Beyond the Ecommerce Behemoth: Examining Amazon's Diverse Business Ventures

Every month we share 2 write-ups on companies we decided to examine as potential additions to our portfolio. Although the companies analysed may tick most of the boxes, if the margin of safety is not considered sufficient, we will not initiate a position but rather monitor the stock.

In case we decide to initiate a position at any time, we will share an Investment Thesis memo. For any additions to existing positions we will update you through our Quarterly Portfolio Updates.

1. Key Facts

Description: Amazon.com Inc. (“AMZN”, “Amazon”, “Company”) is a multinational technology company that operates in various segments such as e-commerce, cloud computing and digital streaming. It is best known for its online retail marketplace, Amazon.com, which offers a vast selection of products and services to customers worldwide. The Company as of December 2022 employs 1,541,000 people.

Key Financials: Over the period FY13 to FY22, the Company depicted a revenue Compound Annual Growth Rate (“CAGR”) of 23.9% and operating income CAGR of 36.5%, reaching a Trailing Twelve Month (“TTM”) revenue of c. $514.0B and operating income of $12.2B (margin of 2.4%). Amazon has cash and cash equivalents and marketable securities of $70 billion compared to total debt and lease liabilities of $162 billion.

Price & Market Cap (as of 7th March 2023): Its market cap is $958.64 billion with a 52-week high of $170.83 and a 52-week low of $81.43, whereas it currently trades at $93.55.

Valuation: AMZN trades at a TTM EV/EBITDA of 16.3 (10 Year average of 31.7) and a TTM EV/Sales of 2.1 (10 Year average of 3).

The rest of the write-up includes the following sections:

2. Business Overview

3. Management

4. Industry

5. Financial Analysis

6. Competitive Advantages, Opportunities and Risks

7. Valuation

8. Concluding Remarks

2. Business Overview

What Amazon does? “Our primary source of revenue is the sale of a wide range of products and services to customers.” 2022 10K. “But in reality we strive for customer excellence through constant innovations while we create value for our shareholders at superior rates, i.e. CAGR of 30.43% since inception.” StockOpine

Note: Given that almost everyone in this planet is aware of Amazon’s history, we do not intend to repeat it but you can read this to get an idea -> Amazon.com | History & Facts | Britannica.

Amazon has 3 reporting segments, North America, International and AWS but does not disclose how its business lines (shown in the graph below) add up to the reporting segments. North America accounts for 61% of total revenue, International for 23% and AWS for 16% with FY22 operating margins of -1% (average FY14 - FY22 of 3%), -7% (average FY14 - FY22 of -3%) and 29% (average FY14 - FY22 of 25%), respectively. Obviously, AWS is the crown jewel of the Company (more on this later).

In this report, we will analyze the 6 key revenue streams shown below providing a digestible description and comments on the financials of each business line.

Source: Stratosphere.io, StockOpine analysis

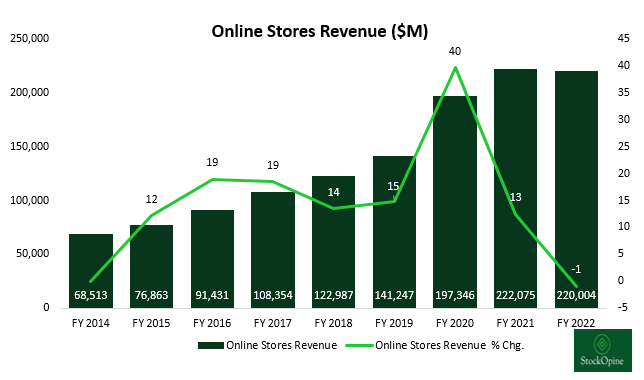

Online stores – the bread and butter

Online stores include product sales and digital media content where Amazon records revenue in gross terms. It effectively sells own inventory on Amazon marketplace offering “a wide selection of consumable and durable goods that includes media products available in both a physical and digital format, such as books, videos, games, music, and software.”

It has everything but few of its key products are Kindle, Ring, Fire tablets, Fire TV and Amazon Echo – Alexa.

For example, Amazon Echo is the leader in the smart speaker devices sector with an estimated share in US of 68% in 2022 (Statista). Per Statista, it is also the global leader with a share of 28% indicating that there is room for growth justified by the expectation of doubling the 65M units shipped in 2021 to 130M units by 2025.

It shall be noted that digital products sold on a transactional basis are also included in this category but not those on a subscription basis. That could be a purchase of a movie without having the Prime membership (more on this later).

Source: Stratosphere.io, StockOpine analysis

Over the years FY14 to FY22 online stores sales depicted a CAGR of 15.7%, growing from $68.5B to $220.0B in FY22. Online store revenue remained the largest contributor to Amazon's total revenue throughout the period, contributing 43% of revenue in FY22 compared to 77% back in FY14.

Regarding the revenue drop of 1% in FY22, we do not think that it is recurring as Amazon continues to expand its product suite. Additionally, total international sales had a negative FX sales impact of $15B thus FX could be a reason of the FY22 drop in online stores.

