Grab Holdings: The Profitability Inflection Point

Dominant, growing, and finally profitable. Is it time to buy?

It’s been a while since our last deep dive as we spent the past few weeks focused on valuation updates and the holiday period slowed longer-form work. We’re starting the year with Grab, Southeast Asia’s leading on-demand platform spanning mobility, delivery, advertising, and financial services. This report looks at how the business is evolving as it moves from scale to profitability. We’re confident this one was worth the wait and wish everyone a strong investing year ahead.

Contents:

Key Facts

Business Overview

Management & Ownership

Industry Overview

Financial Analysis

Competitive Advantages, Opportunities and Risks

Valuation

Conclusion

1. Key Facts

Description: Grab Holdings is the leading Superapp in Southeast Asia, providing a suite of everyday services including Ride-Hailing (Mobility), Food & Grocery Delivery (Deliveries), and Financial Services (Payments, Lending, Digital Banking). It operates across 8 countries, including Malaysia, Indonesia, Vietnam, Singapore, and Thailand.

Key Financials: Grab made its IPO on the Nasdaq in late 2021. From FY20 to trailing twelve months (TTM) ended Q3’25, Grab achieved a revenue Compound Annual Growth Rate (CAGR) of 50%, generating TTM revenue of $3.2 billion. Grab has reached a profitability inflection point after years of investment. Over the same period, the Company improved its operating income from a loss of $1.3 billion to a profit of $26 million. Grab has cash and short-term investments of $7.1 billion and total debt of $2.1 billion.

Price & Market Cap (as of 2 January 2026): Its market cap is $21 billion with a 52-week low of $3.36 and a 52-week high of $6.62, whereas it currently trades at $5.08.

Valuation: Grab trades at a LTM EV/Sales of 5x (4 Year average of 9x).

2. Business Overview

a. Fixing a Broken Industry

Grab traces its roots to 2011, originating from a business plan devised by Harvard Business School classmates Anthony Tan and Tan Hooi Ling. Their objective was to revolutionize the Malaysian taxi industry by using technology to solve deep-seated issues of safety, reliability, and efficiency. At the time, the market was plagued by overcharging, frequent ride refusals, and significant safety risks, particularly for women. With their vision to connect passengers to licensed drivers validated by a runner-up finish and a $25,000 grant at the 2011 HBS New Venture Competition, the groundwork for Grab was officially established.

b. Boots on the Ground

The app officially launched in June 2012 in Kuala Lumpur under the name MyTeksi. The launch was initially financed through personal funds. Despite his family’s significant wealth, Anthony Tan’s father rejected the concept, urging him to remain in the traditional family business. Undeterred, Anthony funded the initial operations using the $25,000 prize money from Harvard and his personal savings, while his mother stepped in as Grab’s first individual angel investor.

Anthony relocated to Kuala Lumpur to lead operations. The app’s debut was met with overwhelming demand, reportedly receiving 11,000 booking requests on its first day. This immediate traction highlighted a critical bottleneck: supply. The team had to recruit as many drivers as they could to meet demand.

However, in 2012, this was easier said than done. The barrier to entry was high as most taxi drivers did not own smartphones and the concept was relatively new. The founding team adopted an intensely hands-on approach to bridge this gap. They visited airports, gas stations, and coffee shops to personally recruit drivers, often having to convince them of the value of mobile technology. The company went as far as purchasing smartphones in bulk and reselling them to drivers on installment plans, effectively subsidizing their fleet’s digitization.

These ground game tactics proved so effective that they became the blueprint for regional expansion.

“In Vietnam, we approached drivers at 4 a.m. at the start of their shifts,” described Aaron Gill, an early executive. “In Singapore, we targeted taxi queues at Changi Airport. One person would explain the app to the driver, and the other would download it onto his phone.”

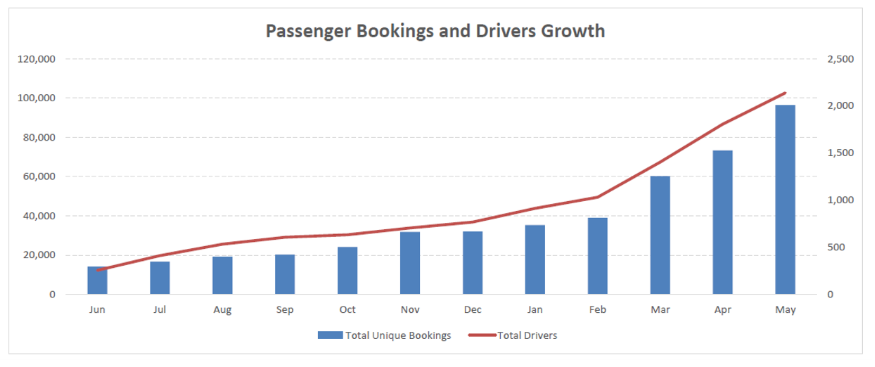

The value proposition was compelling: the app allowed drivers to optimize their routes, earning more while spending less time idling. With the incentives aligned, the supply network began to scale rapidly. By May 2013, data from early investor Vertex Ventures showed that Grab had successfully onboarded approximately 2,000 drivers and was processing 96,386 unique bookings per month.

