This is the first article in the new type/format, as announced in our latest post (Portfolio Update). In this article, we will focus on how PayPal executes on its key strategic areas, such as Branded Checkout, Braintree and Venmo, while comparing it with peers. Additionally, we conduct a DCF and sum of the parts valuation to assess whether the current price levels present a compelling opportunity. Please note that this article does not contain generic information. If you would like a better understanding of how PayPal operates, we suggest that you read our report that was written back in March 2022.

Contents:

Key information

Where does PayPal stand today?

Branded checkout

Braintree & unbranded processing

Venmo

Valuation

Conclusion

1. Key information

PayPal Holdings Inc. (“PayPal”, “Company”) market cap as of 18th of July stands at $83B and has a 52-week low of $58.95 and a 52-week high of $103.3, whereas it currently trades at $74.4.

PayPal trades at a TTM EV/EBITDA of 15.9x (5-Year average of 40x) and a TTM Price / Earnings of 31.5x (5-Year average of 54x).

Note: As of 18th of July 2023

PayPal was called a ‘pandemic darling’ and its performance over the COVID era has smashed the S&P 500, however, when management made its best possible effort to lose trust from investors (withdrawal of 750M active accounts target, consistent downward revision of forecasts, margin compression) and when the macro environment worsened, PayPal came down to earth. Let’s dive in to understand whether this is justified.

Source: Koyfin (affiliate link with a 15% discount)

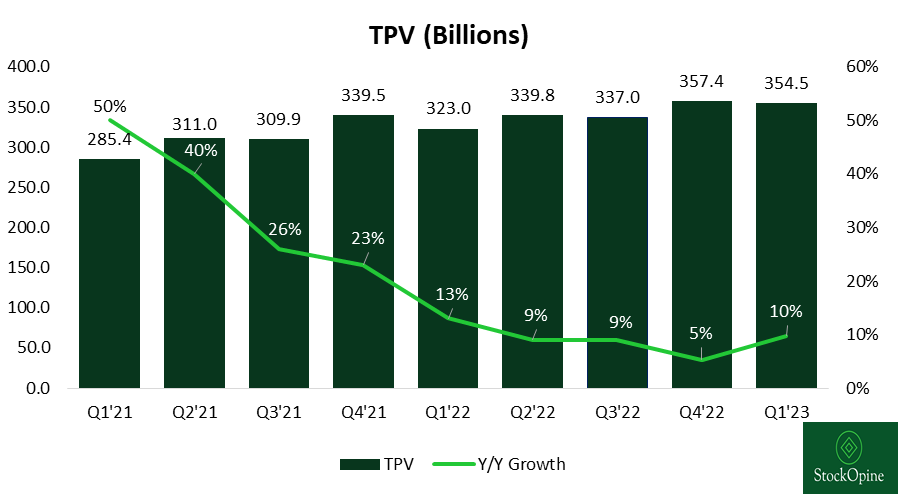

To help you follow along this write-up, here is a breakdown of PayPal’s TPV in the respective payment platforms.

Source: Q4 2022, PayPal Investor Update

2. Where does PayPal stand today?

A picture or two, worth more than a 1,000 words.

