Ashtead Group – Renting is Flexible and Affordable

Every month we share 2-3 write-ups on companies we decided to examine as potential additions to our portfolio. Although the companies analyzed may tick most of the boxes, if the margin of safety is not considered sufficient, we will not initiate a position but rather monitor the stock.

At the end of each write-up, we will state whether we decided to buy the stock or not. If not, keep an eye to our Quarterly Portfolio Update releases in which we will update you for all the transactions that took place during the latest quarter.

The company in this week’s write-up is Ashtead Group (Ticker: $AHT.L), a leader in the equipment rental industry.

1. Key Facts

Description: Ashtead Group (“Ashtead”, “Company”) rents construction and industrial equipment across a wide variety of applications. Ashtead is North America’s second largest equipment rental company and operates in US, Canada and UK under the brand name Sunbelt Rentals.

Key Financials: Over the period 2012 to Q1’2023, the Company depicted a Revenue Compound Annual Growth Rate (“CAGR”) of 15.9% reaching a Trailing Twelve Month (“TTM”) revenue of c. $8.4B. Ashtead has a balance sheet with Cash and Short-term investments of $28 million compared to a debt and lease liabilities amounting to $7,744 million.

Price & Market Cap (as of 22nd November 2022): Its market cap is £22 billion with a 52-week high of £65.7 and a 52-week low of £32.7, whereas it currently trades at £49.9. Ashtead pays dividends since 1993 and its forward dividend yield stands at 1.3%.

Valuation: Ashtead trades at a TTM EV/EBITDA of 8.9 (10 Year average of 7.8) and at a TTM P/E of 19.8 (10 Year average of 17.9).

2. Who is Ashtead?

Ashtead’s durability speaks for itself; the Company has been around for 75 years, founded in 1947 in UK and listed in the London Stock Exchange in 1986. Since July 1988 (price data available on Yahoo Finance), Ashtead generated a compound average annual shareholders' return of c.18% including dividends. Over the years, Ashtead managed to grow and become the second biggest player in North America’s equipment rental industry behind United Rentals. The industry has been undergoing consolidation for years and Ashtead engaged in a high number of acquisitions to gain market share.

From 2011 until April 2021, Ashtead went for 103 acquisitions in North America and paid an average EBITDA multiple of 5.2x for 96 acquisitions (under $100M deals) and 6.1x for 7 acquisitions (above $100M deals).

One of the most significant acquisitions in the Company’s history has been NationsRent Companies, Inc for $1B in 2006. At the time, NationsRent was the 6th largest provider of rental equipment in the US and by paying 1.4x sales and 5x EBITDA for NationsRent, Ashtead became the 3rd largest player.

3. Business overview

At its most basic, our model is simple – we purchase an asset, we rent it to customers through our platform and generate a revenue stream each year we own it (on average, seven years) and then we sell it in the second-hand market and receive a proportion of the original purchase price in disposal proceeds. Assuming we purchase an asset for $100, generate revenue of $55 each year (equivalent to 55%-dollar utilisation) and receive 35% of the original purchase price as disposal proceeds, we generate a return of $420 on an initial outlay of $100 over a seven-year useful life. We incur costs in providing this service, principally employee, maintenance, property and transportation costs and fleet depreciation. Ashtead Group, Annual Report 2022.

Customers

Ashtead offers industrial and construction equipment for rent on a short-term basis to a diversified base of customers like construction, industrial and homeowner customers, service, repair and facility management businesses, emergency response organizations, event organizers, as well as government entities such as municipalities and specialist contractors.

The Company serves 800.000+ customers with its largest reporting segment being the US. In 2022, Sunbelt US served 710,000 customers who generated an average annual rental revenue of $8,500 each indicating a highly fragmented customer base.

Markets

In terms of geographic mix, 81% of Ashtead’s FY22 revenue was from US, 12% from UK and 6% from Canada. The latest reported number of Ashtead’s locations/stores are 991 in the US, 93 in Canada and 181 in the UK. The below table highlights some of the key characteristics of each market.

