Booking Holdings Q1'26: Ignoring the Noise

Strong Execution, Massive Buybacks, and a Portfolio Update

Booking Holdings reported its Q1 2026 earnings, delivering another strong quarter that beat expectations and management’s guidance. Despite the beat, the recent conflict in the Middle East impacted room nights booked and Gross Booking Volume (GBV). This article will bring you up to speed with the company's performance and give you our thoughts on our holding.

1. Financial results

Despite the geopolitical headwinds, the company continued to execute, showing momentum in unaffected regions and expanding its margins.

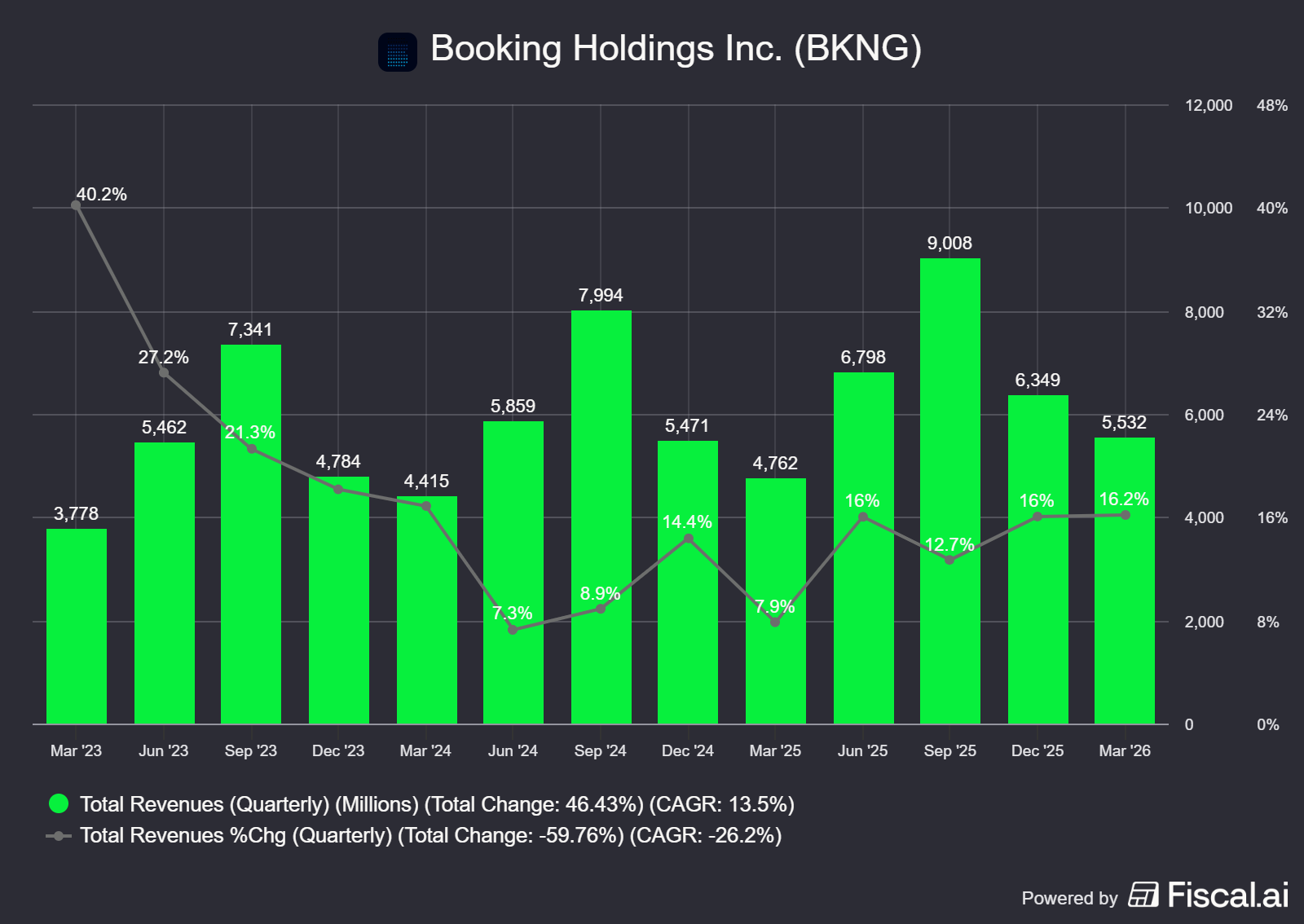

Revenue

Revenue came in at $5.5 billion, representing year-over-year (YoY) growth of 16% (10% YoY on a constant currency basis). The weakness of the USD against other currencies benefited revenue, as Booking generates a large chunk of its revenue outside the US. However, this is a temporary benefit as currencies naturally fluctuate over time. This result exceeded the high end of management’s guidance (14%-16% reported or 7%-9% on constant currency basis). The outperformance benefited from higher merchant revenues, which carry a higher take rate.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

