Cutting Through the Competition: Toro Company's Mow-tivating Journey

Every month we share 2 write-ups on companies we decided to examine as potential additions to our portfolio. Although the companies analysed may tick most of the boxes, if the margin of safety is not considered sufficient, we will not initiate a position but rather monitor the stock.

In case we decide to initiate a position at any time, we will share an Investment Thesis memo. For any additions to existing positions we will update you through our Quarterly Portfolio Updates.

1. Key Facts

Description: The Toro Company (“Toro”, “TTC”, and “Company”) is a ‘leading worldwide provider of innovative solutions for the outdoor environment including turf and landscape maintenance, snow and ice management, underground utility construction, rental and specialty construction, and irrigation and outdoor lighting solutions’. The Company operates through a network of distributors, dealers, mass retailers etc. and employs over 11,250 people as of October 2022.

Key Financials: Over the period FY13 to trailing twelve months (“TTM”) Q1 FY23, the Company depicted a revenue Compound Annual Growth Rate (“CAGR”) of 9.5% and operating income CAGR of 11.4%, reaching a TTM revenue of c. $4.7B and operating income of $624.6 million (margin of 13.2%). Toro has cash and cash equivalents of $174 million compared to total debt and lease liabilities of $1,168 million.

Price & Market Cap (as of 8th May 2023): Its market cap is $11.0 billion with a 52-week high of $117.66 and a 52-week low of $71.86, whereas it currently trades at $105.69.

Valuation: TTC trades at a TTM EV/EBITDA of 16.3 (10 Year average of 15.7) and a TTM EV/Sales of 2.5 (10 Year average of 2.4).

Note: Fiscal year 2022 (“FY22”) ended on 31 October 2022.

The rest of the write-up includes the following sections:

2. Business Overview

3. Management

4. Industry

5. Financial Analysis

6. Competitive Advantages, Opportunities and Risks

7. Valuation

8. Concluding Remarks

2. Business Overview

Its history in brief

The Company has roots dating back to 1914 with a turning point in its long history, being its former CEO Ken Melrose* who served as CEO for 24 years (1981 until March 2005). Under his leadership, TTC grew revenues from c. $247M to c. $1.7B due to the strategic shift to golf courses, sports fields and municipal parks and the Company moved from near-bankruptcy to success. The shift in strategy not only drove results but resulted to a more durable business model as from close to 1/3 professional sales mix it reached almost 65% by 2005 (in FY22 professional segment accounted for 76% of total sales).

The new strategy involved numerous acquisitions and Ken oversaw a number of acquisitions including Wheel Horse, Exmark, Lawn-Boy and Hayter. Acquisitions remain a priority in the capital allocation strategy of the Company (more details in Acquisitions and Capital Allocation).

The success story of TTC is justified by the total shareholder returns since inception, which per stratosphere.io are estimated at 18,338% or 12.8% CAGR (as of 8 May 2023).

*If you are interested to read more about Ken’s leadership here is a quote and a link:

“Under Ken’s leadership, Toro survived and then thrived, as he built a culture of employee engagement long before it was fashionable,” Mike Hoffman, who succeeded Melrose as CEO.

(Source: Ken Melrose, the 'servant leader' at Toro for 24 years, dies at 79)

Business Model

The Toro Company designs and manufactures its products / equipment / systems and sells through a network of more than 150 distributors, dealers, mass retailers, equipment rental centers, home centers, and online (direct to end-users) in more than 125 countries. Toro claims that its mass retailers (Home Depot, Tractor Supply, Ace Hardware) have over 8,000 locations and omni-channel solutions to serve customers whereas its dealer network exceeds 4,000 worldwide.

Its product offering is comprised of leading brands (see below) that serve golf courses, sports venues/fields, professional contractors, underground construction professionals, landscape contractors, agricultural growers, rental companies, government, educational institutions, and homeowners.

Note: Brands | The Toro Company – more details about each brand

Financing

To facilitate sales TTC formed a joint venture with Huntington Distribution Finance (subsidiary of The Huntington National Bank, “HBAN”), namely Red Iron Acceptance (“Red Iron”) in which it holds 45%. Red Iron provides distributors and dealers of Toro a reliable source of inventory financing (Red Iron holds security on the inventory) in the US and usually no down payment is needed, whereas finance charges can be shared (or borne exclusively by TTC) among TTC and the distributor or dealer. Except Red Iron, TTC engages in such agreements with Huntington Commercial Finance Canada (“HCFC”) and other third-party institutions.

The benefit of these agreements is the reduction in the cash operating cycle for Toro, the transfer of credit risk to Red Iron and the like and it provides attractive financing solutions to distributors and dealers.

Why does the above matter to our analysis?