Source: StockOpine Analysis, Ashtead Annual Reports and Quarterly Earnings Presentations

* Trailing 12-month rental revenue divided by average fleet size at original cost measured over a 12-month period

The reduction of locations in the UK is part of management’s plan to migrate to a regional operating center model with fewer but larger locations.

Ashtead’s largest market is construction and represents 40% of the business (55% in FY2007) whereas non-construction business continues to expand by growing the Company’s specialty business. Non-construction related activity like live events, building maintenance, municipal activities and emergency response are typically less cyclical than construction.

General Tool and Specialty segments

In the US, Ashtead operates through General Tool and Specialty rental locations. The General Tool business includes equipment which is more directly related to construction like earth moving, forklifts, mobile elevating platforms, etc.

The specialty rental business consists of products with low rental penetration in predominately non-construction facing markets. Specialty includes the below businesses:

Power and HVAC

Climate control and Air Quality

Scaffold services

Flooring solutions

Pump Solutions

Lighting, Grip and Lens

Ground Protection

Industrial Tool

Shoring Solutions

Temporary Structures

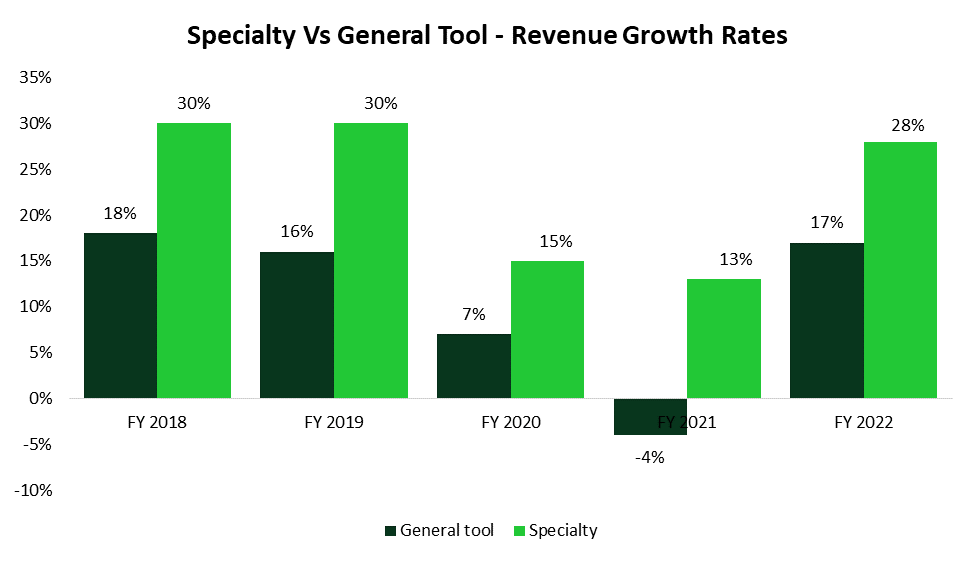

The addition of Specialty stores enables Ashtead to differentiate itself and diversify its customer base and its end markets. Specialty is growing faster than the general tool business and accounted for approximately 30% of North America revenue in 2022 compared to 22% in FY2018.

According to Ashtead, specialty segment has $6B+ revenue potential and plans to increase segment revenue to $2.4B by 2024 ($2B in FY22) under its current strategic roadmap, Sunbelt 3.0.

Source: StockOpine Analysis, Ashtead Quarterly Earnings Presentations

Sunbelt 3.0 (April 2021 – 2024)

In April 2021, Ashtead launched its new strategic plan, Sunbelt 3.0. On a high level the growth plan communicated the following:

Add 298 (126 general tool and 172 specialty) locations across North America bringing the total to 1,234 by 2024. As of July 2022, Ashtead added 88 locations through greenfield openings and 35 through acquisitions.

Transform the UK business to deliver sustainable margins and returns.

Grow specialty business revenue from $1.4 billion to $2.4 billion. Specialty revenue was c.$2billion in FY22.

Grow the general tool business at 9% CAGR (55% from existing locations and 45% from greenfield openings).

