Booking Holdings reported its Q3’25 earnings, delivering another strong quarter that beat expectations. The results showcased robust double-digit growth in bookings, EBITDA margin expansion and accelerating momentum in the U.S. market.

1. Financial results

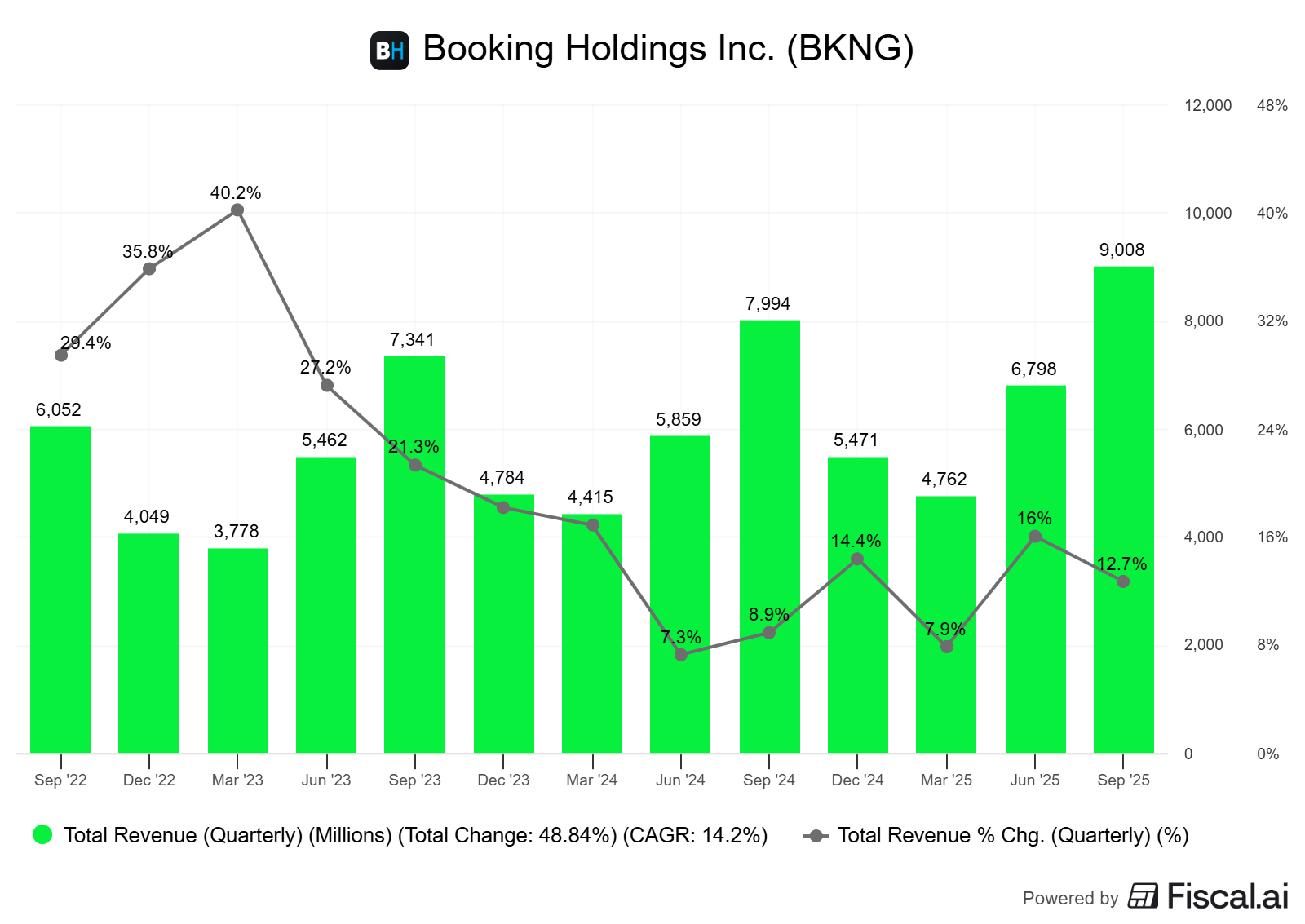

Revenue came in at $9 billion, representing year-over-year (YoY) growth of 13% (8% YoY on constant currency basis). This result exceeded the high end of management’s guidance. For Q4’25, management expects 10%-12% YoY growth.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Adjusted EBITDA for Q3’25 was $4.2 billion, up 15% from the prior-year quarter. This beat the high end of guidance by about 6 percentage points. The Adjusted EBITDA margin was 47.0%, an expansion of 120 basis points from Q3’24, driven by leverage in marketing and fixed operating expenses. Adjusted EBITDA for Q4 is projected to be between $2.0 and $2.1 billion, representing 8%-14% growth.