For Q2 2026, management expects 4%-6% YoY (2%-4% on constant currency) revenue growth. While the growth deceleration of approximately 7 percentage points on a constant currency basis appears steep, it is largely driven by the escalation of the Middle East conflict, which caused a sharp drop in new bookings and elevated cancellations throughout March (with global room night growth plummeting to just 1%). Since those lost March bookings were largely intended for Q2 travel, Q2 is effectively absorbing the revenue hole created by that initial demand shock. This is compounded by management’s conservative guidance assuming the conflict’s impacts will persist for the entire second quarter, compared to just a partial-quarter impact in Q1.

Adjusted EBITDA

Adjusted EBITDA for Q1 2026 was $1.3 billion, up 19% from the prior-year quarter. The Adjusted EBITDA margin was 23.3%, an expansion from 22.9% in Q1 2025, driven by leverage in fixed operating expenses.

Despite the steep revenue deceleration expected in Q2, management guided for Adjusted EBITDA to grow 4% to 6%, perfectly in line with revenue growth. This highlights the beauty of Booking's asset-light business model: their largest expense, marketing, is highly variable and naturally scales down alongside softening demand.

Adjusted EPS

Adjusted EPS for Q1 2026 was $1.14, up 14% from the prior-year quarter. The growth in EPS was lower than EBITDA growth due to a higher tax rate, though this headwind was partially offset by the heavy repurchase program, which lowered the share count by 4%.

