Fortinet Q2'25: Strong Execution Meets Market Doubts

Billings Beat and Raised Guidance Obscured by Market Concerns

In a market where any perceived weakness is punished, understanding the nuances behind the numbers is critical. In our view, Fortinet’s results present a case of the market focusing on a single perceived negative while overlooking a number of positive indicators.

Fortinet beat headline estimates, posted its strongest service billings growth in six quarters, and raised its full-year billings outlook. However, a guidance mix-shift seems to have worried investors. This reaction is short-sighted ignoring the company's execution and competitive position.

We covered Fortinet in depth in April, so if you’d like to better understand its business model before diving into this earnings review, you can read it here.

Now, back to the earnings review. At the end of this report, we also recap what this means for our portfolio, as we mentioned in yesterday’s chat.

1. The Numbers: A Beat Driven by Enterprise Strength

Fortinet's Q2 results surpassed expectations across the board.

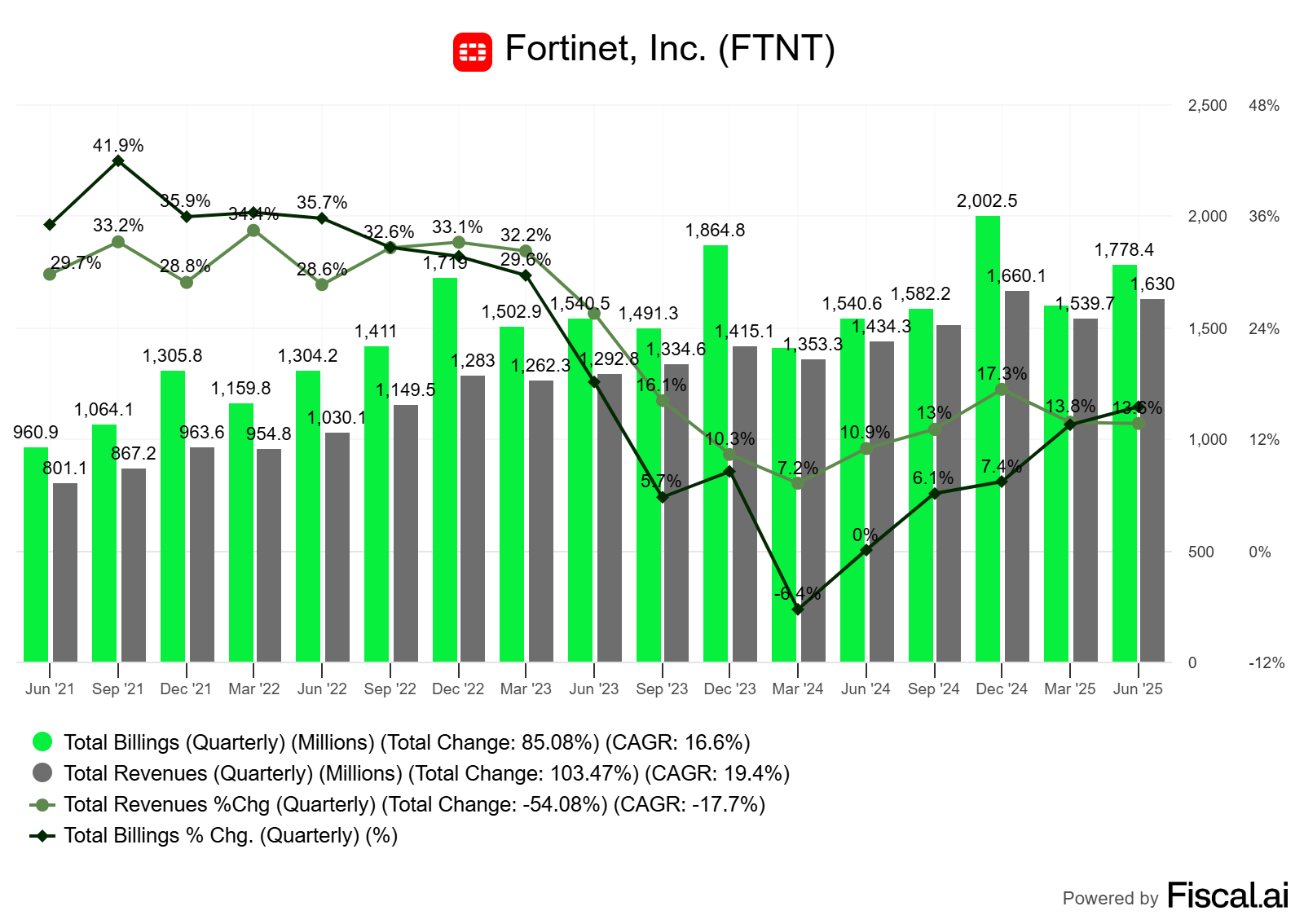

Revenue: Came in at $1.63 billion, representing 14% year-over-year growth and beating both estimates ($1.625b) and the company's own guidance (of 12.9%). This growth was fueled by the rising global demand for their integrated solutions. Geographically, performance was led by EMEA with 18% growth, while the Americas and APAC both grew a solid 11%.

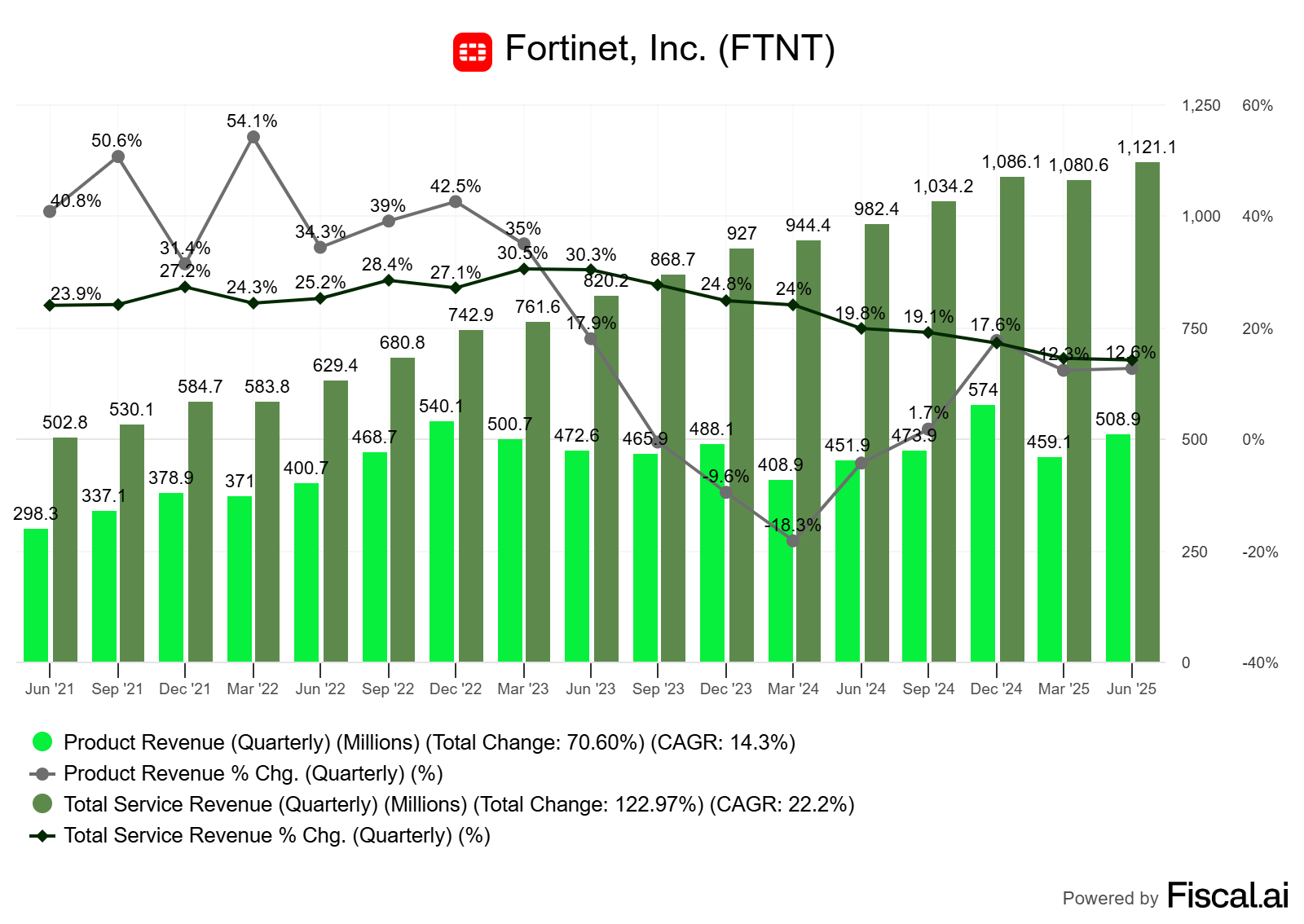

Product Revenue: Grew 13% year-over-year to $509 million. This growth was driven by the ongoing firewall upgrade cycle and strong performance in Operational Technology (OT) security.

