Booking Holdings ($BKNG), a stock we hold in our portfolio, released its Q1’23 results on 4th May 2023. Here is a concise review of the quarter.

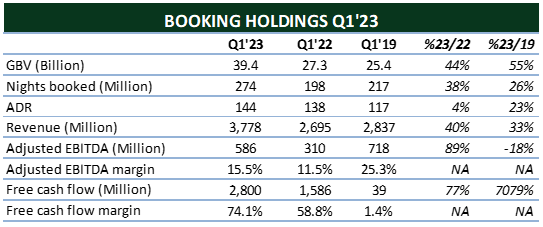

Q1’23 Key Financials and KPIs

Source: Booking Holdings 10-Q reports, Booking Holdings Q1’23 Earnings release, StockOpine analysis

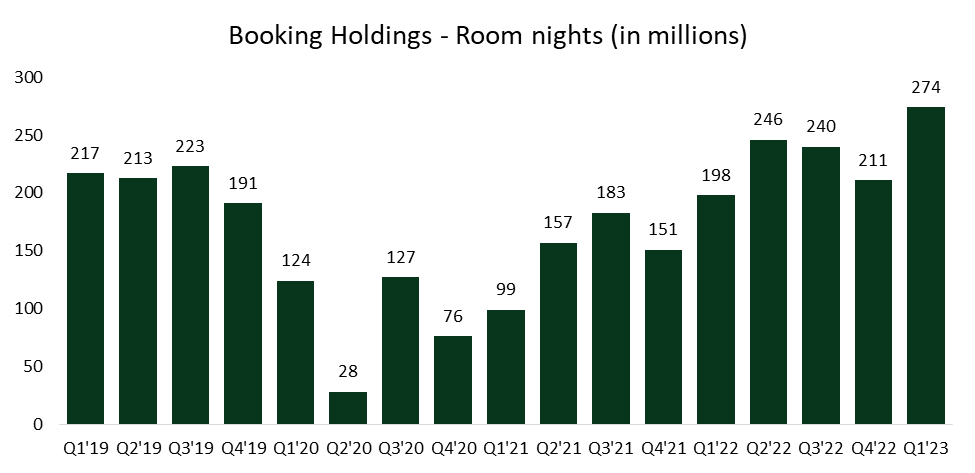

Nights booked reached an all-time high at 274 million, reflecting a remarkable 38% year-over-year increase and a 26% surge compared to Q1’19.

Source: Booking Holdings Q1’23 Earnings release, StockOpine analysis

The growth in nights booked was observed across all major regions, with Asia leading at 100% growth, while Europe and the rest of the world both experienced over 30% growth. However, the year-over-year growth rate in the United States decelerated to high single digits, down from the 35% seen in Q4’22.

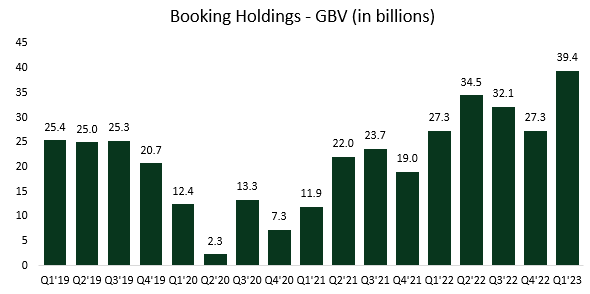

The surge in nights booked contributed to another record-breaking Gross Booking Volume (GBV) in Q1, which exhibited a 44% year-over-year increase (or 52% on a constant currency basis) and an impressive 55% growth compared to Q1’19.

Source: Booking Holdings Q1’23 Earnings release, StockOpine analysis

“Both room night and gross bookings came in ahead of our previous expectations as a result of the continued strength in leisure travel demand and from a lengthening booking window, particularly in Europe and the U.S.” Glenn Fogel, CEO

Despite the ongoing high Average Daily Rates (ADR) and a tightening economy, the travel industry continues to demonstrate resilience.

“Despite the higher ADRs in the first quarter, we have not seen a change in the mix of hotel star ratings being booked or change in length of stay that could indicate that customers are trading down” David Goulden, CFO

* ADR was calculated by dividing Gross Bookings with Nights Booked. It should be noted that Gross bookings include all travel services (i.e., accommodation, car rentals, and flights).

