Estée Lauder’s Turnaround: Can “Beauty Reimagined” Restore Growth?

Weak Outlook, Cost Cuts, and Strategic Shifts

Estee Lauder reported Q2’25 earnings on Tuesday 4th, with the newly appointed CEO Stéphane de La Faveri announcing a new executive team and a new strategic vision “Beauty Reimagined”, aimed at reigniting revenue growth and restoring operating margins.

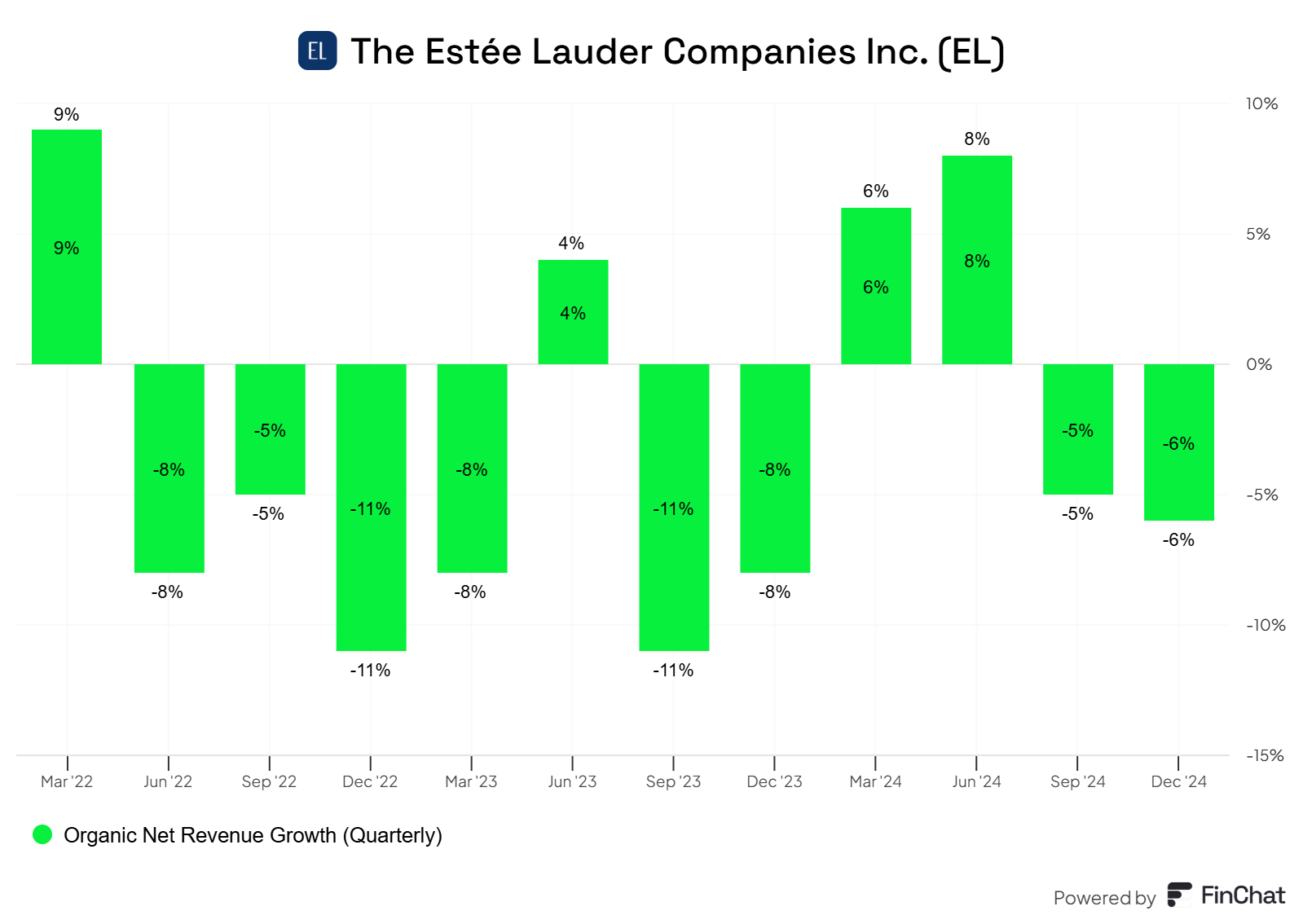

Despite the announcement, the stock tumbled 20% following the release, as investors reacted negatively to the company’s weak Q3 guidance. Management projected organic sales growth of -9% at the midpoint for Q3’25, a further decline from the -6% recorded in Q2’25. The softer outlook was attributed to continued weakness in Asian travel retail.

