ASML delivered a blockbuster end to 2025, beating expectations with record bookings that signal a strong cycle. Driven by insatiable demand for AI infrastructure, customers are aggressively securing capacity for the next generation of semiconductor manufacturing.

⚠ This week marks 3 years since we launched our paid research. To celebrate this milestone, we are offering a 33% discount on all subscriptions (Monthly & Annual) for the next 7 days.

If you have been waiting for the right moment to upgrade, this is it. Lock in the rate and get full access to our deep dives, financial models, and portfolio updates.

a. Results: A Record-Breaking Quarter

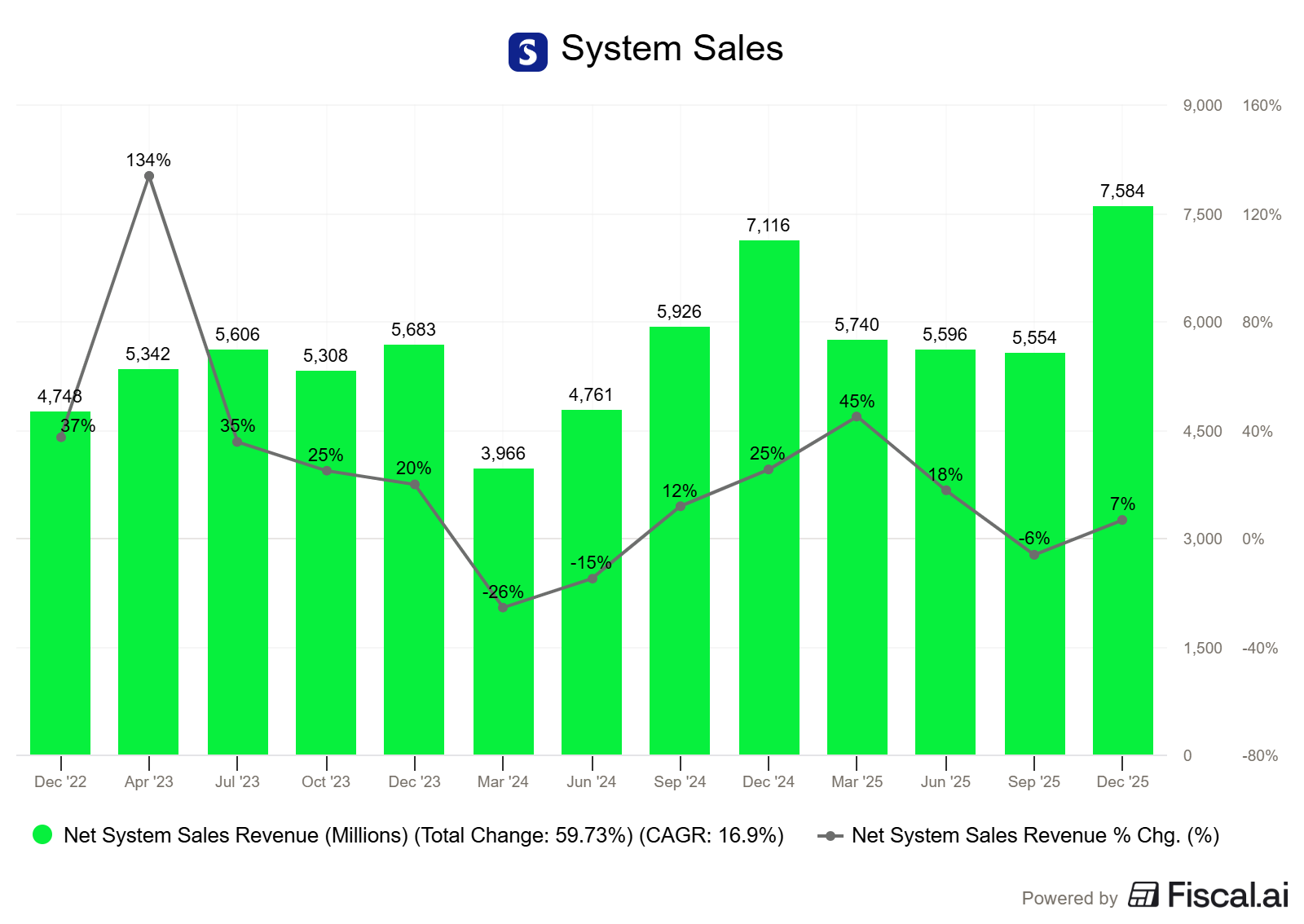

ASML reported Q4 2025 net sales of €9.7 billion, which sits at the higher end of their guidance and reflects a substantial jump from €7.5 billion in Q3. This was largely driven by the EUV systems.

