Evolution AB Q2’24 Earnings

In December 2023, we revisited Evolution AB in our article "Evolution AB: Challenges, Regulations, and Market Dynamics." Since then, the company's stock price has continued to decline, with an additional 8.3% drop following its earnings report on July 19, 2024. The report showed a miss on analyst expectations, with revenues falling short by 2.3% and operating profit by 4.5%. This resulted in the lowest quarterly operating margin (61.2%) seen in the past few years, marking the first time it has dropped below 62% after Q4’22.

In this update, we'll review the results, discuss any significant changes, and provide an updated valuation.

Join us today with a 25% discount for 1 year (applies to the annual plan only).

1. Results Overview

Source: Koyfin (affiliate link with a 15% discount for StockOpine readers)

a. Performance

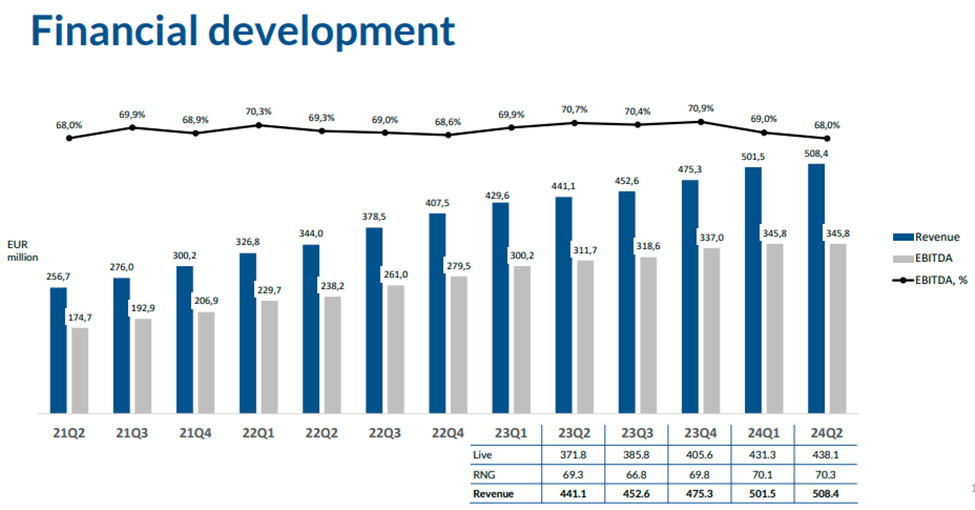

Revenues of €508.4M, increased by 15.3% (17.8% for Live Casino and 1.5% for RNG).

RNG increased by 1.5%, the highest in the last 4 quarters, while releasing 26 games. However, it disclosed losing market share in the US RNG offering and admitted that they could do more.

Revenues were impacted by a large payout to players of about €35m, affecting EVO’s revenue share and FX rates. Growth was 19% in constant FX rates, meaning it would have beaten consensus.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers), StockOpine Analysis

EBITDA of €345.8M, increased by 10.9% - EBITDA margin of 68% Vs 70.7% in Q2’23.

Operating Profit of €311.1M, increased by 10.5% - Operating margin of 61.2% Vs 63.8% in Q2’23.

Profit for the period of €269.1M, increased by 1.9% - Profit margin of 52.9% Vs 59.9% in Q2’23.

Source: Evolution, Q2’24 presentation

It’s worth noting that profitability is affected by a slower growth rate and investments in personnel, which were deemed necessary three quarters ago when the company was facing supply chain constraints. Punishing the company for investing in its long-term growth is unfair and unreasonable.

Headcount over the past three quarters increased year-over-year by 13%, 18.5%, and 21.2% in Q4’23, Q1’24, and Q2’24, respectively, reaching 21,141. This acceleration in the number of employees caused a 27.3% increase in personnel costs, justifying the drop in margins. According to the 2023 annual report, the largest increases in average employees in absolute terms were in the USA and Spain, driving cost per employee higher. Additionally, most of these employees were added in Q4 2023 (about 1,398 vs. 797 in Q1-Q3’23 combined), making their impact on payroll more pronounced in 2024. As long as the company continues to invest and hire more employees to support its studio growth, we remain positive about its prospects. The right balance will eventually be achieved.

“I would like to remind all of you that expansion and recruitment comes together with cost and time-wise costs before revenues. We continue to make great progress in our studio development and all according to plan.” Martin Carlesund CEO

Source: Evolution, Q2’24 presentation

Moving to profit for the period, the margin decline was more pronounced than operating profitability, as the effective tax rate stood at 15.3% compared to 6.7% in Q2’23. This was due to the Pillar 2 regime that came into effect in 2024. In our December valuation, we applied a 16% tax rate for 2024, so this is in line with our expectations.

b. Balance sheet

Cashflow from operating activities of €312.8M (Vs €233.8M in Q2’23) – Margin of 61.5% (53%).

