Here is a look at AMD’s Q4 earnings in case you missed it. AMD closed 2025 delivering record revenue of $10.3 billion, beating the consensus estimate of $9.67 billion and its own guidance of $9.6 billion (+/- $300M). The beat was driven by broad-based strength, particularly in the Data Center and Client segments, while profitability metrics saw a significant boost from inventory reserve releases related to sales to China.

Despite the strong headline results, the stock price fell 17% the next day as the market looked for an even greater surprise. It seems investors still question AMD’s ambitious long-term target of growing revenue at a >35% CAGR over the next five years.

1. Results

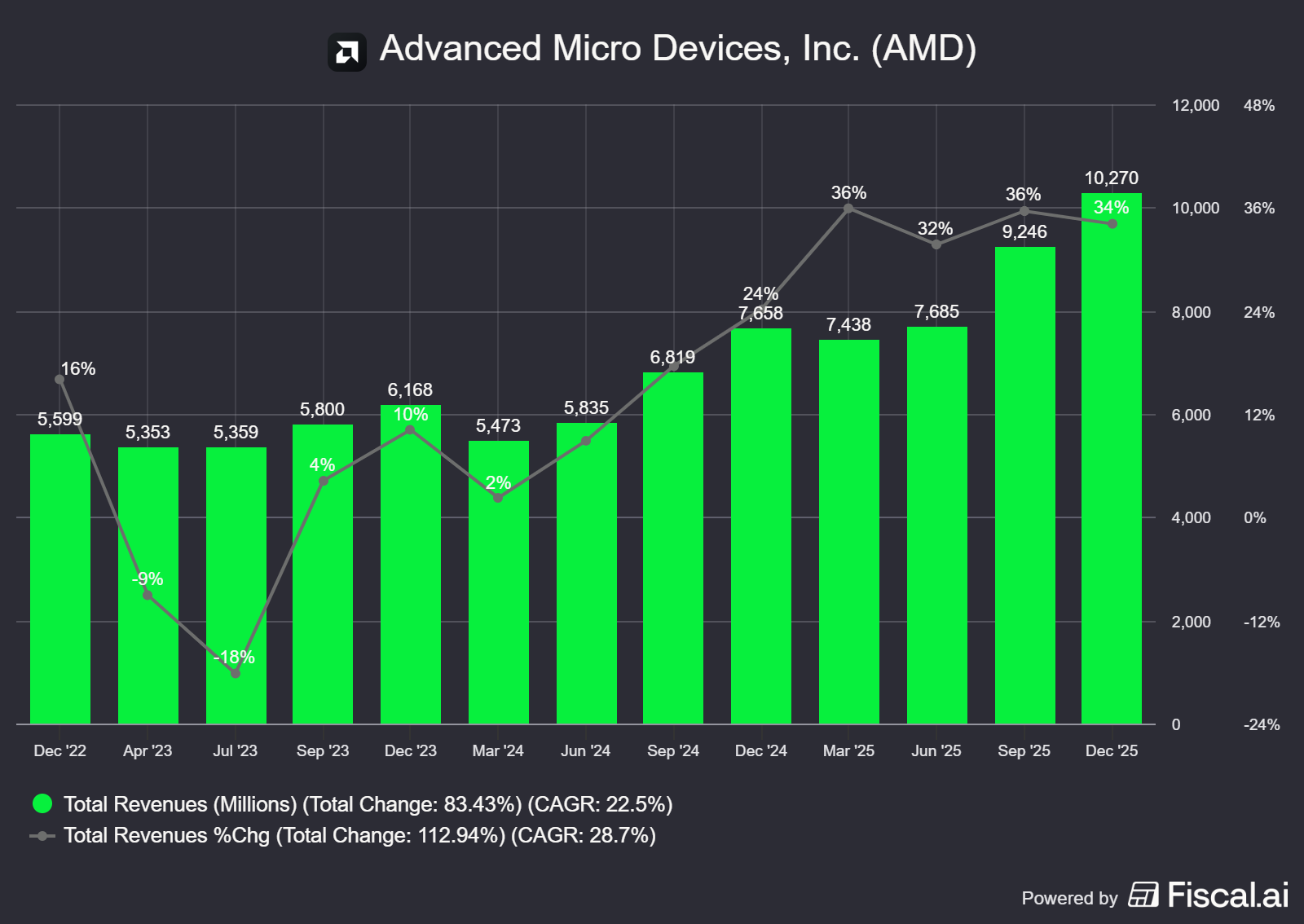

Revenue for the quarter increased 34% year-over-year (and 11% sequentially) to a record $10.3 billion. The upside was fueled by record EPYC and Ryzen sales, alongside a $390 million revenue contribution from Instinct MI308 shipments to China which were not included in the guidance provided in Q3’25.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Non-GAAP gross margin hit 57%, up 300 basis points year-over-year. It is important to note this includes a benefit from the release of $360 million in previously reserved inventory (related to the MI308 China product). Excluding this one-time benefit and the China revenue, the "adjusted" non-GAAP gross margin was approximately 55%, still a healthy expansion driven by favorable product mix.

