Every month we share 2 write-ups on companies we decided to examine as potential additions to our portfolio. Although the companies analysed may tick most of the boxes, if the margin of safety is not considered sufficient, we will not initiate a position but rather monitor the stock.

In case we decide to initiate a position at any time, we will share an Investment Thesis memo. For any additions to existing positions we will update you through our Quarterly Portfolio Updates.

A quick note before we begin. The team is currently offering a 15% discount on all plans until the end of June 2023.

1. Key Facts

Description: Diageo plc (“DGE”, “Diageo”, and “Company”) produces, markets, and sells alcoholic and non-alcoholic beverages. Its portfolio which exceeds 200 brands comprises among others of Johnnie Walker (Scotch whiskey), Smirnoff (vodka), Guinness (beer) and more.

Key Financials: Over the period FY13 to trailing twelve months (“TTM”) 1H FY23, the Company depicted a revenue Compound Annual Growth Rate (“CAGR”) of 4.3% and operating income CAGR of 4.7%, reaching a TTM revenue of c. £16.9B and operating income of £5.3B (margin of 31.4%). Diageo has cash and cash equivalents of £2.8B compared to total debt and lease liabilities of £18.0B.

Price & Market Cap (as of 13th June 2023): Its market cap is £75.2 billion with a 52-week low of £33.0 and a 52-week high of £39.7, whereas it currently trades at £33.5.

Valuation: Diageo trades at a TTM EV/EBITDA of 15.8x (10 Year average of 18.8x) and a TTM EV/Sales of 5.5x (10 Year average of 6.3x).

Note: Fiscal year 2022 (“FY22”) ended on 30 June 2022.

Remaining sections:

2. Business Overview

3. Management

4. Industry

5. Financial Analysis

6. Competitive Advantages, Opportunities and Risks

7. Valuation

8. Conclusion

2. Business Overview

Diageo’s past and present

Diageo’s roots span across multiple centuries, with brands such as Haig Club dating back to the 17th century. The Company itself, however, was formed through the merger of Grand Metropolitan and Guinness in 1997. Soon thereafter, Diageo consolidated its fast-growing spirits segment by selling off subsidiaries in the food industry, such as Burger King, the fast-food restaurant chain and Pillsbury food unit for $1.5 Billion and $4.5 Billion respectively.

Since then, Diageo has become one of the world’s largest manufacturers of spirits and beer and owns over 200 brands with sales in more than 180 countries.

Its portfolio comprises among others of the world's bestselling Scotch whiskey, Johnnie Walker, the world’s bestselling cream liqueur, Baileys, the world’s best-selling premium distilled vodka, Smirnoff and other iconic brands such Tanqueray gin and Guinness beer.

Source: Corporate website

Diageo not only owns leading brands but also some of the fastest growing spirit brands in the world. Per Drinks International (The Millionaires’ Club 2023), Diageo, in 2022, owned 3 of the 10 largest spirits in terms of cases sold, 11* of the top 30 fastest growing brands and held 5 spots in India’s (which is the fastest growing market in alcohol sales as per Statista) top 10 fastest growing brands.

*This includes Black Dog, a brand owned by United Spirits, Diageo’s subsidiary, with a 57.1% growth, Royal Challenge with 53.2%, Chrome Vodka with 46.2%, Casamigos with 45.5% and Don Julio with 44.4%.

Acquisitions

Diageo’s strategy in breaking into new markets or dominating existing markets is supported by acquiring or heavily investing in brands.

Recent acquisitions range from alcoholic spirits (Aviation Gin and Davos Brands), to ready-to-drink (Loyal 9 Cocktails), and to non-alcoholic spirits (Seedlip).

Acquisitions are risky in nature, if Diageo overpays, but the execution in tequila brands is worth noting. Don Julio acquisition in 2015 and Casamigos in 2017 proven to be consequential for Diageo’s success story in this category with sales increasing from c. £105M in FY16 to c. £1.5B in FY22.

