HubSpot Deep Dive: From Inbound Pioneer to AI-First Platform

The AI pivot, the execution risks, and what it's worth.

In 2006, HubSpot defined an era by coining the term “inbound marketing”. Today, the very world it helped create (one of SEO, blogs, and content) is being fundamentally challenged by the rise of Generative AI. For any other company, this might be an existential threat. For HubSpot, it may be its greatest opportunity. With 19 years of unified customer data from over 270,000 customers, HubSpot believes it holds the one thing AI needs to be truly valuable: context. This deep dive will analyze HubSpot at a critical inflection point, dissecting its strategic pivot from a marketing platform to an AI-first company and what that means for its valuation.

Contents:

Key Facts

Business Overview

Management

Industry

Financial Analysis

Competitive Advantages, Opportunities and Risks

Valuation

Conclusion

1. Key Facts

Description: Hubspot is a leading Customer Relationship Management (CRM) and marketing automation platform, designed primarily for small and mid-size companies (SMBs). The company has expanded into a comprehensive, multi-product suite of “Hubs” (including Marketing, Sales, Service, Content, and Commerce). This integrated platform allows customers to consolidate their entire go-to-market tech stack, providing a unified view of the customer journey, which is now being enhanced with a deep layer of AI features.

Key Financials: From FY15 to trailing twelve months (TTM) Q2’25, HubSpot achieved a revenue Compound Annual Growth Rate (CAGR) of 34%, reaching TTM revenue of $2.8 billion. While not yet GAAP profitable, HubSpot has expanded its non-GAAP operating income from a $25.1 million loss in 2014 to an LTM non-GAAP operating profit of $488 million (17.1% operating margin). The company has cash and short-term investments of $1.7 billion, zero debt, and operating lease liabilities of $281 million.

Price & Market Cap (as of 31 October 2025): Its market cap is $25.9 billion with a 52-week low of $418 and a 52-week high of $881, whereas it currently trades at $492.

Valuation: Hubspot trades at a LTM EV/Sales of 8.6x (5 Year average of 16.1x).

2. Business Overview

a. The ‘Inbound’ Philosophy

HubSpot’s entire existence stems from a fundamental shift in marketing philosophy, championed by its founders, Brian Halligan and Dharmesh Shah, during their time as graduate students at MIT in the mid-2000s. They observed that traditional “outbound” marketing tactics like cold calls, spam emails, and broadcast ads were becoming increasingly ineffective. They were interrupting customers instead of attracting them.

Halligan and Shah realized that businesses needed to adapt to this new reality. Their core insight, which they detailed in their best-selling book “Inbound Marketing: Get Found Using Google, Social Media and Blogs”, was to flip the traditional marketing model. Instead of pushing messages out to uninterested audiences, businesses should pull customers in by creating valuable content and experiences tailored to them.

This became the “Inbound Marketing” philosophy. The concept is straightforward: stop chasing customers and help them find you. The strategy involves publishing useful content (such as blog posts, e-books, videos) optimized for search engines (SEO) and shared via social media and email. This content naturally attracts individuals already searching for solutions online, allowing businesses to build trust and credibility, ultimately converting interested strangers into loyal customers.

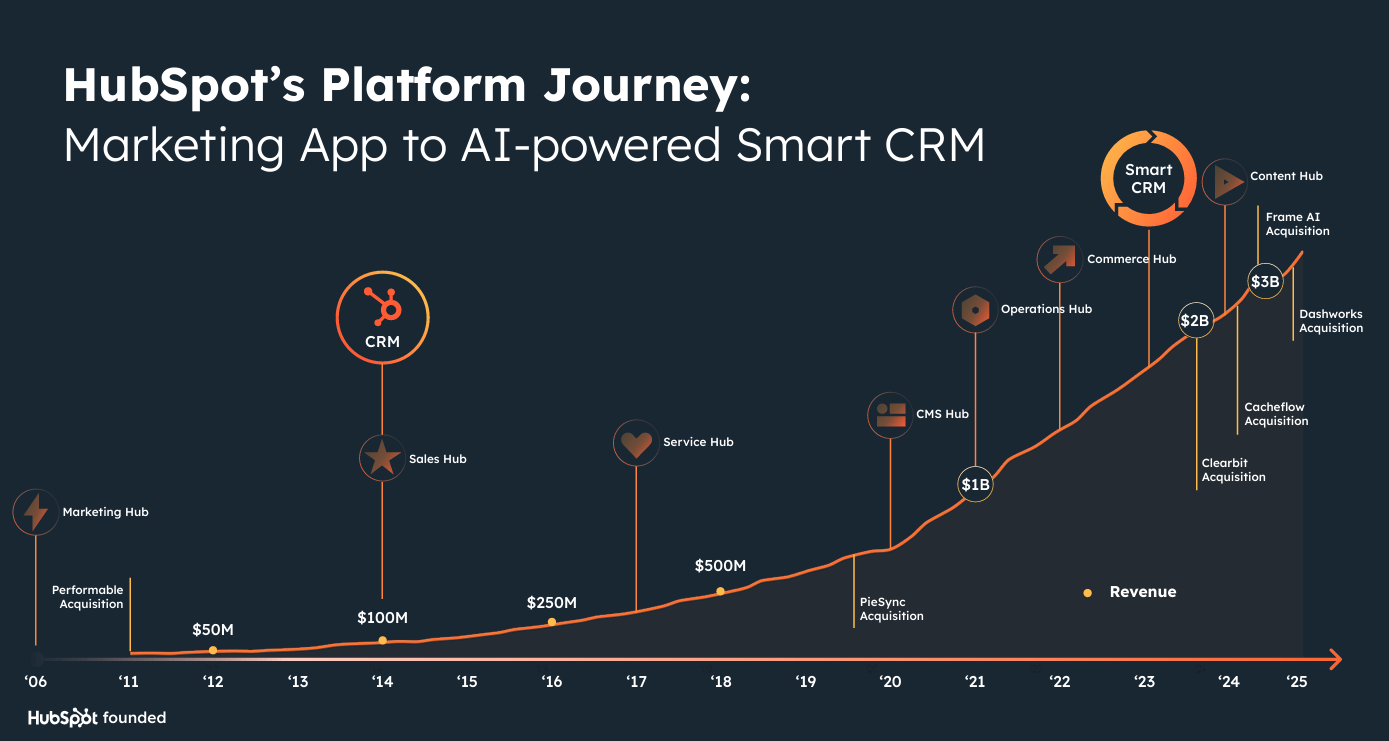

When HubSpot was founded in 2006, this philosophy was its entire focus. The company’s original software was designed as an all-in-one platform to empower businesses, particularly small and medium-sized ones, to execute this inbound strategy effectively.

