ASML Q2'26: Accelerating Demand Drives Another Guidance Raise

Record installed base sales, capacity expansion plans, and High-NA EUV reaching a critical production milestone.

ASML continued its strong momentum into the second quarter of 2026, delivering top-line results and gross margins that comfortably exceeded the company's own guidance. The quarter's outperformance underscores that ongoing AI-related infrastructure investments are driving an insatiable need for advanced computing capacity, cementing a long-term growth trajectory that ASML is positioned to fulfill.

a. Results: Outperforming on High-Margin Upgrades

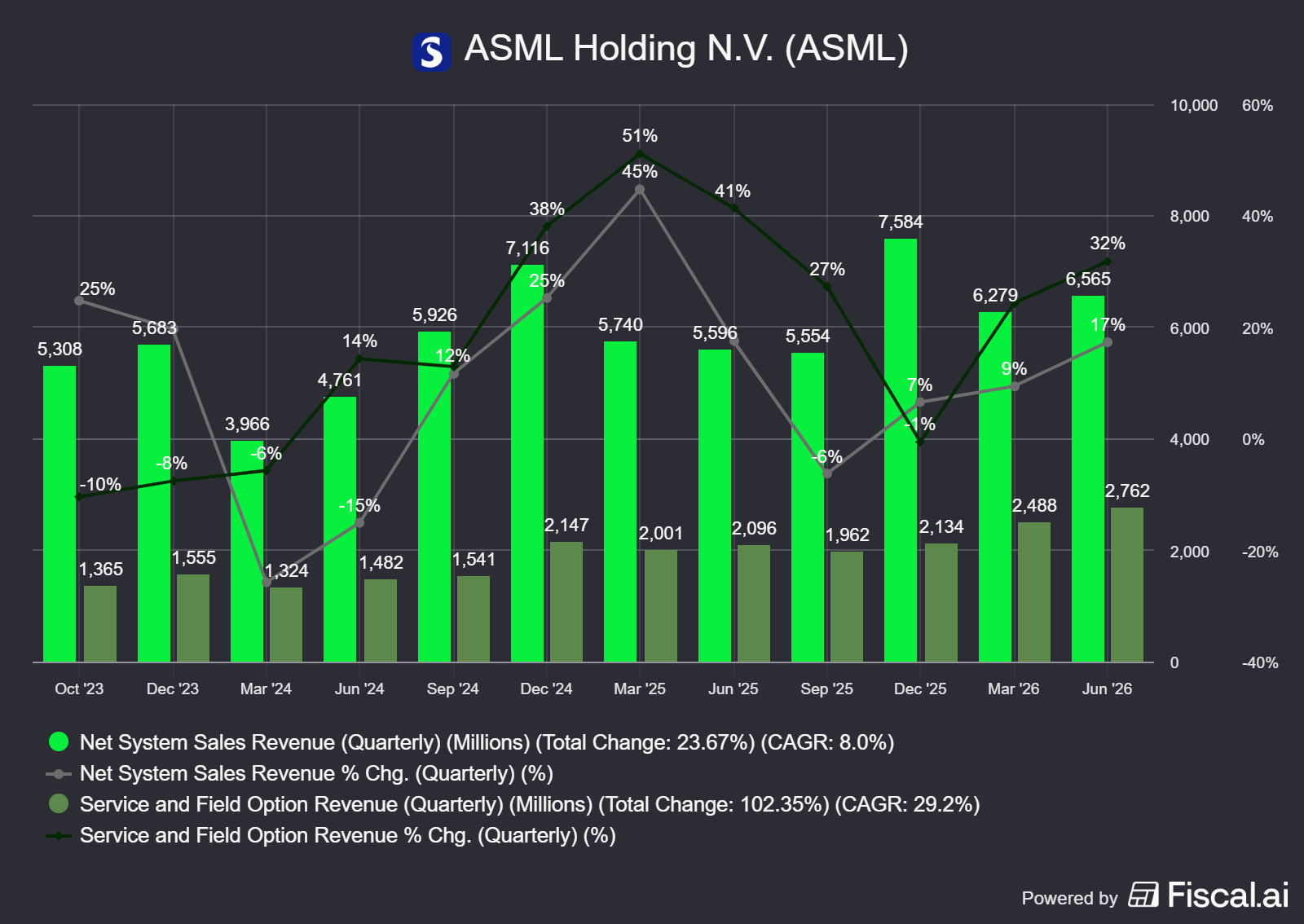

ASML reported Q2 2026 total net sales of €9.3 billion, which landed above the high end of their guidance. Net income reached €2.9 billion, representing 31.3% of total net sales, and resulted in earnings per share of €7.59.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

A standout for the quarter was the Installed Base Management segment, which surged to €2.8 billion, almost €300 million above management’s expectations. As customers push to maximize output from their existing lines to meet demand, high-margin productivity upgrades are driving significant immediate value.