4. Equipment rental industry

The equipment rental industry is primarily driven by construction activity, although rental penetration increased over the years to areas like theme parks, building maintenance, live events, movies, and television production. Hiring of equipment provides a number of benefits for customers as it frees up capital and provides access to skilled labor and technologically advanced equipment. Hiring of equipment is also the preferred choice in periods like today where economic uncertainty and cost of raising capital is high.

The industry has been undergoing consolidation with large players overtaking smaller ones and gaining significant scale advantages. The three leading rental equipment players in the US are United Rentals, Ashtead (Sunbelt), and Herc Rental which hold 16%, 12% and 4% of the market respectively.

Source: Statista

This compares to 4% and 5% market share for Ashtead and United Rentals respectively back in 2010. High fragmentation of the industry is evident by the remaining players’ market share, with the top 4-10 players holding 7%, top 11-100 holding 17% and the rest holding 44%.

Source: Ashtead First Quarter Results FY23 presentation

According to the American Rental Association (ARA), the US market of equipment rental is expected to grow by 11.2% to exceed $55.9 billion in 2022. ARA expects equipment rental revenue to grow by 6.2% in 2023, 2.5% in 2024, 3.3% in 2025 and 3.7% in 2026, reaching more than $65.1 billion.

In Canada, ARA forecasts equipment rental revenue to grow by 14.4% to $4.7 billion in 2022 and reach $5.4 billion by 2026. Ashtead’s market share in Canada according to management estimates, stands at 8% and is the second biggest player behind United Rentals which holds 18% share.

The UK equipment rental market is estimated at £6.6 (c. $7.8) billion and is expected to decline by -1.3% in 2022. Ashtead is the largest equipment rental company in the UK with a 10% market share.

Competition

Comparing the 3 key players, namely, United Rentals, Ashtead (Sunbelt) and Herc Rentals, Ashtead portrays better financial metrics. For instance, revenue and operating income CAGR in latest 8 fiscal years (“FY”) is 14.2% and 14.3%, respectively, well above the 8.8% and 9.2% of United Rentals and the 2.2% and 4.3% of Herc Rentals.

For the latest 5 fiscal years, United Rentals and Ashtead show similar margin profile with an average operating margin of 24.3% and 25.1%, respectively, whereas Herc with an average of 11.8%, lacks behind peers. It shall be noted that both United Rentals and Ashtead had a lower margin in the latest FY compared to the first FY of the analysis by c. 200bps, whereas Herc Rental increased its operating margin from 6% back in 2017 to 18.2% in 2021.

The growth of these companies is mainly funded through net capex (purchase of rental & non- rental equipment less proceeds from disposal) and acquisitions. In the latest 5 FY (excl. 2020) it is shown that Ashtead mainly funds growth through CAPEX (average of 27.4% over sales) compared to acquisitions of 11.9%, Herc with effectively only CAPEX (25.2% of sales) with the exception of 2021 where acquisitions spiked from near 0 to 20.8% of sales, and United Rentals uses an equal proportion of CAPEX and acquisitions (19.3% and 22.5%, respectively).

We cannot conclude whether one funding method is superior to the other as Returns on Capital (“RoC”) (latest 5 fiscal years) vary irrespective of method used, with United Rentals, Ashtead and Herc averaging at 9%, 11% and 4.9%, respectively. Although Ashtead seems to be superior, it shall be noted that it is the only company from the peer group that had a considerable decline compared to the first period under review (from 12.7% to 10.8%). This is not necessarily a cause of concern since returns are impacted by Koyfin calculation method which uses opening capital and in periods where a significant acquisition takes place, the RoC might be inflated as earnings include consolidated results. Therefore, average periods better serve for comparisons (though it should be monitored).

Source: Koyfin, StockOpine analysis | Note: Data represent latest fiscal year (Dec 31, 2021, for United Rentals and Herc Holdings, Apr 30, 2022, for Ashtead), Total Investments = Net CAPEX + Acquisitions

Going forward, Ashtead and United Rentals seem to be better positioned to take on leverage to fund their growth if needed since the Net Debt / EBITDA ratio (TTM) stand at 2.0x (2.0x in latest FY) and 2.9x (3.5x in latest FY), respectively, compared to 5.3x (5.0x in latest FY) of Herc. This is further justified by TTM Interest coverage ratio (EBIT / Interest Expense) which stands at 7.2x (7.0x in latest FY) for Ashtead, 7.7x (5.9x in latest FY) for United Rentals and 4.8x (4.4x in latest FY) for Herc.