Source: Company filings, StockOpine analysis

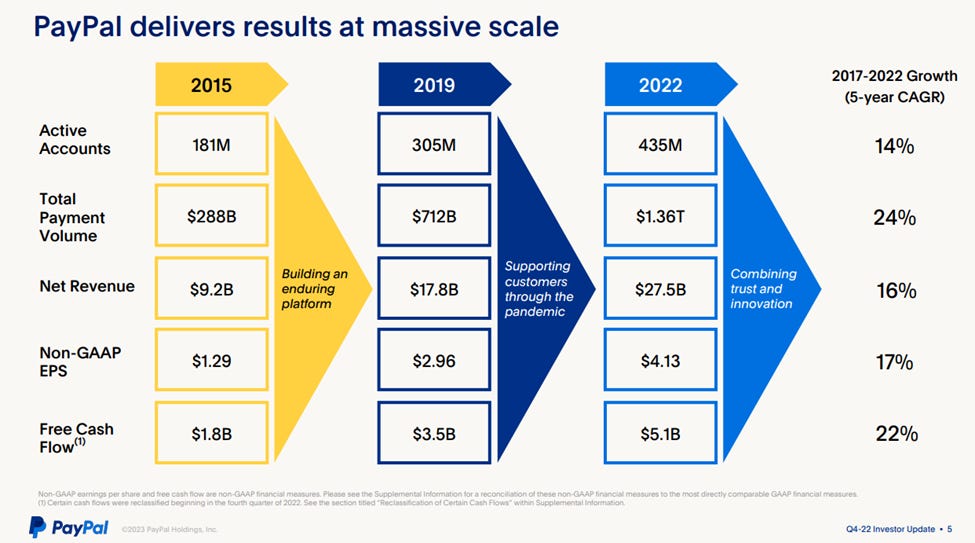

Following the acceleration in Active Accounts during the pandemic period, reaching 435M accounts (of which 35M are merchant accounts) in 2022 compared to 305M back in 2019, we observe the first real churn in Q1’23. This is of low concern as the focus shifted to engagement.

Acting CFO, Gabrielle Rabinovitch recently highlighted this (own emphasis).

“And so we've called out that we have about 190 million monthly active unique users on our platform.

So it's this very sizable number. And our monthly active unique users are actually 20 to 30x more valuable than an overall kind of average active account. And so what we're really focused is on growing that number because when we get someone to use us instead of 8x a month, 16x a month, the incrementality in our business is very, very significant. And so we think about like the best use of our marketing spend, the best use of our rewards programs. It's really about more deeply engaging our base today so that we increase the monthly active unique user base relative to just sort of growing active accounts.”

Looking at the Total Payment Transactions per Active user (“TPA”), the trend is clearly upwards and PayPal depicted a double-digit growth in all of the last 8 quarters showcasing the Company’s ability to execute on the engagement front. As one should have expected, a key driver of this trend is the high growth in unbranded processing and mainly Braintree (which we will discuss later).

As long as TPA grows we are happy, yet we do feel that active accounts remains a meaningful metric for the future success of the Company. It is a relevant number for its network strength and losing to Apple Pay (Statista reported 507M Apple Pay users for 2020 and presumably this number has increased) remains a risk.

Source: Company filings, StockOpine analysis

Another metric that gives a holistic view of performance is total payment volume (“TPV”). TPV has consistently increased over the last years and quarters with Venmo and Unbranded Processing being the key drivers of 2021 while in 2022 was all about Unbranded processing (~40% growth).

The inflection of the trend in Q1’23 (10% or 12% on FX neutral basis, “FXN”) is encouraging as there was a sequential TPV growth acceleration across all key areas with branded checkout increasing by +2 pts to 6.5% y/y, unbranded processing by +1 pt to 30% y/y and Venmo by +6 pts to 9% y/y.

Source: Q4 2022, PayPal Investor Update

All in all, the numbers show that despite the slowdown in 2022, PayPal does well and has various routes that can support its future growth. For the record, total revenue in 2022 grew from $25.4B to $27.5B or by 8.5% (10% on FX neutral basis) while the growth in ecommerce retail market stood at 7.1% in 2022 as per Insider Intelligence. Not too bad!

3. Branded checkout

Branded checkout is the bread and butter of PayPal but it is assumed by many as ‘dead’ and ‘unable to innovate’ losing share to companies like Apple.

This might hold true in certain regions but there are metrics / statistics that imply otherwise. For example, the below chart shared by the Company in its Q4’22 Investor update shows that PayPal’s digital wallet acceptance among the largest retailers in North America and Europe grew faster than any of its peers (in par with Google Pay), reaching 79% or 2.8x its next peer.

Source: Q4 2022, PayPal Investor Update

Furthermore, per Datanyze, PayPal is the #1 software in payment processing with a market share of 40.5%, while the next in line are Stripe with 20.5%, Shopify Pay with 13.7% and Amazon Pay with 4.9%. Although this comparison is not apples to apples it does speak of PayPal’s scale.

Management has repeatedly stated over time that despite losing market share in certain markets their overall position is on a ‘holding or gaining’ share.

PayPal’s Branded Checkout TPV which accounts for ~30% of its total TPV of ~$1.36T (in 2022) grew by 5% in 2022. This is not distant from the growth in ecommerce retail market of 7.1% mentioned earlier while the acceleration in Q1’23 to 6.5% y/y is promising.

The growth in the high margin branded checkout is far from over and we believe that the following quotes justify why (own emphasis).