The current banking turmoil affecting regional banks cannot be ignored as any negative development with HBAN can distort the operating model of TTC. To understand its significance, in FY21 and FY22 the amount financed for dealers and distributors through financing institutions accounted for 69.3% and 72.2% of total sales, respectively (Red Iron FY21: 72.9%, FY22: 72.3% of US sales), whereas the receivable days would have increased from c. 22 days to c. 85 days if such financing arrangements were not in place.

The impairment of the investment in the joint venture ($45.7M) will be immaterial if it crystallizes. What will be distorting is a potential decline in sales and profitability if alternative source of financing at similar terms cannot be found promptly. The Company may have to finance an extended operating cycle through debt negatively affecting its profitability.

What are the mitigating factors?

Per HBAN’s latest 1Q 2023 presentation: a) it has the highest percentage of insured deposits among peers at 69% (SIVB was at 12%), b) it consistently grew deposits above peers despite the challenging environment, c) cash and borrowing capacity as a percentage of uninsured deposits is at 136% with the next best peer at 91%, and d) it has the 3rd best CET1 ratio.

Markets and Sales Mix

The Company has three reportable segments, professional, residential and other while it also provides a breakdown by product type (equipment and irrigation) and geographic market (US and International).

Source: 2022 TTC Annual Report

Professional Segment

Professional segment products (think of reel, riding and walking mowers, all-wheel drive tractors, zero-turn radius riding mowers, heavy-duty walk behind mowers, walk and ride trenchers, vacuum excavators, utility locators, snowplows, sprinkler heads etc.) are primarily sold through distributors and dealers and address the following markets:

Golf market (golf course turf maintenance & irrigation, water application solutions),

Sports fields and Grounds market (sports fields turf maintenance & irrigation, water application solutions),

Landscape contractor market (turf management solutions),

Underground construction market which was enhanced by the acquisition of Charles Machine Works (“CMW”) in FY19 (products are utilized by specialty contractors to install water, gas, electric, telecommunication, fiber optic, and other utility distribution systems).

Rental and Specialty Construction market (primarily sold to rental companies, large retailers and dealers),

Snow & Ice management (snow removal products),

Commercial Irrigation & Lightning, and

Ag-irrigation market.

The below slide gives an indication on the weight of each end market.

Source: Investor Presentation The Toro Company, Q4’22, Note: Underground and specialty constructions were affected by the acquisition of CMW

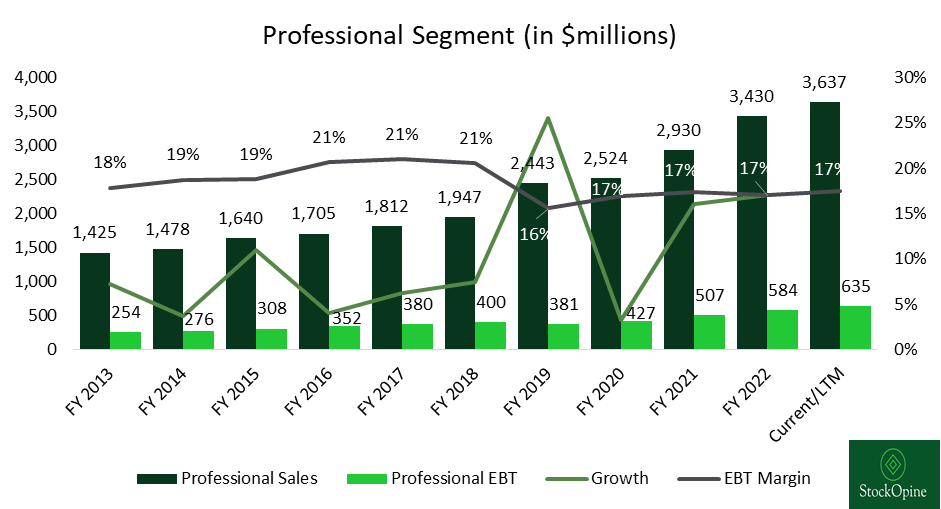

Over the period FY13 to Q1FY23, the Professional segment depicted a CAGR of 10.7% reaching total sales of $3.6B and by FY22 it accounted for 76% of total sales compared to 69.8% in FY13. The segment also generated 84% of TTC’s earnings before taxes (“EBT”) in FY22 (ignoring ‘Other’ which includes corporate costs).

Source: TTC 10K filings, StockOpine analysis

Revenue growth over the years was driven by acquisitions, increase in volumes, and net price realization. For instance, in FY19 the acquisition of CMW was a key determinant of the 25.5% increase whereas in FY22 the growth of 17.1% was driven by net price realization (think of higher prices net-off promotions and incentives) and a 4.1% impact from the acquisition of Intimidator.

The Professional segment is a higher margin business than the Residential and it averaged at 18.4% over the period FY13 to FY22. The decline in FY19 is explained by the acquisition of CMW, however, the margins improved from 15.6% in FY19 to 17% in FY22 following the acquisition.

It shall be noted that Intimidator carries a lower margin but going forward an improvement should be expected in margins as material, freight and manufacturing costs normalize.