5. Financial Analysis

As stated above, Ashtead had a Revenue CAGR of 15.9% for 2012- Q1 2023 (“Historic Period”) while profits and free cash flows were growing at a faster rate reaching an Operating Margin (“OPM”) of 24.7% and a Free Cash flow (“FCF”) margin of 9.5%.

Source: StockOpine Analysis, Ashtead Annual filings

Due to the above growth observed, Revenue increased from $1.8B in 2012 to $8.4B in Q1 2023 on a TTM basis, Operating income from $290M to $2.1B and Free Cash Flow from a negative $20M to a positive $796M.

Revenue growth was driven by rental rate increases, greenfield openings, and bolt-on acquisitions. During FY2022 Ashtead grew revenues by 20% of which 16% was through same-store sales and greenfield openings while 4% was through acquisitions.

Growing revenues and market share over the years required large amounts of CAPEX and funds spent on acquisitions. During the last ten years, Ashtead spent $13.9B in CAPEX and $4.9B in business combinations, whereas its returns on capital averaged at 11% (last five years), the highest among its peers.

Although FCFs demonstrate a significant improvement since FY 2017, when the business acquisitions are deducted, revised FCFs remain roughly at 0 (even negative) levels. Effectively, the expansion funding method shifted from mainly CAPEX (average of 37% over sales for FY12 - FY16 and acquisitions of 5.1%) to a mix of the two (CAPEX average for FY17-FY22 of 25% over sales and acquisitions of 10.6%).

We do not expect significant changes in revised FCFs as the model is capital intensive and to get from a 12% market share to a +20% in the future, will require considerable investments. As long as it grows profitably and its returns on capital remain above peers, we are confident that Ashtead will remain a key player in the industry. The real risk for shareholders is overpaying for acquisitions.

The high FCF margin observed in FY21 (1 May 2020 – 30 April 2021) of 27% was impacted by the pandemic and the negligible growth CAPEX investments resulting to a CAPEX / Sales of 8.5%.

Ashtead’s net debt is $7.7B, representing c.29% of market cap and c. 146% of book value of total equity. The resulting ratio of net debt to EBITDA was 1.6x (2x if we include the effect of IFRS 16) as of July 2022, within the target excluding the effect of IFRS 16, of 1.5x to 2.0x. As indicated above, this ratio is the lowest among peers. Additionally, operating profits sufficiently cover interest expenses with an average interest coverage over FY18-FY22 of 7x (TTM of 7.2x) and thus the default risk is low.

6. Competitive advantages, Opportunities and Risks

Competitive advantages

One of the most prominent competitive advantages of the two key players in the industry is their scale. Scale provides cost benefits like access to equipment from OEMs (Original Equipment Manufacturers) at lower prices and cost efficiencies due to their dispersed locations which can provide efficiencies in expenses like transportation. In addition, during periods of rising interest rates and uncertain future economic conditions, it would be much easier for the two large players to fund future growth opportunities through raising capital. On top of the above, the high capex requirements of the industry, act as barriers of entry further strengthening the competitive positioning of the top two.

Opportunities

In the US, we are undergoing a period of planned increases in infrastructure spending. $1 trillion US Infrastructure bill, transformation of the automotive manufacturing plants to support electric vehicle production as well as the CHIPS Act are some of the large-scale infrastructure developments that stand to benefit the industry. In addition, increased economic uncertainty along with scarce skilled labor would possibly increase rental penetration. During periods of high uncertainty, more companies would consider rental as an alternative to significant capex investments.

Risks

Ashtead’s largest end market is construction which is cyclical and generally lacks economic cycles by 12-24 months. If the economy slows down, it is possible that demand for Ashtead’s services will fall as well. Even though non-construction markets provide some form of diversification, it would not be enough for the Company to stay unaffected.

Furthermore, the top two players in the industry are highly engaged in acquisitions in competing for market share, therefore, there is a risk of diminishing returns on capital if management overpays for those acquisitions in pursuing higher market share.