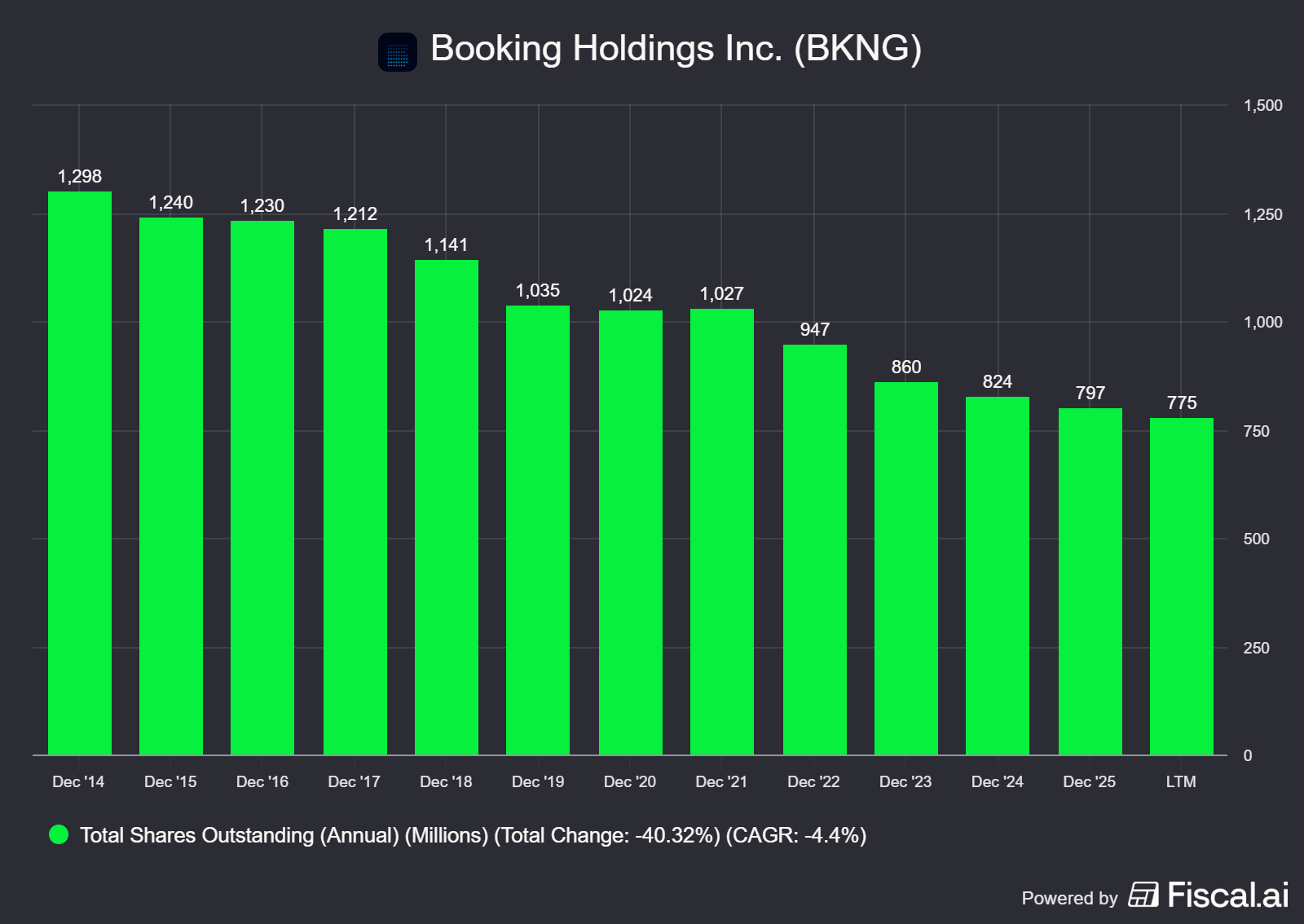

Capital Returns

A massive $4.0 billion was returned to shareholders in the quarter, consisting of a record $3.6 billion in share buybacks and $343 million in dividends.

Booking Holdings has consistently bought back shares over the last decade. CEO Glenn Fogel commented on this aggressive strategy:

“Since 2014, we have reduced our share count by over 40%, even after accounting for the dilutive impact of stock-based compensation by opportunistically investing in this long-term vision through our share buyback program.

No one is better positioned than we are to understand what our long-term value can and should be relative to market fluctuations on any given day or quarter. As I just mentioned, we have reduced our share count by over 40% in 12 years. Importantly, we have done so at the average price per share of $93, thereby generating significant incremental investment returns for our shareholders by betting on ourselves at the right times, and while always preserving and exercising the flexibility to invest in both the organic and inorganic growth of our business. It is a strategy that we are very committed to.”