“This isn't a zero-sum game between digital wallets. We are all feeding off of people manually entering their card. That's still 25% to 30% of the market. We're taking a lot of share from that as our other digital wallets.” Dan Schulman, President & CEO

“Well, I mean we definitely have goals to increase it in the double digits, and that is really about making sure that we are thinking about the next generation of Checkout, which is going to include AI, which is going to use the data that comes from the unbranded business to really create sort of the demographic of the consumer, which enables us to then target in a much better way and enables merchants to be able to target the consumer in a much better way” Peggy Alford, EVP Global Sales

The growth of unbranded helps in gathering important data and also deepens relationship with merchants. When implemented, checkout comes with the latest integration updating legacy integrations and creating better experiences for customers and merchants making it more relevant in the payment ecosystem.

Does it innovate?

With all the updates going on, such as reduced latency, passwordless authentication, rewards, Venmo and PayPal operability and package tracking refining the experience, engagement and thus results are expected to improve. As shown in the picture, there is a +33% payment conversion when PayPal is an option vs cards at checkout and +25% uplift on consumers to complete a purchase due to the payment method selected.

Source: Q1 2023, Investor Update

If you are not convinced yet, just note that in 2022 Dan Schulman CEO indicated that

"We had record platform availability in 2022, and we put out approximately 80,000 software releases.”

while in Q1’23 PayPal Investor Update the following was noted,

“In addition, PayPal is helping to power payments through Microsoft Teams. This allows many service-based small business owners like dietitians, cooking instructors, therapists or tutors to receive payment during a one-on-one appointment or in the class, directly in Microsoft Teams.”

Isn’t that an innovation?? One can argue otherwise but we are pretty happy with the efforts and progress.

PayPal Vs Apple Pay

This is a huge debate and no one can argue that Apple Pay is not catching up. It has the network, trust and reliability to compete on the branded business while it has one great advantage. Near-field communication (“NFC”) that enables contactless payments.

PayPal claims to have the highest acceptance at merchants, the highest conversion rates and the lowest loss rates for merchant partners while its add-on services like rewards, discounts, promotions, Buy Now, Pay Later (“BNPL”), package tracking enhance its offering. Nonetheless, they do admit that authentication (catching up with passwordless login, passkeys, biometrics) and NFC chip are where Apple stands out.

This relationship is competitive, yet, PayPal partnered with Apple Pay to tap on its Tap to Pay technology (NFC) and to allow consumers in US to use PayPal and Venmo on their Apple Wallet. Consumers come first and when ease of transaction comes to place this is a solid move. Why miss that customer when he/she wants to use his/her Apple device?

Apple appears to have the leverage, though it is more of a mutual relationship as Apple also benefits by having Apple Pay as an option when online stores use PayPal’s unbranded checkout flows. Two statistics are also worth noting:

a) Per Statista, the latest global market share for Android mobile operating system stands at 70.8% vs 28.4% for Apple.

b) The total transaction value in the Digital Payments market is projected to reach $9.46T in 2023 and $14.78T by 2027, depicting a compound annual growth rate (“CAGR”) of 11.8%.

Obviously, the market is huge and growing, the competition is intense and constant innovation is necessary, though, having ~70% Android mobile operating systems makes it clear that this is not a ‘winner takes all’. It’s no coincidence that in June 2023, PayPal also announced the rollout of its Tap to Pay on Android for Venmo and PayPal Zettle users in US expanding the Tap to Pay functionality to its wider customer base.

4. Braintree & unbranded processing

Unbranded processing (of which the majority is Braintree – a full stack processor) is the fastest growing payment platform of the Company with a TPV growth rate of 40% in 2022 and 30% in Q1’23 (42% for Braintree), however, due to lower take rates and higher cost of funding, the segment has negative impact on transaction margins and thus on operating margins of the Company. At least for now…we will cover this shortly.

The key competitors are Stripe and Adyen and management has consistently stated that they are taking share from them (own emphasis).

“On the unbranded side, look, we're clearly taking share. Without a doubt.” Gabrielle Rabinovitch, Acting CFO

“We've also taken share from not only incumbents but also the 2 that you've mentioned. So we're winning deals, again, Adyen and Stripe, especially through our bundled value position and our integrated offering.” Frank Keller, SVP Merchant & Payments

Let’s dive into the numbers to understand whether this is the case.