The following screenshots reveal the importance of acquisitions in Diageo’s strategy over the years:

Source: Diageo’s Annual Report FY22

The acquired brands account for £7.9B or 22% of total Diageo’s assets in FY22. Including goodwill and other intangibles (primarily the distribution rights for Ketel One vodka) they account for 33% of total assets.

Source: GAGNY 2023 Diageo presentation

“Since fiscal '17, we have invested £2.2 billion in acquisitions, ten of which are in fast-growing super premium price segments. During the same period, proceeds from divestitures, which are mostly brands that either did not really fit within our portfolio, and mostly played in slow-growing segments, have netted us £1.2 billion”, Lavanya Chandrashekar, CFO (own emphasis)

It can be concluded that Diageo’s does not perform acquisitions just for the sake of it but targets brands that will be the next key growth drivers and are aligned with consumer trends such as premiumisation.

Segments

For the purpose of this analysis we will focus on two distinct breakdowns, i.e. by region and by category, expanding on specific brands if deemed necessary.

Geographic breakdown

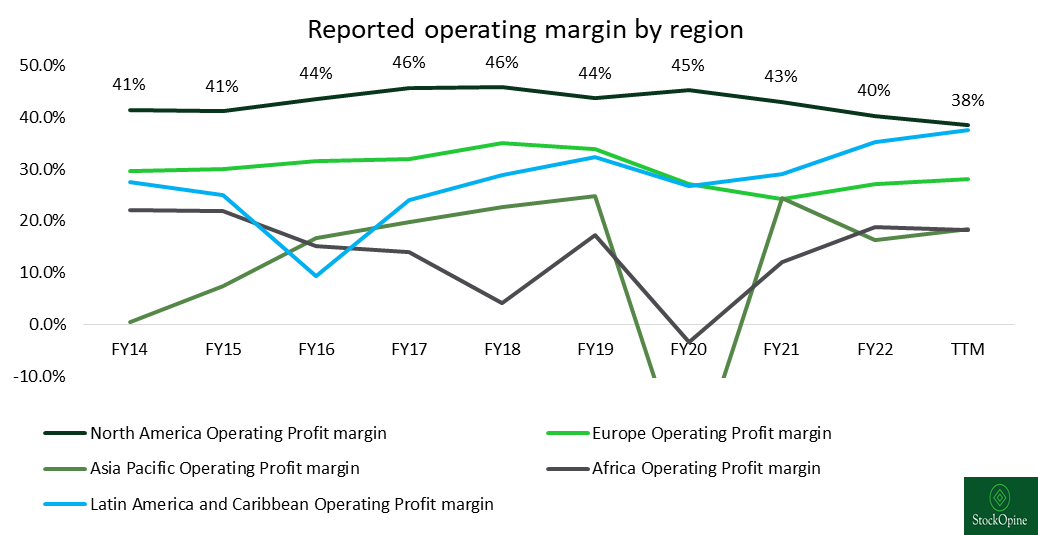

Diageo’s reports revenue and operating profit by North America, Europe, Asia Pacific, Africa and Latin America and the Caribbean.

Source: Diageo’s Annual filings, Stratosphere.io, StockOpine analysis

North America

North America is the largest market of Diageo and as of FY22 it accounted for £6.1 billion or 39.4% of total net sales, whereas over the period FY14-1H FY23 it depicted a CAGR of 8%. Following the COVID-19 outbreak, all regions’ net sales declined except North America which showed strong off-trade market in the second half of FY20 and double digit growth rates on Tequila net sales (36%). Since then, revenue mix from North America has increased significantly from the 32% to 35% range to the ~40% levels.

North America is the largest and the most profitable segment, driven by premiumisation trends of the market. The declines observed in the below chart regarding North America margins from FY21 onwards, are mainly justified by marketing expenses which grew from 17% of net sales in FY20 to 18% in FY21 and 19.7% in FY22.

