Evolution reported its Q3 2025 earnings, and has underdelivered, particularly in Asia, where cyberattacks affected growth and led to the company’s first year-over-year total revenue decline. On a positive note, Europe showed signs of stabilization, and the EBITDA margin came in at 66.4%, above the previous two quarters and within the full-year target range of 66%–68%.

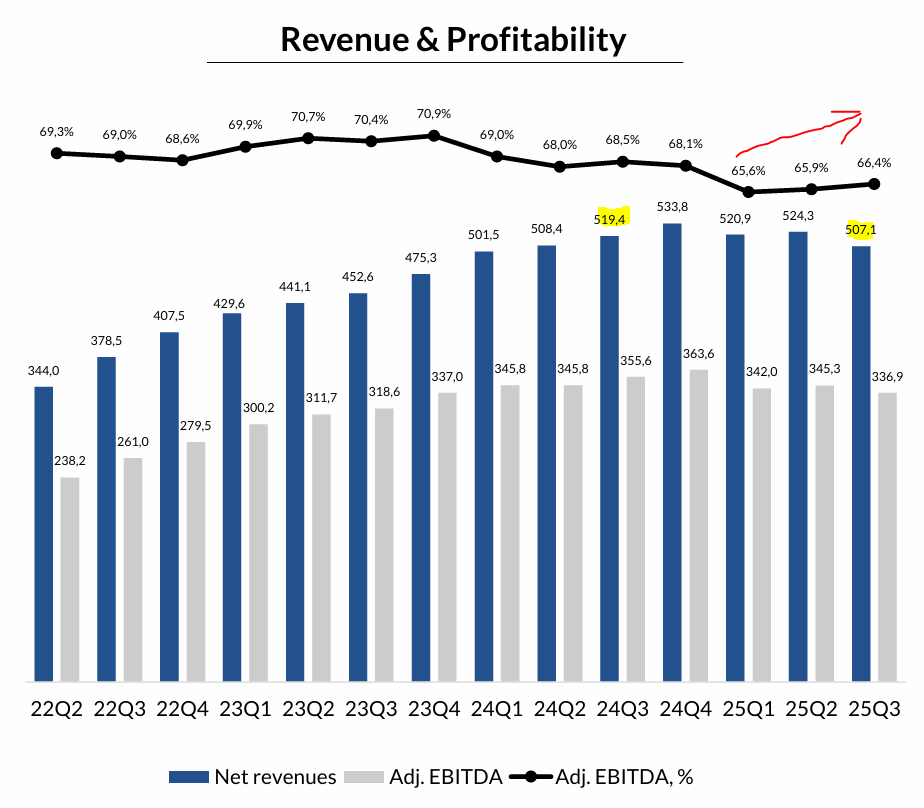

Revenue reached €507.1 million, down 2.4% year-over-year and below expectations of €535 million. EPS also missed estimates at €1.25 versus €1.33 consensus, representing a 20% YoY decline.

The market reacted negatively, with the stock down around 8%. We therefore need to take a closer look to determine whether this sell-off is justified.

1. Performance overview

Revenue at €507 million declined 2.4% YoY, but on a constant currency basis, it grew by 3.9%. Still, this is a deceleration from the prior quarter’s 8.8% cc growth.

EBITDA was €336.9 million, resulting in an EBITDA margin of 66.4%, a 0.5% improvement from the prior quarter, but a 2.1% decline from the prior year. Nevertheless, it reflects healthy sequential growth.

Source: Evolution AB Investor Presentation Q3’25

Operating expenses grew 5.3% YoY, a notable improvement from the 10% YoY growth in the prior quarter, with personnel costs linked to new table launches and general studio expansion being the primary driver (+6.3% YoY). Personnel costs were down 4.9% QoQ, mainly due to a reduction in the number of FTE (end-of-period full-time employees equivalent fell from 16,311 to 16,094), reflecting also the shift in the resource mix.

“When it comes to cost per employee and the cost base, we have talked about all since actually July 2024, where we have the strike in Georgia in that situation and the cost mix and we had to shift a little bit. So we had an unfavorable cost mix. Now we’re starting to be able to shift that, which is what we have talked about during the quarters that we need to have a better and favorable cost mix. It’s not like we’re cutting delivery right now. It’s -- we are putting the delivery in the studios, which are good.” Martin Carlesund CEO

Source: Evolution AB Investor Presentation Q3’25

Management is already implementing broad cost-cutting measures, which are expected to continue into 2026 and help improve margins.