Source: Company filings for Adyen and PayPal, Stripe 2022 annual letter, Bloomberg News, Stripe Revenue and Growth Statistics (2023) (backlinko.com), StockOpine analysis | Note: Adyen volumes were translated to USD using the average rate for each year per ECB

The higher growth rate of Braintree (~40%) justify that management is right. They lagged behind initially but in 2022, PayPal had some great wins (Airbnb, Live Nations, Uber etc.) which allowed it to win market share. The competitive advantage of PayPal is clearly bundling (think of what Microsoft does with Teams and Office) and the ability to offer a wide range of solutions in a single deal. More likely than not, this will allow it to capture more market share in the future.

“And we're leveraging that relationship, create bundled capabilities. We're really this trusted partner out there that can serve Pay with PayPal, Pay with Venmo, Buy Now, Pay Later, post-purchasing capabilities out of one hand. And those packaged deals are sticky. They create a nice value prop. They provide us the ability to negotiate top of the stack placement.” Frank Keller, SVP Merchant & Payments

Additionally, Peggy Alford EVP Global Sales states that Braintree has better auth rates than peers which means that the percentage of transactions passing through (and thus resulting to a complete payment) is higher keeping both merchants and customers happy.

Looking at take rates, Adyen’s gross take rate stood at 1.16% in 2022 while Stripe’s stood at 1.85% in 2021. Despite the lower take rates, Adyen is profitable at EBITDA margins of ~8%-11% (using gross revenue) while Stripe generated an EBITDA margin of 4% in 2021 and was loss making in 2022 (growing at all costs??).

Per our estimates, the take rate of Unbranded processing (includes Braintree), currently ranges within 0.9% - 1.25%* indicating that not only PayPal differentiates on bundling but also offers an attractive price.

*TPV of Venmo stood at $245B in 2022 and generates over $100M per month (implied take rate of 0.5%), while if we assume a take rate of 3% for Checkout & Other, the resulting rate for unbranded which had a TPV of $400B in 2022 is 1.2%. Doing a similar exercise for 2021 yields an unbranded take rate of 0.9%. Per these estimates, Unbranded processing revenue is estimated at ~$4.5B-$5.0B for 2022.

Take rates & Margins

Over the years take rate has declined significantly as eBay business was lost and as Unbranded and Venmo businesses grew. Recently, the key explanation that management gives for the lower take rates, the higher expense rates and consequently lower transaction margins is a change in mix towards unbranded.

Source: Company filings, StockOpine analysis

Although this harms the business profitability in the short term (chart below), it is a conscious decision that will expectedly drive margins higher in the future.

Source: Company filings, StockOpine analysis

For starters, PayPal currently serves large companies in the US with higher volumes and thus lower take rates but with the launch of PayPal complete payments (“PPCP”) it will tap into a new unbranded total addressable market of ~$750B (estimated by management) and will allow it to serve SMBs and regions like Europe driving margins higher. PayPal doesn’t have a strong presence outside US while Dan Schulman indicated that they never had a product to compete on the lower end of the marketplace.

Considering that Unbranded Processing in 2022 generated about $4.5B-$5.0 sales (own estimates) and comparing this to the gross revenues of €3.4B (38% of total sales) for Adyen in the EMEA region one can understand that the opportunity is real.

“We know that we are able to -- just because of interchange, we're able to get higher margins on our unbranded products outside of the U.S., especially in Europe, and there is a very high demand for them. And so PayPal Complete Payments enables us to offer our processing products at a higher margin outside of the U.S.” Peggy Alford, Executive VP Global Sales

Furthermore, the add-on services like risk and FX as a service have higher margins and as these expand (land and expand strategy) margins will go higher.

PayPal is serious about the unbranded margin expansion. This is not just a 5-year desire but something that is happening today and will likely have an impact in less than 2-years. We applaud the growth in unbranded and we acknowledge management’s efforts to improve unbranded margins. The recent execution on the non-transactional expenses (-6% y/y in Q4’22 and -12% y/y/ in Q1’23) is an example that helps to regain trust in management.

5. Venmo

Venmo and digital wallets is the third pillar of PayPal’s strategy. As shown in an earlier chart, Venmo generated a TPV CAGR of 55% over 2018-2021 while the TPV FXN growth in 2022 stood at 7%.