Source: Vertex Ventures

c. Expansion and the Defeat of Uber

Following its Malaysian debut in 2012, Grab expanded into the Philippines, Singapore, and Thailand in 2013, followed by Vietnam and Indonesia in 2014. This expansion was fueled by its first major institutional backing in 2014 from Vertex Ventures, at a time when the app had approximately 250,000 monthly active users.

Growth coincided with the 2013 arrival of Uber. Despite Uber’s deep pockets and superior tech, they failed to dominate, leading to a five-year battle for the region. Grab’s eventual victory was rooted in hyper-localization. While Uber tried to replicate its US model, Grab adapted to the nuances of Southeast Asia.

Cash Adoption: Realizing that credit card penetration was low, Grab accepted cash payments from Day 1—a feature Uber was slow to adopt, effectively locking itself out of the mass market.

Beating Traffic: In congested cities like Ho Chi Minh City, Grab launched GrabBike (motorcycle taxis), a culturally attuned solution that allowed passengers to weave through traffic.

Regulatory Strategy: Unlike Uber’s infamous “move fast and break things” approach, Grab positioned itself as a partner to governments, working collaboratively to solve traffic and safety issues.

As noted by early investor Vertex Ventures:

“Uber worked on the principle of ‘anti-regulator’ while Grab has always worked with regulators. In SEA, the ‘anti-regulator’ approach does not work. Perhaps the key factor... lies in the company’s management – where the Founders lead and run the business. Competitors like Uber were managed by hired professionals with no Founders’ mentality.”

In March 2018, the battle ended in a historic consolidation. Uber surrendered, selling its entire Southeast Asian operations to Grab in exchange for a 27.5% equity stake, with CEO Dara Khosrowshahi joining Grab’s board. This victory cemented Grab’s uncontested leadership in the region.

d. The Superapp Pivot

With Uber’s exit, Grab pivoted from a ride-hailing app to a comprehensive “Superapp” ecosystem. The acquisition of Uber’s assets allowed Grab to immediately scale GrabFood, leveraging its massive driver fleet to deliver meals.

Simultaneously, the Company moved to capture the region’s massive underbanked population. GrabPay, originally introduced in 2016 as an in-app payment method, was relaunched in November 2017 as a full-fledged digital wallet for third-party merchants. This fintech ambition culminated in Grab securing digital banking licenses in Singapore and Malaysia, giving Grab the opportunity to become a digital financial services powerhouse.

This evolution transformed Grab from a utility app into a synergistic ecosystem. By stacking high-frequency services like Mobility and Delivery atop a financial layer, Grab created a self-reinforcing flywheel. Today, the platform functions as a walled garden where users acquired through daily commutes or lunch orders are naturally funneled into higher-value services like payments, lending, and insurance.