b. The HubSpot Platform: From Marketing Tool to AI CRM

The original Hubspot platform integrated tools for social media, SEO, blogging, website content management, marketing automation, email, and analytics, solving the pain point of businesses needing multiple applications for these tasks.

The founders specifically targeted SMBs, a segment largely ignored by competitors who focused on upmarket clients. As the founders discussed in their ‘Crucible Moments’ interview with Sequoia Capital, they believed the internet leveled the playing field for SMBs and that inbound marketing offered a cost-effective way for these businesses (often lacking large budgets) to gain traction online.

“You used to need a ton of money to get found online, but all of a sudden, there was Google and social. And if you create a great piece of content, it would spread and pull people in like a magnet. Now, all of a sudden, any small business could create content and your success in marketing shifted and your success became much more about the width of your brain than the width of your wallet.” Brian Halligan

“But trying to put all the pieces together to kind of leverage the internet in the way that it needed to be leveraged and to do inbound marketing, it just was a science project for a lot of these companies. They did not have the time or the talent to actually do all those things.” Dharmesh Shah

While investors initially balked at the SMB focus due to perceived high acquisition costs and churn rate, Halligan and Shah argued that the efficiency of inbound marketing negated this concern.

“Everyone’s reaction to SMB was consistent. Don’t do it. No one liked the idea of doing a small business play.” Brian Halligan

The CRM Launch: The Trojan Horse

Source: Hubspot Q2’25 Earnings presentation

The next pivotal moment arrived in 2014, coinciding with the company’s IPO. Recognizing that the owner of the CRM often wins the customer relationship, HubSpot introduced its free CRM product.

They realized that the sales process was outdated, and the CRM available at the time was complex and affordable only to big customers. SMBs were still using spreadsheets, email and memory to manage their customer relationships. And the CRM, was not given only to existing customers, it was given out for free.

The two main barriers keeping SMBs from using a CRM were that existing products were too complicated or too expensive. HubSpot aimed to remove both of these.

This aligned perfectly with the company’s core mission “Help millions of organizations grow better” as former Chief Strategy Officer Brad Coffey explained in a 2015 blog post detailing the decision:

“From a culture perspective, giving the CRM away for free wasn’t a crazy idea. Our overarching mission is to solve for the customer and the entire inbound movement is rooted in the idea that the size of your brain matters more than the size of your wallet. We didn’t want a product that would only be valuable to our existing marketing customers or to companies with big budgets; we wanted one that would empower any business to grow. The simplest way to remove any barriers to smarter prospecting was to make the CRM free to everyone. Growing the number of visitors, leads, and customers is a goal shared by thousands of companies HubSpot reaches every day. But many of them don’t use the core, modern tools to engage with those prospects effectively. These companies are relying on email, spreadsheets and their memory to move their deals through the sales process. They simply don’t have a CRM -- and they should. We found that cost and complexity were the big inhibitors of adoption.”

Now, Hubspot was going head-to-head with the elephant in the room, Salesforce, a Company synonymous to CRM.

But this freemium CRM became the “Trojan horse”, attracting a massive user base and dramatically lowering customer acquisition costs. It established the central, unified database for customer information. From this foundation, HubSpot systematically expanded its offerings, adding specialized, paid “Hubs” that were integrated into the free CRM.

The Hubs: A Multi-Product Suite

Source: Investor Day 2025 Presentation

Today, the HubSpot platform consists of several integrated Hubs built around the core CRM:

Marketing Hub: The original inbound marketing suite. It surpassed $1.5B in ARR as of Q2’25 (up 11% year-over-year) and recognized as a leader by Gartner for fifth consecutive year. It is the largest hub in terms of ARR, being approximately 50% of Hubspot’s total ARR ($2.9 billion as of the end of 2024). The hub provides a comprehensive toolset which includes features for lead generation (forms, landing pages), content creation (blogging, video hosting), and marketing automation. It also integrates email marketing, social media management, SEO tools, and performance-based advertising analytics.

Sales Hub: Introduced alongside the CRM in 2014, it is the second largest hub, providing tools for deal pipeline management, quoting, forecasting, meeting scheduling and more. It has seen rapid growth, up 24% year-over-year as of Q2’25, and cited as $500 million plus business in Q1’23.

Service Hub: Launched in 2018, with tools for ticketing and support. Service Hub growth is sustained in the high 20s.

Content Hub: Initially part of the Marketing Hub , it was unbundled and launched as a standalone CMS product in 2020 and rebranded/relaunched with significant AI capabilities in 2024. It is the fastest growing hub, and saw significant increase in attached rates to marketing hub, increasing to 54% in Q4’24 compared to 13% in prior year.

Operations Hub (now Data Hub): Launched in April 2021 to help sync customer data and automate processes.

Commerce Hub: Launched in 2023, this is a key feature that enables customers to accept payments to facilitate quoting, billing, and payment collection directly within the CRM. As of October 2024, and since launched in 2023, HubSpot has processed more than $1 billion in GMV. This is relatively small but payments have ample room of opportunity to grow.

