Earnings in Focus: Booking Holdings, Evolution AB & Meta

Yesterday, we shared the April 2025 Valuation Update, which compares current stock prices to our estimated intrinsic values. The report also included earnings overviews for Adyen, Allegion, PayPal, Evolution, Meta, and Booking.

To continue delivering value to our free subscribers, we’re sharing the earnings highlights for Evolution, Meta, and Booking below.

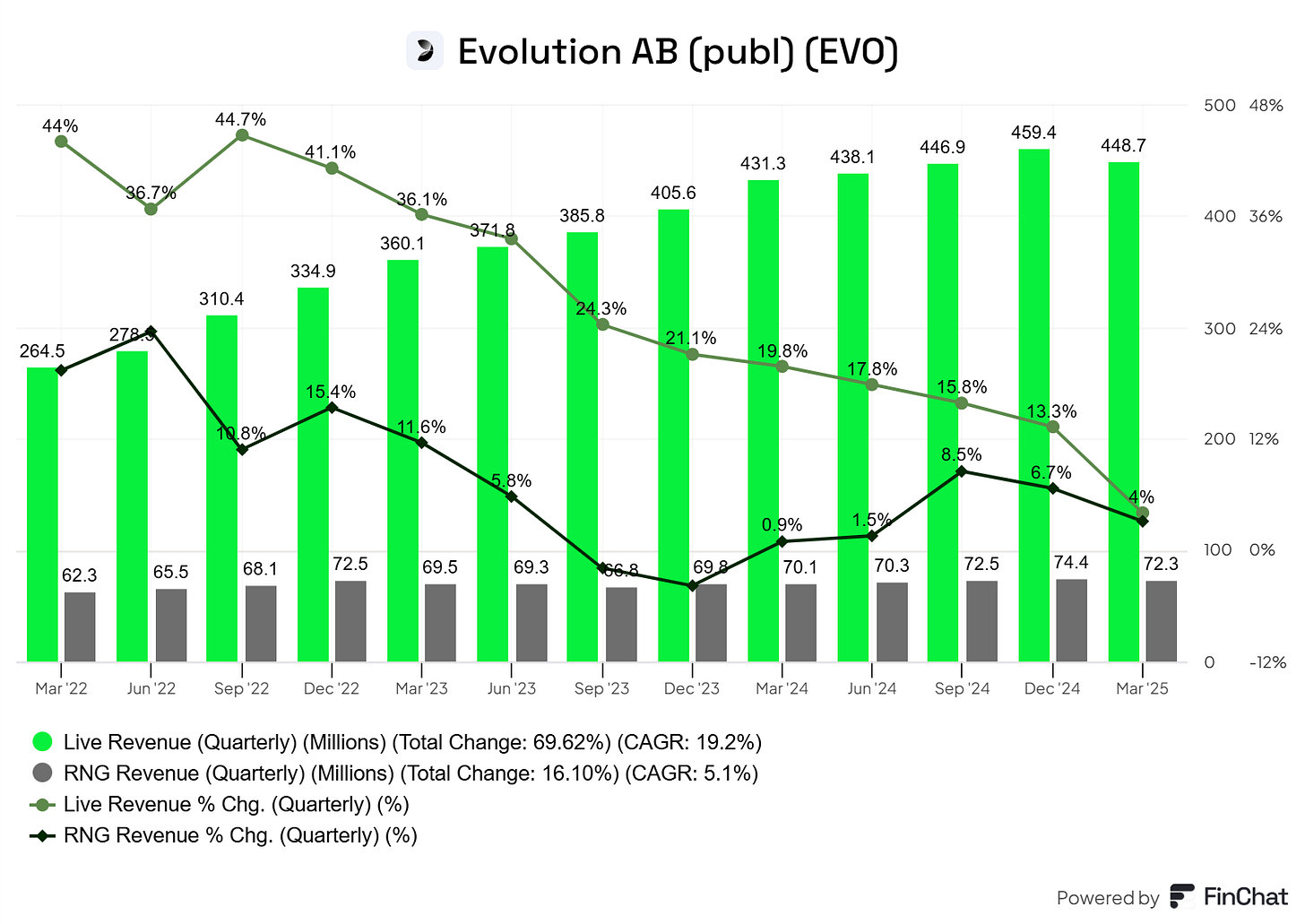

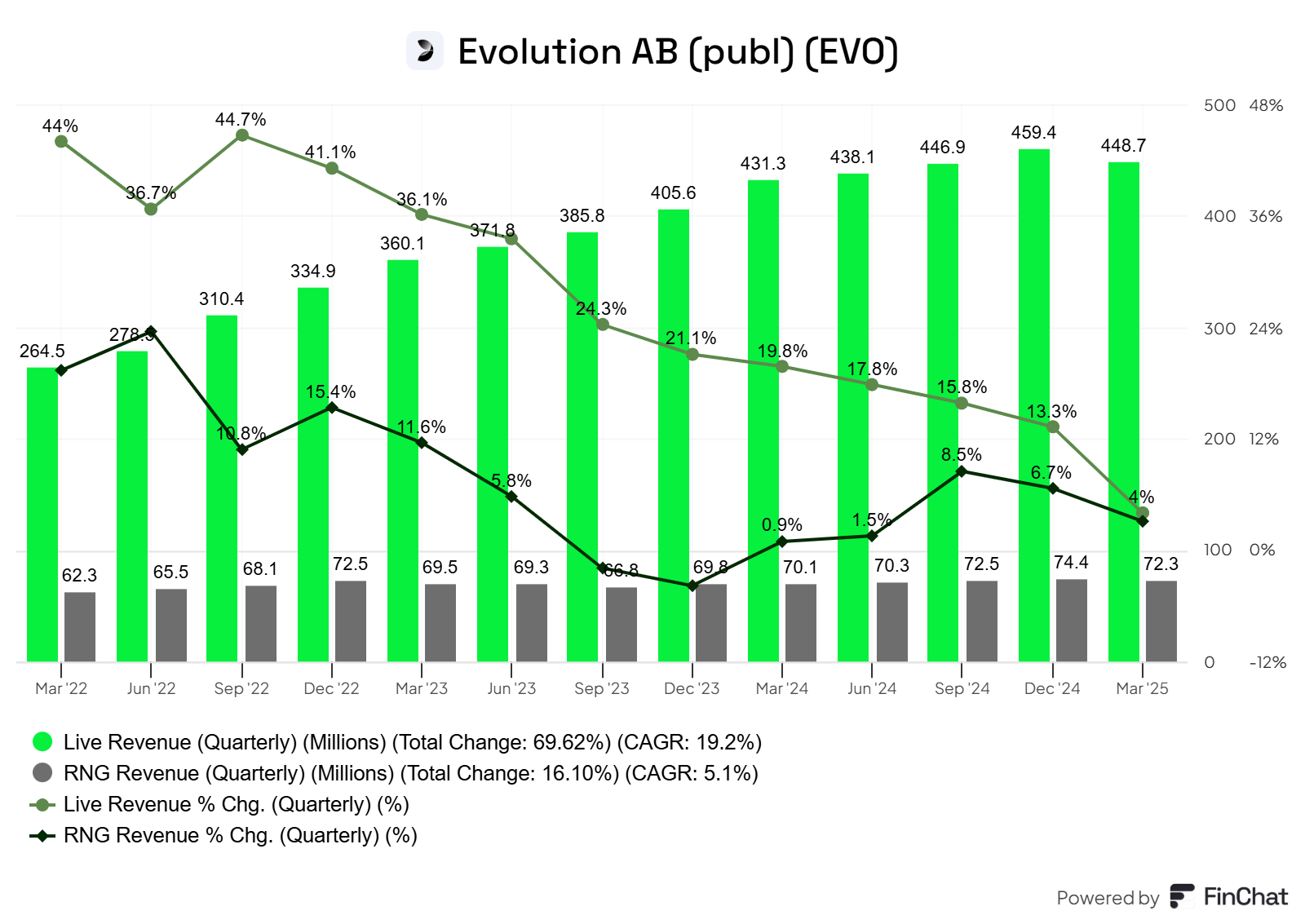

Evolution AB Q1’25

Evolution reported Q1 2025 net revenues of €520.9 million, a 3.9% increase (6.1% on constant currency) compared to Q1 2024 (€501.5 million), reflecting a significant slowdown in growth. Live Casino revenue grew 4% YoY to €448.7 million, while RNG revenue grew 3.1% YoY to €72.3 million. EBITDA fell 1.1% YoY to €342.0 million from €345.8 million, with an EBITDA margin of 65.6%, down from 69.0% in Q1 2024. Profit for the period dropped 5.4% to €254.7 million (€1.24 EPS) from €269.2 million (€1.27 EPS).