Source: Grab Investor Day 2022

e. The IPO, The Crash, and The Pivot

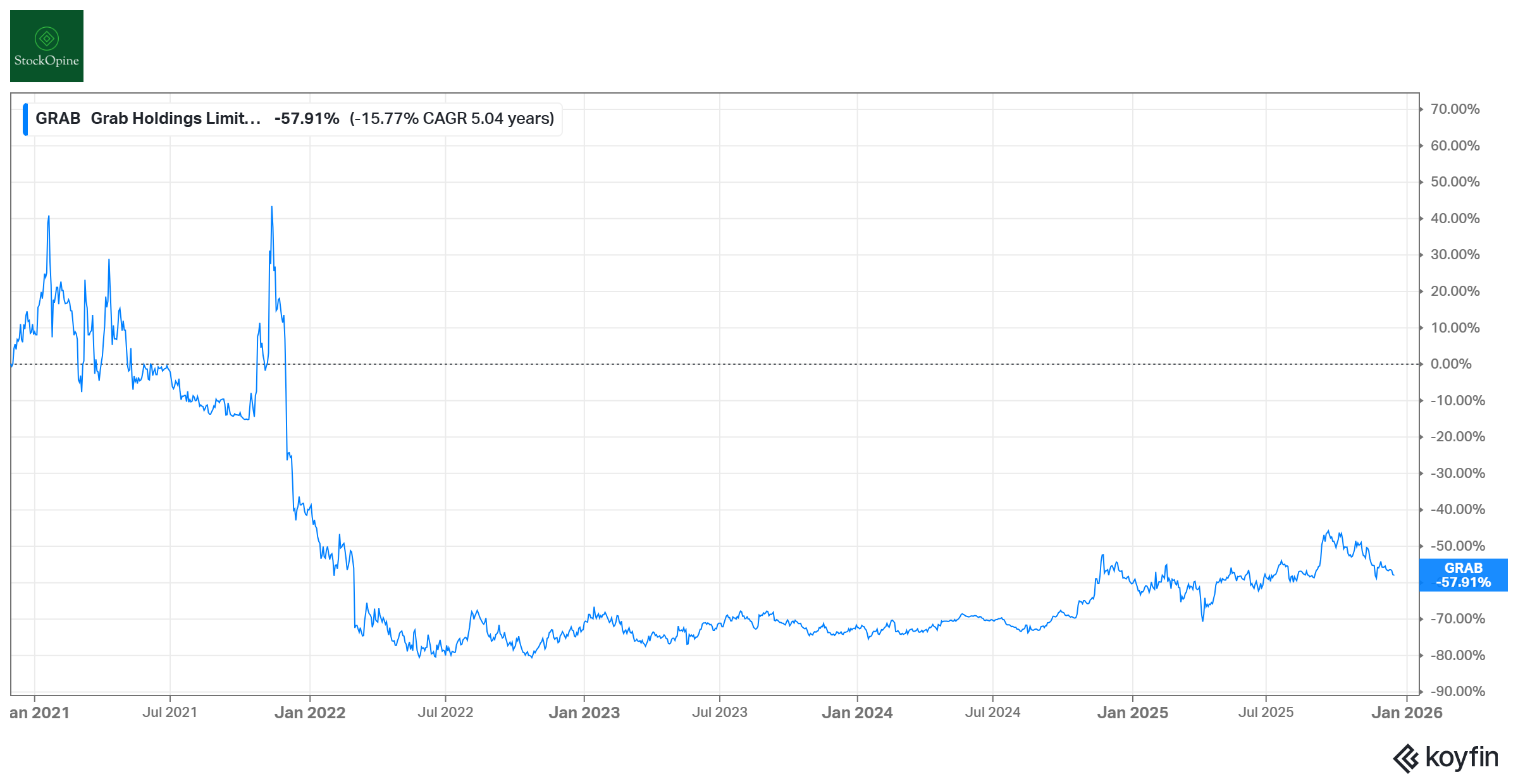

In December 2021, Grab went public on the Nasdaq via a merger with Altimeter Growth Corp, the largest SPAC deal in history, valuing the company at nearly $40 billion. However, the post-listing experience has been a volatile ride for shareholders, with the stock currently down approximately 57% from its IPO price.

Priced for perfection at the peak of the 2021 SPAC bubble, the valuation left no margin for error. At $40 billion, Grab was trading at over 20x revenue while simultaneously burning roughly $1 billion in cash annually. Inevitably, reality failed to meet these heightened expectations.

The most painful reality check occurred in March 2022, when Grab released its Q4’21 earnings—its first major report as a public company. Revenue collapsed 44% YoY to just $122 million (missing analyst expectations of ~$167 million). The cause was the aggressive growth strategy: Grab had poured massive amounts into driver and rider incentives to defend its market share. Because Grab reports revenue net of these incentives, this spending effectively wiped out its top line, shocking investors who had focused on top-line growth.

It is only recently (late 2024/2025) that the stock has begun to stabilize. This shift has been driven by a decisive change in management’s tone from growth at all costs to sustainable profit. The promise fulfilled by delivering the firstGAAP profitablele quarter in Q3’25.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