This multi-hub strategy allows customers to consolidate their go-to-market tech stack on a single platform, reducing complexity and providing a unified view of the customer journey, a significant value proposition in today’s fragmented software landscape.

Integral to the platform’s value is its openness. HubSpot boasts a robust App Ecosystem with over 1,900 integrations (more than 10x over the last five years) of third-party apps. Customer usage is high, with the average number of active integrations per customer growing from 10 to 14 over the last 5 years. This ecosystem approach increases stickiness and embeds HubSpot into customer workflows. HubSpot views its unified data platform as a key differentiator in realizing value from AI faster than competitors, as AI thrives on the complete customer context provided by having marketing, sales, and service data in one place.

c. The Go-to-Market Strategy

HubSpot’s go-to-market strategy is to acquire customers across the entire business spectrum, from individuals to large enterprises. Its freemium-based pricing model acts as the flywheel for the entire system, designed to make it easy for customers to try, buy, and grow with the platform. This results in a scalable model. As small businesses grow, their needs become more complex, and they naturally upgrade to the higher-priced Pro and Enterprise tiers, becoming high-value customers.

The overall approach is “bimodal,” focusing on two distinct goals simultaneously:

Driving Volume: At the lower end (Free and Starter tiers).

Driving Value: At the higher end (Professional and Enterprise tiers)

The Bimodal “Flywheel”: Tiers

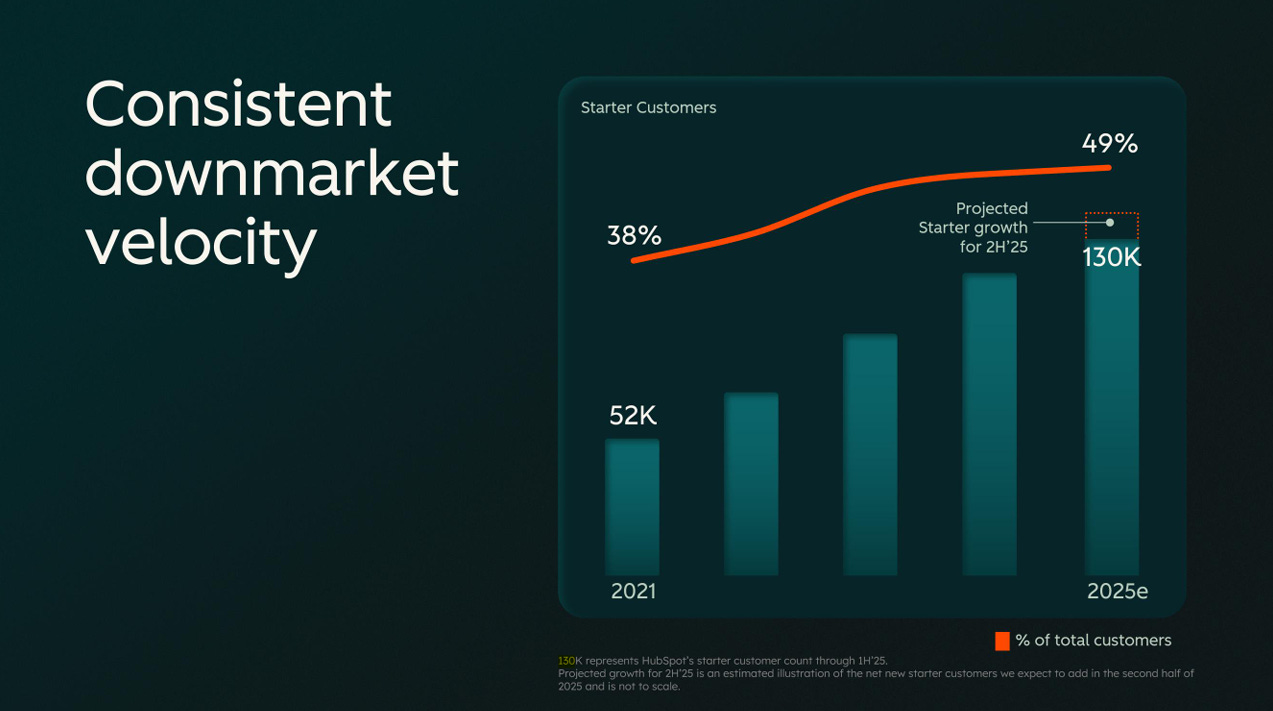

Free and Starter Tier: This is the high-volume tier used to attract millions of small businesses. The Starter tier alone represents about half of all customers (up 10 percentage points over the last 4 years), though it contributes only a small percentage of revenue, as it typically serves single-seat businesses at a low price points (around $15/month).

Source: Investor Day 2025 Presentation

Pro and Enterprise Tiers: While the Starter tier drives customer volume, the Professional and Enterprise tiers drive the vast majority of revenue. This is a targeted, high-touch approach for larger, more complex businesses.

The 2024 Pricing Overhaul

In an effort to reduce friction, accelerate customer acquisition, and encourage upgrades, HubSpot initiated a significant pricing strategy adjustment that took effect in March 2024.

The core problem was the jump from starter to pro, which customers consistently cited as a major point of friction. The legacy model included a high base fee plus a minimum number of paid seats (e.g., 5 for Pro) for its higher tiers. This created a significant entry cost.

The new model attacks this friction directly:

It lowered the price of the Starter tier to boost free-to-starter conversions.

It eliminated seat minimums from Pro tiers, allowing customers to start with exactly what they need and buy more as they grow.

As CEO Yamini Rangan noted, “by lowering the price per seat for pro and enterprise, it reduces that friction. And again, we’re seeing that. And in making this change, there are more customers that start with starter and then continue to upgrade into pro and enterprise, which is exactly what we want in order to be -- to have a great”

This change created an intentional trade-off: a lower Average Subscription Revenue Per Customer (ASRPC) in the short term, which is expected to be ultimately offset by higher customer volume. Early signs validate this thesis:

Free-to-Starter conversion is at an all-time high, up 50% year-over-year.

