Booking Holdings: Strong Finish, But What’s Driving the Pullback?

Q4'25 Earnings Review

Booking Holdings reported its Q4 and Full Year 2025 earnings, closing out the year with double-digit top-line growth, margin expansion, and a 25-for-1 stock split announcement. Despite exceeding Wall Street’s estimates and its own guidance, the stock faced downward pressure following the release.

Here is a breakdown of the numbers and the headwinds spooking the market.

1. Financial results

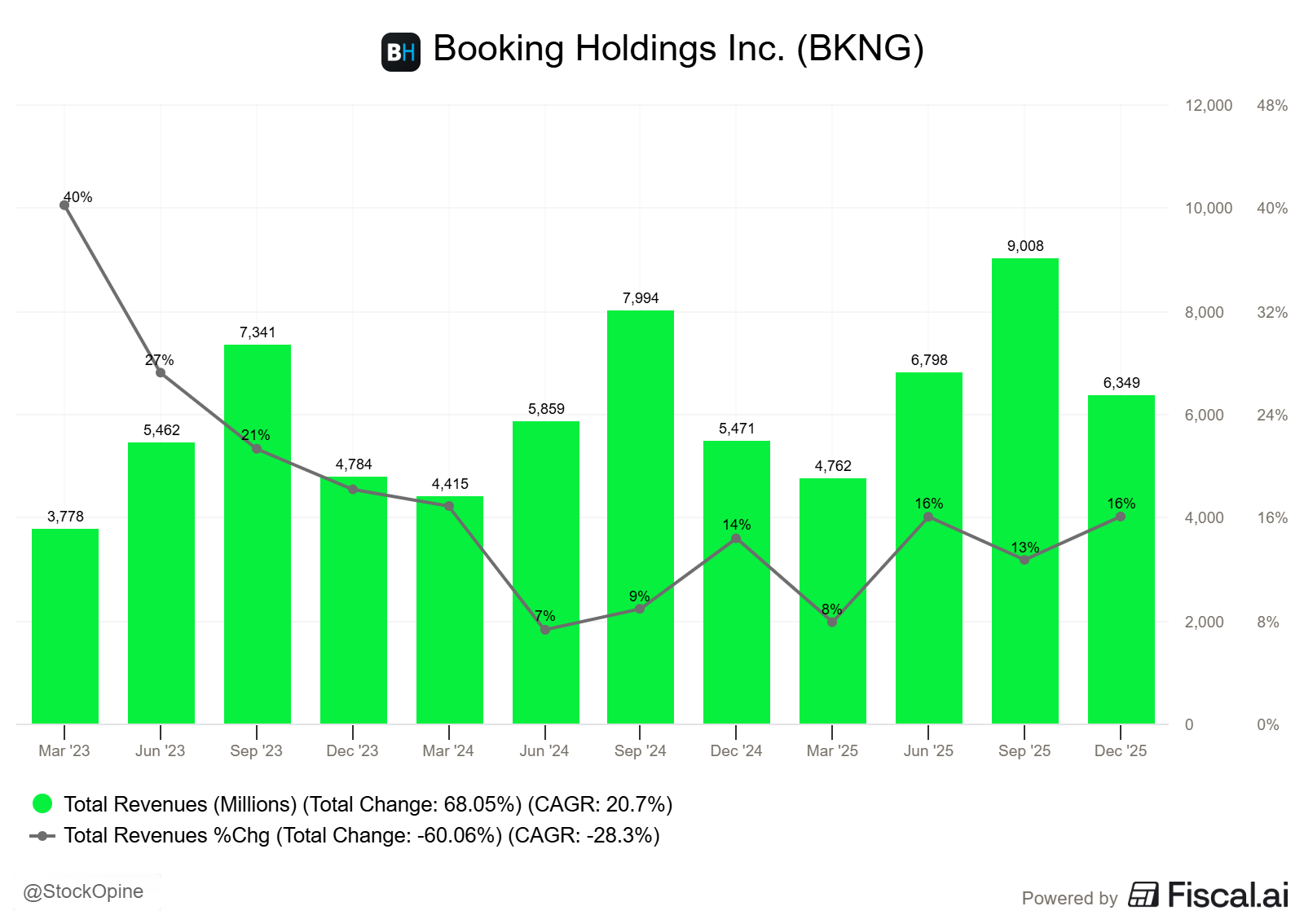

Revenue: Reached $6.3 billion, up 16% year-over-year, or approximately 11% on a constant currency basis. This exceeded the high end of management’s guidance by about 4 percentage points, driven by higher than expected payments revenue.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Profitability: Adjusted EBITDA grew 19% year-over-year to $2.2 billion, with the Adjusted EBITDA margin expanding to 34.6% from 33.8% in the prior year. Adjusted EPS came in at $48.80, up 17% year-over-year.