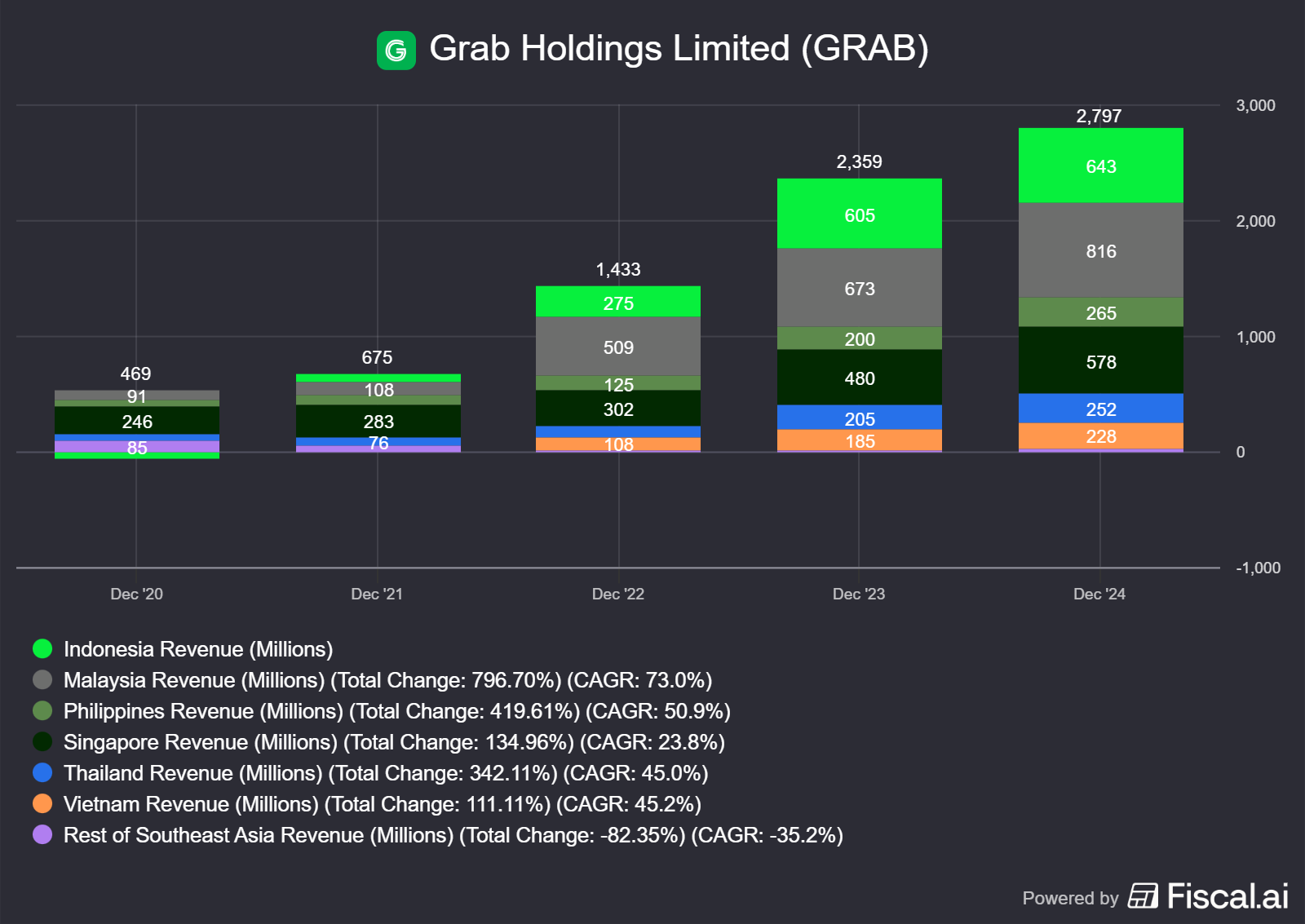

f. Geographic Footprint

Grab has built a diversified revenue base with the platform’s reach spanning to over 800 cities across eight countries in Southeast Asia. As of FY24, Malaysia stands as the largest revenue contributor at $816 million (29% of total revenue), followed by Indonesia at $643 million (23%), and Singapore at $578 million (21%).