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

2. KPIs

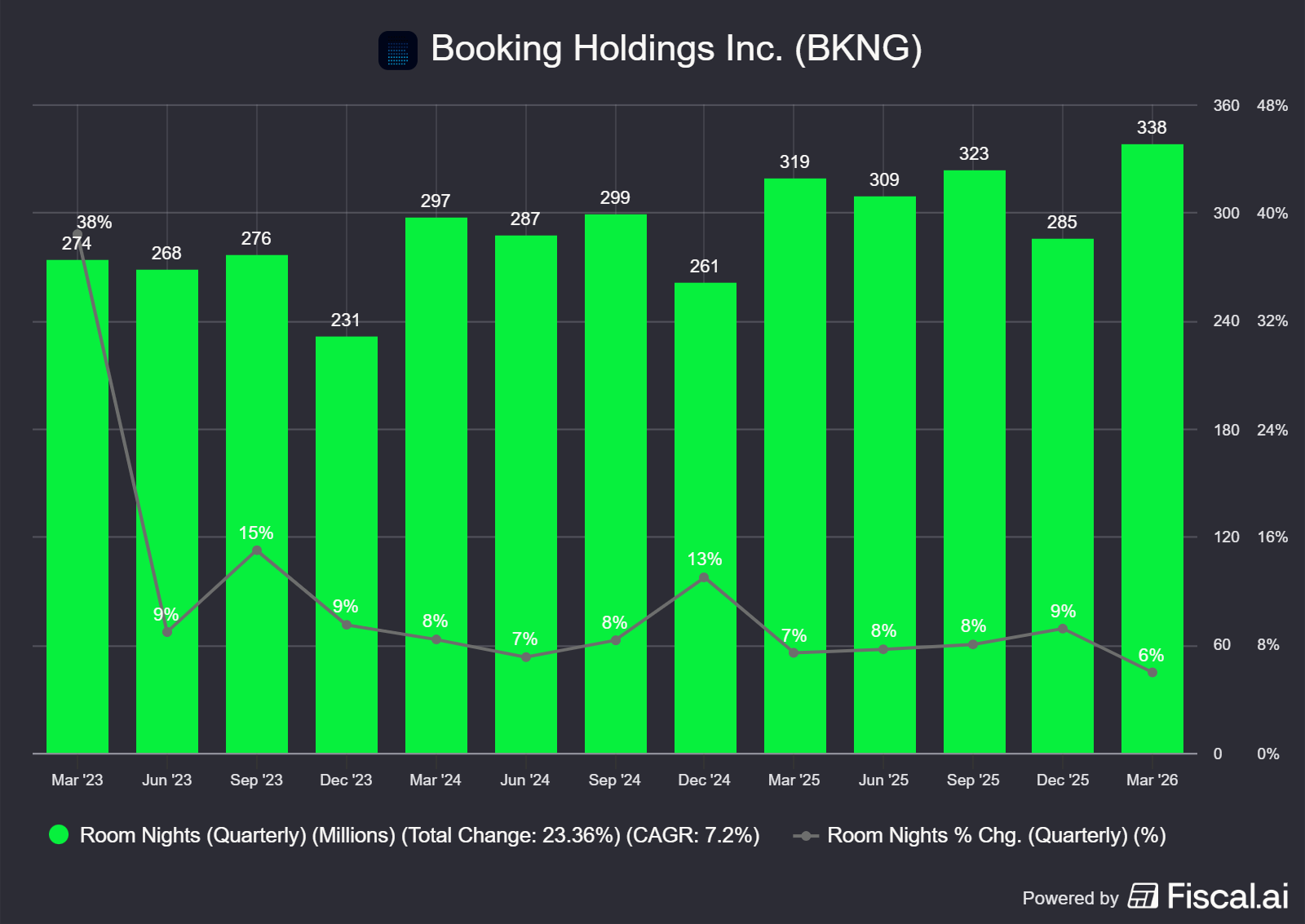

a. Nights Booked

Nights booked for the quarter reached 338 million, up 6% YoY. Management estimated that the Middle East conflict negatively impacted room night and GBV growth by about 2 percentage points. Excluding this impact, room nights would have been up by approximately 8% (exceeding management's prior guidance of 5% to 7%).

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

The U.S. accelerated for the fourth consecutive quarter, growing in the low teens (Vs low double digit in Q4 2025), driven mainly by domestic travel.

Europe was up mid-single digits (Vs high single-digit in Q4 2025). While the region was negatively impacted by bookers traveling to the Middle East, intra-regional demand from European bookers remained strong, up high-single digits.

Asia was up high-single digits. Within Asia, intra-regional demand from Asian bookers was up low-double digits.

Rest of World (which includes the Middle East) was down low-single digits.

Looking ahead, 2%-4% room night growth is projected for Q2 2026, assuming the conflict’s impacts continue through the end of June.

To quantify the regional exposure: bookers in the Middle East (including Turkey and Egypt) represented approximately 4% of global room nights in 2025. If we include inbound travel to the Middle East, the region represents approximately 7% of global room nights.