Free cash flow of €280.2M (Vs €223.2M) – Margin of 55.1% (50.6%).

Strong balance sheet with Cash and Cash equivalents of €689M compared to lease liabilities of €79.1M (nil debt).

c. Outlook

Maintains full year EBITDA guidance of 69% to 71%, implying that next two quarters should be at least 69.5% on average. Considering that Evolution is coming out of its accelerated expansion phase, this is not unachievable.

Evolution will open a new studio in the Czech Republic in August, marking its entry into a new regulated market.

To initiate two new studios in the year.

d. Capital Allocation (as announced on 18th of July 2024)

The minimum dividend policy of 50% of net profits remains intact.

Ad-hoc M&A based on opportunities with long-term enhancing financial terms.

Distribution of excess cash (after business investments and dividends) mainly through share buybacks. €400 million (or about 2% of outstanding shares) was approved until the next 2025 AGM. Buybacks are beneficial at the right price, and today’s price seems attractive. Since the announcement, the company has been acquiring about 70k shares per day.

CAPEX: As seen from the chart below, CAPEX was accelerated over the last 3 quarters, aligning with the expectation that supply chain issues should be overcome. The company has invested in new studios and expanded existing ones (tangibles) as well as into games (intangibles). The target of €120m for the year is more than halfway there with €68m already invested.

Source: Evolution, Q2’24 presentation

e. Regional

Although Asia, which remains its largest segment (39.5%, surpassing Europe at 37.6% in Q1'24), grew by 22% year-on-year, it only added $3.1 million sequentially in absolute terms (whereas in Q2’23 it added $10.5 million sequentially).

This resulted in a total sequential growth of $6.9 million ($6.8 million from Live). Looking back to Q1'20, we couldn't find any quarter where Evolution added less than $10 million in total in a subsequent quarter. This was the disappointing finding from the quarter, though it's worth noting that in the previous quarter $26 million were added.

The highlight of the quarter was Latam, which added $3.6 million (a year-on-year growth of 16.9%, despite Brazil being in the waiting room for regulation) and North America, which saw year-on-year growth of just 8.5% but a sequential revenue decline of $1.9 million. The weakness in North America was in RNG, while Live grew in line with the market.

Europe grew by 9.2%, and with increased studio capacity (a weakness identified in our latest article), management expects further growth in the future.

Source: Evolution January-June report 2024

f. Other highlights

Evolution launched live games in Delaware at the beginning of July, following the March 2024 launch of online slots with Rush Street Interactive, making it its sixth US state. In June, it announced that Crazy Time was made available to players in Pennsylvania and West Virginia after its launch in December 2023 in New Jersey. Crazy Time was also voted the best new game under the EGR North America 2024 awards.

“The reception from players in New Jersey has been fantastic, and Crazy Time is now one of our most popular live dealer games in the state. We’re incredibly excited to bring the unique Crazy Time online entertainment experience to players in Pennsylvania and West Virginia, with more US states set to join in the fun soon.” Jacob Claesson, Evolution CEO North America

This gives us confidence that North America sales could reaccelerate.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers)

The launch of Lightning Storm after the reporting period generated significant excitement from management. Although the number of players spiked at launch, it appears it hasn't matched the success of Funky Time last year. However, more time is needed to assess its performance fully.

Source: iGaming Tracker Limited, Live Casino Player Numbers - Hourly Chart (igamingtracker.com)

Evolution has agreed to acquire Galaxy Gaming, a developer and distributor of innovative casino table games. This announcement was made a day before the earnings report. The acquisition will enhance Evolution's portfolio and talent pool, particularly in North America, where growth is still in its early stages. Galaxy Gaming holds 131 licenses worldwide, including 28 in US states (out of a possible 29), which will further strengthen Evolution’s relationships with US regulators. The acquisition is priced at $85 million, or $124 million including debt. This results in Next Twelve Months EV/Sales and EV/Adjusted EBITDA multiples of approximately 4.2x and 9.9x, respectively, which seem reasonable. The Trailing Twelve Months EV/EBITDA multiple is around 13x, significantly lower than previous acquisitions like NetEnt, which had a multiple of 28.4x, indicating improved capital allocation discipline. For those interested in merger arbitrage, Galaxy Gaming is currently trading at $2.77 per share, compared to the agreed acquisition price of $3.20 per share, offering a potential upside of approximately 15.5% over one year, though this comes with the risk of the deal not closing.

2. Updated Valuation

Do you want to unlock the valuation part? Join us today with a 25% discount for 1 year (applies to the annual plan only).