Ashtead: “Our business is positioned to win in the near, medium and long term”

Ashtead delivered, but faced a harsh day negative reaction of 9.4%, attributed to missing EPS expectations by 3 cents or 3.77%. Is this drop justified? In light of our recent article released on February 15th Ashtead: Building Success Brick by Brick, we feel it's necessary to update you with our thoughts.

a. Highlights Q3’24 (ended 31 January 2024)

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers; if you are a paid subscriber, you can benefit from a 3-month free trial) | *$4M miss or 0.35%.

Revenue of $2,658 million, a YoY constant currency growth of 9%. For comparison, United Rentals reported a revenue growth of 13.1% in its quarter ended December 31, 2023, or 7.5% when adjusted for the Ahern deal from last year.

Rental revenue of $2,356 million, a YoY constant currency growth of 7%.

EBITDA of $1,168 million, a YoY constant currency growth of 7%.

Operating Profit of $591 million, a YoY constant currency decline of 3%.

Adjusted EPS of 81.4 c, a YoY constant currency decline of 11%.

b. Other relevant financials

The Net Debt to EBITDA ratio, excluding IFRS 16, increased to 1.9x compared to 1.8x in October 2023, remaining within the target range of 1.5x to 2.0x. This increase was primarily driven by additional capex of $1.2 billion in the quarter and 10 additional bolt-on acquisitions totaling approximately $200 million. Although Free Cash Flow (FCF) remains negative due to accelerated investments, improvements are anticipated in FY2025 as management plans to reduce capex by about $590 million.

It’s worth noting that there are no financial health issues as the availability of $2.2 billion exceeds $450 million, thus eliminating the need for covenant monitoring.

Added an additional 32 North American locations, with 19 acquired through acquisitions.

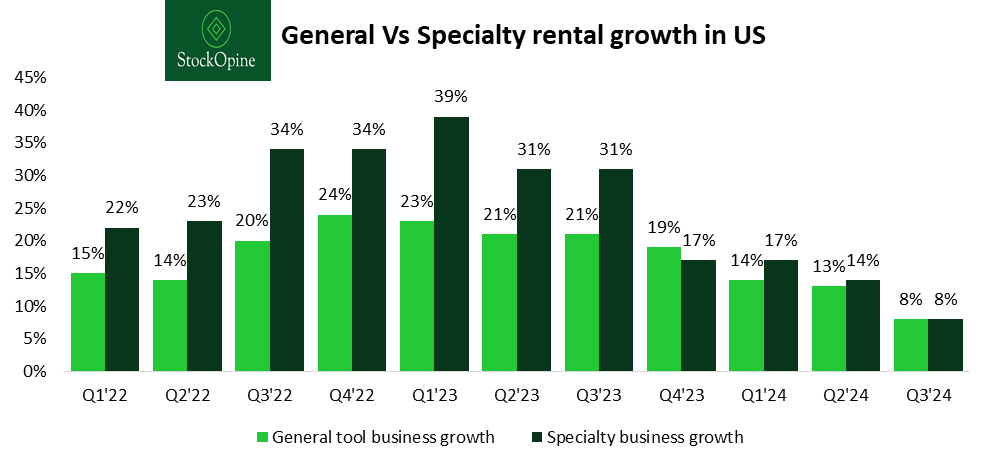

The Specialty mix, a margin accretive segment, experienced a single-digit growth of 8%. While this growth may not seem impressive, it is attributed to the lower occurrence of large-scale emergency response work related to natural disasters in North America. Given the low rental penetration in specialty, we anticipate a reacceleration of growth over the medium term.

Source: Ashtead Investor’s Presentations, StockOpine analysis

If you'd like to share your feedback with us and ensure that your voice is heard, please take a few minutes to complete this survey.

Regional EBITDA margins decreased for North America and Canada, with Canada experiencing a more pronounced year-over-year impact, falling to 35.5%, its lowest level since 2022 and well below the long-term target of 40%-45%. The primary reason for this decline is attributed to the impact of the Film & TV business. Excluding this, management claims an improved EBITDA margin compared to last year over the last 9 months.