Following the onset of the conflict, Booking saw elevated cancellations and lower travel demand, resulting in overall March room night growth dropping to 1%. The impact in March was about 6 percentage points (half from reduced bookings, half from increased cancellations). Therefore, if it was not for the conflict, room nights would have grown at a healthy rate of 7% in March.

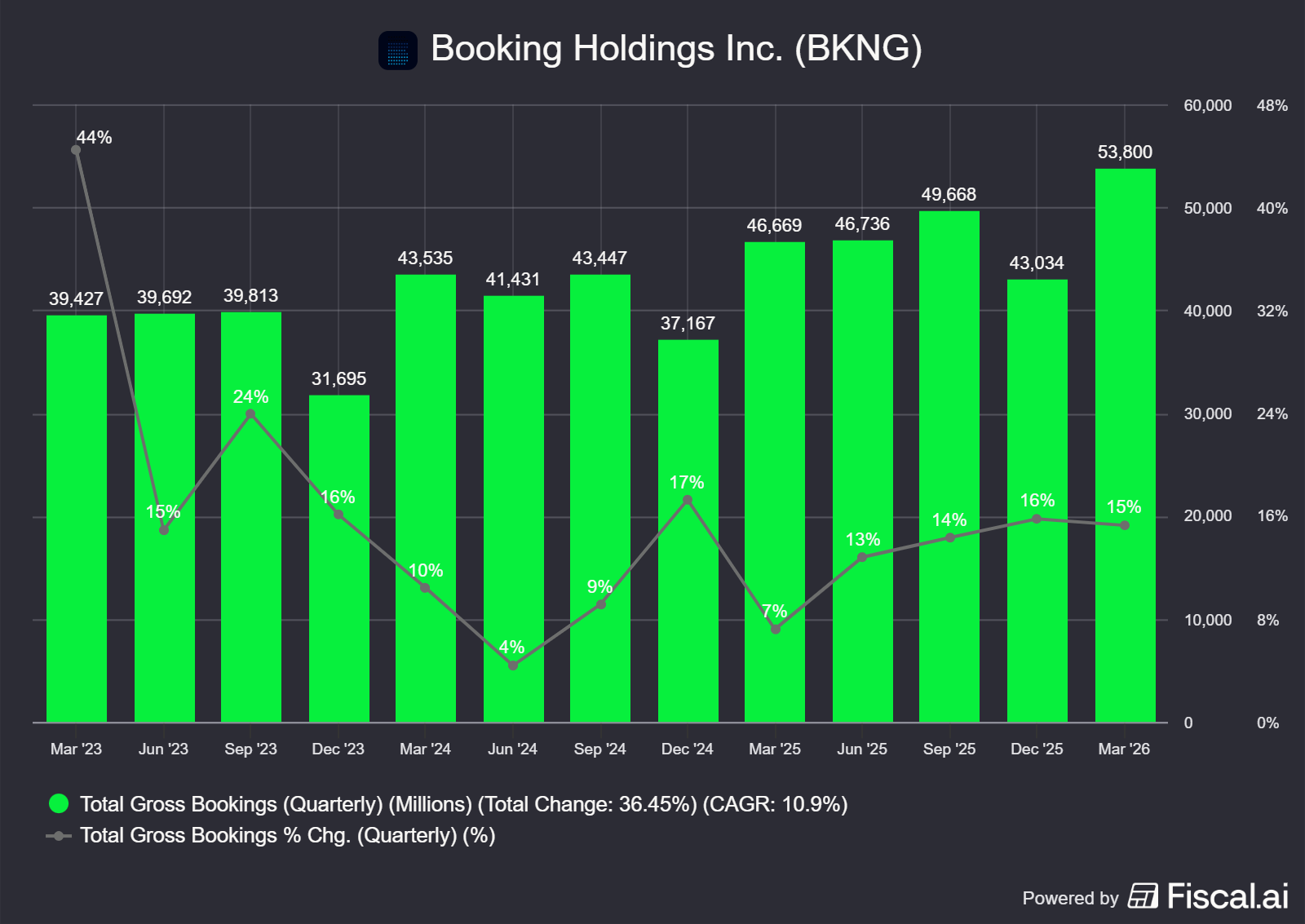

