Q1’2022 results

Key metrics

Key quotes from Q1 earnings call

Outlook for Q2’2022

The CEO, Management Ownership and Compensation

Industry

Valuation

As the travel industry is recovering from the pandemic, the booking volume for holidays is at all-time high. This momentum is expected to continue throughout 2022 and beyond and as a result, Booking Holdings and Airbnb could be major beneficiaries of this trend. In this article we will briefly discuss the travel industry and management, review Q1’22 results and Q1’22 metrics, consider their outlook for the rest of the year and proceed with a valuation estimate to assess whether any of them provides a good entry point for outsized returns. As of 3 June 2022 $ABNB and $BKNG are down 28.03% and 2.64% respectively.

1. Q1’2022 RESULTS

Firstly, let’s dig into their results for Q1’2022. The below analysis is considering Q1 2019 which excludes the impact of the pandemic.

* ADR for Booking was calculated by dividing Gross Bookings with Nights Booked. It should be noted that Gross bookings include all travel services (i.e., accommodation, car rentals, and flights).

** Cash & Cash equivalents & marketable securities as well as Debt for ABNB, represent December 2019 figures rather than Q1’19.

*** Q1'19 Debt of BKNG includes convertible bond.

AIRBNB Q1’2022

GBV of $17.2B, up 67% Y/Y and up 73% from Q1 2019. Growth driven by increase in Nights and Experiences Booked, combined with continued strength in ADR (Average Daily Rate), despite the ongoing pandemic, the war in Ukraine, and macroeconomic headwinds.

Record on Nights and experience booked which surpassed 102.1m increasing 59% Y/Y. Compared to Q1 2019 nights and experiences are up 26%.

Revenue of $1.5B, up 70% Y/Y. Revenue exceeded pre-pandemic Q1 2019 by 80%.

Net loss of $19 million significantly improved compared to a net loss of $1.2 billion (includes one-time items of $782 million) in Q1 2021 and $292 million in Q1 2019. The positive change in Q1 2022 compared to prior periods was driven by substantially higher revenue and cost management.

First quarter of positive Adjusted EBITDA of $229 (excludes $195M of SBC) compared to Adjusted EBITDA in Q1 2021 of $-59 million and Q1 2019 of $-248 million. Adjusted EBITDA margin was 15% for Q1 2022.

$1.2B of net cash provided by operating activities, up from $618 million in Q1 2021 and $314 million in Q1 2019. The key driver of the increase was unearned fees, totaled $1.7 billion as at 31 March 2022 compared to $904 million as at 31 December 2021.

$1.2B of free cash flow (79% of revenue), up from $611 million (69% of revenue) in Q1 2021 and $277 million (33% of revenue) in Q1 2019.

BOOKING HOLDINGS Q1’2022

Record GBV of $27.3B, up 129% Y/Y and up 7% from Q1 2019 (previous record). Increase in GBV is due to increase in ADRs by 18%, offset by 9% decrease in nights booked compared to Q1 2019.

198 million room nights booked, up 100% Y/Y and down 9% versus Q1 2019.

Revenue of $2.7B, up 136% Y/Y. Revenue was down 7% versus Q1 2019.

Net loss of $700 million which included an unrealized loss on equity securities of about $987 million (includes investments in Meituan, Grab Holdings and DiDi Global). This compares to a net loss of $-55 million for Q1 2021 and net income of $765 million (including unrealized gains on marketable equity securities of $451 million) in Q1 2019.

Adjusted EBITDA of $310 million (including SBC) compared to Adjusted EBITDA in Q1 2021 of $-195 million and Q1 2019 of $718 million. Adjusted EBITDA margin was 11.5% for Q1 2022 compared to 24.9% for Q1 2019. The decrease in adjusted EBITDA relate primarily to the timing differences between gross bookings and revenue recognition.

$1.7B of net cash provided by operating activities, up from negative $-207 million in Q1 2021 and $150 million in Q1 2019.

$1.6B of free cash flow (59% of revenue), up from negative $-272 million in Q1 2021 and $39 million in Q1 2019.

$948 million in share repurchases in Q1 which brings the outstanding authorization to $9.5B. In addition, in April 2022, the Company repurchased approximately $325 million of its common stock. The Company expects to complete repurchases under the remaining authorization within the next three years.

Further to the above, and as it can be observed from the table both companies improved their net debt position.

