Fortinet Q3'25: Record Profits & AI Wins, But Outlook Fears Spook the Market

A beat-and-raise quarter gets punished as investors fixate on SASE ARR

Fortinet delivered a strong Q3, beating estimates across the board, posting record-high operating margins, and most importantly raising its full-year guidance for billings, operating margin, and EPS. However, the continued deceleration in service revenue, coupled with reduced 2025 guidance for that segment and an expected slowdown in Q4 sales growth, worried investors.

If you need a refresher on the business model, our previous deep dive is available here:.

1. The Numbers: A Beat Driven by Record Profitability

Fortinet’s Q3 results surpassed expectations, with operational efficiency being the standout story.

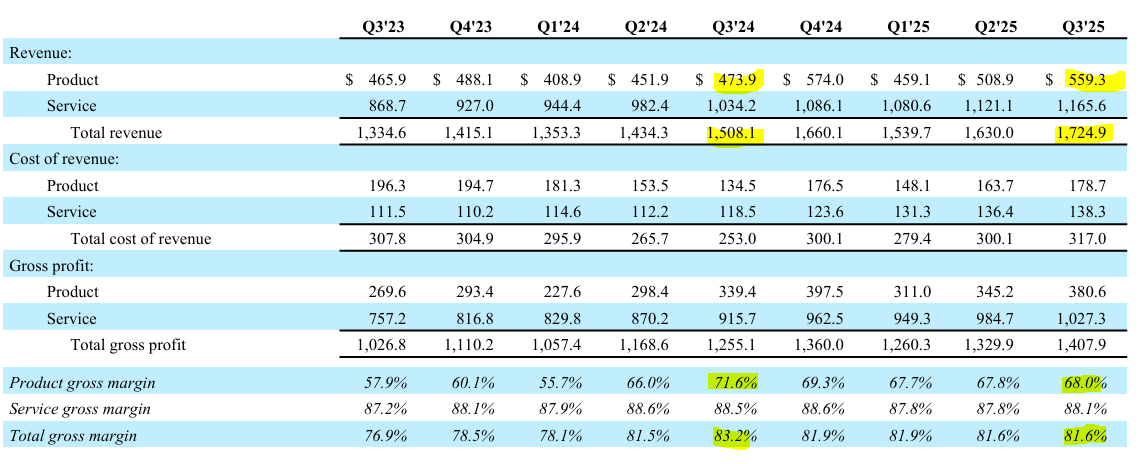

Revenue: Came in at $1.72 billion , representing 14% year-over-year growth and beating the company’s own Q2 guidance (midpoint of $1.7B). Growth was led by EMEA (19% growth) and APAC (16% growth).