The average number of Pro Plus customers added quarterly increased by 16% post-launch.

The share of customers who upgrade their Sales or Service seat is about 3 points higher under the new model.

The change is expected to be a 2-point tailwind to Net Revenue Retention in 2025 and a continued benefit in 2026.

A critical component of the March 2024 pricing change was the introduction of the Core Seat. The rationale of this decision was to unbundle and monetize the Smart CRM platform itself, rather than giving it away through the purchased hubs.

Legacy Model: Under the old model, only about 20% of users required a paid seat. These were “Persona Seats” for sales or service reps. The core CRM editing functions were often used for free by admins and operations.

New Model: The Core Seat is now required for edit access to the Smart CRM, while free “View-Only” seats are unlimited. This move directly monetizes the admin and operations users who derive value from the platform. As a result, about 60% of users who purchase under the new model now take a paid seat.

This strategy has been validated quickly. In just 18 months, the Core Seat surpassed $100 million in ARR and is growing quickly, confirming the thesis that significant untapped value existed in the Smart CRM.

The Solutions Partner Ecosystem

A defining component of HubSpot’s strategy is its vast ecosystem of over 6,000 “Solutions Partners” (e.g., marketing agencies, sales consultants), which contributes approximately 40% of customer ARR. This channel is highly effective in acquiring larger, upmarket customers.

In late 2023, HubSpot announced a significant change to its commission structure (effective in 2025), shifting incentives from retention to acquisition. The legacy 20% lifetime commission was replaced by a 3-year commission on new deals, and lifetime commissions for existing deals are revoked if solution partners are not actively engaged with customers.

Despite this controversial change, the channel remains robust; co-selling (a key indicator of partner engagement) grew 41% year-over-year in Q1 2025, followed by 29% in Q2 2025. While the long-term effect on the partner ecosystem is still to be seen, we expect the new structure to drive profitability improvements for HubSpot in the future.

d. Customer Landscape

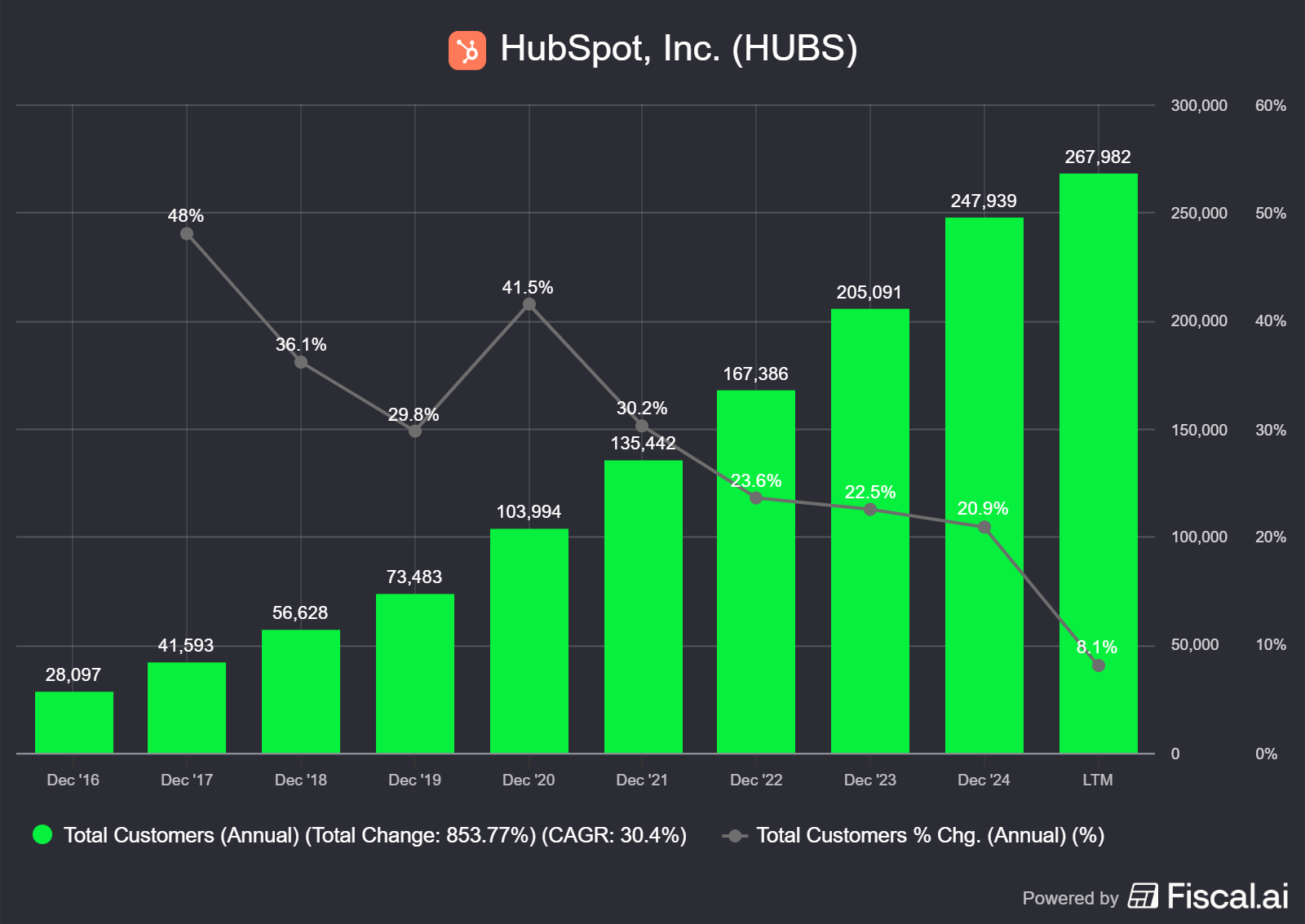

HubSpot’s customer base has evolved significantly from its early days, growing from 11,000 customers at its 2014 IPO to over 270,000 today. The company primarily targets small and mid-size companies, generally those with 2-2,000 employees, with its largest segment being the 20-200 employee cohort.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