Source: Company filings, StockOpine analysis

Even though the TPV growth decelerated materially in 2022 to 6.6% Vs 44% in 2021, it accelerated sequentially in Q1’23 from 3% to 8.5%. Monetization efforts have also started to play out well with an increase of 33% in revenues to ~$1.2B (own estimates) from ~$900M revenues in 2021. We believe that there is more room for expansion.

“By the way, that's not to say that it's not growing great. It's doing over $100 million of revenue every single month, growing at double digits. It's obviously a meaningful part and a growing part of PayPal. But I think there's so much more that we can do with the franchise.” Dan Schulman, CEO

Dan Schulman also agrees on take rate expansion but here’s why we think this is achievable.

First of all, the resulting take rate is estimated at 0.5%, up from 0.4% in 2021, but as it expands on the business side with the Tap to Pay partnerships on iOS and Android (discussed earlier) this would eventually go higher (just look at Venmo business profile transaction fees of 1.9% + $0.10 and 2.29% + $0.10 for contactless payments). On top of this, the full rollout of paying with Venmo on Amazon is another gateway for take rate expansion. We consider that growing take rate is a realistic expectation as out of the 90M US active accounts, 2/3 are monthly active indicating that the app is part of their everyday life.

Venmo has similar users as Cash App (of Block) which as of 31 December 2022 had 51M monthly transacting actives (up to 53M in Mar-23), yet monetization wise Venmo does badly. It is estimated that Cash App revenue (excluding Bitcoin) per monthly active stands at ~$69 in 2022 (up 32% compared to 2021) while Venmo’s respective amount stands at ~$21 (up by ~20% Vs 2021). Assuming Venmo manages to achieve $45 over the next three years, Venmo revenue could increase by 117.5% (CAGR of 26.5%) to about $2.6B (from current run rate of ~$1.2B) without even tapping on the international market.

Is there a reason to believe that Venmo can’t compete with Cash App? We think no and many others agree as Venmo scores 4.9 in App store and 4.2 in Google Play store while Cash App scores 4.8 and 4.6, respectively.

6. Valuation

We analyzed the 3 key pillars of PayPal and we can conclude that its competitive position remains strong despite the fierce competition, while the execution on unbranded processing, the potential on Venmo and the wider industry forecasts* indicate that the future is still bright.

* a) Global Retail Ecommerce Forecasts 7.1% in 2022, 8.9% in 2023, 9.4% in 2024, 8.8% in 2025 and 8.1% in 2026, b) The total transaction value in the Digital Payments market is projected to reach $9.46T in 2023 and $14.78T by 2027, depicting a CAGR of 11.8% and c) The Payment Gateway Market size is expected to grow from USD 13.97 billion in 2023 to USD 29.89 billion by 2028, CAGR of 16.43%.

The stock price as of 18th of July 2023 stands at $74.37 with a year to date return of 4.4%. The Company's market capitalization is $83B and it trades at an EV/EBITDA TTM multiple of 15.9x. Based on our DCF valuation, the estimated price of PayPal is $89, 19.5% higher than its current price, with an expected IRR over a 5-year period of 15.2%.

Source: StockOpine analysis

To estimate the fair value of PayPal, we assumed a revenue CAGR of 7.6% in line with analysts’ expectations as of 2025 and using own estimates thereafter. By 2027 we reach total sales of $39.7B which translates to a TPV of ~$2T, if a take rate of 2% is assumed. Comparing these assumptions with industry expectations and taking into account the unbranded processing and Venmo potential we can conclude that we are relatively prudent.

In terms of profitability, we used an average EBITDA margin of 20.1% and terminal projected EBITDA margin of 20.9%. The estimated EBITDA margin is higher than the 5-year average EBITDA margin of 19.1% but there are few reasons why we believe this is feasible: a) the cost optimization program that is underway, b) a saving of 0.7% on Stock-based compensation compared to the 5-year average of 5.7%, and c) better monetization of Venmo which will partly offset the negative impact from unbranded processing. Even if unbranded margin expands due to PPCP, it is worth noting that Adyen’s gross EBITDA ranges at ~8%-11% levels, well below the current levels of PayPal. As this is a critical assumption, refer to our sensitivity analysis for a better understanding of how does the estimated value change when the margin changes.