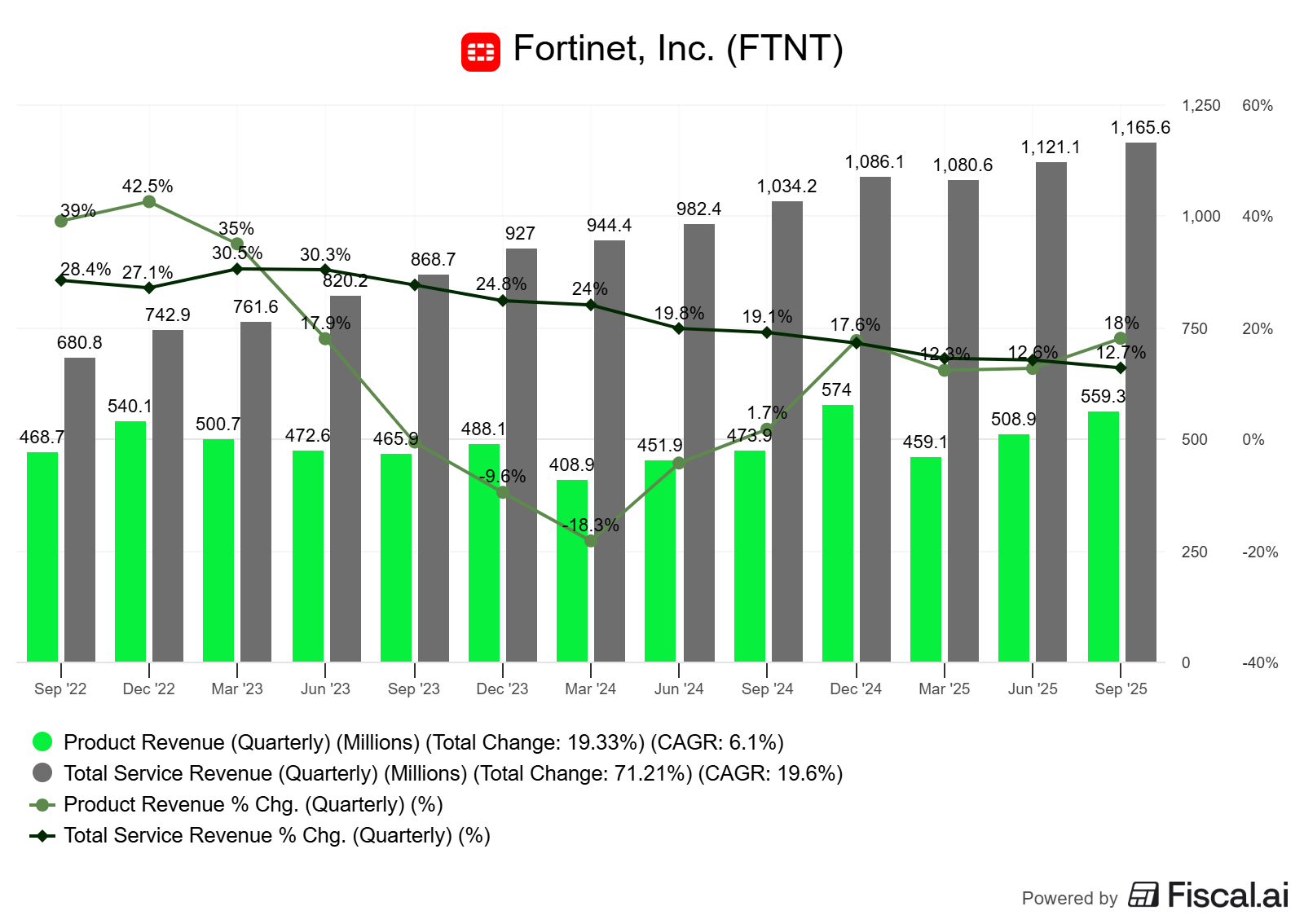

Product Revenue: Grew 18% year-over-year to $559 million, a significant beat. This growth was driven by strong performance in multi-product deals and OT security. As per management, the 2026 end-of-support cohort was not a significant driver of product revenue growth in the third quarter but was rather driven by upgrades and expansion across products.

Service Revenue: Grew 13% year-over-year to $1.17 billion. This was the 9th consecutive quarter of decelerating growth but the product revenue growth acts as a leading indicator of future service growth. Service growth is expected to improve in the 2nd half of 2026.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