Non-GAAP operating income was a record $2.9 billion, up 41% year-over-year. The operating margin expanded to 28%, up from 26% a year ago. Non-GAAP EPS was a record $1.53, up 40% YoY.

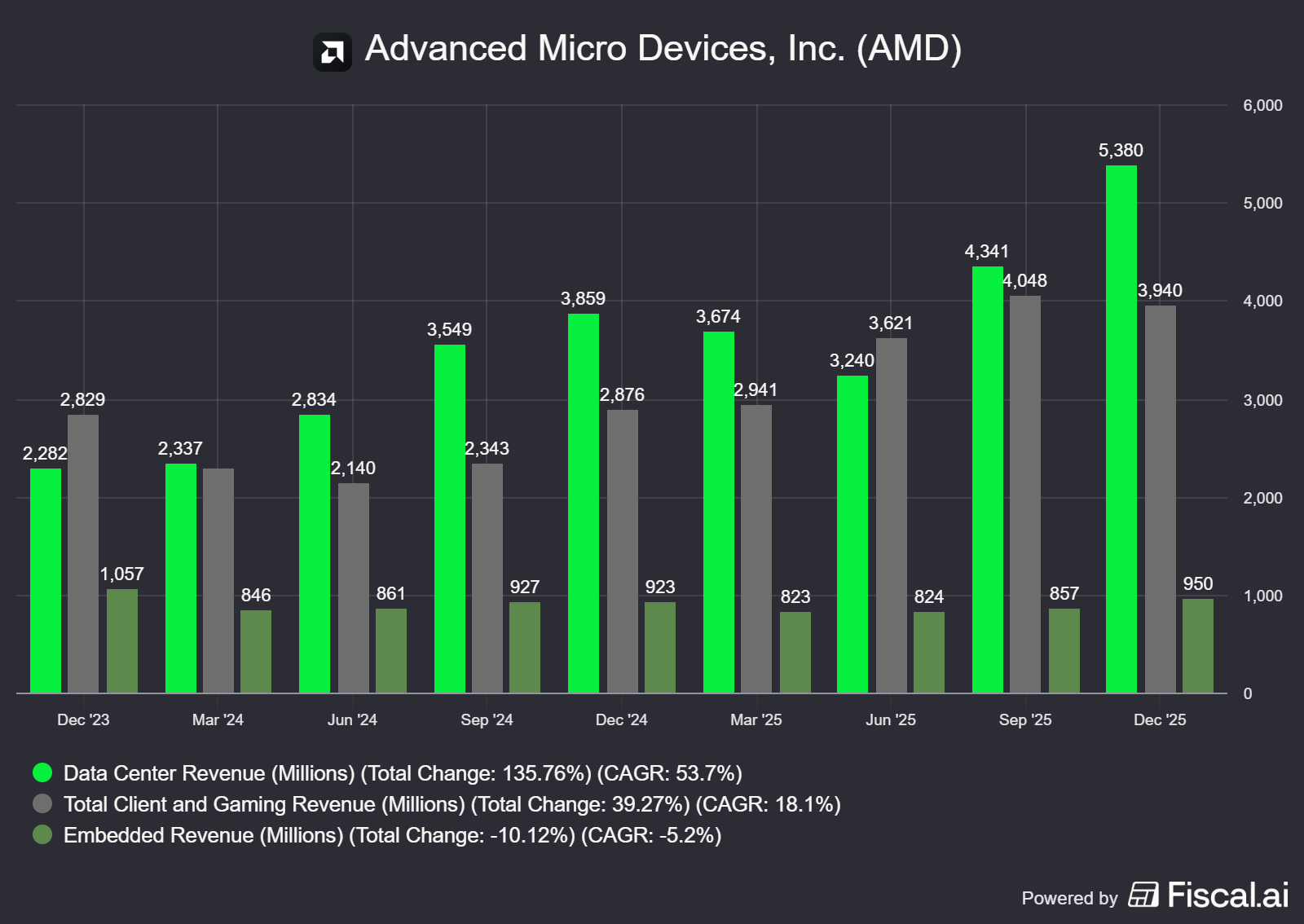

2. Segments

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

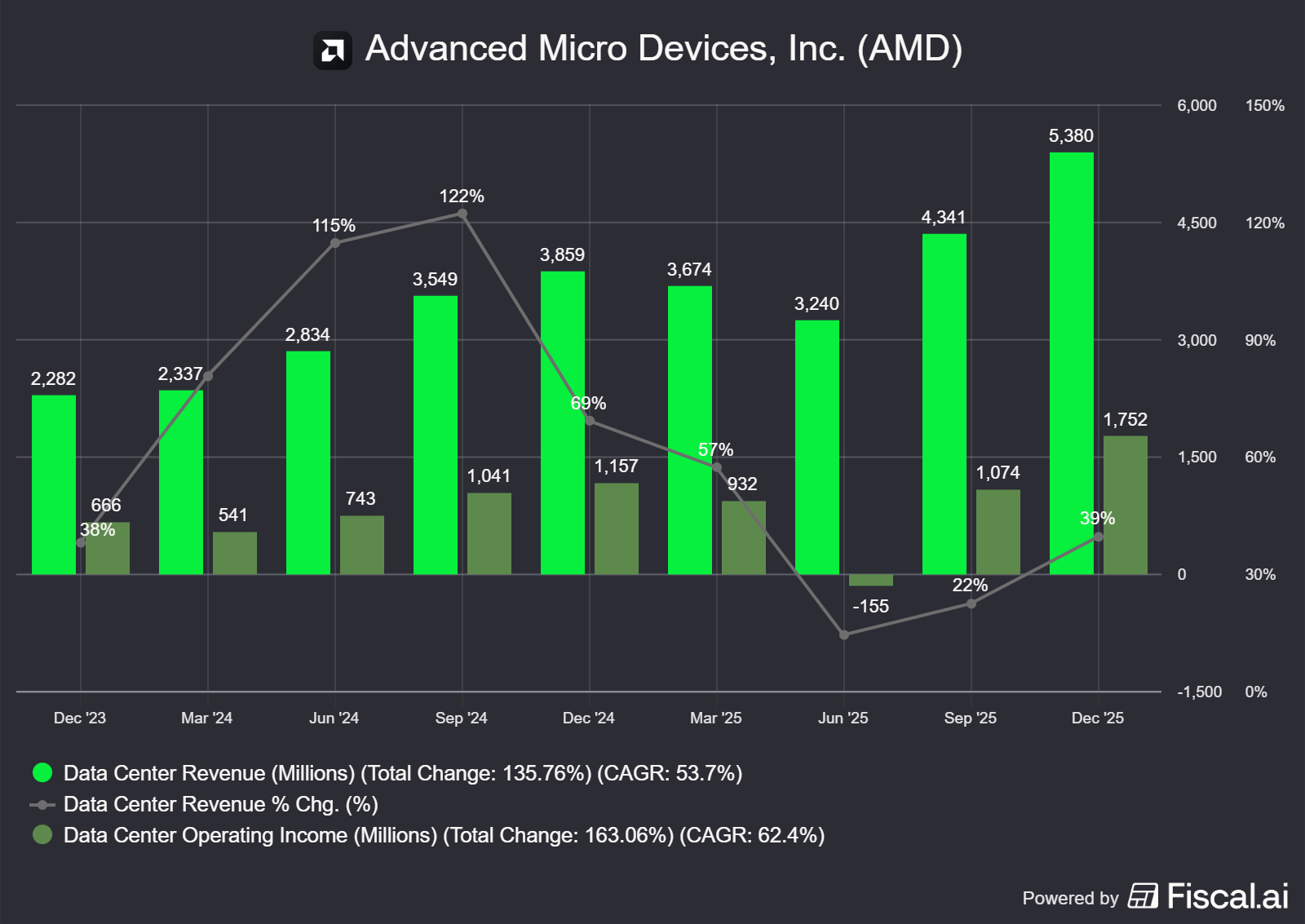

a. Data Center

The Data Center segment remains the growth engine, with revenue hitting a record $5.4 billion, up 39% year-over-year. This acceleration (compared to 22% growth in Q3) highlights the massive demand for both general-purpose compute and AI infrastructure.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

The segment reported an operating income of $1.8 billion, representing a 33% operating margin. This is a significant jump from the 25% margin seen in Q3, aided by the inventory reserve release mentioned earlier.

