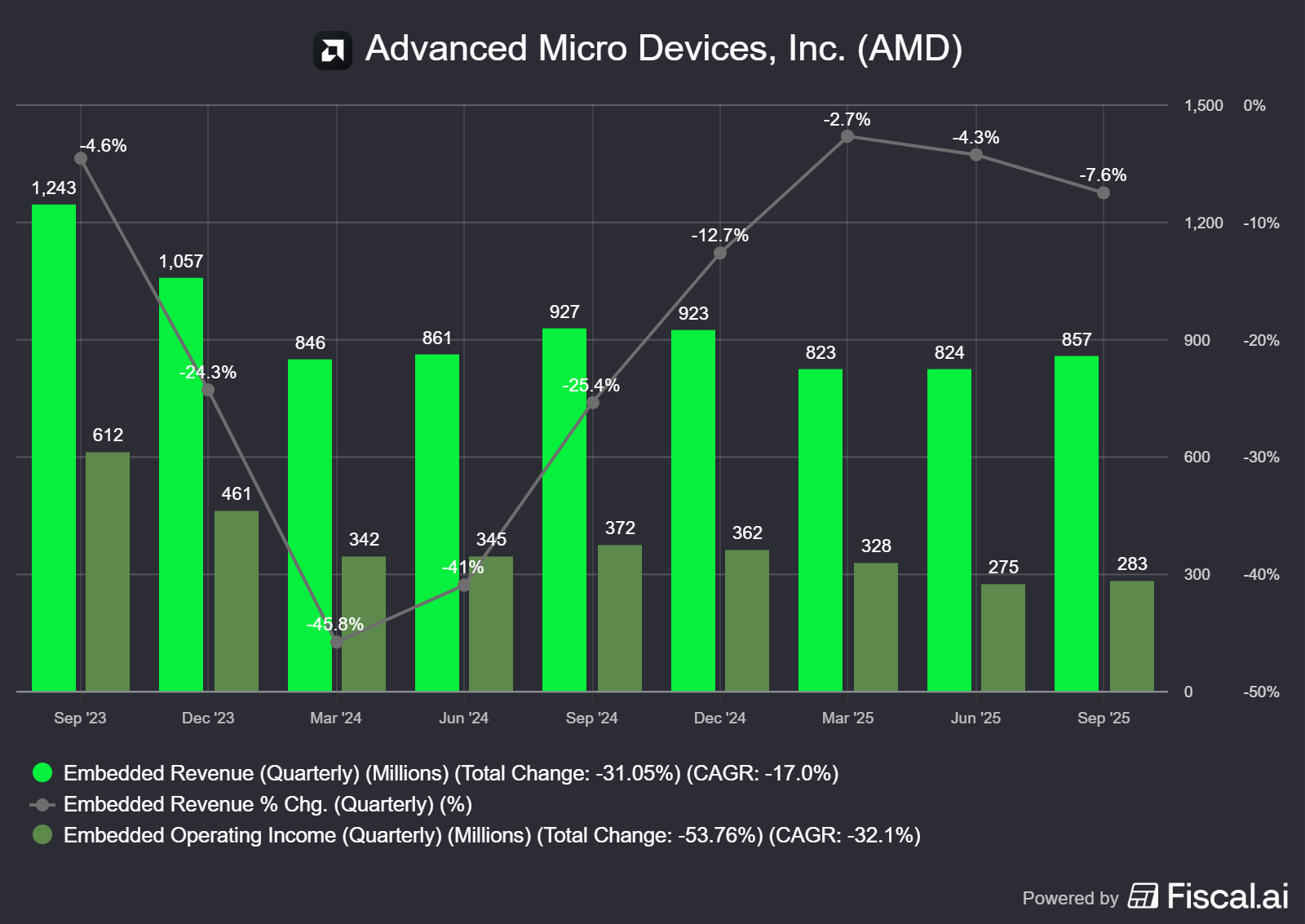

c. Embedded

The Embedded segment revenue was $857 million, down 8% year-over-year, as the market continues to correct. However, the segment showed signs of strengthening, with revenue growing 4% sequentially. Operating margin declined to 33% from 40% last year due to product mix. Despite the near-term cyclical weakness, the design-win pipeline remains exceptionally strong, with AMD on track for a second straight year of record design wins already totaling more than $14 billion year-to-date.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