Adjusted EPS for Q3’25 was $99.5, up 19% from the prior-year quarter. EPS saw faster growth from adjusted EBITDA as a result of a 4% lower average share count.

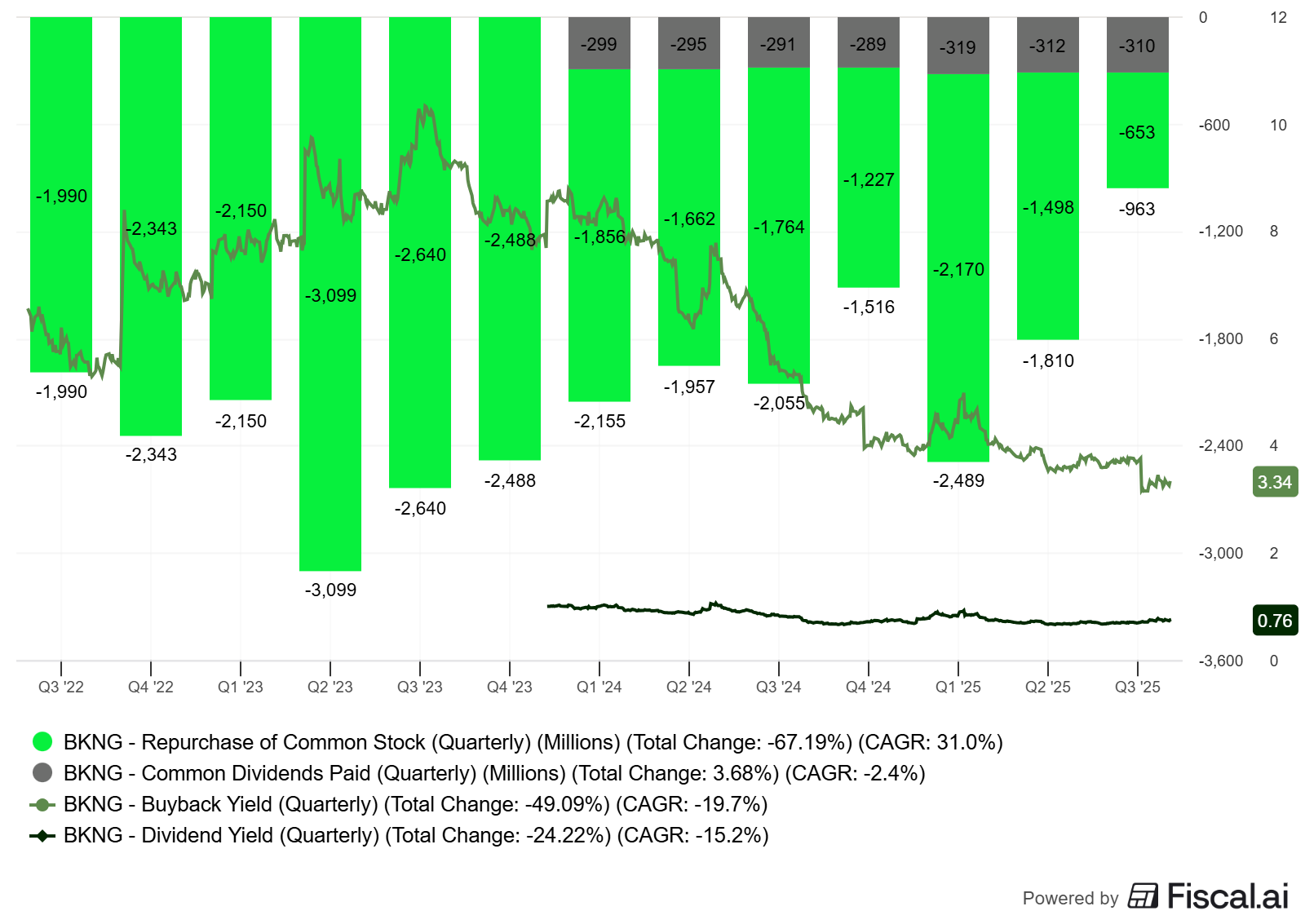

Capital Returns: Approximately $1 billion was returned to shareholders, consisting of $700 million in share buybacks and $300 million in dividends.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