Source: StockOpine analysis

Alternative Accommodation

Alternative accommodation also experienced substantial growth, with room nights increasing by 45% compared to Q1’22. The global mix of alternative accommodation room nights rose to approximately 33%, up from 31% in Q1’22.

“In the U.S., our mix of alternative accommodation room nights, while still low relative to our global mix, has increased meaningfully in the first quarter, reaching highest level ever and was also our absolute highest room nights in U.S. alternative accommodations ever.” Glenn Fogel, CEO

Additionally, the number of global listings for alternative accommodations reached approximately 6.7 million in the quarter, representing a 2% increase compared to the year-end of 2022.

Direct and App Bookings

During the quarter, direct bookings achieved their highest level ever, indicating a growing trend of customers booking directly. Direct bookings are margin accretive and are expected to play a key role in future margin expansion as their share continues to grow.

45% of the room nights were booked through the company’s mobile apps in Q1’23 which is 5 percentage points higher than Q1’22.

Take Rates

The revenue as a percentage of Gross Booking, known as take rates, stood at 9.6%, slightly down from 9.9% in Q1’22 and significantly lower than the 11.2% recorded in Q1’19. However, this decrease is primarily due to a timing difference between GBV and revenue. Management reiterated that accommodation take rates remained consistent with 2019 levels.

Payments

Regarding payments, Booking .com processed 45% of gross bookings through its payments platform in Q1’23, a notable increase from approximately 34% in Q1’22 and 42% in Q4’22.

Profitability

Adjusted EBITDA of $586 million came in below the guidance of $600 million, representing EBITDA margin of 15.5% compared to 11.5% in prior year.

According to David Goulden, CFO, the lower adjusted EBITDA was attributed to increased marketing expenses incurred due to higher than expected gross bookings in future quarters.

Despite this, management still expects a few percentage points improvement in the adjusted EBITDA margin for the full year compared to the 31% margin achieved in FY 2022. This optimistic outlook provides confidence and the possibility of surpassing the EBITDA margin we estimated in our valuation back in July, in which we assumed an EBITDA margin of 31% for 2023.

While management anticipates that reaching pre-COVID margin levels may not be feasible due to a shift in the mix from agency to merchant, they do expect to grow the EBITDA margin beyond the levels seen in 2022. The primary driver of this growth will be the continued increase in the direct booking mix.

Free Cash Flow

Booking Holdings generated strong free cash flow (FCF) of $2.8 billion for the quarter, representing a remarkable 77% year-over-year increase. The company's increasing mix of payments through its platform has positively impacted the company's cash operating cycle, contributing to Q1 becoming a robust cash flow quarter.

Outlook

In terms of travel demand, room night growth remained strong in April, although the year-over-year growth decelerated to the mid-teens due to strong comparisons from 2022. Looking ahead to Q2’23, management anticipates mid-single-digit growth in room nights, while GBV is expected to increase by approximately 4% more. This growth is driven by the flight mix gaining share and the strengthening of constant currency ADR, resulting in an estimated GBV growth rate of approximately 9%.

David Goulden, CFO, mentioned that revenue as a percentage of gross bookings is expected to be around 120 basis points higher than the previous year. This is primarily due to a reduced negative impact from timing differences and increased revenue from payments. However, these positive factors will be partially offset by increased investments in merchandising and a higher mix of flights.

Overall, management forecasts imply a 20% growth in revenue and a 35% growth in adjusted EBITDA for Q2’23. These projections reflect the company's expectations for continued growth and favorable financial performance in the upcoming quarter.

Concluding Remarks

In conclusion, Booking Holdings' Q1’23 earnings report, highlighted solid performance across various key metrics, demonstrating the company's resilience and strong position in the travel industry. With record-breaking nights booked and impressive GBV growth, the company continues to capitalize on the global demand for travel.

Additionally, the increasing direct bookings is a positive indicator for future margin expansion. Despite the slight shortfall in adjusted EBITDA, management's commitment to margin improvement provides confidence in the company's long-term prospects.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward-looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

This post may contain affiliate links, which means that we might get a commission if you decide to sign-up using any of these links. No extra cost is charged to you.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.