2. Segment Breakdown

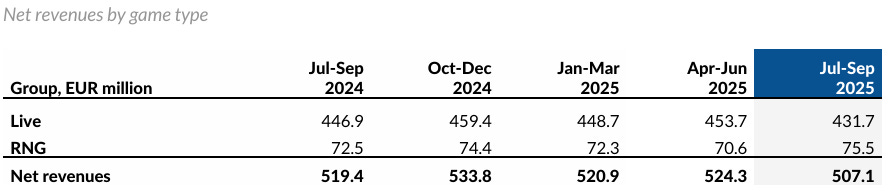

The Live segment generated €431.7 million in revenue, down 3.4% YoY and 4.8% QoQ. This marks the first ever YoY decline, with Asia being the main drag, as we will review shortly. During the quarter, the segment also released the Ice Fishing game show, offering a faster-paced experience that has received positive initial feedback.

On a positive note, the RNG segment delivered €75.5 million in revenue, up 4.1% YoY and 6.9% QoQ, setting a record quarterly revenue. This improvement was driven by Nolimit City slots. Additionally, the company launched a new RNG brand, Sneaky Slots, created from scratch. According to management, this brand addresses a clear market gap with titles that are bold, characterful, and engaging.

Source: Evolution AB Investor Presentation Q3’25

3. Regional performance

Europe

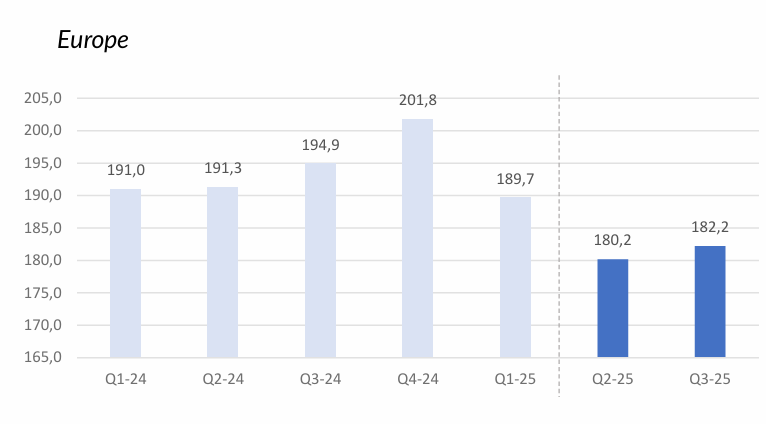

Revenue in Europe was €182.2 million, reflecting a 6.5% YoY decline but a 1.1% QoQ increase. Q2’25 marked the first quarter with the full ring-fencing impact, and the QoQ improvement in Q3 is a promising sign of stabilization in Evolution’s largest regulated market.

The expectation that no further measures are foreseeable in the near term also supports confidence in future growth, which could gradually return to its historic 9–10% range.

“Worth mentioning is also that we got recognition for our ring fencing from one of the largest regulators in Europe, where we were pointed out as one of the best B2B suppliers. I’m happy with the progress in Europe in this quarter.” Martin Carlesund CEO

Meanwhile, dialogue with the UK Gambling Commission is ongoing, but the CEO remains confident about the potential outcome, which can be another vote of confidence following the Black Cube legal case, in which Playtech was found to have funded the initiation of the report back in 2021:

“We still have to wait for the outcome, but I truly believe that we have the most sophisticated compliance framework among all providers targeting the U.K.”

Source: Evolution AB Investor Presentation Q3’25

Asia – The Terrible News

Cybercrime has been a drag on the region for a while, however, in the prior quarter it reached a record revenue of €209.1 million, with the company stating it was now in a much better position to combat these issues. Three months later, the situation worsened. Revenue came in at €189.1 million, marking the first-ever YoY decline (-6.5%) and a 9.6% QoQ drop.

Management attributed this weakness to two main factors:

Overextended countermeasures against cybercrime.

A volatile regulatory environment.

Let’s assess these in more detail.