Going forward international e-commerce growth and online grocery (sales to customers who order goods online for delivery or pickup at physical stores) are expected to drive further growth.

Andrew Jassy, CEO “I'd just start by saying that we think grocery is a really important and strategic area for us. It's a very large market segment, and there's a lot of frequency in how consumers shop for grocery.”

“But I think that we have a very significant opportunity in the grocery segment. I think we're building a pretty broad grocery network across online and physical, and you're going to see us continue to work on it.”

Profitability is undisclosed but given the expectation of the growth in international ecommerce, the existing negative profitability of international operations and the anticipation of international sales becoming profitable, we believe that over the long term this segment could be profit accretive.

Andrew Jassy, CEO “and we think it's the right investment and believe we're going to have a large profitable international e-commerce business.”

Physical Stores – nothing promising yet

Physical stores include the product sales in stores. Any sales to customers that order goods online for delivery or pickup at the physical stores are included in “Online stores.”

This segment was created as a result of the acquisition of Whole Foods (Grocery store chain) in 2017 for $13.2B and currently also includes Amazon Go and Amazon Fresh physical store sales.

Source: Stratosphere.io, StockOpine analysis

Over the years FY17 to FY22 physical store sales depicted a CAGR of 26.7% but this was affected by the mid-year acquisition in FY17. The only noteworthy increase was the one in FY22 of 11% but we don’t think that this segment will move the needle for Amazon given the postponement of opening new Amazon Fresh physical stores until the economic and differentiation (vs Whole Foods) equations are resolved.

Furthermore, the recent announcement for closing Go convenience stores along with closures of Amazon Fresh stores reported in Q4’22 justify that this segment is struggling.

Third-party seller services – a key growth driver

For this segment, the Company does not sell own inventory but inventory of third parties on Amazon’s marketplace and generates revenue through commissions on sales and related fulfillment, shipping fees, and other third-party seller services.

AMZN competes with companies like Shopify, eBay, Alibaba etc. and although the competition is high the Company managed to increase sales from less than $12B in FY14 to c. $118B in FY22, i.e. a CAGR of 33.4%.

This segment increased faster than online store revenue and contributed 23% to revenue in FY22, indicating the growing number of third-party sellers on Amazon's platform. This was also highlighted in Q4’22, as sellers comprised a record 59% of overall unit sales for the quarter.

Source: Stratosphere.io, StockOpine analysis

Amazon competes with peers on price, selection of products, customer experience and seller experience (such as commission rate, fulfillment services, fast delivery etc.). Having nearly 2 million third-party seller partners on Amazon helps the Company differentiate itself and at the same time provide great deals to customers that need it the most. In comparison with Shopify it seems that there is room for growth for Amazon as Shopify reports ‘millions’ of merchants and Shopify appears more merchant centric.

Nevertheless, Amazon improved the value proposition to merchants over the years and it is no coincidence that sales grew by 10x since FY14. Recent developments include:

Buy with Prime (in US) that increases shopper conversion by 25%, Amazon does the fulfillment while it lets merchants offer the benefits that come with Prime (fast, free delivery, easy returns etc.).

3-way match on the Amazon Business mobile in US helping 1m active users on Amazon Business (no need for handheld scanners).

Merchant Cash Advance Program providing eligible Amazon sellers with easy and quick access to capital (up to $10M) when they need it.

Other than the recent developments, Amazon has the A-to-z Guarantee that protects customers (timely delivery and condition) when they buy items sold and fulfilled by a third-party seller. This adds value to consumers and further credibility for third-party sellers. To be eligible for the A-to-z Guarantee a purchase should be made through Amazon Pay button that ensures fast, seamless and secured checkout minimizing frauds.

Pricing fees, i.e., the commissions that Amazon gets from sellers vary depending on the service (i.e. if it includes, storage, fulfillment etc.), type of product and whether sellers are signed up on its Professional Selling Plan but given the overall growth in the segment, pricing does not appear to be a repellent factor for merchants.

Subscription Services Revenue – network effect benefits

These services include annual and monthly subscription fees associated with Amazon Prime memberships ($14.99 per month or $139 per year), access to content including digital video, audiobooks, digital music, e-books, and other non-AWS subscription services.

Amazon Prime is estimated to have over 200M users and subscribers receive a vast of benefits relative to what they pay; such as free and fast shipping on eligible items, ultrafast Fresh grocery delivery, a free, one-year Grubhub+ membership, access to streaming of movies (Prime Video), TV shows, music (Prime Music – over 100m ad-free songs), books (Prime Reading), unlimited photo storage with Amazon Photos, free games and a free channel subscription on Twitch.tv (Prime Gaming) as well as exclusive discounts and deals.

Source: Stratosphere.io, StockOpine analysis

Over the years FY14 to FY22 subscription services depicted a CAGR of 37.5% growing from $2.8B in FY14 to $35.2B in FY22, with the number of Prime subscribers being the key driver of the growth (rising from an estimated 46M subscribers in 2015 to over 200M by the end of 2021) as well as membership price hikes like in 2021 and 2018 as Amazon continued bundling new services in its Prime offering.