While the sharp decline may seem excessive at first glance, it’s worth noting that the stock had already climbed 20% from October 31 to February 3, driven primarily by optimism surrounding the new CEO’s appointment and sequential improvements in China for certain peers, rather than any significant fundamental changes.

Article contents:

Financial results

Outlook

Profit Recovery and Growth Plan

Beauty Re-imagined

Conclusion

1. Financial Results

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

a. Revenue

Estée Lauder reported Q2 revenue of $4 billion, reflecting a 6% decline in both total and organic sales. This was at the lower end of the company’s guidance range (-6% to -8%) provided in October. However, it marked a deterioration from the -5% organic sales decline in the prior quarter. The decline was primarily driven by continued weakness in travel retail, which saw double-digit declines, and a challenging environment in Asia Pacific, particularly in Mainland China, Korea, and Hong Kong SAR, where consumer sentiment remains low.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

On a positive note, gross margin improved by 310 basis points (bps) year-over-year to 76.1%, benefiting from Estée Lauder’s Profit Recovery and Growth Plan (PRGP) announced in November 2023. The improvement was driven by reduced inventory write-downs, lower discounting, and strategic pricing actions. However, this also highlights the root cause of the previous margin decline, excess inventory buildup in FY22 and FY23, particularly in travel retail, which ultimately led to inventory write-offs and discounting to normalize stock levels.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

b. Operating Income

Adjusted operating income declined 20% year-over-year to $462 million, resulting in an adjusted operating margin of 11.5%, down from 13.5% in the prior year. The 200-bps deterioration was mainly due to sales deleverage and increased investments in consumer-facing activities, partially offset by gross margin improvements and PRGP cost savings.

On a GAAP basis, Estée Lauder reported an operating loss of $580 million, compared to a $574 million profit in the prior year. The losses were primarily driven by $861 million in goodwill and intangible asset impairments, including $773 million from Tom Ford and $88 million from Too Faced, along with $181 million in restructuring and other charges. This suggests that the new management team chose to take the hit upfront rather than delaying it, a move that shields them from blame for past leadership decisions.

Estée Lauder’s largest acquisition, Tom Ford ($2.6 billion, FY23), has now seen $773 million (nearly one-third of the purchase price) written off within just two years. Similarly, Too Faced ($1.45 billion, acquired in 2016) has recorded over $1 billion in impairments since 2020. Dr. Jart+, valued at $1.7 billion at the time of its full acquisition in 2019, has also seen $510 million in write-offs since FY22. This highlights a poor track record in M&A.

c. Performance by region

Source: Estee Lauder Earnings Releases, StockOpine Analysis

Asia Pacific

Asia Pacific was the weakest-performing region, with revenue declining 11%, driven by double-digit declines in Mainland China, Korea, and Hong Kong SAR, due to lower consumer demand. Performance in Korea was further impacted by Dr. Jart+ exiting the travel retail channel.

On a more positive note, Japan posted double-digit organic growth, with both travel and domestic demand remaining strong. In Mainland China, Estée Lauder, La Mer, and Le Labo saw market share gains in makeup, skin care, and fragrance, respectively. Additionally, The Ordinary is set to debut in Mainland China this month, and management continues to expand the company’s presence on high-growth platforms like TikTok Shop, LINE, and Shopee.

EMEA (Europe, Middle East & Africa)

EMEA’s organic sales declined by 5%, reflecting continued weakness in the Asia travel retail business, where lower replenishment orders hurt performance. Travel retail sales declined by double digits, impacted by a challenging retail environment and subdued Chinese consumer sentiment.

As previously noted, Estée Lauder’s high exposure to travel retail has been a key factor behind its underperformance in recent years. The segment accounted for 27% of FY22 sales, but its contribution declined to 19% in FY24 and is expected to further deteriorate in FY25. Management emphasized efforts to reduce the company’s reliance on travel retail, with CEO Stéphane de La Faverie stating:

“Travel retail remains an important part of the business. But it is very clear that we are reducing overall the dependency on travel retail and reducing the volatility of our overall business. That being said, I want to just be clear, travel retail is an important channel for us to recruit and retain consumer. And in many instances, as certainly you've seen, it is a window of creating brand desirability for our brand around the world.” Stephane de la Faverie