CEO Martin Carlesund attributed the slowdown in growth and lower profitability to two main factors:

Ring-fencing of regulated markets: Technical measures were implemented to ensure games are only available through locally licensed operators in regulated jurisdictions in Europe. This impacted revenue most in markets with low channelization, with European revenue flat YoY and down 6% sequentially. The share of revenue from regulated markets rose to 45% from 39% a year ago.

Asian cyber activity: Ongoing efforts to combat criminal cyber activity in Asia, which limited revenue growth in the region (Asia revenue +2.2% YoY, flat sequentially).

Despite these challenges, the company reaffirmed its full-year 2025 EBITDA margin guidance of 66% to 68%, with confidence in a strong H2 recovery driven by an extensive product roadmap (over 110 new releases planned for 2025) and continued studio expansion, including new locations in Romania, New Jersey, Brazil, the Philippines, and Michigan. On a positive note, North America showed strong growth (+15% YoY), and LatAm grew by 9.7% YoY).

While this was a weak quarter, the shift toward regulated revenue should benefit Evolution over the long term. We previously shared a stress-test calculation in the chat, which highlights that the current price is highly attractive. However, with EVO already representing over 5% of our portfolio, we’ll look to add only if we see a clear shift in fundamentals.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

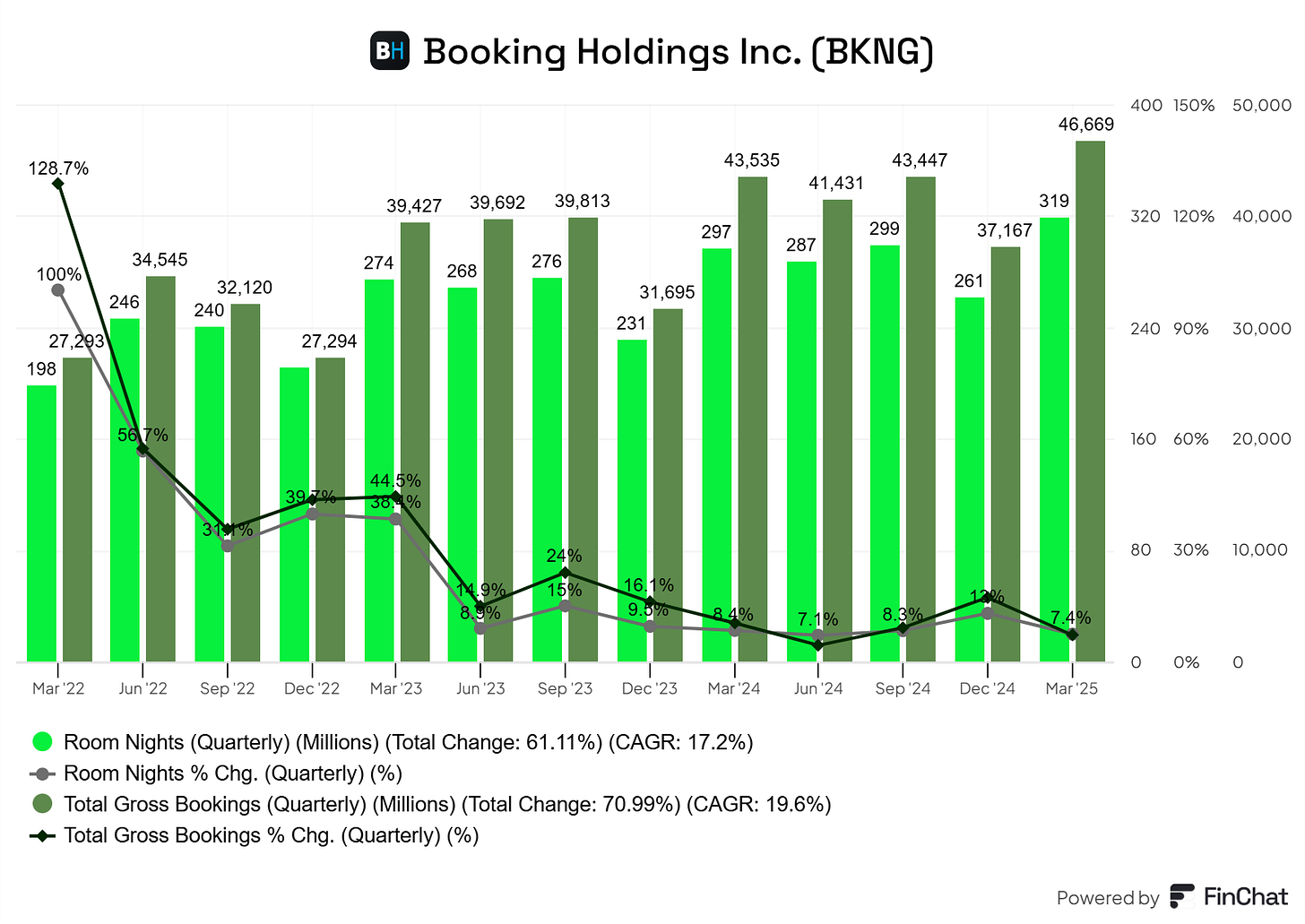

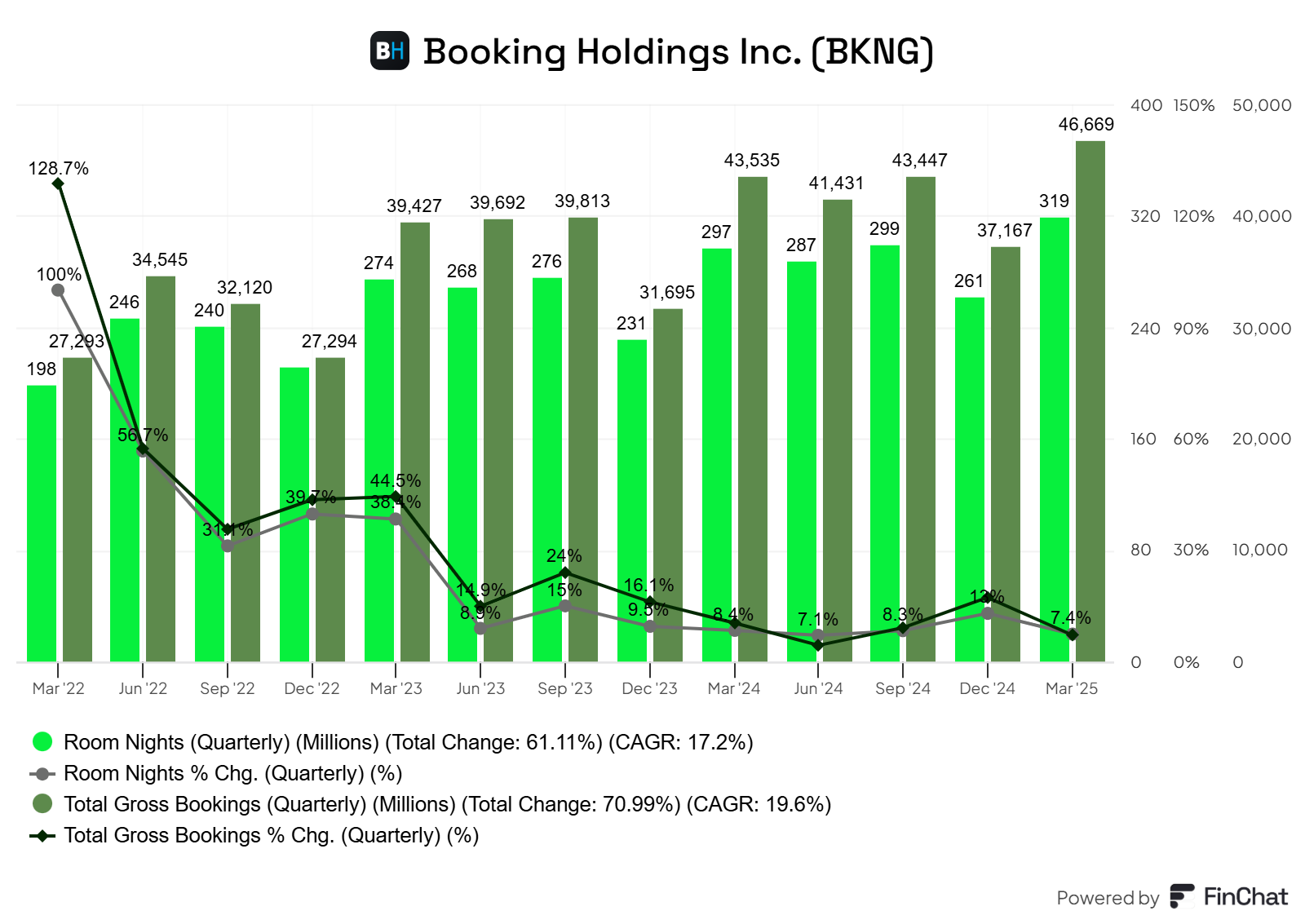

Booking Q1’25

Booking Holdings started 2025 on a strong note, with revenue up 7.9% YoY (10% in constant currency) to $4.76B. Gross bookings rose 7% YoY (10% cc) to $46.7B, and room nights grew 7.2% to 319M. Operating income jumped 34% to $1.1B, with margin expanding to 22.3% from 17.9%.

However, GAAP net income fell 57% YoY to $333M, driven by a hit from non-operating items, including a $392M debt discount amortization adjustment, $389M FX loss on euro debt remeasurement, and partially offsetting items like a $158M fair value change on the conversion option of convertible bonds and a pension accrual reversal. As a result, GAAP EPS dropped 55% to $10.07 (from $22.69).

Adjusted EPS rose 22% YoY to $24.81 (vs. $20.29), stripping out these one-offs. Other highlights include:

Direct booking mix in the mid-60s

Alternative accommodations room nights up 12% (now 37% of mix), outpacing Airbnb’s 8% growth

Connected trip transactions rose 35% but still represent a high-single-digit share

Management highlighted ongoing AI initiatives aimed at improving the user experience and mentioned collaborations with OpenAI, Microsoft, and Amazon to advance agentic AI aligned with the connected trip vision.

Looking ahead, Q2 guidance is 11% growth in both bookings and revenue (midpoint). While management flagged macro and geopolitical uncertainty, leisure travel demand remains resilient.

Booking also continues to return capital, generating $3.2B in FCF (+21% YoY), paying $319M in dividends, and repurchasing $1.8B in stock, with $25.9B remaining under its buyback program. Overall, a strong quarter with meaningful KPI improvements, reinforcing our confidence in Booking’s long-term success.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