To derive the free cash flows to the firm we deducted projected Capex requirement of 3.2% over revenue which is in line with the target of management of 3% but lower than its 5-year historic Capex of 3.9%. FY22 ratio stood at 2.6%.

In terms of the terminal EV/EBITDA multiple, we assumed a multiple of 15x which is lower than its current TTM multiple of 15.9x and its 5-year average of 33x (excluding 2020). The main reason of this assumption is due to the fact that we expect gains to be derived from earnings growth rather than a multiple expansion, yet we will happily welcome any change in market perception. For context, Adyen trades at a multiple of 58x while Fiserv and Global Payment trade at multiples of 13.7x (19x, 5-year excluding 2020) and 12.2x (20.5x, 5-year excluding 2020), respectively.

To calculate the value per share we used the minimum required return that we aim to obtain from our investments (i.e., 10%) under the current environment, adjusted for net debt and non-operating assets / liabilities identified and thereafter divided the resulting value by the number of shares.

Based on these calculations and assumptions (which may not materialize), we estimate a value per share of $89, which is higher than the current price of $74, resulting to an IRR over a 5-year period of 15.2%.

Sensitivity analysis

The below table gives an indication of the potential upside/(downside) %age compared to the current price ($74 as of 18th July 2023) when the terminal multiple and the terminal EBITDA margin are changed.

Source: StockOpine analysis

Sum of the parts – back of the envelope calculation

Source: StockOpine analysis

The breakdown of revenues for 2022 is derived from the analysis we mentioned earlier (repeated for ease of reference).

*TPV of Venmo stood at $245B in 2022 and generates over $100M per month (implied take rate of 0.5%), while if we assume a take rate of 3% for Checkout & Other, the resulting rate for unbranded which had a TPV of $400B in 2022 is 1.2%.Per these estimates, Unbranded processing revenue is estimated at ~$4.5B-$5.0B for 2022.

Braintree & Unbranded value was estimated by multiplying its 2022 TPV of $400B with the average EV / TPV ratio of Adyen and Stripe (estimate of Stripe value can be found here), that is 0.07x resulting to an EV of $26.7B.

Venmo value was estimated by multiplying its revenue of ~$1.2B with the latest EV/Sales ratio of Block (excluding Bitcoin sales) of 4.5x, resulting to an EV of $5.4B. We believe that this is a sensible approximation as 50% of Block’s gross profits are derived from the Cash App ecosystem.

By deducting the above from the current EV of PayPal of $84B, we reach an implied value for the rest of the business of c. $52B that translates to an EV/Sales ratio of 2.4x. That is well below the 5.6x of Fiserv, 5.1x of Global Payments, 4.5x of Block, 4.7x of Adyen and its own average of 5.4x since 2015 (excluding 2020 and 2021). Based on this, we can assume that the rest of the business can be valued at a minimum of 3x EV/Sales, resulting to a potential upside of 15%.

7. Conclusion

As previously mentioned, we maintain our belief that the business remains healthy, and investors need not be discouraged. Although competition dynamics are evolving, PayPal continues to be a relevant player, and the sequential acceleration of TPV growth across all pillars demonstrates that growth remains robust. While it is reasonable to acknowledge that the growth rates observed during the pandemic era will not be sustained, we anticipate steady growth in the high single digits, accompanied by margin improvements.

Considering the appealing valuation, tomorrow* we will increase our allocation to our biggest loser, which currently accounts for 3% of our portfolio and has incurred a loss of 30%, by 1.5% (to reach 4.5% allocation).

* subject to the price trading below $78

Note: There are many things that we did not discuss on this article like management which admittedly improved with John Kim as a CPO and Gabrielle Rabinovitch as Acting CFO, yet the new CEO appointment is what matters the most. BNPL also grows exponentially and PayPal takes share.

Great insight! I completely agree that Paypal seems to be the most cost-effective option among its major competitors, and it appears to have a strategic advantage in maintaining its take rates at a lower level than the others while remaining profitable for an extended period of time. It's interesting to note that the current EV/EBIT ratio is much lower for a mature company that is not growing. There is definitely potential for Paypal to double its EV/EBIT ratio, which could translate into a share price of around $120. However, a more realistic approach would be to consider the DCF, which suggests that the share price could be around $90. Overall, it seems that Paypal has a strong upward potential with minimal downside, making it an attractive investment opportunity.