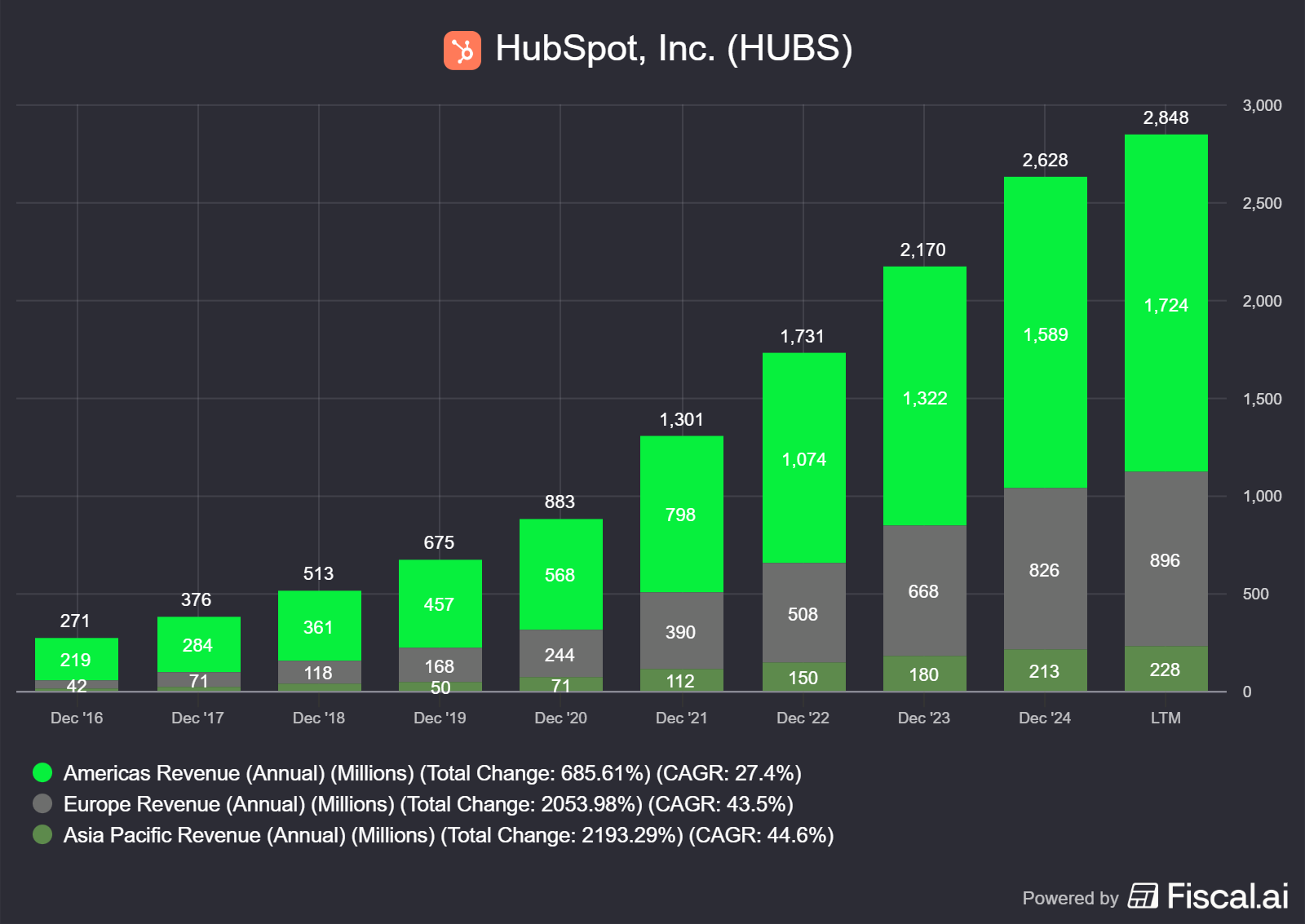

The business is also geographically diverse, with 39% of revenue coming from outside the US. Subscriptions are the dominant revenue source, accounting for 98% of revenue, with the remaining 2% from services like on-boarding, training, and Commerce Hub payments.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