Net System Sales: Reached €7.6 billion, with EUV accounting for 48% of the mix (vs. 38% in Q3). EUV includes the recognition of revenue for two High-NA systems.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

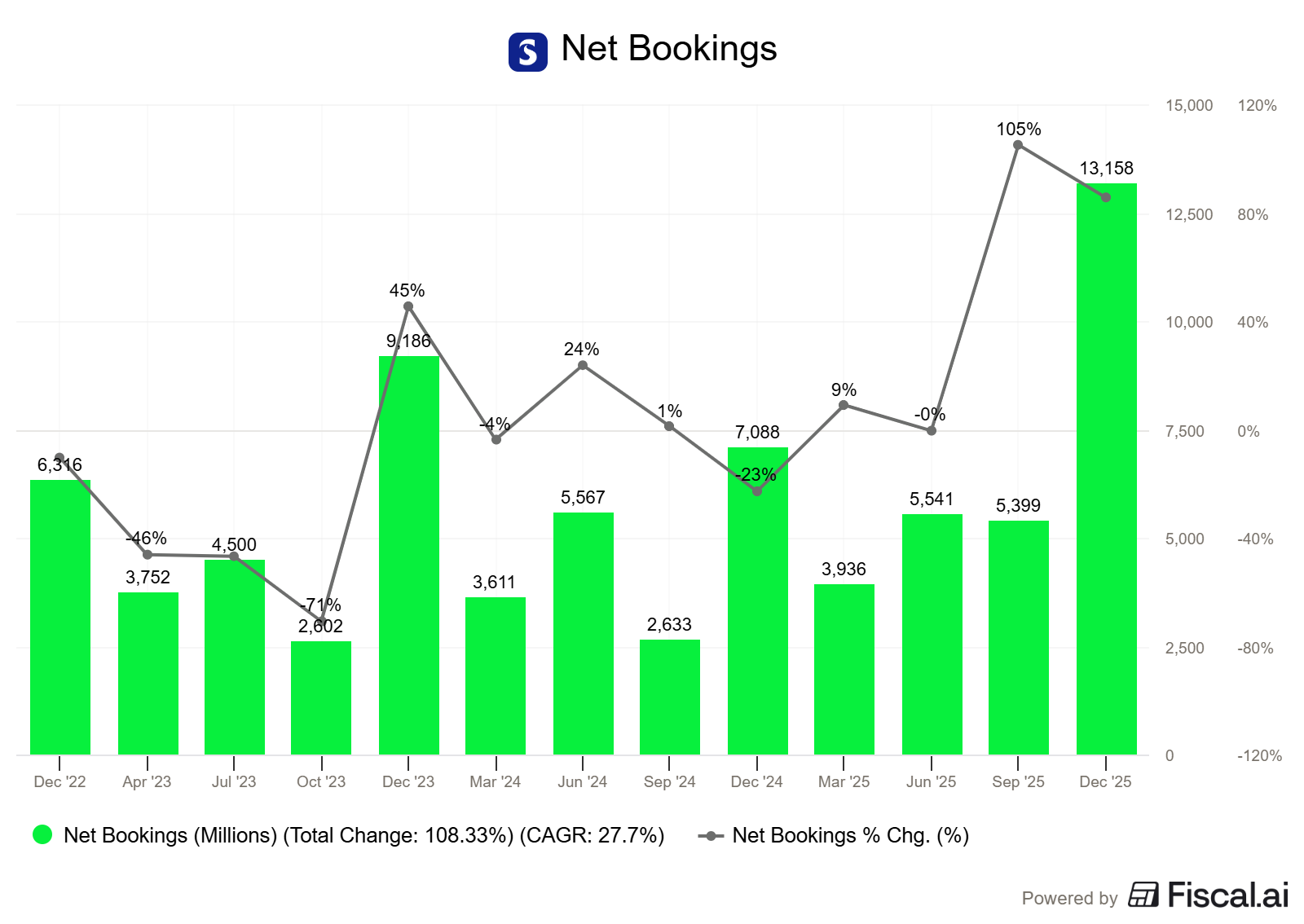

Bookings: The headline number was the record net bookings of €13.2 billion (vs. €5.4 billion in Q3). This included €7.4 billion in EUV orders alone, a clear signal that customers (Logic and Memory) are aggressively preparing for 2nm and advanced DRAM nodes.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

For the first time in recent memory, Memory bookings (56%) surpassed Logic (44%), driven by frantic demand for HBM (High Bandwidth Memory) and DDR5 to support AI workloads.

The gross margin came in at 52.2%, up from 51.6% in Q3, landing comfortably within guidance despite the dilutive impact of early High-NA system recognition. Net income was €2.8 billion, representing 29.2% of sales.

b. Backlog & Services

While the headline revenue figures grab the attention, two underlying metrics confirm the durability of this cycle:

Record Backlog: The order book ended the year at a massive €38.8 billion. The quality of this backlog is pristine. EUV systems now account for €25.5 billion (or 66%) of the total, providing visibility for 2026. Furthermore, the risk of cancellations from China has largely dissipated, as the region now represents only ~20% of the backlog, aligning future revenue with a more sustainable geographic mix. For context, China sales accounted for 33% in 2025 and 36% in Q4’25.

“As part of the outlook for non-EUV, we expect the China region's share in our total net sales in 2026 to be in line with our current system backlog, which is around 20 percent.” - Christophe Fouquet, CEO

Installed Base Management grew 26% YoY to €8.2 billion in FY25. CFO Roger Dassen highlights upgrades as “the easiest and fastest way for customers to get additional output capacity” in a supply-constrained market. The momentum continues into Q1’26 with expected sales of ~€2.4 billion (implied +20% YoY), driven by “increasing service revenue from our growing installed base of EUV systems” and strong “appetite for upgrade business” to solve short-term capacity needs.