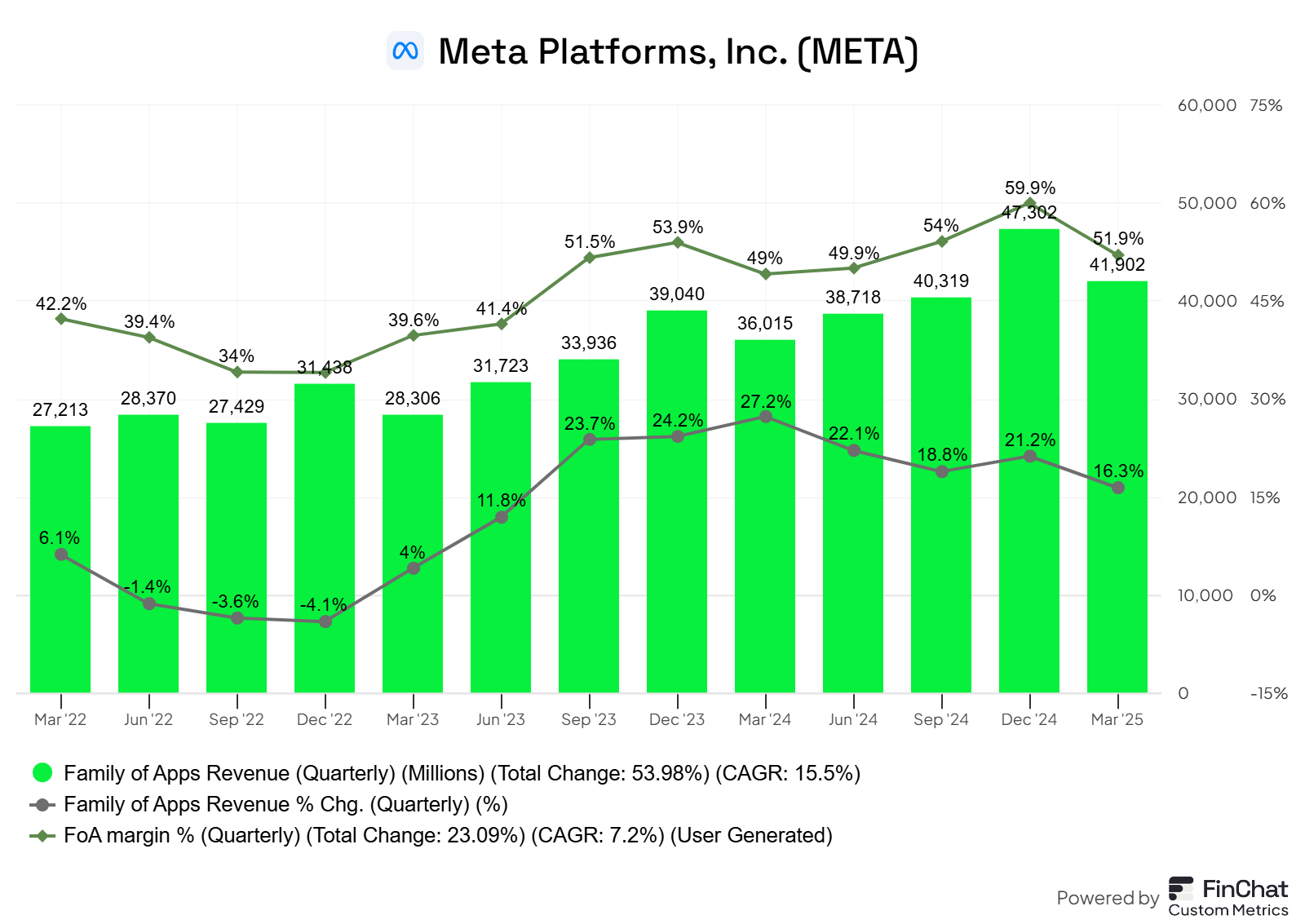

Meta Q1’25

Meta reported a strong Q1, with DAP up 6% YoY to 3.43 billion. Total revenue grew 16% YoY (19% in constant currency) to $42.3 billion, beating the $41.4 billion consensus by 2.3%. Family of Apps (FoA) revenue rose 16.3% to $41.9 billion, while Reality Labs (RL) revenue fell 6% to $412 million due to lower Quest sales, partially offset by growing Ray-Ban Meta smart glasses adoption, now with 4x as many monthly actives YoY.

Operating income rose 27% YoY to $17.6 billion, with margins expanding from 38% to 41%. FoA contributed $21.8 billion in operating profit, while RL posted a $4.2 billion loss. Net income surged 35% to $16.6 billion, with EPS of $6.43 (+37% YoY), beating consensus by 23.5%.

Free cash flow came in at $10.3 billion (24% margin), down from $12.5 billion last year due to heavy AI-driven capex, which rose to $13.7 billion including leases (vs. $6.7B in Q1’24). Given the commitment to invest in the AI era, Capex guidance was raised to $64–$72 billion (from $60–$65 billion) to support accelerated AI infrastructure, while opex guidance was lowered by $1 billion.

Engagement saw notable gains, especially in video, driven by AI-powered recommendations as time spent rose 7% on Facebook, 6% on Instagram, and 35% on Threads.

Threads reached 350 million MAUs, up from 320 million last quarter.

Meta continues its monetization efforts via AI tools like GEM (twice as efficient at improving ad performance), boosting Facebook Reels conversions by 5% in testing. Ads are also expanding to Threads across 30+ markets, though the platform isn't yet a major revenue driver. WhatsApp saw the strongest Meta AI usage which approached 1 billion MAUs while “Other” revenue within FoA rose 34% to $510 million, fueled by WhatsApp business messaging and Meta Verified.

Q2 revenue guidance is $42.5–$45.5 billion, implying ~12% YoY growth at the midpoint.

A potential headwind is the European Commission’s decision concluding that Meta’s "Subscription for No Ads" model is not compliant under the Digital Markets Act. Europe accounts for ~23% of sales, and while Meta plans to appeal, regulatory risk remains. Meta’s execution has been remarkable, and while the ROI on its aggressive AI capex remains a risk, Zuckerberg has consistently delivered.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

That’s a wrap! If you enjoyed this, why not take advantage of our 2-day free trial to see if our full offering aligns with what you're looking for?