7. Valuation

The stock price as of 22nd of November 2022 stands at £49.9 and is down by 15% YTD. The market cap of the Company stands at £22B and trades at an EV/EBITDA TTM multiple of 8.9x. Based on our DCF valuation the estimated price of Ashtead Group stands at £43.7, which is below the current price level by 12.6%, with a resulting IRR over a 5-year period of 7.4%.

Source: StockOpine analysis

To estimate the fair value of Ashtead we assumed a revenue CAGR of 9%. For FY 2023, rental revenue growth, we used 15.4% which is line with guidance provided by management in Q1’23. Beyond FY2023, we estimated rental revenue growth rates based on industry expectations, applying a factor of 2x for US and 3x for Canada to account for market share gains.

Per our view, this is reasonable given the recent expansion in Canada and the long-term goal of achieving 20% market share in US. Based on our assumptions, market share in the US increases from 12% to 15% in FY 2027 whereas for Canada it increases from 8% to 11%.

In terms of profitability, we used an average projected EBITDA margin of 48% and a terminal EBITDA margin of 48.3%. Both average and terminal EBITDA margins are higher than the average 5-year EBITDA margin for 2018 - 2022 of 46.3%, however, our assumption accounts for a gradual improvement in margins similar to Company’s execution as of today. In addition, both average and terminal EBITDA margins are within the target range of 47-49% set by management for FY24.

To derive the free cash flows to the firm we deducted projected Capex requirements of $3.3 billion or 36% of revenue for FY23, in line with management guidance. Beyond FY23, we gradually reduced capex requirements to 28% in line with its FY17-FY22 average, excluding FY21, for which capex was impacted by COVID-19.

In respect to the terminal EV/EBITDA multiple, it is assumed to be around 7x which equals its 5-year average excluding FY21.

To calculate the value per share we used the minimum required return that we aim to obtain from our investments (i.e., 10%) under the current environment, adjusted for net debt and non-operating assets / liabilities identified and thereafter divided the resulting value by the number of shares.

Based on the above calculations and assumptions used (which of course may not materialize at all), we reach a value per share of £43.7, which is below the current price of £49.9, resulting in an IRR over a 5-year period of 7.4%.

Sensitivity analysis

The below table gives an indication of the potential upside/(downside) %age compared to the current price (£49.9 as of 22nd November 2022) when the terminal multiple and the discount rate are changed.

Source: StockOpine analysis

8. Concluding Remarks

There is a lot to like about Ashtead, large and fragmented industry undergoing consolidation, durability of the business model, strong track of execution, scale advantages and high industry barriers of entry.

Although Ashtead makes a good fit to our portfolio, the stock appears pricey at this level considering our estimate of the Company’s fair value. In that respect we would not be buyers here and we will reconsider our decision in case the stock falls close to £40.

You can find us at Commonstock and on Twitter @StockOpine.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward-looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

This post may contain affiliate links, which means that we might get a commission if you decide to sign-up using any of these links. No extra cost is charged to you.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.

Nice write-up. What are your thoughts on clustering & how that has improved economics & provided a platform to distributed more specialty equipment in a geographic area with a small amount of incremental investment & thus large incremental margins? Also, the strategy of green fielding locations that are clustered to gain market share & using M&A to enter new markets. Equipment rental is a local market share business thus Ashtead can have higher RoA than larger competitors like URI if its local market shares are greater than URIs. IMO your cap-ex estimates include growth cap-ex which has generated the 20%+ growth & does not include the affects of disposals. If you make those adjustments I get a terminal cap-ex of 19% of sales for replacement cap-ex only (as would be implied in a terminal value). The historical 5-yr FCF margins are at 10% including growth cap-ex and 29% before acquisitions (see latest investor presentation page 28). So IMO your terminal FCF margins (AT) should be somewhere between 10% and 29%. Using a current EBITDA multiple in terminal assumes that the terminal will have same capital intensity as today when the company is in high growth mode. This will not be the case for Ashtead so using a terminal multiple of FCF or adjusted NI may be more appropriate.