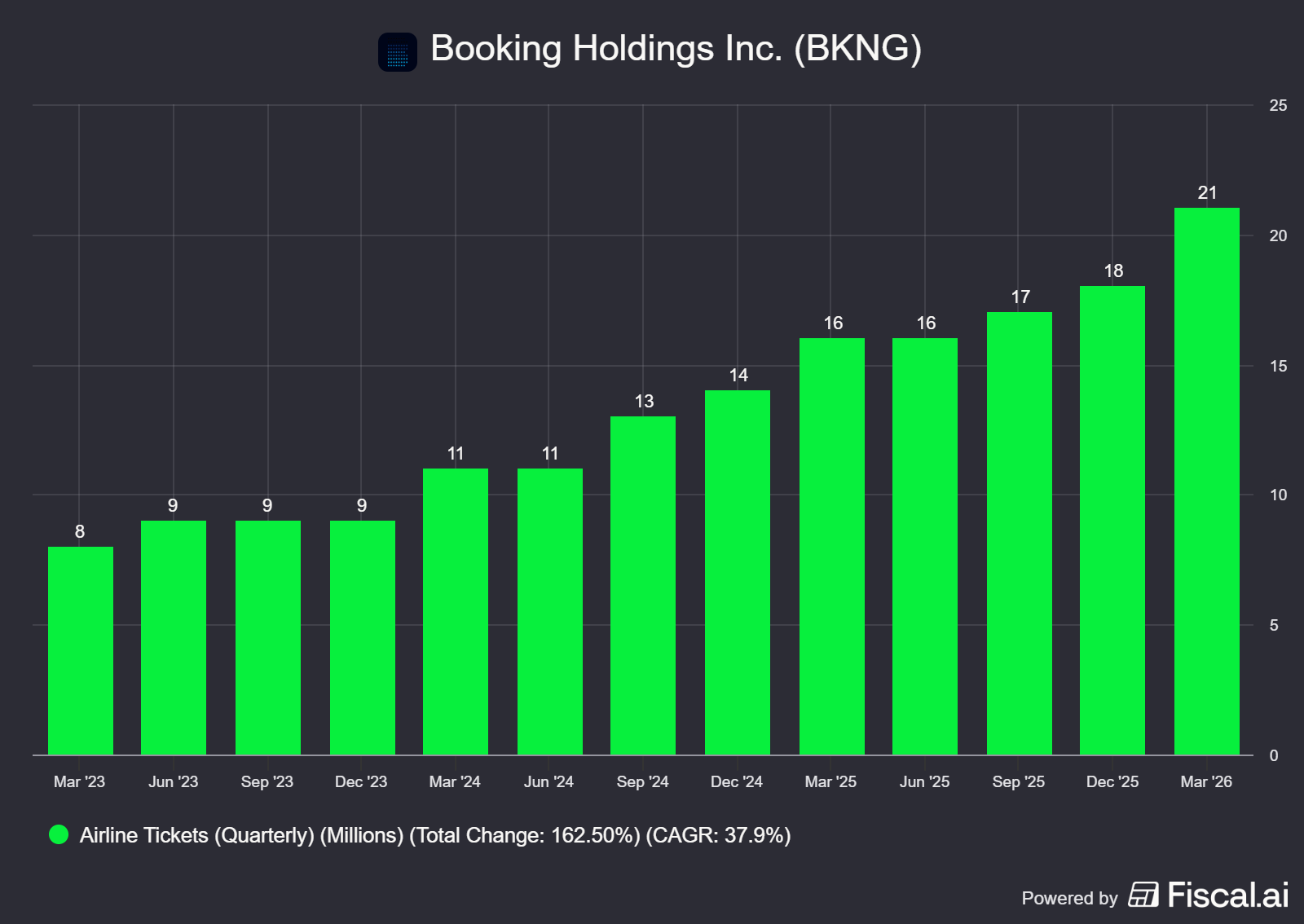

b. Gross Bookings

Gross Bookings in Q1 2026 reached $53.8 billion, a 15% increase (8% on a constant currency basis). Growth was driven by the 6% room night growth, a 1% increase in constant currency ADRs, and a 28.5% growth in airline tickets. Looking ahead, Booking projects 4%-6% gross bookings growth for Q2 2026 (2%-4% on a constant currency basis, which is in line with room nights).