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

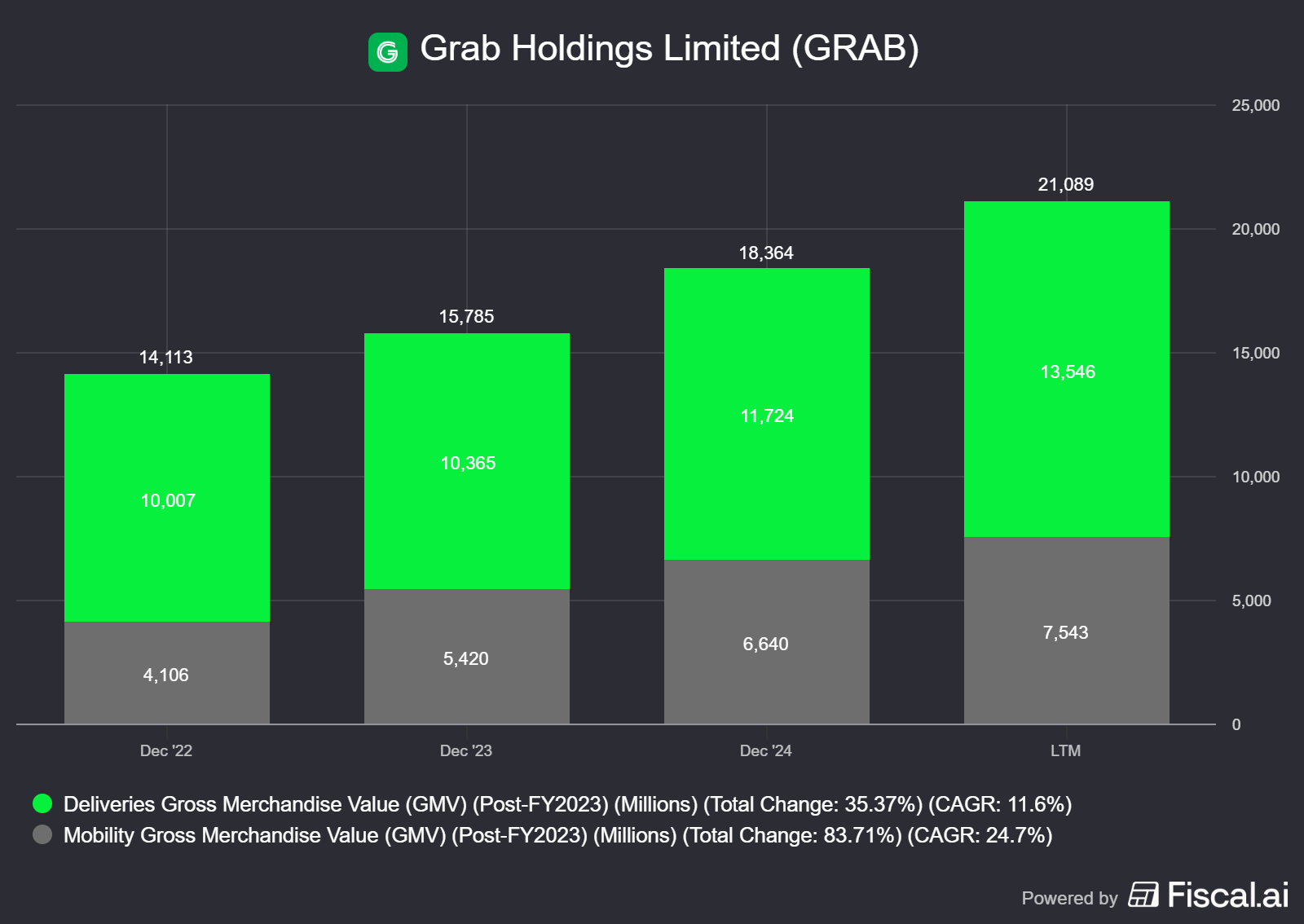

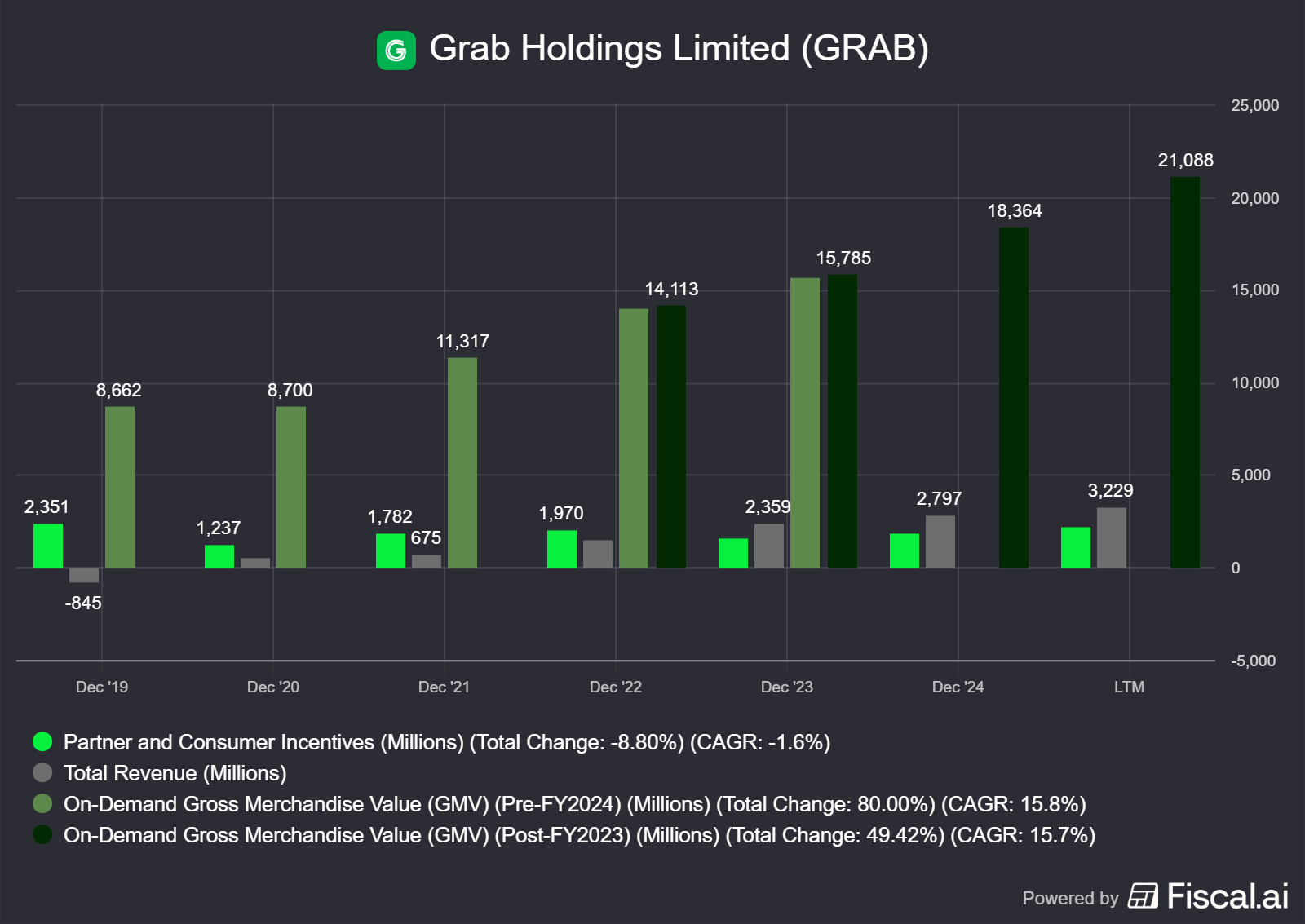

g. GMV, Take Rates and Incentives

The adoption of the platform is best measured by Gross Merchandise Value (GMV)—the total amount users spend on mobility and deliveries. This metric has demonstrated robust growth, expanding from $14 billion in FY22 to $21 billion over the last twelve months, representing a 16% CAGR.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

