Booking Holdings BKNG 0.00%↑ reported its Q2’22 results on 3rd August 2022. The below commentary is a preview of Q2 2022 earnings.

Q2’2022 FINANCIAL RESULTS

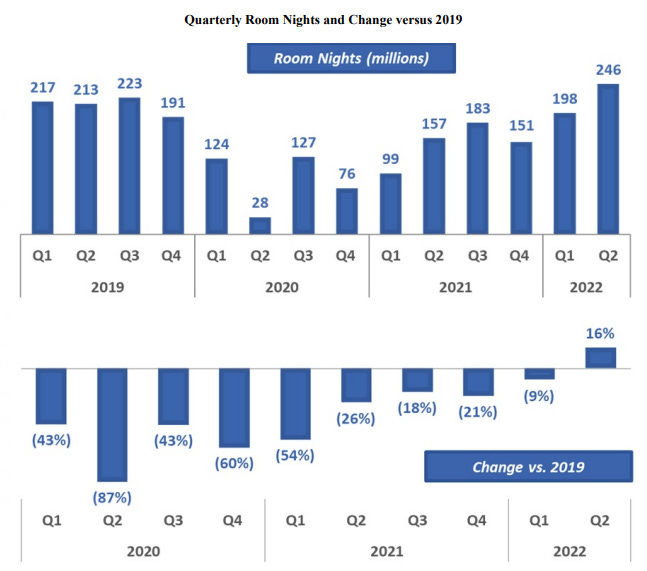

Source: Booking Holdings 10-Q reports, Booking Holdings Q2’22 Earnings release, StockOpine analysis

* ADR was calculated by dividing Gross Bookings with Nights Booked. It should be noted that Gross bookings include all travel services (i.e., accommodation, car rentals, and flights).

The below comparison is based on Q2 2019 unless otherwise stated.

REVENUE

Revenue of $4.3B, up by 12% from Q2 2019 (20% on a constant currency basis). Revenue growth was driven by the continued recovery of travel demand.

Record Gross Bookings of $34.5B, up 38% (48% on a constant currency basis) from Q2’2019. Growth driven by increase in Room Nights, combined with the continued strength in ADR (Average Daily Rate).

246M room nights booked (highest quarter ever), surpassing pre-pandemic levels. Room nights increased by 16% compared to Q2’2019 and 24% quarter over quarter.

Room nights in Europe and U.S. were up by 20% and 30% respectively. Even though growth has improved in all regions relative to Q1, Asia was down high-single-digits. Excluding bookings from Russia, Ukraine and Belarus from the comparison, overall room nights would have been up by 21%.

Source: Booking Holdings Inc. Form 10-Q June 30, 2022

Constant currency ADR growth versus 2019 accelerated from 18% in Q1 to 25% in Q2, primarily due to higher rates in Europe.

David Goulden, CFO, “Despite the higher ADRs in the second quarter, we have not seen a change in the mix of hotel star-rated levels being booked or changes to length of stay that could indicate that consumers are trading down”.

Mix of merchant revenues increased from 35% in Q2 2019 to 44% in Q2 2022.

PROFITABILITY

Adjusted EBITDA of $1.1B (including SBC) compared to Adjusted EBITDA in Q2 2019 of $1.37B. Adjusted EBITDA margin was 25.3% compared to 36.1% for Q2 2019. The decrease in adjusted EBITDA relate primarily to the timing differences between gross bookings and revenue recognition.

David Goulden, CFO, “If we were to normalize for negative timing impacts on revenue in the second quarter, our adjusted EBITDA would have been meaningfully higher than in Q2 2019”.

Adjusted EBITDA was also adversely affected by foreign exchange rates. David Goulden, CFO “Our Q2 EBITDA would have been about 10% higher if FX were in line with Q2 2019.”

Net Profit of $857 million which included gains on equity securities of about $181 million. This compares to a net profit of $979 million (including gains on equity securities of $17 million) in Q2 2019.

$2.6B of free cash flow (61% of revenue), up from $1.7B (44% of revenue) in Q2 2019.