2. KPIs

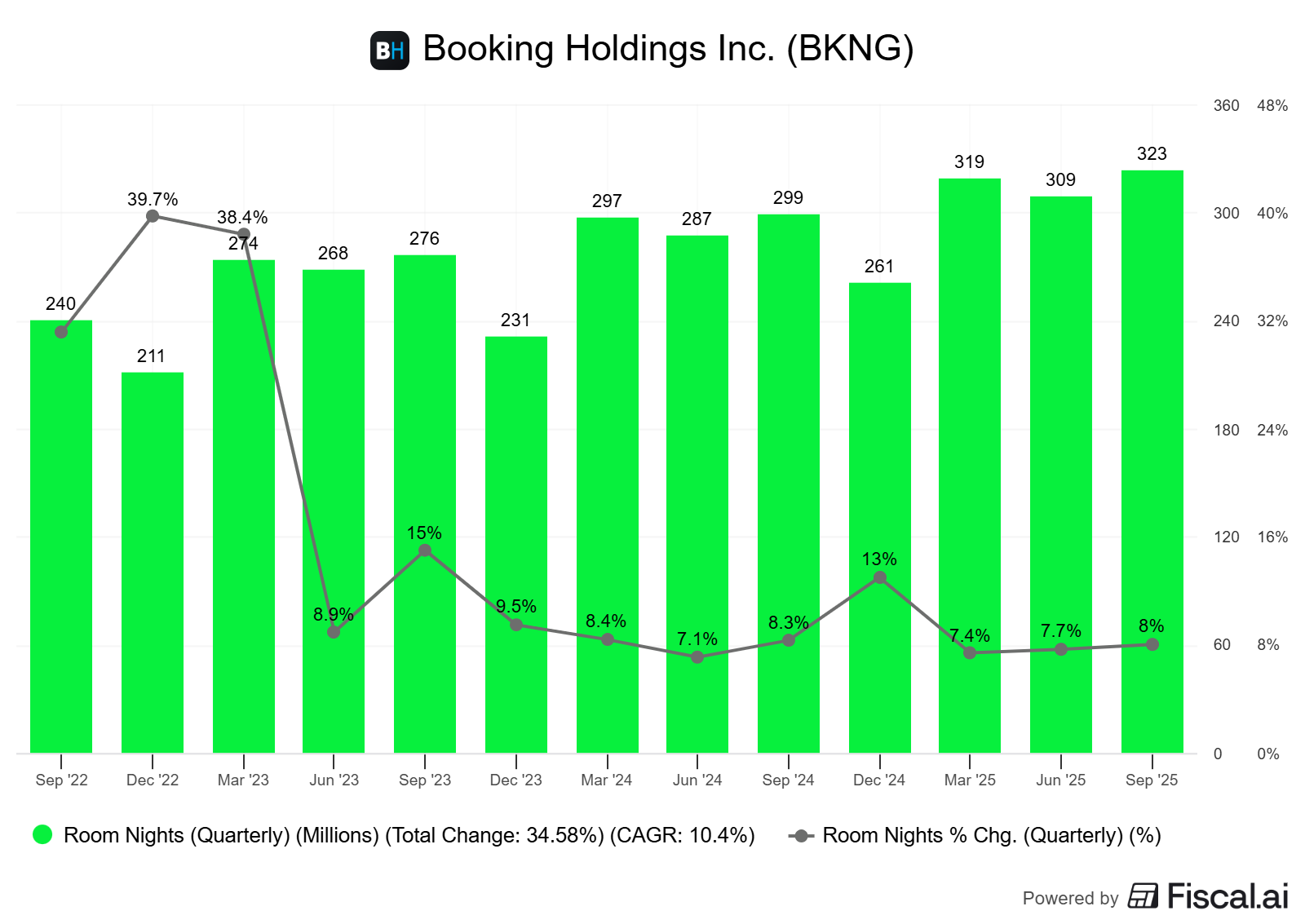

a. Nights Booked

Nights booked for the quarter reached 323 million, up 8% YoY and exceeding the high end of the guidance by 3 percentage points. Growth was driven by broad-based strength across all regions.

Europe and the U.S. were up high single digits.

Asia and Rest of World were up low double digits.

Notably, U.S. room night growth accelerated meaningfully from low single digits in Q2.