In terms of the outlook, management reiterated the target to grow Data Center revenue by >60% annually over the next 3-5 years and scale AI revenue to “tens of billions” by 2027.

EPYC Processors

Server CPUs continue to be a dominant force. Sales of 5th Gen EPYC "Turin" processors accelerated, accounting for more than half of total server revenue in the quarter. Management highlighted that the need for Agentic AI workflows is actually driving higher demand for powerful CPUs to act as head nodes. As CEO Lisa Su noted:

“We exited the year with record server share... EPYC has become the processor of choice for the modern data center, delivering leadership performance, efficiency and TCO."

Instinct accelerators

The AI business continues to scale rapidly. Key highlights from the quarter include:

MI308 China Revenue: AMD recognized ~$390 million from MI308 sales to China. Management guided for another ~$100 million in Q1 2026 but is not forecasting further China revenue beyond that due to the dynamic regulatory environment.

MI350 Ramp: The MI350 series is ramping well, with 8 of the top 10 AI companies now using Instinct for production workloads.

Next-Gen Roadmap: The focus is shifting to the MI450 and the Helios rack-scale platform, scheduled for launch in H2 2026. This is viewed as a major inflection point.

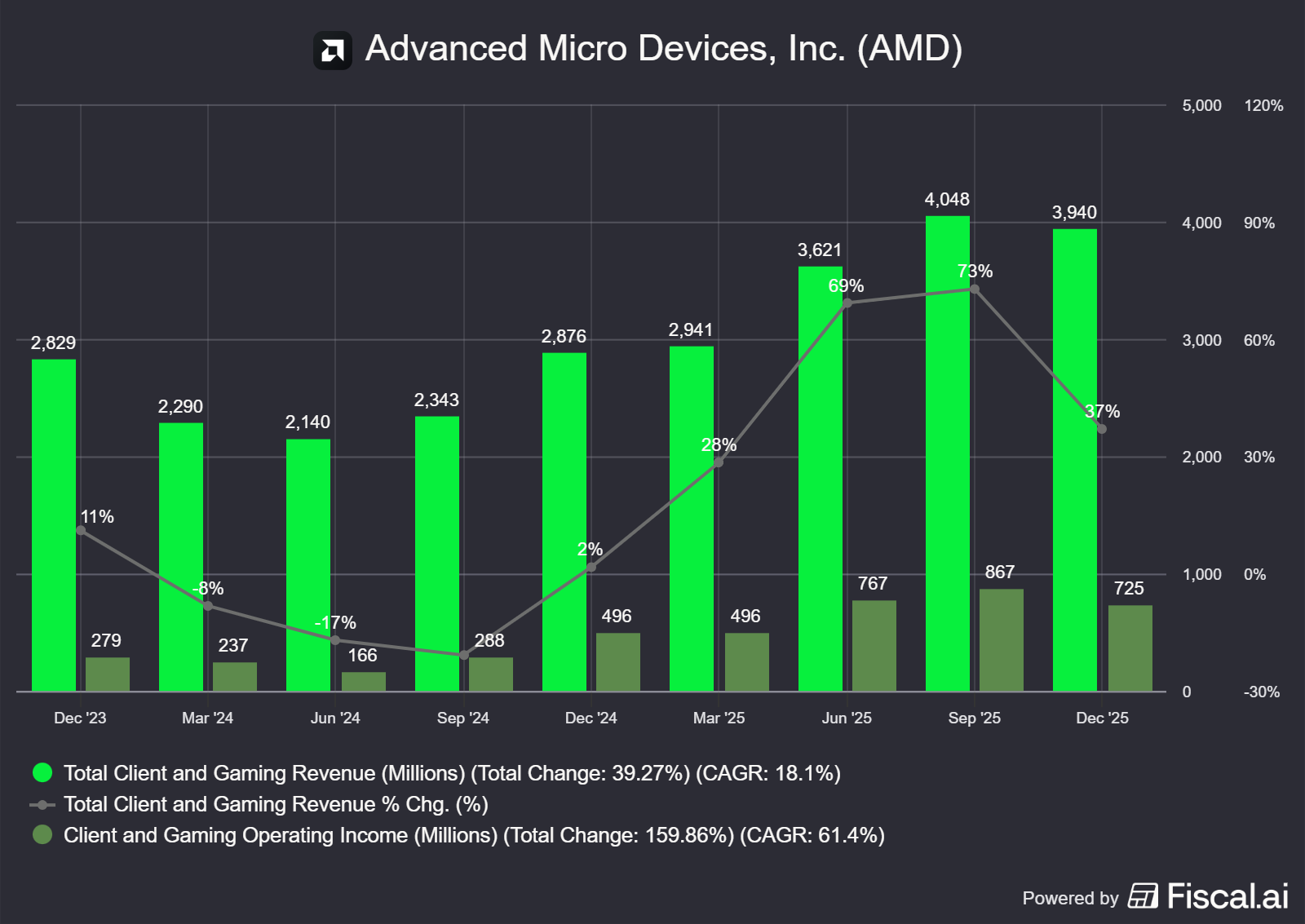

b. Client & Gaming

The combined Client & Gaming segment delivered revenue of $3.9 billion, up 37% year-over-year. Operating income was $725 million (18% margin).

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Client

The Client (PC) business was a standout performer, growing 34% year-over-year to a record $3.1 billion. This growth was driven by the Ryzen desktop and mobile CPUs as well as strong commercial adoption. Commercial PC sell-through grew by more than 40% year-over-year, marking a successful expansion into the enterprise notebook and desktop market.

Gaming

Gaming revenue saw a holiday boost, up 50% year-over-year to $843 million, driven by higher semi-custom revenue and Radeon GPU sales. However, management cautioned that as we enter the seventh year of the current console cycle, semi-custom revenue is expected to decline by a significant double-digit percentage in 2026.