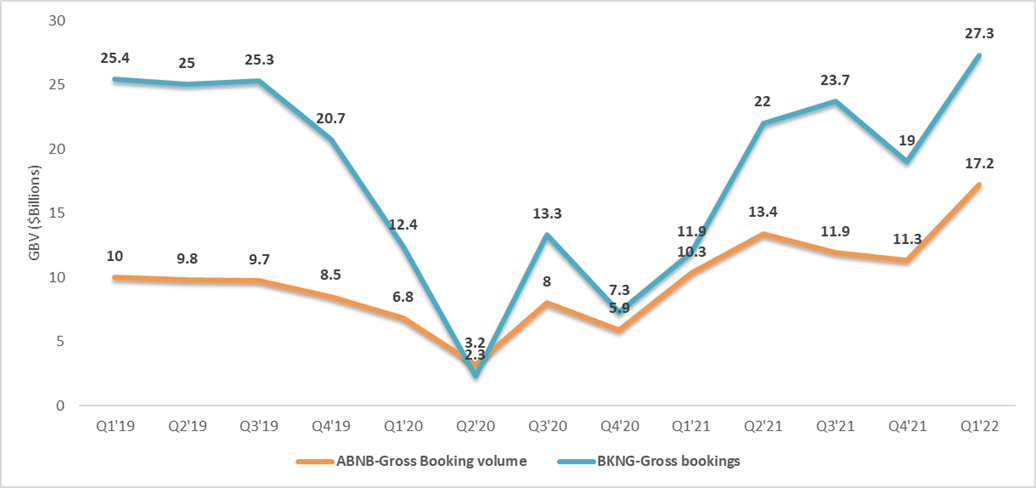

2. KEY METRICS

Let’s now evaluate how the two companies performed during the last 3 years by comparing their gross bookings, nights booked and Average Daily Rates (ADR).

Gross Booking Volume (GBV)

Nights booked

Average daily rate (ADR)

Both companies’ metrics show that they are in a recovery mode with their GBV’s of Q1’2022 reaching new highs with the major driver being the growth in ADR. The price appreciation and thus higher ADR was driven by inflation, strong demand as well as hospitality sector-wide price appreciation. It currently seems that inflation has a positive short-term impact.

While both companies faced a steep decline in GBV and nights booked during the pandemic (BKNG also faced a considerable decline in ADR), BKNG’s decline was steeper, crossing ABNB in Q2’2020. ABNB demonstrated a more robust business model during the pandemic crisis.

3. Key quotes from Q1 earnings call

Booking

1. New record in GBV for April 2022

Glenn Fogel, President and CEO “Bookings continued to strengthen in April, with room rates increasing 10% and gross bookings up over 30% versus 2019, making April a record month for gross bookings and our first month that global room nights exceeded 2019 levels”.

2. Alternative accommodation

Glenn Fogel, President and CEO, on global mix of alternative accommodation “For alternative accommodations, our global mix of room nights in the first quarter increased to about 31%, a couple of points higher than in Q1 2021. We continue to work on improving our alternative accommodation product globally with an additional focus on the US market.”

Glenn Fogel, President and CEO on competition in the alternative accommodation space, “And I've talked about this in the past in the alternative accommodations area, where we think we are not as well positioned as some of our competitors, stating the fact particularly in the US, so we absolutely need to go out.”

3. Connected trip and the flight offering on Booking

Glenn Fogel, President and CEO, “On our connected trip vision, we continue to make progress as we work on the foundations, such as developing a flight offering on Booking, which is now live in 40 countries.”

Glenn Fogel, President and CEO, “This flight offering gives us the ability to engage with potential customers who choose their flight options early in their discovery process, and allows us an opportunity to cross sell our accommodation and other services to these flight bookers.”

David Goulden, CFO “Airline tickets booked in the first quarter were up 152% versus 2019 and up 69% versus 2021, driven by continued expansion of Booking's flight platform, as well as continued flight ticket growth at Priceline.”

4. Take rates in 2022

David Goulden, CFO “Our current best estimates of take rates in 2022 is just below 15%, which is lower than 2019 primarily due to timing. We expect the underlying accommodation take rates will remain stable.”