Looking ahead, 4%-6% growth is projected for Q4’25. Deceleration is expected due to shorter booking window anticipated in Q4.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

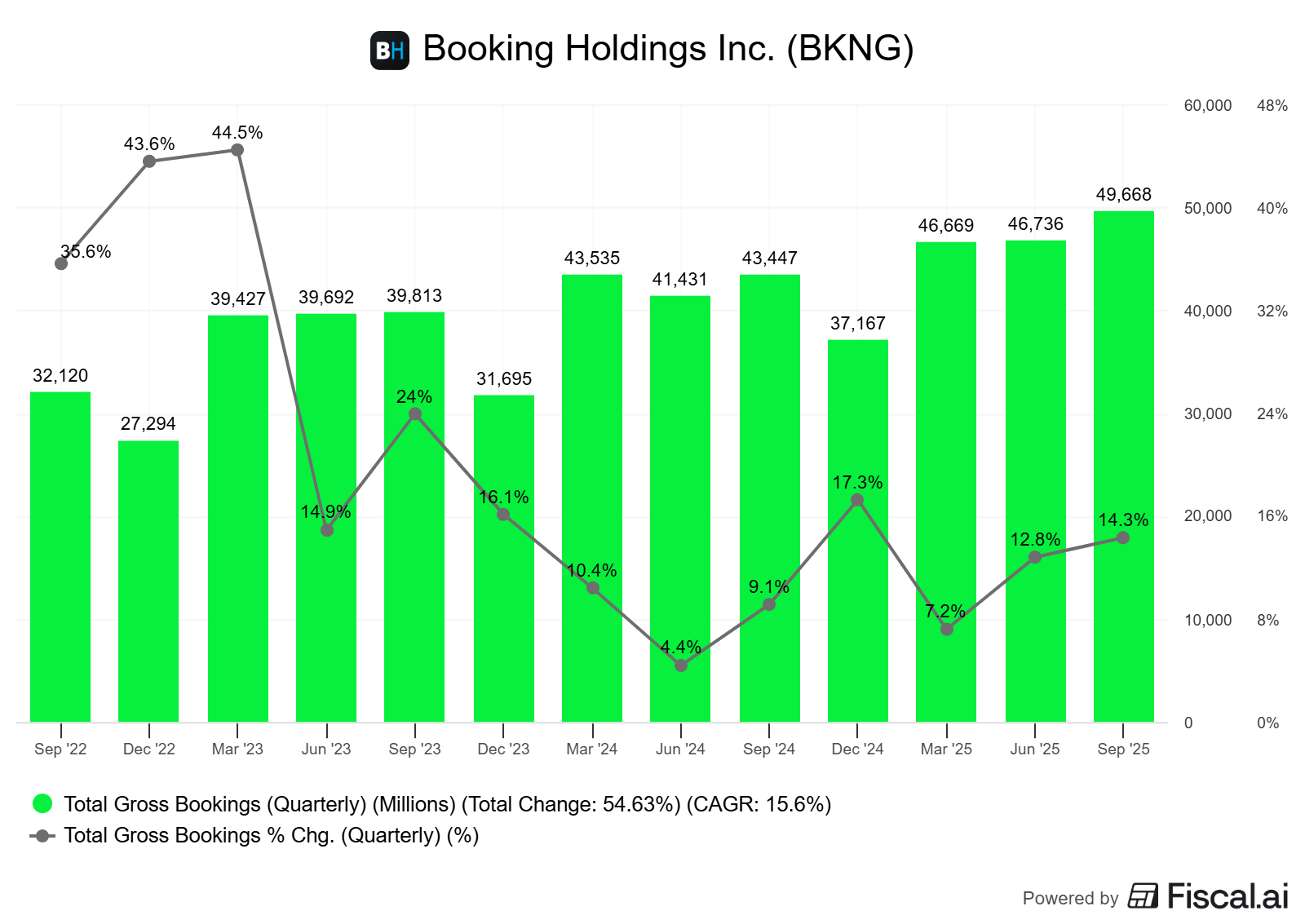

b. Gross Bookings

Gross Bookings in Q3’25 reached $49.7 billion, a 14% increase (10% in constant currency) that also exceeded guidance. Growth was driven by the 8% room night growth, 32% growth in air tickets, and a 1% increase in constant currency ADRs. Looking ahead, Booking projects 11%-13% growth for Q4. FX will positively affect Gross Bookings by 5 percentage points and airline tickets will have 2 percentage points of positive impact.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)