Source: Diageo’s Annual filings, Stratosphere.io, StockOpine analysis

In general, marketing cost is not expected to come down as management considers it a required investment to drive future long term returns.

“I mean, if you look at the last 3, 4 years, we've massively up weighted investment in the U.S. market…. So we build our marketing budgets bottom-up, but what you see in the trend is our orientation is to lean in and spend more because we do believe there's plenty of attractive growth to be had. And we are very focused on the sustainability of the growth, as I talked about earlier. This is not just about delivering a return in the next 6 months. So that's the approach we take.” Ivan Menezes, former CEO (own emphasis)

Europe

Europe sales have declined as a percentage of sales to 20.8% or £3.21 billion as of FY22 compared to an average of 24.4% over FY14-FY19, whereas over the period FY14-1H FY23, it depicted a CAGR of 2.4%. Europe was hit hard during the pandemic and only managed to exceed pre-pandemic levels in FY22. Although Europe seems like a laggard, it is worth noting that margins are generally in line with the Company’s average and in the last 6 months it depicted a growth of 10%, demonstrating that it remains a relevant market for the future success of Diageo.

Asian Pacific

A rather complicated region is the Asian Pacific market which as of FY22 generated 18.7% of net sales or £2.88 billion and over the period FY14-1H FY23 it depicted a CAGR of 10.7%. Success of Diageo in the region is driven by Diageo’s Indian offerings like Mc. Dowell’s No.1 (largest Whisky brand in terms of cases, and 4th largest Rum brand) as well as its market position of owning 5 of the top 10 fastest growing brands in India.

India and Greater China are key markets for Diageo’s future. It is estimated that Scotch is the number 2 spirit in China behind Baijiu (a white liquor) while India recently exceeded France as the largest Scotch whisky market (per Scotch Whisky Association page 12), a category where Diageo is the undisputable leader.

Profitability fluctuates and is generally lower than other regions (chart above) as the market is more volatile (brand impairments due to Russia-Ukraine war in FY22, Covid-19 regulations in India and Korea in FY20 hitting the fair value of the respective cash generating units etc.) yet it remains an exciting region.

“So, we're definitely seeing that Scotch is hot and you saw it in the numbers today and we definitely do believe there is an opportunity for Scotch to continue to recruit consumers. Especially when you look at it from a lens of emerging markets, Latin America, Asia, India, there's definitely opportunity for us to use Scotch as a way to recruit more consumers into spirits and then within the spirits framework, to premiumise the category as well.” Lavanya Chandrashekar, CFO (own emphasis) Scotch presentation

A potential tailwind to Asia Pacific sales is regulation. As noted earlier, Asia Pacific sales account for less than 20% of net sales while India’s excise duties disproportionately account for over 31% of total excise duties. Management revealed that it expects Indian duties to come down (given recent developments) and if these come down, Diageo would be able to pass on these reductions to consumers to boost demand.

Latin America and the Caribbean

As we don’t see anything fascinating for the Africa region other than generating net sales of £1.682 Billion or 10.9% of total sales in FY22 and having numerous brewing facilities, we will jump into the Latin America and the Caribbean (“LAC”) region.

LAC contributed £1.525 Billion in revenues for FY22, which accounts to 9.9% of total revenues. A rather slow growth region over the period FY14-1H FY23 with a CAGR of 5.5%, but accelerated growth since FY20 due to the efforts in advertising and promotion, the growth in Scotch and the premiumisation trends. LAC, since FY20, is the fastest growing region of Diageo, with a CAGR of 31.7%, compared to a CAGR of 15.6% in North America over the same period.

LAC is growing fast and it is the second most profitable segment of the Company due to Scotch’s (a rather premium spirit) expansion impacting sales mix.