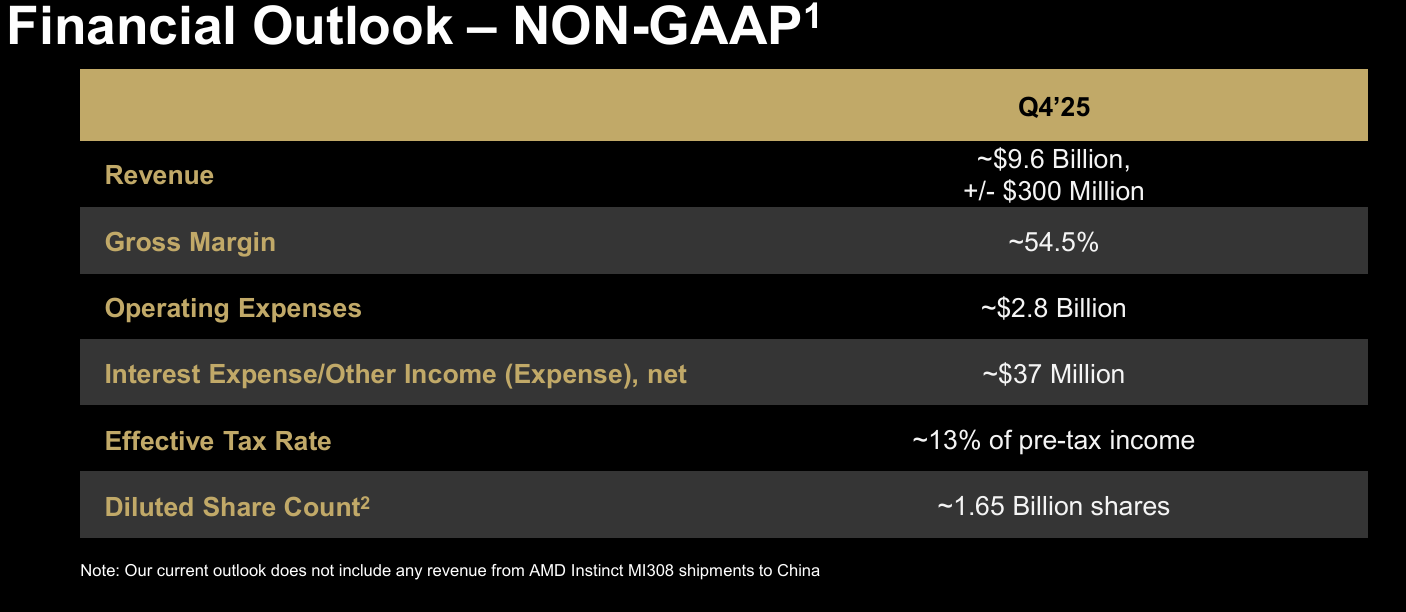

3. Outlook

For the fourth quarter of 2025, AMD expects revenue to be approximately $9.6 billion (+/- $300 million), implying 25% year-over-year growth at the midpoint.

This growth is expected to be driven by:

Data Center: Up double-digits sequentially, with strong growth in server and a continued ramp of MI350 GPUs.

Client & Gaming: Down sequentially, as Client revenue is expected to increase but Gaming is guided to be down strong double digits.

Embedded: Up double-digits sequentially, signaling a strong recovery.

Notably, this guidance does not include any revenue from MI308 shipments to China.

Non-GAAP gross margin is guided to be approximately 54.5%. The company also guided for non-GAAP operating expenses of approximately $2.8 billion, implying a non-GAAP operating margin of approximately 25%, a one-percentage-point improvement over Q3’25.

Source: AMD Earnings Presentation Q3’25

4. Conclusion

AMD’s Q3 results were a strong beat, demonstrating the strength in its core CPU businesses, which hit all-time records. While the Embedded segment is still navigating a cycle, the AI accelerator business just received its ultimate validation. The strategic partnerships with OpenAI and Oracle is validating AMD’s strategy in an effort to get a higher share from Nvidia’s pie (Nvidia reported $41B revenue from its data center segment in the latest quarter compared to $4B for AMD).