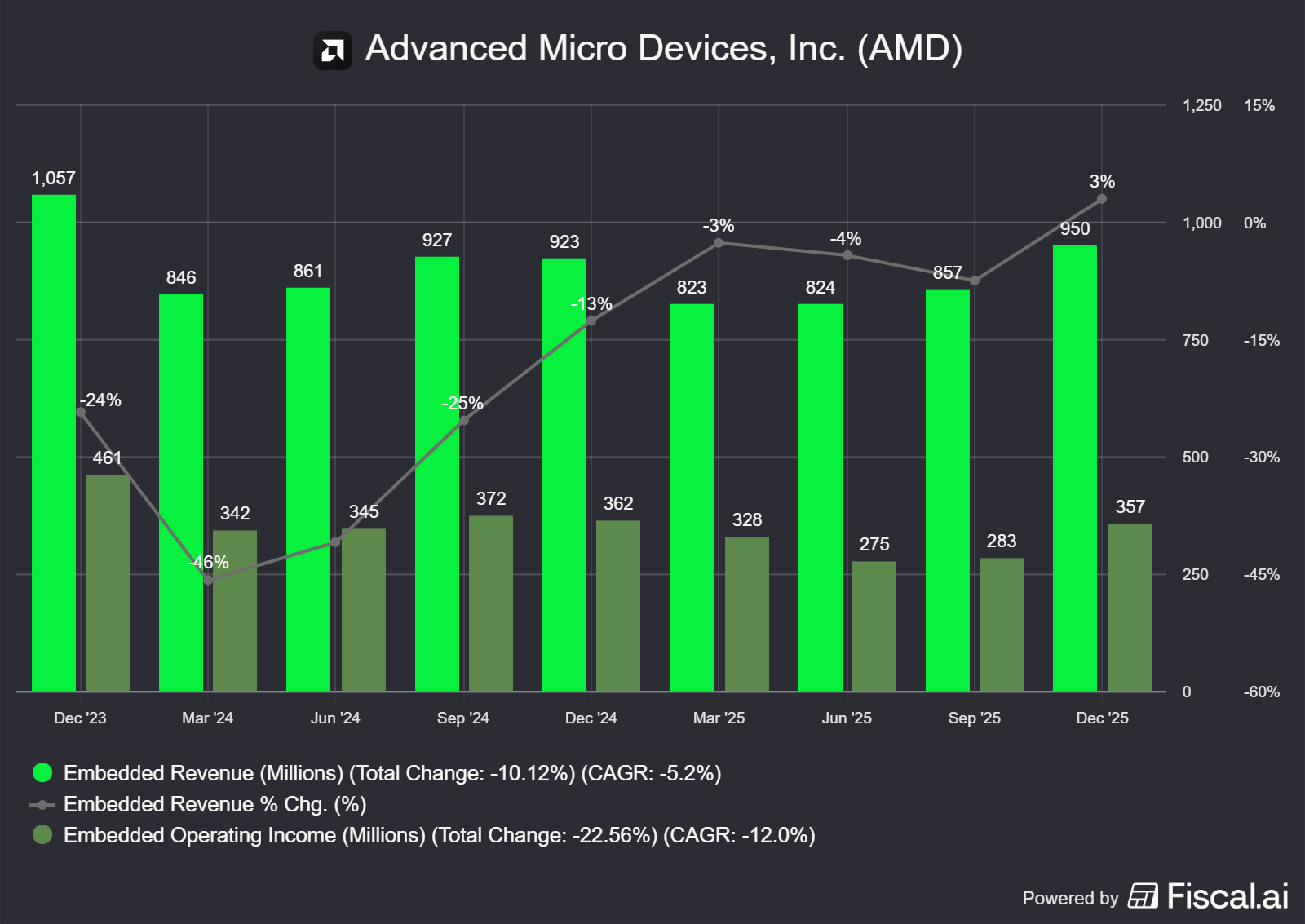

c. Embedded

After several quarters of correction, the Embedded segment has returned to growth. Revenue was $950 million, up 3% year-over-year and 11% sequentially. While the recovery is modest, the long-term indicators are strong. AMD closed $17 billion in design wins in 2025, up nearly 20% YoY, positioning the segment for sustained growth as inventory levels normalize across the industry.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

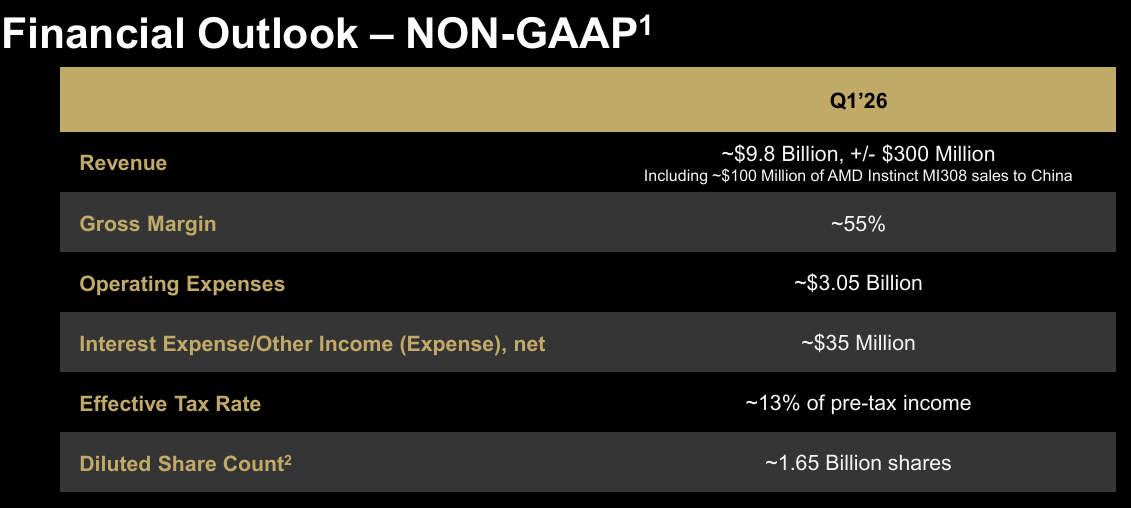

3. Outlook

For the first quarter of 2026, AMD expects revenue to be approximately $9.8 billion (+/- $300 million).

This represents 32% year-over-year growth.

Sequentially, this is a slight decline of ~5%, driven by seasonal decline. Management noted that Data Center is expected to grow sequentially, offsetting seasonal declines in Client, Gaming, and Embedded.

The guidance includes approximately $100 million of MI308 sales to China.

Non-GAAP gross margin is guided to be approximately 55%, and operating expenses are expected to be around $3.05 billion, reflecting continued aggressive investment in the AI roadmap. This implies a non-GAAP operating margin of approximately 24%, which is in line with Q1’25.

Source: AMD Earnings Presentation Q4’25

4. Conclusion

AMD closed 2025 with a strong performance, proving that its Data Center strategy is firing on all cylinders. EPYC CPUs have proven to be a “must-have” for new AI infrastructure, driven by the rise of agentic workloads, allowing AMD to exit the year with record server market share. Additionally, record revenue in both the Client and Data Center segments confirms that AMD is winning share in traditional markets while successfully ramping its AI business.

The market, however, remains skeptical that AMD can hit its ambitious long-term growth targets. Time will tell, but the upcoming launch of MI450 and Helios in the second half of 2026 will be the true test.