We are of the opinion that the Professional segment is more critical for the long-term success of the Company as it is more durable and less prone to economic cycles.

Q4’22 Richard Olson CEO (own emphasis) “And that's probably the key point is most of our products are used for essential tasks. They're not discretionary. So especially in the context of a business, many of our Professional customers are -- have delayed purchases through the early part of the pandemic, and they're already behind. And our products are consumed when they're used. So if they're being used then they're being consumed and they need to be replaced.”

Residential Segment

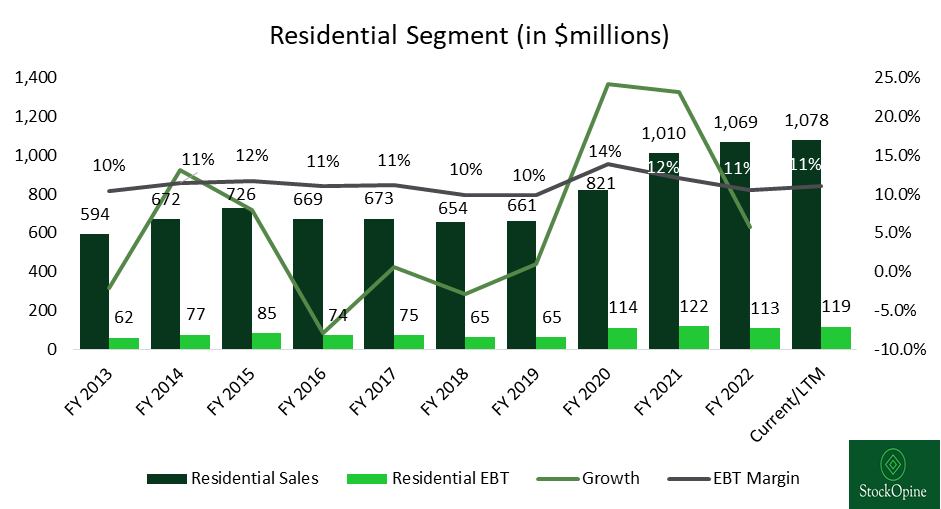

Residential segment consists of products, such as walk power mowers, zero-turn riding mowers, and snow throwers which are generally sold to home centers, mass retailers, dealers, hardware retailers, as well as online (direct to end-users).

Source: TTC 10K filings, StockOpine analysis

Over the period FY13 to Q1FY23, the Residential segment depicted a CAGR of 6.6% reaching total sales of $1.1B and by FY22 it accounted for 24% of total sales and 16% of TTC’s EBT (ignoring ‘Other’ which includes corporate costs).

Revenue growth in latest years aligns with other companies that benefited from customer trends in spending more for their homes.

Margin wise, the Residential segment averages at 11.2% (Vs 18.4% of the Professional) and it dropped from 13.8% in FY20 to 12% in FY21 and 10.5% in FY22 mainly due to the higher material, freight and manufacturing costs. The lower margins compared to the Professional segment are justified by the fact that consumers purchase Residential products at mass retailers like Home Depot and home centers which typically offer lower price points.

Although margin is expected to improve due to productivity efficiencies and normalization in the above mentioned costs, we can infer that TTC Residential segment has less pricing power compared to the Professional segment. This is further supported by the fact that over the years, Home Depot accounts for ~10% of total sales or c. 35%-40% of residential sales.

Notes on the by product and geographic mix

By Product: Since FY13 the weight on equipment grew from ~81% to ~90% as the acquisitions such as CMW, Venture Products (Ventrac Brand) and Intimidator further enhanced the equipment offering.

Geographic: “We believe many opportunities exist in the international markets, and over time, we intend for international net sales to comprise a larger percentage of our total consolidated net sales.”

When you see that in the 10K you might envision that the future is still ahead for the international segment. Yet this is not the case as with a CAGR of 4.6% since FY13 (Vs 11.2% of US) and international weight declining from ~30% to 19.6%, one can understand that international market is unlikely to move the needle (at least organically). Needless to say that the same 10K comment appeared back in FY15 when the weight stood at 25.5%.

Manufacturing

Source: Investor Presentation The Toro Company, Q4’22

TTC has manufacturing facilities across the globe with the majority located in the US and with 90% of its manufacturing hours attributable to the North America operations. Given the weight of US sales this makes sense.

It follows a ‘Kanban’ manufacturing system which effectively is just-in-time manufacturing aiming to maximize efficiencies and improve processes. Nevertheless, the abnormal supply chain disruptions over the last couple of years along with the strong demand resulted to an elevated backlog of c. $2.3B (as of FY22 and Q1FY23) which management strives to normalize.

“And we will be working to bring down the backlog. In some cases, that can be done more quickly because the supply chain constraints has resolved more quickly. Others will extend out throughout the year, but we know we're going to be managing the backlog throughout the year.” Richard Olson, Chairman and CEO, Q4’22