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

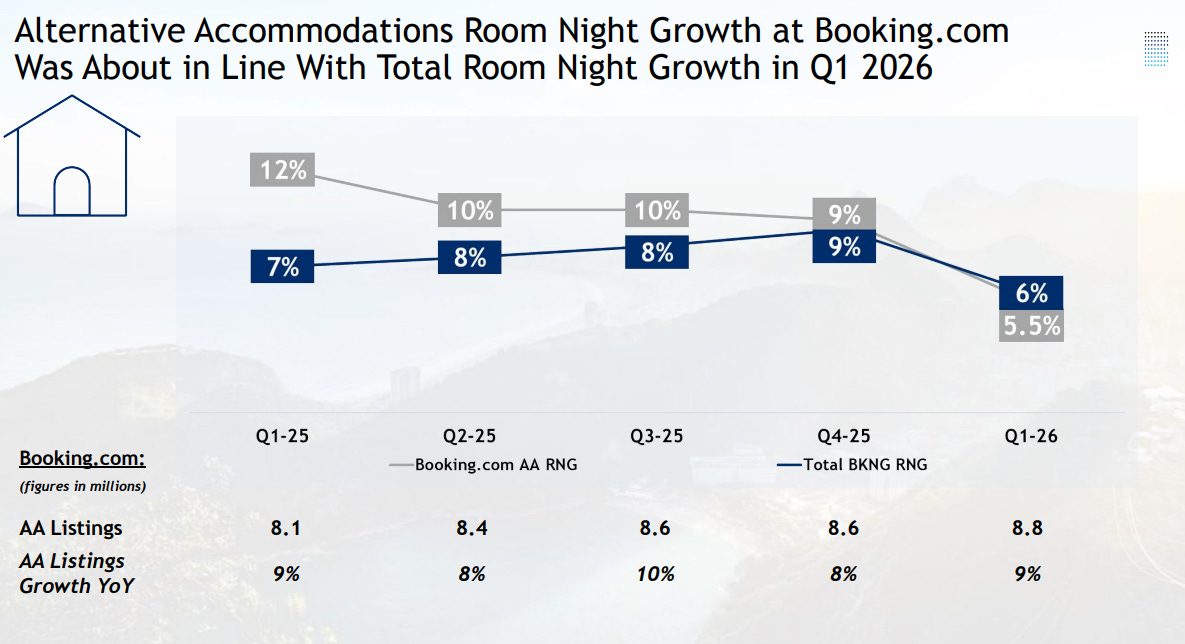

3. Alternative Accommodation

Alternative accommodation room nights on Booking.com grew 5.5% YoY. At first glance, this appears to be the first quarter that alternative accommodations grew at a slower pace than the company's total room nights (6%). However, that 6% figure applies to the entire Booking Holdings parent company, which was lifted by strong regional growth from sister brands like Agoda and Priceline in the U.S. and Asia.

On the core Booking.com platform, alternative accommodations actually outpaced traditional hotels, allowing the segment's mix to successfully expand to 38% of Booking.com’s room nights, up from 37% in Q1 2025. Furthermore, the underlying supply engine remains highly positive, with active listings reaching 8.8 million, a 9% increase YoY.

Source: Booking Holdings Q1’26 presentation

4. Direct and App Bookings

The shift to direct, high-loyalty bookings remains strong, validating the company’s brand power.

The TTM mobile app mix was in the high-50% range, up from the mid-50% range last year.