Considering the added benefits that customers get, price hikes are immaterial (i.e. in 2021 monthly went from $12.99 to $14.99) and very appealing relative to competition. For example, Netflix that has 231M paid subscribers and provides entertainment content without the added benefits of Prime has a Basic package of $9.99 and a Standard one of $15.49 per month.

Profitability wise, we presume that it is far from close to the operating margins of Netflix (17.8% in 2022) given the transportation costs for delivery, however, Prime should not be treated as a stand-alone business. It is about bringing more users to Amazon and retaining them while they spend more on the ecommerce side. This also attracts more merchants (Buy with Prime) strengthening the network effect of being on Amazon’s marketplace.

Brian Olsavsky, CFO “And we see a direct link between that type of engagement and higher purchases of everyday products on our Amazon website. So the health of Prime is very strong.”

This section is not solely about Prime as Amazon takes steps to enhance its healthcare offering with in-office and virtual healthcare services effectively streamlining the whole care service (through the acquisition of One Medical for $3.9B - More details) and the RxPass (available to Prime members only so further cross-selling) that offers unlimited prescription medications for only $5 per month.

“Any customer who pays more than $10 a month for their eligible medications will see their prescription costs drop by 50% or more, plus they save time by skipping a trip to the pharmacy,” John Love, vice president of Amazon Pharmacy.

AWS Revenue – the crown jewel

Amazon started offering IT infrastructure services in the cloud back in 2006 whereas its current CEO Andrew Jassy along with Jeff Bezos were the pioneers of this idea that turned out to be its most precious asset.

The Amazon Web Services (“AWS”) segment generates revenue from the global sales of compute, storage, database, analytics, built-in security, backups and other services for start-ups, enterprises, government agencies, and academic institutions. Generally, when a client joins a cloud provider is ‘locked-in’ and it’s difficult to migrate to a different provider.

Cloud computing has three main models, namely, Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS) and Amazon explains them simply in this link.

We are not cloud experts but going over AWS site, one can understand that AWS offers vast of services for an organization to support any cloud workload. As per its website it has more than 200 fully featured services for compute, storage, databases, networking, analytics, AI, security, IoT etc.

Its flagship products are Elastic Compute Cloud (EC2) that rent out computer processing power, e.g. renting virtual servers that allow users to run their computer applications and the Simple Storage Service (S3), which effectively rents data storage in the cloud.

Let the experts do the comparison!! Gartner ranks AWS as a Leader in its Magic Quadrant for Cloud Infrastructure and Platform Services (“CIPS”) with the highest score in ‘Ability to execute’.

Source: Gartner

Per Gartner, AWS leads on breadth and depth of capabilities and exceeds the second close competitor, Microsoft Azure by 2 times in the CIPS market, whereas ‘Gartner client inquiry surfaces that AWS often optimizes for the short term when dealing with customers’ which is something to follow up if it remains the case.

Source: Stratosphere.io, StockOpine analysis

Over the years FY13 to FY22 AWS revenue grew from $3.1B to $80.1B, i.e. a CAGR of 43.5%, representing 16% of total revenue compared to 4% in FY13, while at the same time operating margin grew from 10% in FY14 to 29% in FY22 reaching $22.8B. Growth is mainly justified by cloud adoption and customer usage. Some pressures are expected in the near future for Cloud IT spending but the long term trend is intact (see Industry section).

The following quote explains just that but also shows a better picture for client relationships than what was addressed by Gartner.

“And the reality is that the way that we've built all our businesses, but AWS in this particular instance, is that we're going to help our customers find a way to spend less money. We are not focused on trying to optimize in any one quarter or any one year, we're trying to build a set of relationships in business that outlast all of us. And so if it's good for our customers to find a way to be more cost effective in an uncertain economy, our team is going to spend a lot of cycles doing that.”, Andrew Jassy, CEO

Efficiencies - The interesting stuff

Amazon has a tendency to turn costs into revenues (think of fulfillment, AWS etc.)!

Compute power needs energy, but energy costs. AWS Graviton3 (first Graviton in 2018) a CPU custom designed by AWS delivers up to 3x better performance compared to AWS Graviton2 processors for ML workloads. Graviton2 offers up to 40% better price performance for cloud workloads and Graviton3 provide up to 25% better compute performance and it is more energy efficient, i.e. 60% less energy. Obviously, Amazon strives for efficiencies.

Fulfillment centers and physical stores also need energy so Amazon in order to optimize costs grew its renewable energy capacity to 20 gigawatts (“GW”), enough to power 5.3 million U.S homes by growing its capacity by 8.3 GW in 2022. Amazon is also the largest corporate buyer of renewables and through these investments it aims to achieve a 100% powering through renewable energy by 2025.

Do you know what could be the new revenue line for Amazon? It feels that this would be renewable energy!