5. Shift to merchant revenues (payments facilitated by Booking)

Glenn Fogel, President and CEO “On payments, 34% of Booking's gross bookings were processed through our payment platform in the first quarter, which is our highest quarterly level ever”

David Goulden, CFO “We are getting an increase in the overall take rate from our mix toward payments and from the fact that we get additional revenue from payments.”

AIRBNB

1. Profitability

David Stepheson, CFO “And I’m really excited that in 2022 we’ll have our first full year of net income profitability, so just on a full net income basis to be profitable this year feels excellent.”

2. Long-term stays

Brian Chesky, CEO “Guests are staying longer, even living on Airbnb. Long-term stays of 28 days or more remained the fastest-growing category by trip length compared to 2019. Long-term stays accounted for 21% of gross nights booked in Q1 2022, up from 13% in Q1 2019 and down from 24% in Q1 2021. Long-term stays are at an all-time high, more than doubling in size from Q1 2019.”

3. Capital allocation

David Stepheson, CFO, “We will continue to have a balance sheet that enables us to be ready to invest when and where we find that it's appropriate. It does enable us to do M&A in the future if desired, although M&A is not our primary driver of growth. We still plan to grow organically as our primary means. But we'll continue to evaluate our balance sheet use and make sure that we are deploying capital appropriately.”

4. Impact of inflation

David Stepheson, CFO, “I think we're just not seeing price appreciation impact our business negatively. We had our strongest quarter ever. We have even stronger demand for Q3 and Q4 than we've ever had.”

5. Airbnb in a recessionary environment

Brian Chesky, CEO, “In a recession, if that were to happen, is that probably more people would turn to hosting. That would be number one. So that we would expect, and number two, travelers would probably become more budget conscious. And that would probably have a benefit to Airbnb as well. Now, the downside, of course, the recession is often times fewer people travel. But again, I think we're a pretty resistant business, whether it's economy's good or bad, we're pretty adaptable model.”

4. Outlook for Q2’2022

AIRBNB

Nights and Experiences Booked growth rate in Q2 2022 (compared to Q2 2019) will approximate the growth rate in Q1 2022 (compared to Q1 2019), i.e., 26%.

ADR expected to be flat in Q2 2022 on a year-over-year basis. Stable ADR in Q2 2022 suggests GBV growth in line with nights and experiences, i.e., 27% compared to Q2’2021.

Q2 2022 revenue between $2.03 billion and $2.13 billion, up 56% compared to Q2’2021 and 71% compared to Q2’2019, using the mid-point forecast.

Low double-digit EBITDA margin percentage improvement on a year-over-year basis. Adjusted EBITDA margin for Q2’2021 stood at 16.2%.

Booking

Management did not provide clear guidance due to the Russia/Ukraine conflict and due to the pandemic. Despite this, the management noted the following:

April 2022 room nights increased about 10% versus 2019 driven primarily by Europe, excluding Russia, Ukraine and Belarus and all regions showed improving room nights growth in April. Europe was up in the high teens percent in April and up about 30% excluding Russia, Belarus and Ukraine.

April gross bookings increased over 30% versus 2019, driven by growth in room nights, continued accommodation ADR strength, as well as continued strength in flight bookings. April gross bookings increased to almost $11 billion, which was a new monthly record.

The recent strength in ADRs is expected to continue for the remainder of the quarter and as a result, the difference between the level of room nights growth and gross bookings growth for the full second quarter is expected to be around 20 percentage points better, which is similar to what it was in April.

Revenues as a %age of gross bookings will be about 200 basis points lower than the second quarter of 2019. This is mainly timing related, and is based on the bookings acceleration observed.

If the company sees similar top line growth rates for the rest of the quarter as for April, the management expects adjusted EBITDA to be over $900 million for the quarter.

Based on the above comments from management, and assuming that growth in gross bookings is similar to April 2022 compared to April 2019 (i.e., 30%), the gross bookings could reach c. $32.55 billion with a revenue of $4.35 billion and an effective EBITDA margin of around 21%. Such revenue translates to a growth of c.13% compared to Q2’2019 and 102% compared to Q2’2021.

5. The CEO, Management Ownership and Compensation

Booking

Glenn Fogel, CEO

Glenn has served as Chief Executive Officer and President of Booking Holdings Plc since January 2017 and CEO of Booking since June 2019. He joined the Company in 2000 and served several positions including Head of Worldwide Strategy and Planning and Executive Vice President. Prior to that, he was a trader at a global asset management firm and prior to that was an investment banker specializing in the air transportation industry. Glenn is 60 years old.