Service Revenue: Grew 14% year-over-year to $1.121 billion. Security subscriptions, grew 15%, and support and related services, grew 13%.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Billings: Reached $1.78 billion, up 15% YoY, ahead of the consensus $1.722 billion. This strength was broad, but management called out that “among our top 5 verticals, financial services, the vertical with arguably the most sophisticated and discerning security purchasers led the way with billings growth of over 30%.” A critical data point, which the market seems to have ignored, is that Service billings grew by 17%, the highest growth rate in the past 6 quarters.

Customer and Deal Momentum: Fortinet saw tremendous success moving upmarket, with the total dollar value of deals greater than $1 million increasing by a remarkable 51% YoY. At the same time, Fortinet continued to expand its broad customer base, adding over 6,900 new organizations in the quarter (up from 6,300 in Q1’25), showing continued momentum in the SMB space.

EPS: Non-GAAP EPS was $0.64, a 13% increase from the prior year and well above the consensus estimate of $0.59.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Gross Margin remained strong in Q2 at 81.6% compared to 81.5% in Q2’24. Product gross margin expanded significantly to 67.8% (from 66%) as one-time inventory charges normalized, while Service gross margin dipped slightly from 88.6% in Q2’24 to 87.8% due to strategic investments in cloud capacity.

Operating Margin of 33.1% for Q2 beat guidance mid-point of 32% but was below Q2’24 margin of 35.1%. The year-over-year decline was expected and as explained by management is a result of planned investments in sales headcount, costs from recent acquisitions, and foreign exchange headwinds.

Shareholder Returns: In Q2, Fortinet repurchased 4.6 million shares for a total cost of $401 million. Approximately $1.6 billion remains under the current share buyback authorization.

Free Cash Flow for the quarter was $284.1 million , a decrease from $318.9 million in the prior-year period. This decline reflects the planned increase in infrastructure investments to support the expansion of hosted security solutions. Capex in Q2’25 was $167.8 million compared to $23.1 million in Q2’24.

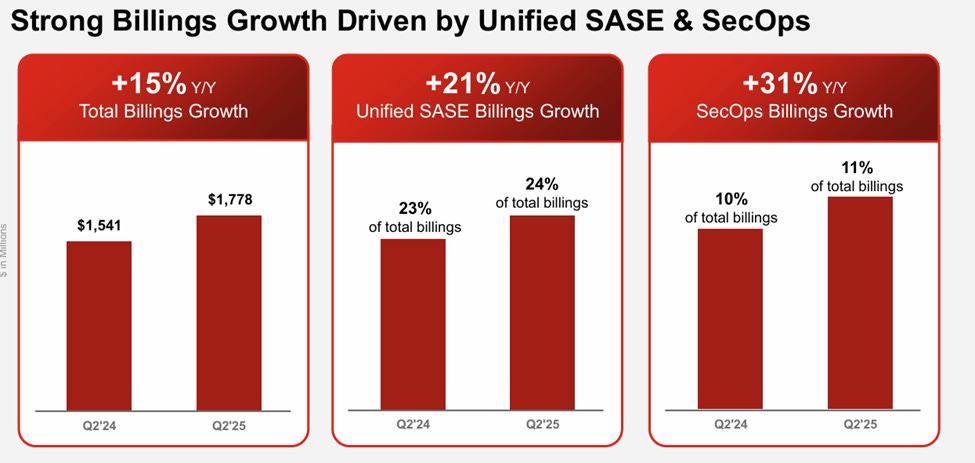

2. The Growth Engines: SASE and SecOps

Unified SASE and Security Operations (SecOps) now represent a combined 35% of total billings, up from 33% in the prior year.

Source: Fortinet Q2’25 earnings presentation

SecOps was the star performer as it showed accelerating momentum across the board.