Champion Homes in a Rebounding Market ($SKY)

After five quarters of revenue decline due to muted demand in housing, Champion Homes (former name: Skyline Champion) returned to growth. With dynamics in place such as the start of a declining interest rate cycle, peaking of sales orders and recovery of the retail and REITs channels we are revisiting the Company to assess its performance, compare it to peers and perform a valuation.

If you're interested in learning more about Skyline Champion Corporation's business model, you can read our article, Skyline Champion Corporation – A Compelling Investment Opportunity, which we released in February 2023 (since then, the share price has increased by 39%). After that, check out the detailed update we published in September 2023, Skyline: On an acquisition spree. These resources will give you a solid understanding of the company before you dive in.

Brief Overview:

Champion Homes ("Champion", "Company") Overview

Champion offers a leading portfolio of manufactured and modular homes, park model RVs, accessory dwelling units (ADUs), and modular buildings for the multi-family and hospitality sectors. It is the second-largest player in the industry, behind Clayton Homes, owned by Berkshire Hathaway. From FY15 to the trailing twelve months (TTM) ending Q1 FY25, Champion achieved a revenue Compound Annual Growth Rate (CAGR) of 12.5% and an operating income CAGR of 66.9%. The company’s TTM revenue reached $2.2 billion, with operating income of $171.4 million and an operating margin of 7.8%. Champion also has a strong balance sheet, with $549 million in cash and cash equivalents, and only $25 million in long-term debt.

Key Investment thesis

The company operates 43 manufacturing facilities across the U.S. and 5 in Canada, providing cost efficiencies through bulk purchasing and reduced transportation costs. It holds a dominant position with 29% of U.S. production facilities (43 out of 148) and maintains a strong presence in the HUD code homes wholesale market with a 19.9% share, slightly down from 20.4% in FY23 but still second in the market. Manufactured home sales in 2023, at 89,000 units, are well below the historical average of ~200,000 due to limited financing options and historically low interest rates favoring traditional homes. With a leading portfolio, recognized as the "Most Trusted Manufactured Home Builder" for four consecutive years and receiving top design honors, the company is well-positioned to benefit from industry tailwinds like growing demand for affordable housing, easing regulations, and improved financing options for manufactured homes, especially as current mortgage rates make borrowing for traditional homes significantly more expensive.

Contents:

Performance Update

Industry

Valuation

Conclusion

1. Performance update

a. Revenue

With sales starting to ramp up, Champion’s revenue in the most recent quarter ending June 2024 reached $628 million, up 35%. Of course this amount includes sales of Regional Homes, an acquisition which closed in Q2’24. Excluding Regional Homes, revenue increased 2.5%, reversing from a decline of 12.9% in Q4’24 and a decline of 24.5% in Q3’24. Therefore, Q1’25 marks the first quarter of revenue growth, signaling better times ahead, particularly as we are at the onset of the interest rate cut cycle in the U.S.

Source: Koyfin (affiliate link with a 20% discount; if you are a paid subscriber, you can benefit from a 3-month free trial) * Q3’24 to Q1’25 also include revenue from the acquisition of Regional Homes

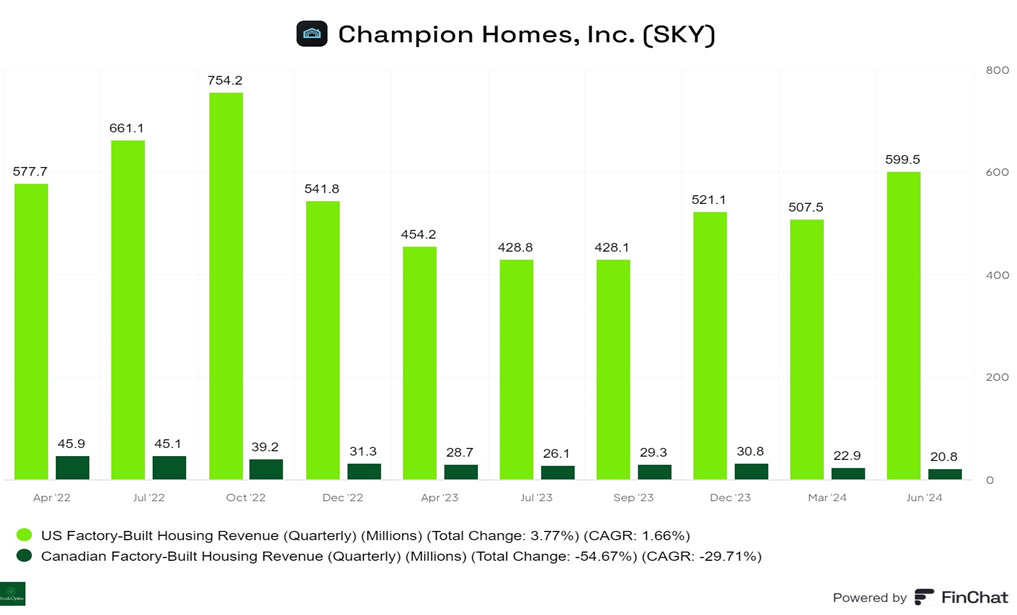

Revenue growth was driven by strong growth in the US which was up 40% year over year (up 4.5% excluding Regional Homes) offset by softer demand in Canada; where revenues declined by 20.4% year over year as a result of economic uncertainty and higher interest rates persisting.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

On a sequential basis (Q3’24 to Q1’25 include the acquisition of Regional Homes US) revenue growth in US was up 18%, accelerating from 3% decline in Q4’24. Sequential growth in US was primarily driven by community and retail sales channels. In Canada, revenue declined 9% sequentially, an improvement compared to the 26% drop in Q4'24. Overall, the US, which accounts for 94% of total sales, is showing positive signs of accelerating revenue growth, while softened demand in Canada continues to impact the market.

b. Home Sales

Revenue was up as a result of growth in the number of houses sold which grew 33% year over year reaching 6,705 units. Growth was driven by US with homes sales up 36%, reaching 6,538 houses sold while average selling price was up by 3%, due higher mix of retail units sold.