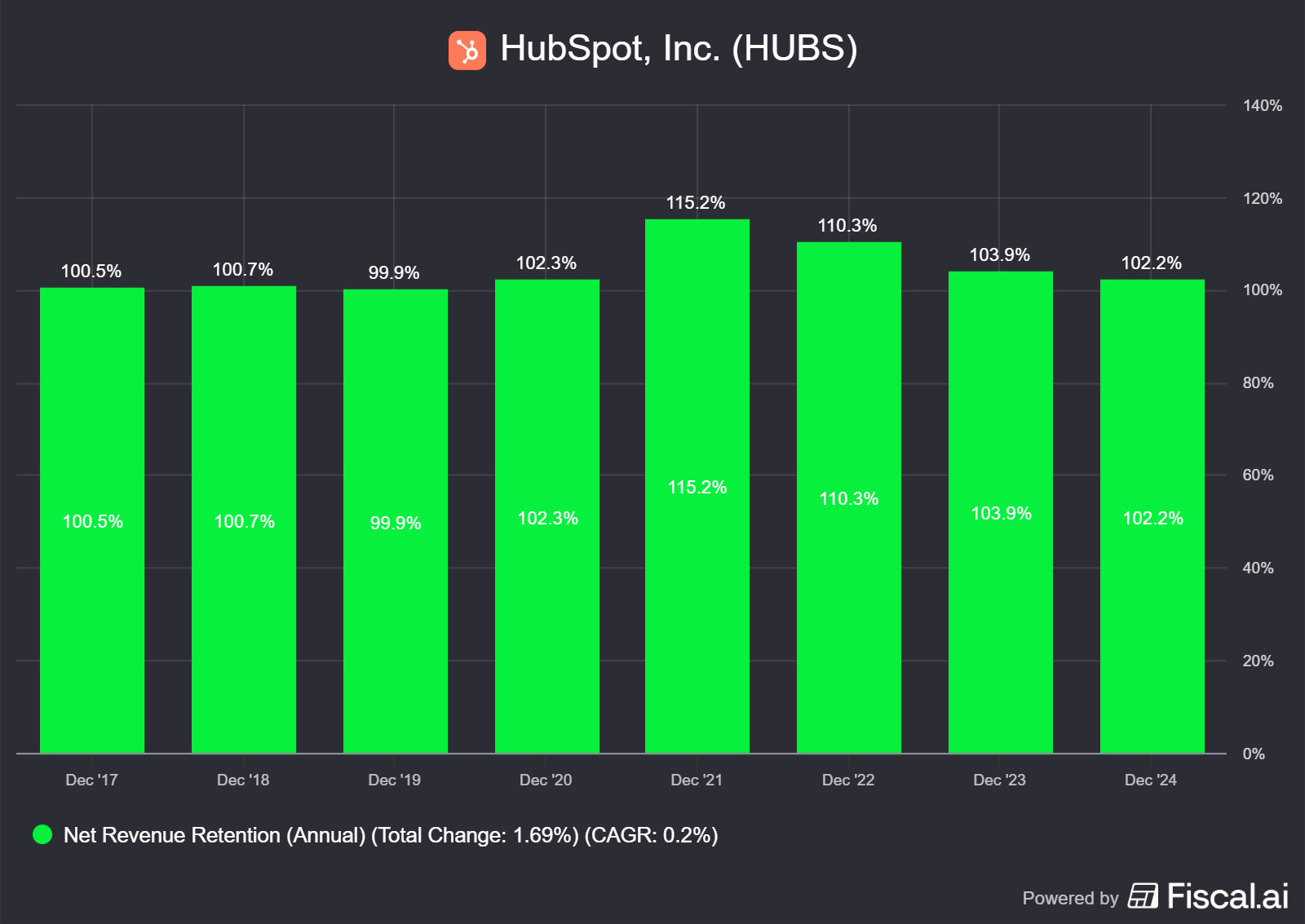

Retention (NRR vs. CDR)

HubSpot tracks two key retention metrics that tell different stories:

Customer Dollar Retention (CDR): This metric primarily reflects churn and has remained stable and healthy in the “high 80s” (88% as of 1H’25). This stability highlights the platform’s stickiness.

Net Revenue Retention (NRR): This metric includes expansion from existing customers (upgrades and cross-selling). After tracking above its 110% long-term target, NRR fell post-Q2’22 to 102% by 2024. This decline was primarily driven by a slowdown in expansion motions as macroeconomic pressure (high inflation and interest rates) forced companies to optimize spend, reduce seats, and slow upgrades.

“The area where we continue to see challenge is the same one we’ve been talking about for a number of quarters, which is on that net upgrade rate… we’re also seeing lower volume of customers adding contacts and seats… customers… are really looking to optimize their spend across the board.” Kathryn Bueker, CFO Q2’23

To combat this, HubSpot enforced the pricing changes discussed in the previous section. As of Q2’25, NRR ticked up to 103% (102% in Q1’25), an improvement almost entirely driven by strong seat upgrade performance from the new model. While seat upgrades are strong, other expansion motions (like tier upgrades) are still lagging behind.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

The Upmarket & Multi-Hub Trend

A core component of HubSpot’s strategy is moving “upmarket” by selling more products to larger customers, as multi-product customers have demonstrably better retention. The key indicator of this strategy’s success is multi-hub adoption, which shows a clear and sustained trend of customers consolidating their tech stack onto the HubSpot platform.

“New and existing customers are consolidating their go-to-market technology stack on HubSpot. … The share of our installed base ARR that has on a single hub is now just 12%, more than 60% of Pro Plus ARR is on 3 or more hubs and customer ARR on 5 or more hubs has grown from 0 to 28% in Q2.” Kathryn Bueker, CFO