However, the critical lever for investors is the Take Rate which is the percentage of GMV or the commission that Grab retains as revenue. Grab currently reports a take rate of approximately 14%, but this figure is net of the incentives paid to consumers (discounts) and partners (driver bonuses). Historically, these incentives were aggressive, often exceeding the commissions earned to stimulate supply in rural areas or during market launches. As recently as FY22 and FY23, Grab reported “excess incentives” of $580 million and $391 million respectively, meaning they paid out more than they earned in specific segments.

As the marketplace matures, management is rationalizing this spend, turning a former headwind into a tailwind. Over the last three years, Grab’s net take rate averaged 14% while incentives consumed roughly 10% of GMV. By comparison, Uber reports a take rate closer to 27%. This spread highlights the massive latent profitability in Grab’s model. In a rationalized monopoly/duopoly environment, if Grab can structurally reduce incentives by just 3 percentage points, nearly all of that savings would flow directly to the bottom line as incremental profit.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers) *Post FY23 Grab made reporting changes to its On-Demand GMV

h. User Base and Monetization Trends

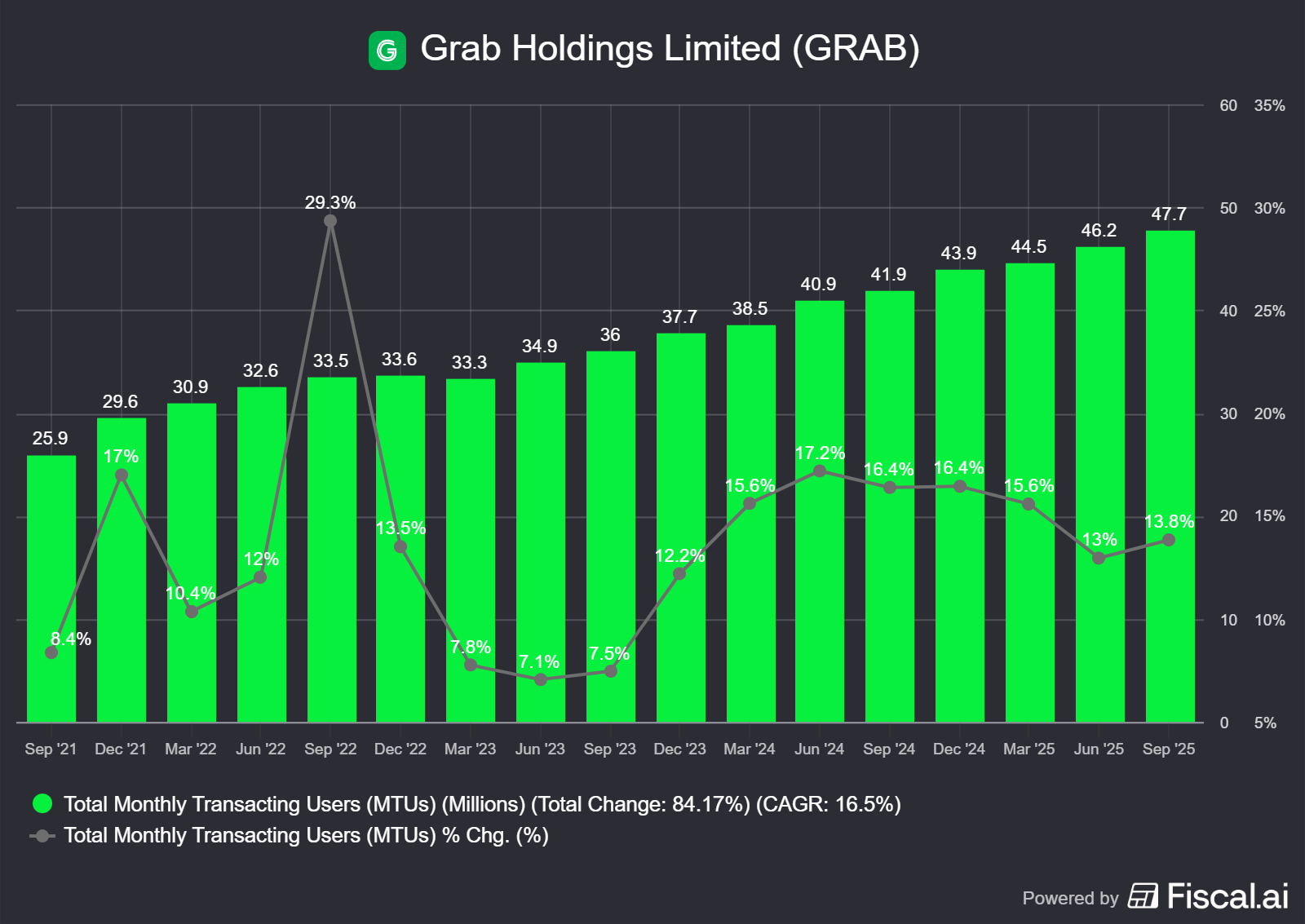

Grab’s user base continues to expand, reaching 48 million Monthly Transacting Users (MTUs) as of the end of 2024, a 16% CAGR since 2021. Despite this scale, the runway remains long; 48 million users represent only roughly 10% of the working-age population in its operating regions. In a market consolidating around 2-3 key players—similar to the US (Uber, Lyft, DoorDash) or Europe (Uber, Bolt, Wolt)—Grab’s leadership position allows it to capture the majority of this remaining penetration.

Notably, growth is accelerating, with MTUs up 14% YoY in Q3 ’25, and Daily Transacting Users growing even faster than the monthly metric.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

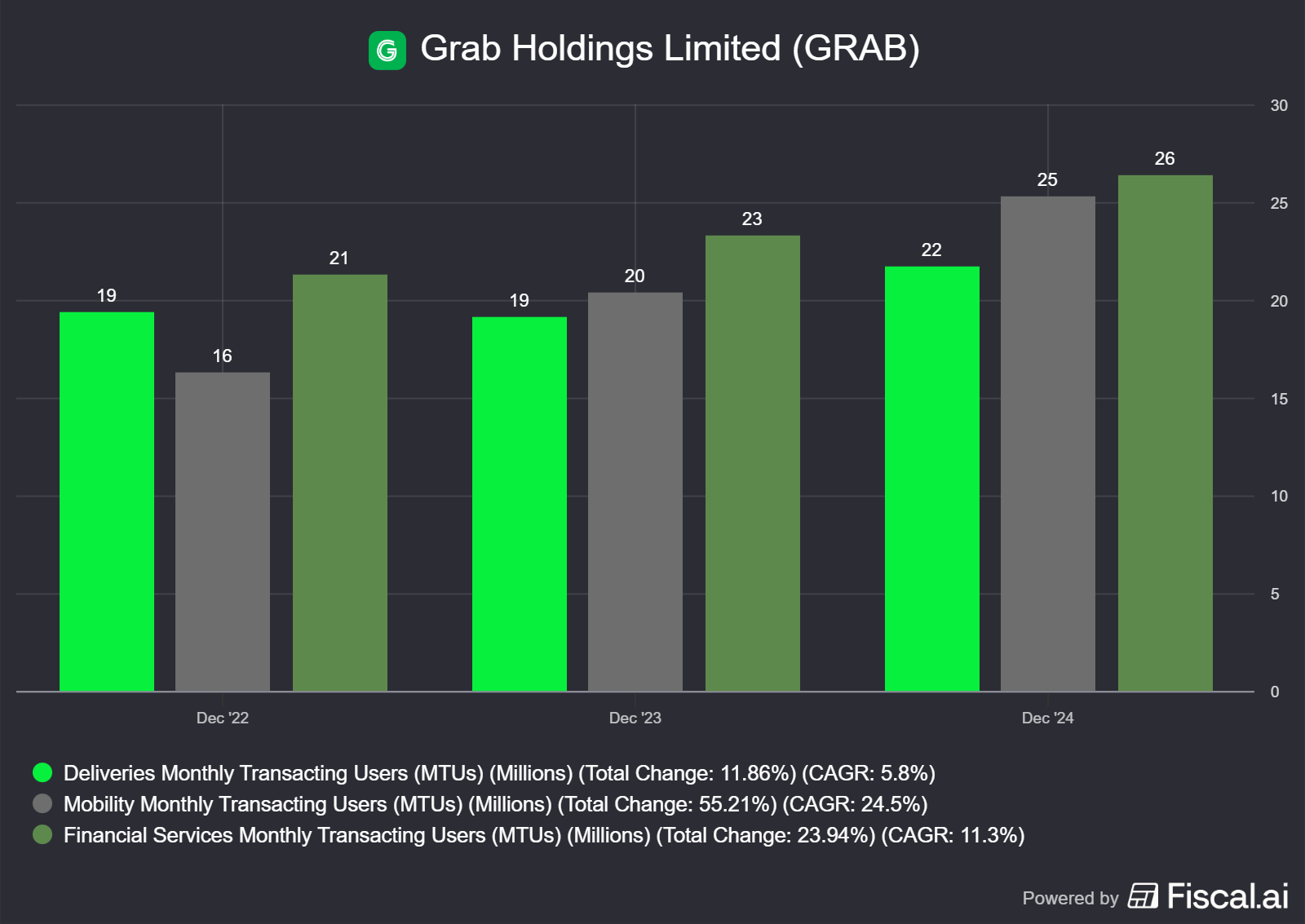

Breaking this down by segment as of the end of FY24, Financial Services leads with 26.4 million MTUs (+13% YoY), followed by Mobility at 25.3 million (+24% YoY) and Deliveries at 21.7 million (+14% YoY).