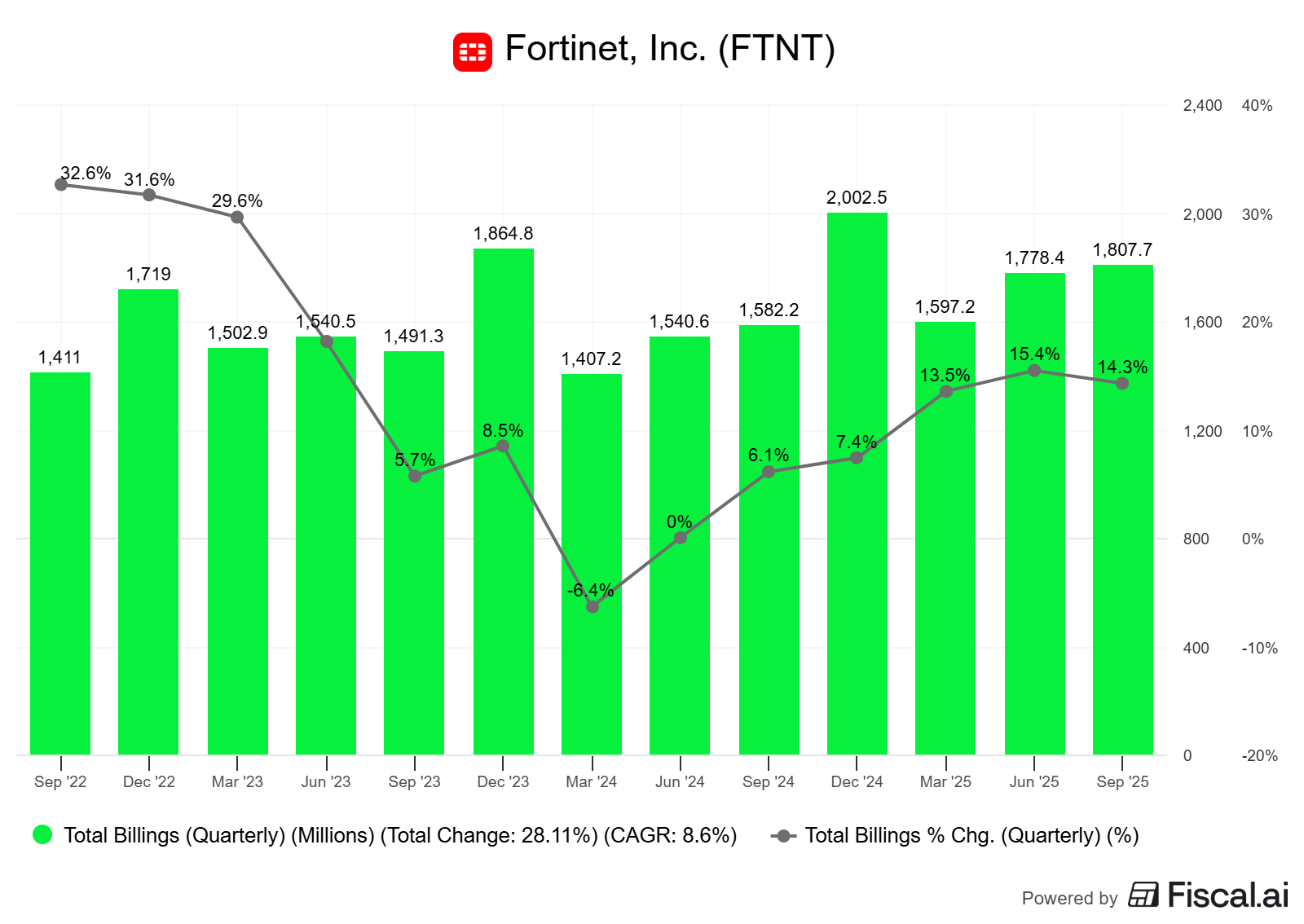

Billings: Reached $1.81 billion, up 14% YoY, beating the Q2 guidance midpoint of $1.8B.

Customer and Deal Momentum: Fortinet continues to win large deals. The total dollar value of deals greater than $1 million increased 32% YoY (51% in Q2’25). The company also added approximately 6,600 new customers in the quarter (Vs 6,900 in Q2’25).

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

EPS: Non-GAAP EPS was $0.74, a 17% increase from the prior year and well above the consensus estimate and guidance (midpoint $0.63).

Gross Margin: Non-GAAP Gross Margin was 81.6%. While strong, this was down from 83.2% in Q3’24 , reflecting a lower product gross margin (68% in Q3’25 vs 71.6% in Q3’24) and a mix shift towards product revenue (32% in Q3’25 vs 31% in Q3’24). That said, margin was significantly higher than the guidance of 80.5% due to improved cost control.

Source: Fortinet Q3’25 supplementary data

Operating Margin: Non-GAAP Operating Margin hit 36.9% , a third-quarter record and up 80 basis points from last year. This was driven by operational efficiencies and strong cost management.

Shareholder Returns: In Q3, Fortinet executed a massive repurchase, buying back 23.3 million shares for a total cost of $1.83 billion or 3% of total shares!! Approximately $796 million remains under the current share buyback authorization.

Free Cash Flow: Adjusted Free Cash Flow was $646 million, for a 37% margin. This was up from $605 million last year, even after accounting for a $51 million increase in infrastructure investments.