In this week’s write-up, we are revisiting FactSet, a leader in the financial data and analytics industry. We will assess FactSet’s performance over the past year, cover recent developments, compare its performance to industry peers, and conclude with a valuation update. For those interested in a deeper dive, we covered FactSet in June 2023; here is the link to our comprehensive report.

Brief Overview:

FactSet Overview: FactSet is a leading data and analytics company serving the financial services industry. The company provides financial data and applications that enable investment professionals to research investment ideas, analyze, monitor, and manage their portfolios. Over its 40-year history, FactSet has built an extensive data network. With 95% of the company’s revenue being subscription-based, FactSet’s annual subscription value (ASV) plus professional services reached $2.2 billion as of Q3'24. Over the past decade, FactSet has steadily grown its revenues and operating income at a CAGR of 9.2%.

Key Investment thesis: FactSet’s diverse market offerings, high client retention, affordability relative to leading peers, and extensive data and content provider network make it a compelling long-term investment opportunity.

Source: Koyfin (affiliate link with a 20% discount; if you are a paid subscriber, you can benefit from a 3-month free trial)

Contents:

Performance Update

Industry

Valuation

Conclusion

1. Performance Update

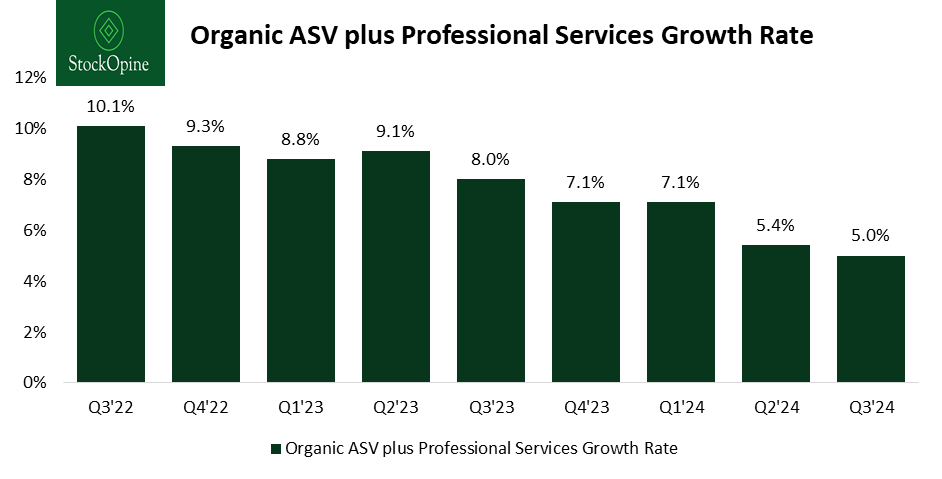

a. Deceleration of ASV growth

The current year has not been a great one for FactSet’s topline growth. Annual organic ASV growth decelerated from 7.1% in FY23 to 5% as of Q3'24, falling behind management’s FY25 mid-term target of 8%-9% annually. Additionally, FactSet revised its ASV organic growth guidance for FY24 from 7% at the start of the year to 4.8%.

Source: FinChat.io (affiliate link with a 15% discount for StockOpine readers), StockOpine Analysis

Similarly, revenue growth decelerated from 7.3% in Q4’23 to 4.3% in Q3’24, leading analysts to revise their sales forecasts downward. This resulted in a flat share price over the past year, despite it reaching about $490 before coming back to prior year levels.

Source: Koyfin (affiliate link with a 20% discount; if you are a paid subscriber, you can benefit from a 3-month free trial)

The main macro risk we highlighted in last year’s report materialized. Low capital market activity and a high-interest rate environment led to prolonged sales cycles, reductions in client headcount, and tighter client budgets, negatively affecting revenue growth. These cyclical headwinds impacted not only FactSet but other industry players as well, confirming that this is a sector-wide issue rather than company-specific. For example, S&P Global also experienced longer sales cycles and effects from banking consolidation.

The banking sector, in particular, experienced significant headcount reductions, eroding demand. According to the Financial Times, global banks cut more than 60,000 jobs during 2023 due to lower capital markets activity and deal-making, marking one of the worst years since the financial crisis, with this trend expected to continue in 2024. For example, at the start of 2024, Citigroup said it would cut 20,000 jobs over the next two years. According to Goldman Sachs’ quarterly filings, its workforce was reduced by 2.2% from Q1’23 to Q1’24, reflecting 1,000 job cuts. Similarly, Bank of America headcount was reduced by 5,000 or 2.3% from Q1’23 to Q1’24.

Additionally, institutional buy-side firms are implementing cost cuts and headcount reductions, decelerating workstation sales. These firms also face fee pressure from the rise of passive funds, now surpassing active funds in assets under management—another risk noted in our report.