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

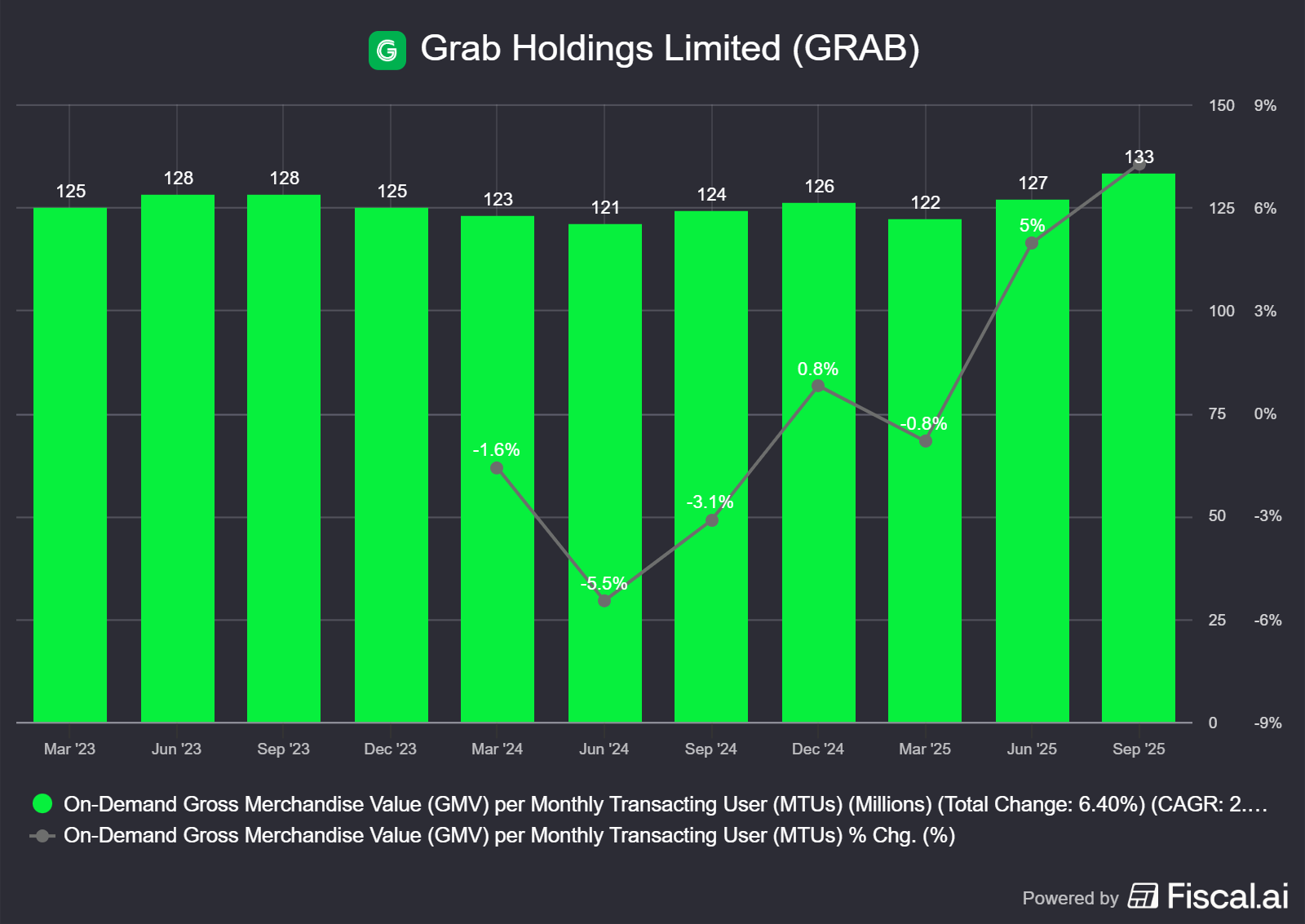

Alongside user growth, the monetization per user is reaching an inflection point. While GMV per MTU saw a strategic decline in 2024 (dropping 2% to $494), this was a calculated trade-off to drive mass-market adoption through affordable options like "GrabCar Saver" and "GrabFood Saver." This strategy is now bearing fruit. In Q3 ’25, Grab recorded its second consecutive quarter of rising wallet share, with GMV per MTU growing 7% YoY, proving that the new affordable cohorts are increasing their transaction frequency and graduating into the broader ecosystem.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)