$1.3B in share repurchases in Q2 2022 and total repurchases for the year to just over $3B. The outstanding authorization now stands at $7.4B. The Company expects to complete repurchases under the remaining authorization in about two years (previous expectation in Q1 was three years).

ALTERNATIVE ACCOMODATION

Alternative accommodation room nights grew by 25% compared to Q2 2019. The global mix of alternative accommodation room nights was about 32% which is in line with Q2 2021 and higher than Q2 2019.

David Goulden, CFO “Within Europe, our mixed alternative accommodations continues to be meaningfully higher than the global average. In North America, our mix of alternative accommodations remains low relative to global average. However, we did see an encouraging increase in mix versus Q2 2021 in that region.”

Glenn Fogel, CEO, “In the second quarter, we saw the largest sequential net increase in alternative accommodation properties since 2019 and we now have 6.6 million alternative accommodation listings on Booking .com.”

It should be also noted that $ABNB reported over 6 million of active listings in Q2 2022.

TAKE RATES

Revenue as a percentage of Gross booking was 12.4%, down from 15.4% in Q2’2019. The decrease is due to timing difference between gross booking and revenue recognition (increase in gross bookings drives revenue as a percentage of gross booking lower as revenue is recognized at the time of check-in and not at the time of the booking).

Accommodation take rates for the year are expected to remain stable relative to 2019. Overall take rates for the year are expected to be in the mid 14% range due to higher mix of flights and negative impact of foreign exchange rates.

MOBILE AND APP BOOKINGS

40% of the room nights were booked through the Company’s apps in Q2 2022 which is consistent with Q2 2021 and about 10 percentage points higher than in 2019.

Glenn Fogel, CEO “Booking. com's app continued to set new records in terms of monthly active users in Q2 and remains the number-one downloaded OTA app globally according to a third-party research firm.”

PAYMENTS AND CONNECTED TRIP

Connected trip refers to the Company’s long-term strategy to build a more integrated offering of multiple elements of travel connected by a payment platform.

Glenn Fogel, CEO on payments, “38% of Booking. com's gross bookings were processed through our payment platform in the second quarter, which is our highest quarterly level ever”.

Increasing payments through the platform improves working capital cycle of the business, however it drives operating margins lower (merchant revenues have lower margins than agency revenue). In addition, non-accommodation services (i.e. flights) which are part of the Company’s Connected Trip vision have lower margins and can also negatively affect future operating margins.

However increased payments through the platform are a net benefit to the business as they add incremental EBITDA dollars.

SUPPLY OF PROPERTIES

As of 30 June 2022, Booking .com had over 2.5 million properties on its website (400,000 hotels, motels, and resorts and over 2.1 million alternative accommodation properties), representing an increase from approximately 2.4 million properties as at 30 June 2021.

The year-over-year increase in total properties was driven by an increase in alternative accommodation properties.

OUTLOOK

Room night growth for Q3 2022 is expected at 4% relative to Q3 2019. This implies a year over year growth in room nights of 27%.

Strength in ADR is expected to continue at similar levels seen in Q2 2022 (19% ADR growth compared to Q2 2019), implying an ADR of c. $135.

Revenue as a % of GBV is expected to be 70 basis points lower than in Q3 2019 due to an increase in the mix of flights and some impact from foreign exchange rates.

Q3 adjusted EBITDA expected to be slightly above Q3 2019. Management noted that EBITDA is adversely affected by FX rates. According to management, Q3 EBITDA growth at current exchange rates versus 2019 would have been about 15 percentage points higher than the current EBITDA expectation.

Based on the above, gross bookings for Q3 2022 could reach c. $31.4B with a revenue of $6.03B and an effective EBITDA margin of around 41%. Such revenue translates to a growth of c.20% compared to Q3’2019 and 29% compared to Q3’2021.

CONCLUDING REMARKS

Overall, it was a satisfactory quarter with the company benefiting from the continued recovery of travel demand as well as from the strength in ADRs. It looks like management continues to execute towards the connected trip vision with increasing mix of room nights coming through the direct channel, increase in mix of merchant revenue, improvements in alternative accommodation offering and flights continuing to be a source of new customers.

Previous write ups on Booking Holdings Inc.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.