ASML Q1 2026: Surging EUV Demand Drives Guidance Hike

Accelerated capacity expansion, surging Low-NA productivity, and the maturation of High-NA EUV

ASML started 2026 with a solid first quarter, as total net sales and gross margin landed at the high end of guidance. The results confirm that the semiconductor industry’s growth outlook is solidifying, driven primarily by ongoing AI-related infrastructure investments that are pushing demand for advanced chips beyond current supply.

a. Results: Strong Execution Amid High Demand

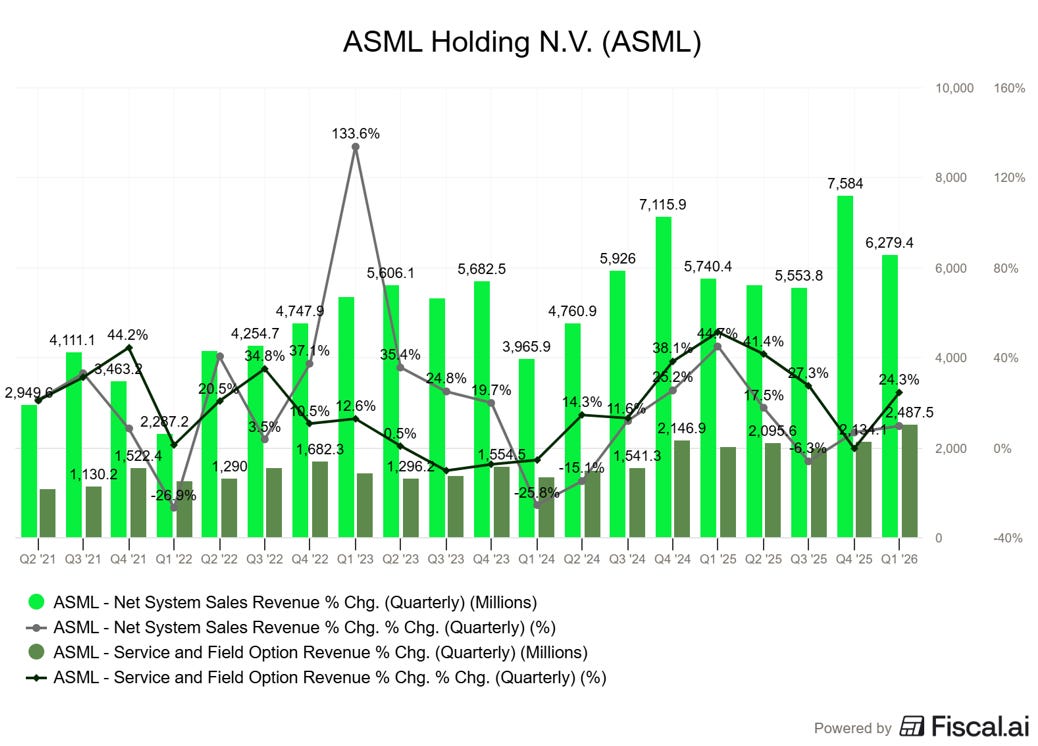

ASML delivered Q1 2026 total net sales of €8.8 billion, up 13% year over year. Net income grew 17% YoY to €2.8 billion. The Installed Base Management segment, which includes service and field options, performed strongly at €2.5 billion (+25% YoY), driven by the expanding EUV installed base and high-margin performance upgrades requested by customers to increase immediate output.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

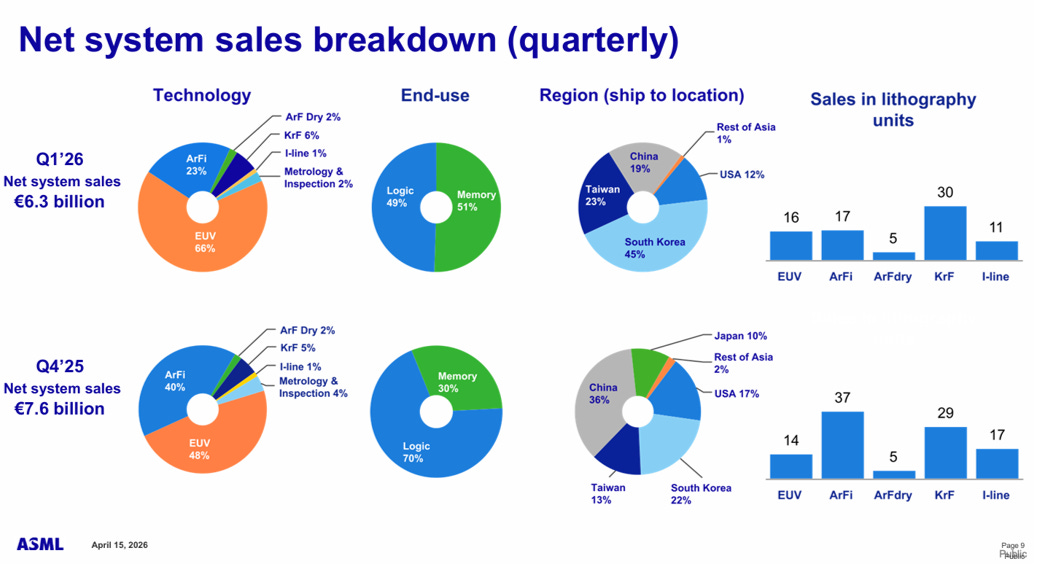

In Q1 FY26, Net System Sales reached €6.3 billion, marking a 9% year-over-year increase. A significant driver of this growth was the EUV segment, which contributed €4.1 billion (approximately 65% of total sales), including revenue from two High-NA systems. This represents a substantial 28% increase in EUV revenue compared to the previous year. Despite a modest 3% rise in unit volume, EUV sales were primarily increased by higher ASP, as previously noted by the management. Sales of non-EUV (DUV) systems accounted for the remaining €2.1 billion. Memory captured the majority of net system sales at 51%, versus logic at 49%. This reflects the accelerating adoption of EUV in DRAM, as customers shift aggressively to gain performance and capacity.

“The reason for that is, of course, performance, but it’s also capacity, because if you are going to use more EUV layers, you are going to need less multi-patterning. Multi-patterning takes a lot of space also in the fabs. I think this is also definitely another argument in favor of EUV. I think this was mentioned, by the way, by this U.S. customer in their call.” - Christophe Fouquet, CEO

Source: Q1’2026 earnings presentation

China’s share of net system sales fell sharply to 19% in Q1 2026 (from 36% in Q4 2025), consistent with management’s expectation of ~20% for the full year, in line with backlog composition. This regional decline was effectively countered by a surge in South Korea, which jumped to 45% of total sales, highlighting ASML’s reduced vulnerability to export controls in China. A global shortage of high-end memory is forcing companies like Samsung to accelerate their equipment orders.

The gross margin reached 53.0%, supported by a very high-margin mix in the service and upgrade business.

Below the paywall, we dive into ASML’s upgraded outlook, critical technology developments, and what this means for the stock’s long-term trajectory…