“Whisky in Latin America is directly associated with status and aspiration. The consumer wants to show they are successful, they want to show that they know how to appreciate quality and they want complexity and intensity in flavours. All of that basically is Scotch. That's why Scotch is thriving in Latin America.” Alvaro Cardenas, President in Latin America and Caribbean

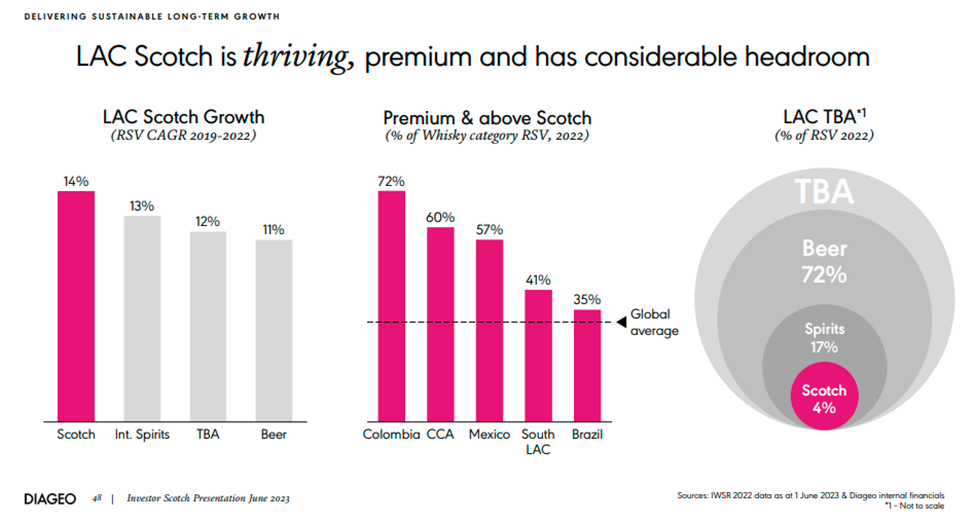

So how does Diageo stand in the LAC Scotch market?

It is the clear leader with a 70% market share in Scotch (next peer has 19%) or 74% in the premium plus categories. Per Alvaro Cardenas, President in Latin America and Caribbean the number one, number two and number three brands, are Johnnie Walker, Buchanan's and Old Parr, respectively (all owned by Diageo).

And what is the opportunity?

Source: Investor Scotch presentation Diageo, June 2023

Scotch is growing faster than the TBA industry (14% Vs 12% CAGR over FY19-FY22) whereas it only accounts for a small portion of LAC’s TBA at 4% compared to 14% internationally (as provided by Diageo – source IWSR 2022) indicating a considerable room for growth.

Additionally, during the Scotch presentation Alvaro Cardenas indicated that LAC region has favourable demographics with 340 million legal purchasing age (“LPA”) consumers compared 160 million in US, a growing middle class from 22% fifteen years ago to a current 38% and high acceptance in younger LPA consumers strengthening the opportunities for success in the region.

Sales by category

Source: Diageo’s Annual filings, StockOpine analysis | Notes: *In FY16 Canadian and US Whiskeys were reported as North American Whisky, **First time it is reported

The key category is Scotch accounting for 27% of total sales in 1H23, while other important categories are Tequila, up from 1% in FY16 to 11% in 1H23 (CAGR of 56.6%), Vodka and Beer whose sales declined as a percentage of sales over FY16-FY22, yet, they generated a CAGR of 2.1% and 4.6%, respectively.

Whisky

Even though Diageo does produce International whiskey, such as Bulleit whiskey and the internationally loved Crown Royal, Scotch is at the core of Diageo. The Company produces over 40 Scotch whisky brands, including Johnnie Walker, The Singleton, Buchanan’s, J&B, Grand Old Parr, Talisker and many more. Diageo operates 30 Scotch whisky distilleries, which account for +20% of total whisky distilleries in Scotland.

As indicated on the latest Scotch presentation, Scotch is the 2nd largest international spirit category accounting for 14% of TBA (IWSR 2022) while it is the leading