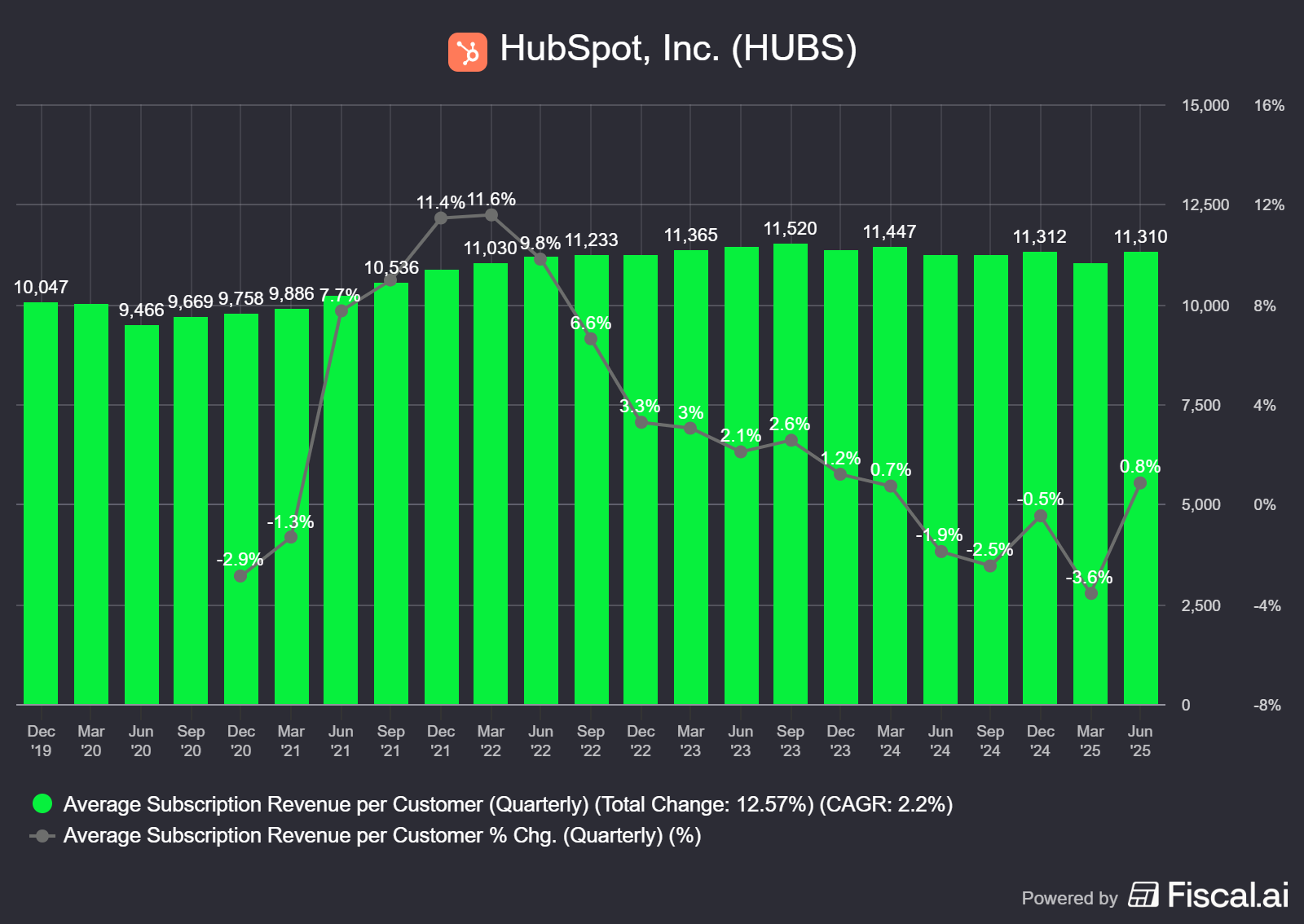

ASRPC and Net New ARR Trends

The recent pricing changes have intentionally impacted the headline ASRPC metric, as the company is acquiring a high volume of lower-cost Starter tier customers. However, management highlighted in Q3’24 that ASRPC growth, excluding the Starter tier, was in the mid-single digits. After three consecutive quarters of decline, ASRPC increased 1% in Q2’25 and is expected to grow at that rate for the back half of the year.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

More importantly, Net New ARR growth, which hit a low point in 1H 2023, has seen momentum, a clear sign of revenue re-acceleration.

“As you can see, net new ARR was challenged beginning in 2022... and hit a low point in the first half of 2023. Over the last 2 years, we have seen building momentum and a nice step-up in net new ARR growth in the back half of 2024. Since then, net new ARR growth has outpaced revenue growth. We are executing well, and our growth is beginning to accelerate.”

e. AI Strategy: The Future

HubSpot is embedding AI across its entire platform, infusing it into all hubs and tiers to drive adoption and increase the value of its core products. The company’s monetization strategy is two-pronged: driving upgrades to Pro+ tiers, which include premium AI features, and capturing consumption-based revenue through additional credits.

As CEO Yamini Rangan highlighted in Q4 2023, the plan has been to use AI as a key driver for tier upgrades:

“While all of our tiers... have AI features, we have a lot more features at the pro and enterprise tiers. In fact, 65% of the features that are becoming generally available in the first half of 2024 will be in the pro+ tier. So the way we think about it is that it will drive a lot of upgrades... And then longer term, when we drive even more sophisticated features like AI agents, then we may charge specifically for it.”

HubSpot’s competitive advantage in the AI era is not the AI models themselves, but its unified data platform. The company’s thesis is that while LLMs know the public web and provide generalized insights, HubSpot has the specific customer context—both structured (residing within the CRM) and unstructured (calls, emails). This allows the AI to provide insights and value tailor-made to a specific customer’s data.

This AI initiative is consolidated under the “Breeze” platform and includes Breeze Copilot, which acts as AI-powered companion, embedded AI features across the hubs and AI Agents that execute tasks.