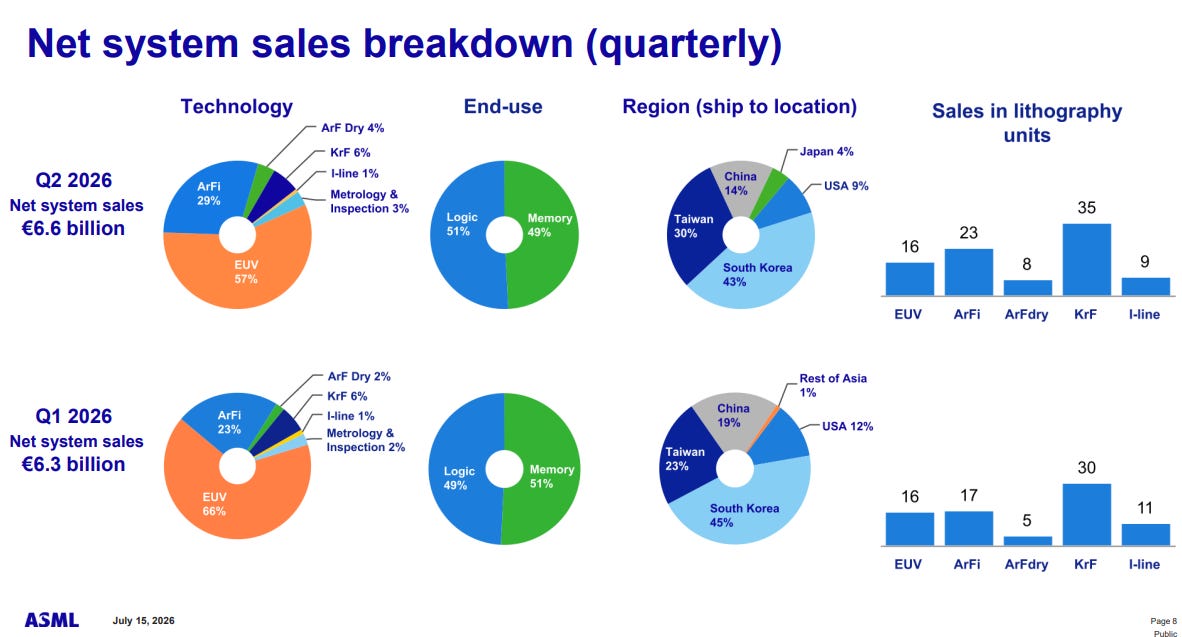

In Q2 2026, net system sales reached €6.6 billion. This included €3.8 billion from EUV system sales and €2.8 billion from non-EUV system sales. End-use was almost equally split, with logic capturing 51% of net system sales and memory taking 49%. The gross margin came in at a strong 54.0%, beating guidance, driven primarily by the favorable mix of very high-margin components within the Installed Base Management business.

Source: ASML Q2’26 Earnings Presentation

b. Outlook: Raising the Bar (Again) for 2026

Given the sustained order momentum and clear visibility provided by long-term customer commitments, ASML has updated its full-year 2026 guidance.

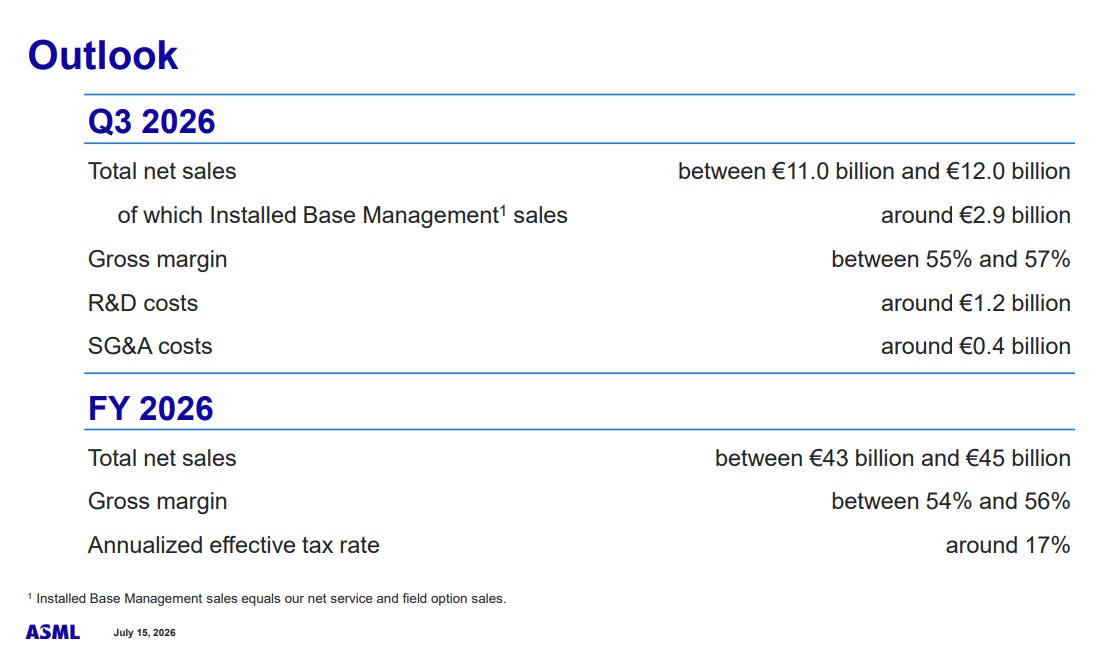

The company now expects total net sales for 2026 to be between €43 billion and €45 billion, a ~16% increase from the prior target. Full-year gross margin expectations are now set between 54% and 56%. This growth is fueled by advanced logic and memory customers entering long-term agreements and aggressively adding capacity. As a result, ASML anticipates memory-related net system sales to grow by over 75% this year, while advanced logic/foundry is expected to grow over 25%.

For the third quarter of 2026, ASML projects:

Total net sales: Between €11.0 billion and €12.0 billion.

Installed Base Management: Around €2.9 billion.

Gross margin: Between 55% and 57%.

Operating costs: R&D expenses are projected at around €1.2 billion. SG&A costs are expected to be around €0.4 billion.

Source: ASML Q2’26 Earnings Presentation

c. Technology: Scaling Capacity and High-NA Production Milestone

ASML is scaling its operations aggressively to ensure supply can meet this structural demand, with visibility now extending multiple years.

EUV Capacity Expansion: ASML expects