Ownership

As per the latest 14A filing (26 April 2022), Glenn holds 34,522 shares in the company which represent less than 0.1% of the total shares. All directors and executive officers own 52,387 shares (including the CEO), representing less than 1%.

Compensation

Booking’s CEO compensation for 2021 was $29.9M excluding accounting adjustments of $24.1M for prior year (2018 and 2019) PSU grants due to COVID. Total compensation for 2021 was $54.0M. As per the filing, the company claims that CEO’s compensation is in line with peers’ compensation (excl. accounting adjustments).

The accounting adjustment relates to PSUs granted in 2018 and 2019 that would be completely forfeited as a result of the pandemic. The Compensation Committee Adjusted the vesting factors of those PSUs in early 2021 so that Glenn Fogel would receive the benefit for the strong performance achieved prior to the COVID-19.

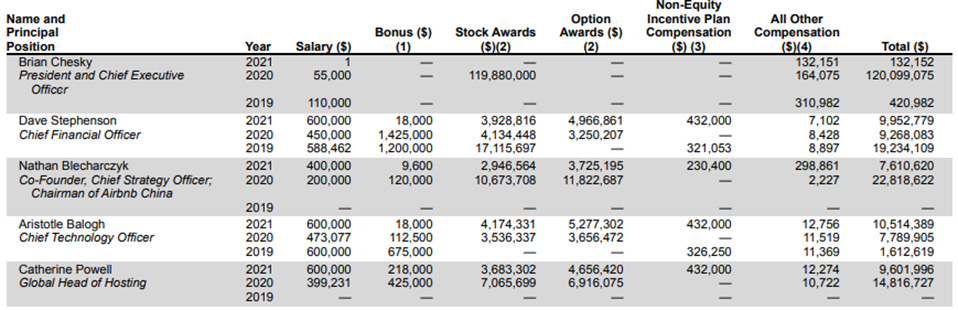

Below is a summary of the compensation of the executive team for the year 2021:

Source: Proxy statement 2022

Airbnb

Brian Chesky, CEO

Brian is one of the three co-founders of Airbnb. He co-founded the company in 2008 and serves as Chief Executive Officer and Head of Community. Brian is 40 years old and he received a Bachelor of Fine Arts in Industrial Design from the Rhode Island School of Design.

Ownership

As per the latest 14A filing (22 April 2022), Brian holds 12% ownership in the company and 27.1% voting power. The 3 founders together have a total voting power of 72.0% and 32.1% ownership. The management team of Airbnb has skin in the game with CEO’s future compensation linked to the company’s stock price.

Compensation

Airbnb’s CEO receives nominal amounts in terms of compensation, except for 2020, in which year he received a Restricted Stock Unit award which vests over a ten-year period. The grant-date fair value of stock awards granted in November 2020 was $119.88M. The total compensation for 2021 was $132.1k (salary of $1).

In 2020, he was granted 12 million performance-based RSU award intended to cover ten years of compensation. The award is directly linked to the stock price of the Company and may be earned, if at all, based on the 60-trading days trailing average closing stock price exceeding progressively higher stock price hurdles, ranging from $125 in 2021 to $485 in 2030.

Below is a summary of the compensation of the executive team for the year 2021:

Source: Proxy statement 2022

6. Industry

Airbnb and Booking Holdings operate in similar markets and generate revenues within those markets, though, their operational model and targeted clientele is not necessarily the same.