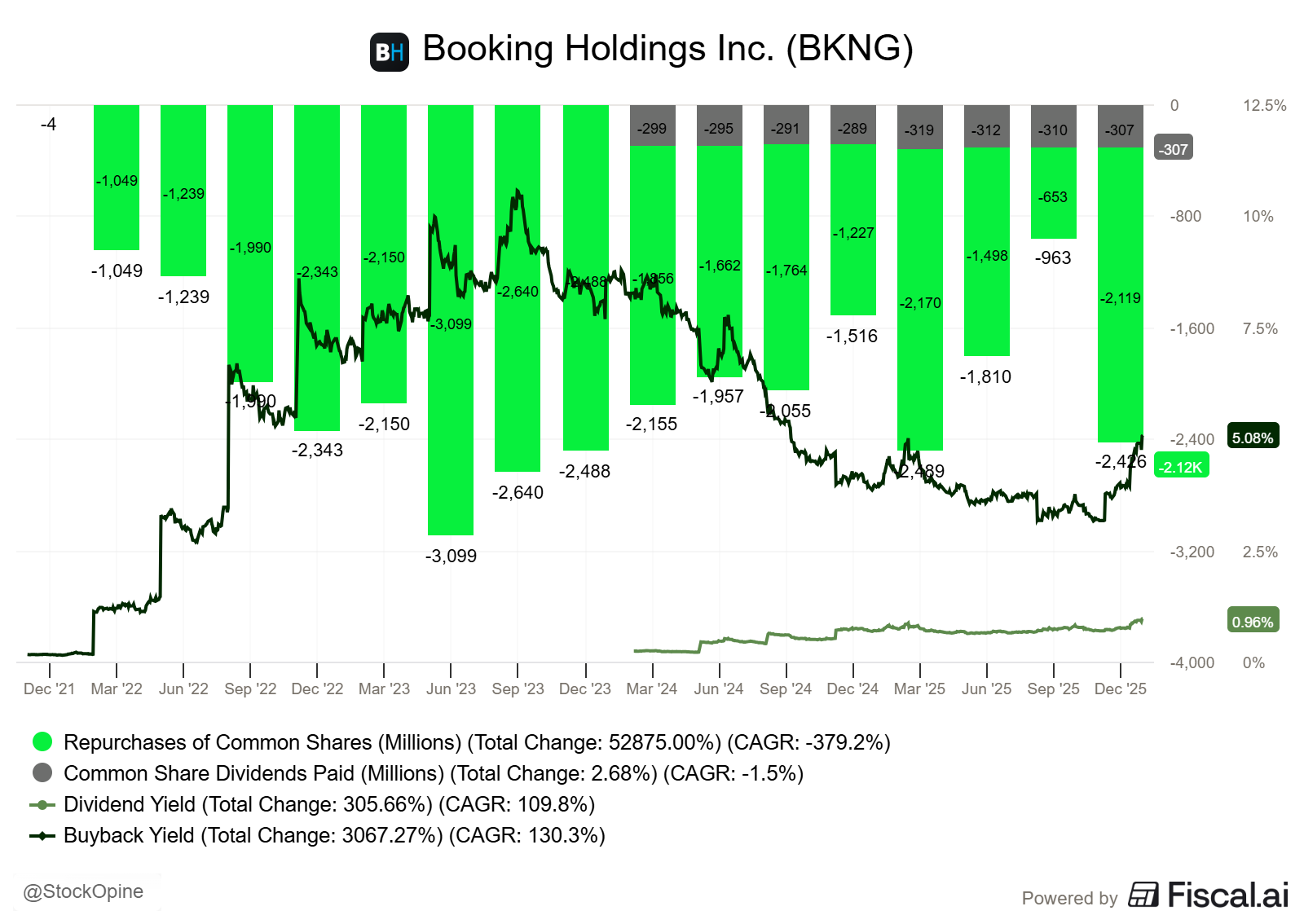

Capital Returns: Free cash flow surged 120% year-over-year in Q4 to $1.4 billion. The company rewarded shareholders by returning $2.4 billion in Q4 alone, the highest quarterly amount since 2023, through a mix of share repurchases and dividends. Furthermore, the Board approved a 25-to-1 stock split effective April 2, 2026, and raised the quarterly dividend by 9.4% to $10.50 per share.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

