We have initiated a position in Booking Holdings $BKNG. Below is a summary of our investment thesis with the most important factor being its valuation:

After being hit by the pandemic during 2020-2021, the online market for travelling and accommodation is recovering. According to Business Wire, Global Online Travel Market Size is projected to be US$ 1,464 Billion by 2027, from US$ 801Billion in 2021 (CAGR of 10.6%).

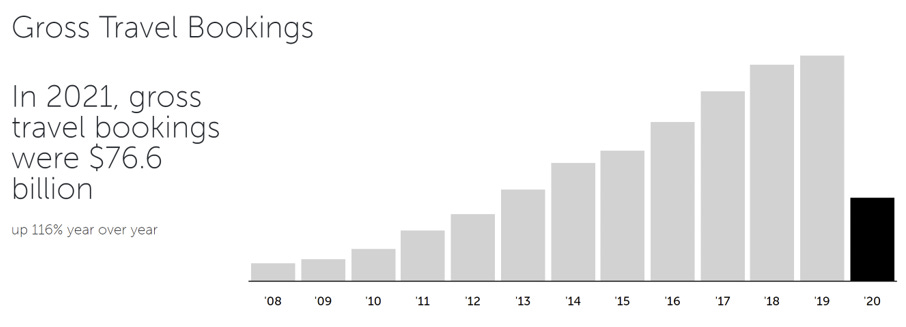

Online travel agencies (OTA) like Booking will be one of the beneficiaries of this trend. Early signs of recovery appeared with Gross Booking Volumes (GBV) of major OTAs surging to all-time highs due to increase in nights booked and increase in Average Daily Rates (ADRs). For example, Booking had Q1’2022 GBV of $27.3B, up 129% Y/Y and up 7% from Q1 2019. Airbnb had GBV of $17.2B, up 67% Y/Y and up 73% from Q1 2019.

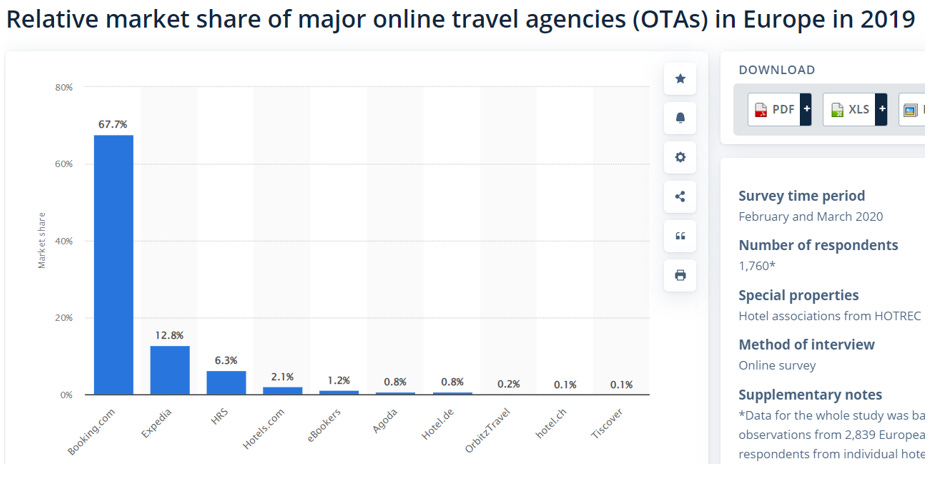

Booking is a leader in OTA market. For example, its market share in Europe in 2019 was 67.7% according to Statista. Global wise it generated the highest revenue in US$ billion for 2019 and 2020. Also the large number of hotel listings on Booking creates a network effect and acts as a barrier for new entrants in OTA. For instance, in 2021, 590 million room nights were booked across Booking Holdings. This is below the pre-pandemic 2019 figure of 844 million which is explained by the fact that the market has not fully recovered.

Heavy share buybacks over the span of the last 10 years. Total shares have been reduced from 49.9M in 2012 to 41.1M in 2021. This approximates to $23B of share buybacks compared to cash generated from operations (over the same period) of approximately $32B. Around 70% of the cash generated from operations were returned to shareholders, without disrupting the business from growing.

Optionality: Other than accommodation / lodging choices, Booking offers the option to book a flight, to rent a car, to book a visit to an attraction or activity and to book an airport taxi transfer. Needless to say, but you can also use your Genius discount on certain items.

Valuation: Analysts expectations for 2026 EBITDA average at $10.1 billion, whereas in our valuation we use an EBITDA of $8.9 billion. Assuming a multiple EV/EBITDA of 18 (in line with 2015-2019 average) we reach an Enterprise Value of $160.6 billion (difference is due to rounding) compared to today’s EV of $82.9 billion. Potential IRR on EV terms is around 15.8%.