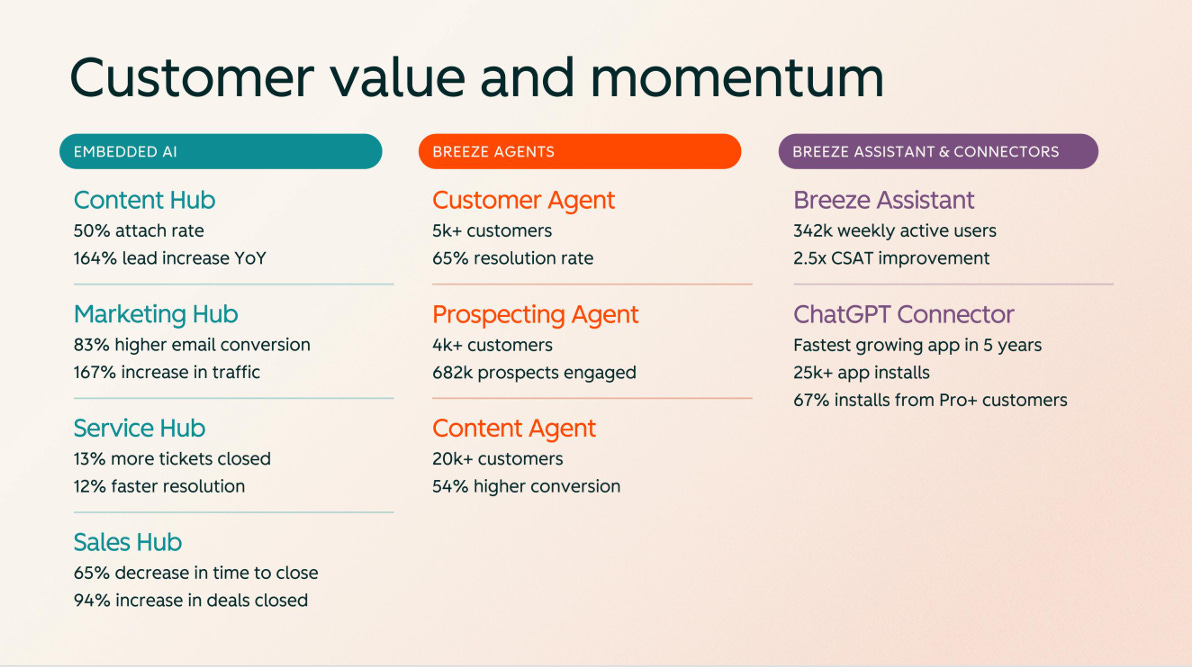

Embedded AI Features

These tools function as an assistant, designed to streamline tasks and provide data-driven recommendations. Key features include:

Sales Hub: AI meeting assistant to streamline preparation and follow-up, deal intelligence and guided actions to recommend next steps.

Service Hub: AI-powered ticket sentiment analysis, feedback summaries, and GPT-powered chatbots.

Content Hub: A suite of AI tools for content creation, remixing, and maintaining a consistent brand voice.

Usage metrics for these features signal accelerating adoption. Copilot engagement more than doubled from 270,000 active users in Q4’24 to 660,000 in Q1’25. AI features in the Content Hub have significantly boosted its attach rate to the Marketing Hub, now at 50%. Meanwhile, more than 40% of Service Hub customers are already leveraging AI capabilities.

Source: Investor Day 2025 Presentation

Featured AI Agents

Featured AI agents are designed to do work on your behalf and even communicate with each other.

“They are the AI coworker that can now take on more jobs like support, prospecting, account research and then allows the rest of the teams to do high-value work. Now there are a whole universe of agents out there. So I want to try and simplify HubSpot’s approach to agents. We build featured agents for go-to market teams to get work done. Now our prospecting agent will do account research and outreach. The customer agent will help support tickets, but also answer questions across sale and marketing. And the newly launched data agent today, it enriches customers’ data with AI. Each of these agents will get work done, but they can also call on each other to do more for our customers. Then, we are providing the ability for our customers and partners to build custom agents.” Yamini Rangan

Customer Agent: The agent focused on support. It is already used by over 5,000 customers (2,500 customers in Q1) and achieved a 65%+ resolution rate, having resolved over 1 million tickets. Customer agents close tickets 39% faster than non-users.

Prospecting Agent: This agent watches for intent signals, researches prospects and send personalized outreach, saving time for reps. It has been used by over 3,700 customers and 17,000 are on waitlist.

Content Agent: This agent helps create and personalize content. It has been used by over 12,000 customers to generate content over the last year.

The Agent Builder Ecosystem

Beyond providing its own featured agents, HubSpot is creating an ecosystem for others to build their own agents, pursuing a bimodal strategy to capture agent builders at both the high and low ends of the market.

Breeze Studio (The Upmarket Solution): Launched in September 2025, Breeze Studio is an agent platform integrated directly within HubSpot. It is designed for HubSpot customers and partners to build and list custom AI agents on the Breeze Marketplace. This addresses the complex, higher-end agent needs of companies.

Agent.ai (The “Citizen Builder” Network): At the other end of the spectrum, HubSpot is also developing Agent.ai, a low-code tool that operates as a network outside the core platform. It targets “citizen builders” solving simpler, specific tasks for themselves or small teams. This initiative has shown strong early traction, attracting over 2 million users who have built more than 46,000 agents.

Connecting to the frontier AI models

Instead of viewing frontier models as competition, HubSpot is integrating with them, turning a potential threat into a strategic partnership.

In Q2’25, the company has launched connectors for OpenAI’s ChatGPT, Anthropic’s Claude, and Google’s Gemini. The value proposition is simple: it allows a customer to ground a powerful, general-purpose LLM with their own private, specific CRM data.

This allows a user to ask ChatGPT: “find my highest-converting cohorts from recent contacts and create a tailored nurture sequence to boost engagement”. The AI can only provide that valuable, specific answer because the connector feeds it the context from the Smart CRM. The adoption has been high, as 20,000 customers have already used it to access insights across 23 million CRM records.

AI is also driving leverage within Hubspot

Beyond enhancing its customer-facing products, HubSpot is deploying AI internally as a key lever to drive operational leverage and scale its business.

As the company explained in its 2025 Analyst Day:

“our agent handled about half of our customer tickets in the first half of 2025. As a result, we have been able to hold support headcount flat for over 2 years. In marketing, we are heavy users of AI for content generation and personalization, and we have seen both efficiency gains and also higher conversion rates as a result of AI. And finally, we have started to deploy AI tools across our employee life cycle that we believe will allow us to continue to scale our best-in class G&A efficiency.” Kathryn Bueker, CFO

💭 You’ve seen HubSpot’s powerful strategic pivot from an inbound pioneer to an AI-first company. The product and the narrative are compelling.

But does the execution match the vision? And more importantly, what is it worth?

The rest of this deep dive is under paywall and addresses the following:

Management: Does the leadership team have the right incentives and track record to navigate this complex shift?

Industry: How does HubSpot really stack up against Salesforce and Adobe, and just how big is its total addressable market?

Financials: We analyze the true cash flow, margin, and future outlook to see when this bet will actually pay off.

Risks: We consider the risks of AI cannibalization and competition from the frontier AI models.

Valuation: We run a full DCF model to determine our price target for the stock and whether it’s a buy.

To see our full analysis, valuation, and final conclusion, become a paid subscriber.