2. KPIs

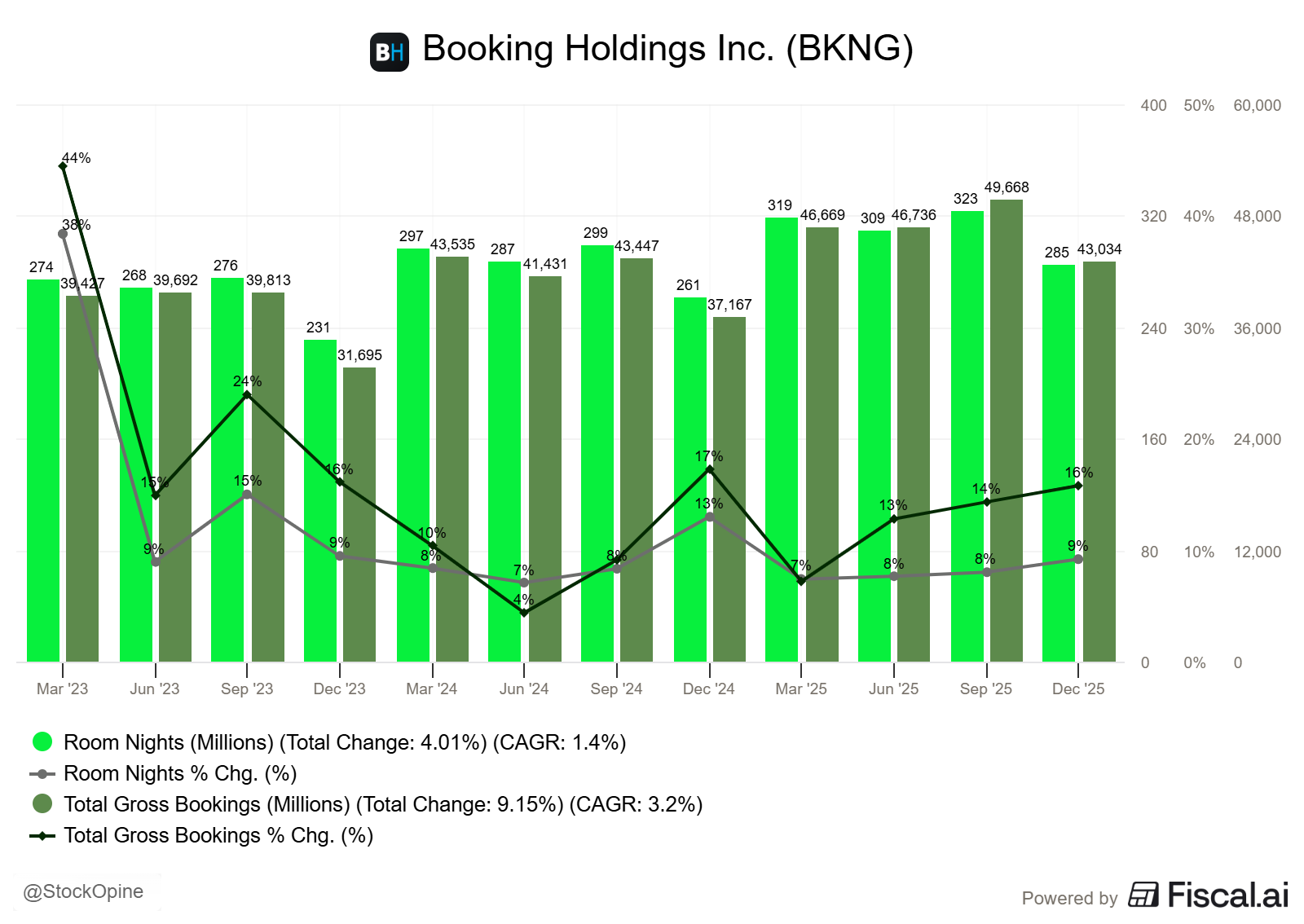

Room Nights & Gross Bookings

Room nights grew 9% year-over-year to 285 million, beating the top end of guidance by 3 percentage points driven by strong Asia and US as well as an expanded booking window. Total gross bookings increased 16% to $43.0 billion.

Growth was broad-based. Asia and the US each delivered low double-digit room night growth, while Europe and the rest of the world grew in the high single digits.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Alternative Accommodation

Alternative accommodation room nights (representing 36% of total room nights) at Booking.com grew approximately 9% in Q4, and total listings reached 8.6 million, an 8% increase year-over-year. However, analysts on the earnings call pointed out that growth in this segment is “continuing to slow a little bit”,

raising questions about its long-term trajectory. Glenn Fogel, CEO, acknowledged the slowdown and noted that despite performing well, he believes there is room for further improvement in that area.

“We're growing it. It's nice, but we got more to be done, and we got more to be done there and improving the product and certainly there are areas where we are still nowhere near where I'd like to be in terms of inventory, but we are building it. So I hope nobody takes something from this call and thinks, oh, it's not as important. No, it is important and it's something that we are going to continue to be working hard on.”

To read the analysis into how Booking is shifting to a Merchant Model, their tangible AI cost savings, the LLM threat analysis, and the final valuation verdict, you can upgrade to the premium tier.