The TTM B2C direct mix, which excludes performance marketing channels, held steady in the mid-60% range. This remained resilient despite the conflict, as the Middle East traditionally has an above-average direct mix, offset by continued declines in SEO traffic (which is only a small contributor to the overall direct channel).

Genius level 2 and 3 customers accounted for a high-50% share of TTM room nights, up from the mid-50% range last year.

As the mix of direct bookings increases, the company can gain further operating leverage on marketing expenses.

5. Merchant Bookings

Merchant gross bookings reached 72% of the total this quarter, highlighting a massive multi-year evolution from just 23% in Q1 2019, 51% in Q1 2023, and 67% last year. This expanding mix is a strategic win: it enables the Connected Trip by allowing Booking to seamlessly bundle multiple travel verticals into a single customer transaction. Financially, it boosts revenue yield by capturing payment processing economics alongside standard commissions, while generating a massive float of upfront cash that earns substantial interest income.

6. Connected Trip

The Connected Trip strategy continues to expand customer wallets and lock in loyalty.

Flight tickets booked grew 28.5% YoY, while attractions tickets jumped 25%.

Connected Trip transactions (trips booked across more than one vertical) grew in the high-teens range YoY. These transactions now represent a low double-digit percentage of Booking.com’s total transactions.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

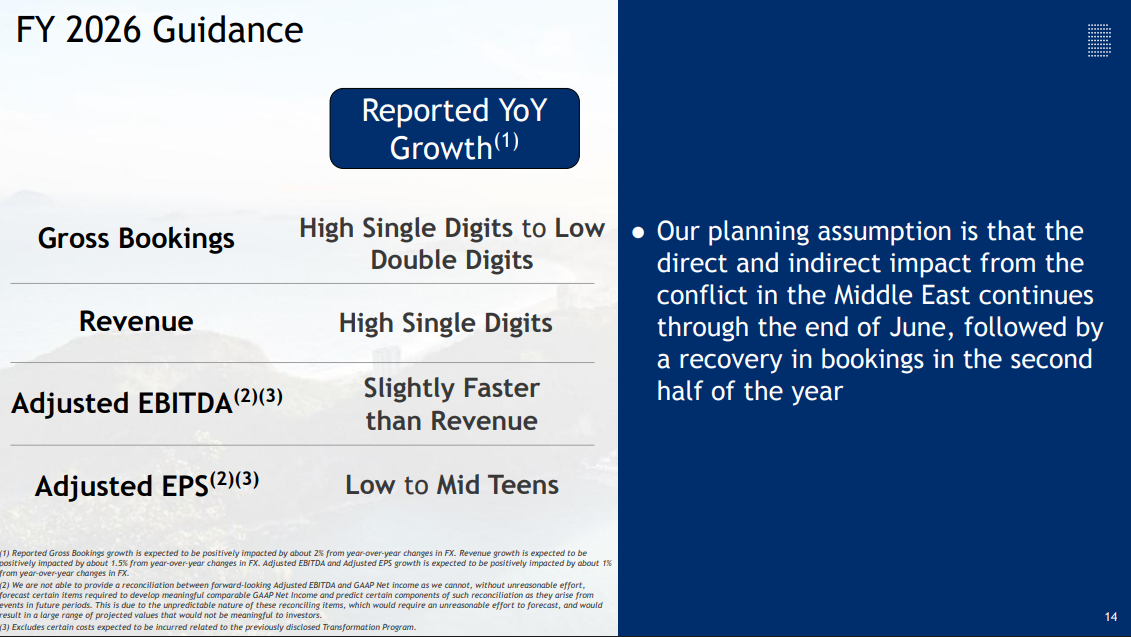

7. Outlook

Due to the conflict in the Middle East, management adjusted their revenue guidance expectations for the full year. Assuming the conflict is sustained until the end of June and is followed by a recovery in bookings in the second half of the year, they expect high single-digit revenue growth compared to low double digit expected in prior guidance. Despite lowering the bottom end of the ranges, management kept the high end of guidance for Gross Bookings and Adjusted EPS in line with their prior expectations.

Source: Booking Holdings Q1’26 presentation