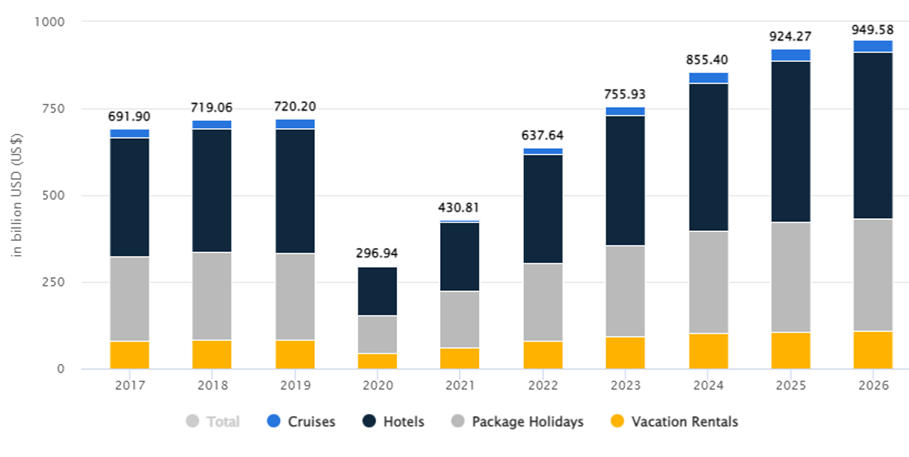

We consider Travel & Tourism market as their broad market, in which revenue is projected to reach US$637.70bn in 2022 and show an annual growth rate (CAGR 2021-2026) of 17.12%, resulting in a projected market volume of US$949.60bn by 2026.

Source: Statista, Travel & Tourism market revenue

The industry is considered cyclical, and the current economic environment creates uncertainty, but at least, the growth forecast adds some comfort as to whether the two companies will be able to grow in the foreseeable future. Projected revenue CAGR (2021-2026) for Airbnb is c.23.0% whereas for Booking Holdings is c.20.3% for the same period.

Although a higher CAGR is projected by analysts for the two companies, the competitive advantage that the two platforms have due to their network justify those growth rates. For the record, Airbnb claims to have more than 4 million hosts across 220 countries (over 6 million listings in Q1’22), whereas Booking Holdings Inc claims to have 28+ million listings (hotels, apartments, homes etc.) in +220 countries. As per 10-Q filing, Booking has 2.4 million properties on its website.

It shall be noted that the two platforms held the two top spots in Apptopia rankings in terms of downloads for 2020 and 2021, with Booking having 13 million more downloads in 2021 compared to 2020 (increase of 26%, from 50 million to 63 million), whereas Airbnb downloads increased from 42 million to 44 million. Agoda is also owned by Bookings Holdings.

We identified Hopper as a potential threat, considering its increase in downloads. It shall be noted that as per Apptopia, most of the downloads come from US, in which Hopper increased from 5.3 million in 2020 to 15 million in 2021 (#1).

Source: Apptopia

7. Valuation

For the valuation of Airbnb and Booking the revenue growth was based on analyst’s consensus. As a sanity check, we compared this to the broad industry (Travel & Tourism) growth, as provided by Statista, which is estimated to be c.17% for 2021-2026.

In terms of profitability, we used an average projected EBITDA margin of 32% (gradually increasing to 34%) for Booking Holdings, which is below the 2015-2019 margin (adjusted for SBC) of 36.4% due to higher competition in the market (Airbnb, meta search platforms etc.), investments in alternative accommodation, connected trip investments etc.

For Airbnb, an average projected EBITDA margin of 21% (gradually increasing to 31%) was used, which is below Booking’s margin mainly due to higher expected SBC. Given that a) management expects a first-year net income profitability for 2022, b) the high operating leverage of the company and c) the positive tone of the earnings call, we believe that the company will be able to achieve high profit margins soon.

→ Positive tone (by CFO):

“We actually have 16% fewer people at the end of Q1 '22 than we did at the end of Q1 2020 before we had our layoffs. And yet we think we're being more productive than ever before”

“but we're making nice strides and improvement in leverage so that we gain continued profitability. And one of the things we noted in the letter is that we're expecting for the full year a modest expansion in our overall EBITDA margin rate”

“in 2022, we'll have our first full year of net income profitability. So just on a full net income basis, to be profitable this year feels excellent”

To estimate free cashflows to each firm we adjusted for Capex based on historic averages.

In respect to the terminal multiple, it is assumed to be around 15x for Booking, below its 5-year average of 18x (2015-2019) whereas, higher multiple of 20x was assigned to Airbnb as we believe that the company could further expand its EBITDA margin after the 5-year horizon and would still be at an earlier stage growth compared to Booking.

To estimate the value per share we used the minimum required return that we aim to obtain from our investments under the current environment, adjusted for net debt and non-operating assets / liabilities identified and thereafter divided the resulting value by the number of shares.

Based on the above calculations and assumptions used (which of course may not materialise at all), it seems that BKNG has a potential upside of 12.2%, whereas ABNB has no upside from current price levels. The resulting IRR over a 5-year period is 12.8% for Booking Holdings and 8.8% for Airbnb.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.