IDEXX Laboratories: A Masterclass in the Razor-and-Blade Model

How a Widening Moat and Sticky Customer Base Create a Compounding Machine

This month, we are focusing on IDEXX Laboratories, the undisputed global leader in the veterinary diagnostics market.

In short, IDEXX provides veterinarians with a comprehensive suite of in-clinic diagnostic instruments, software, and external reference laboratory services that are critical for delivering modern animal healthcare.

The foundation of the company's immense success lies in its "razor-and-blade" business model. By placing its diagnostic instruments (the "razors") directly into veterinary clinics, often through multi-year commitment programs, IDEXX secures a predictable and highly profitable recurring revenue stream from the subsequent sale of consumables (the "blades") needed to run the tests. This strategy creates a powerful competitive moat and provides the business with revenue visibility.

In this report, we will dissect this business model, analyze the industry trends that support it, and conclude with a valuation of the company to determine if its shares represent an appealing investment opportunity at today's prices.

Without further ado, let’s dive in.

Contents:

Key Facts

Business Overview

Management

Industry

Financial Analysis

Competitive Advantages, Opportunities and Risks

Valuation

Conclusion

1. Key Facts

Description: IDEXX Laboratories (“IDXX”, “IDEXX”, and “Company”) is a global leader in the veterinary diagnostics market. It develops, manufacture, and distribute products and provide services primarily for the companion animal veterinary (the core business), livestock and poultry, dairy and water testing industries.

Key Financials: From fiscal year 2015 through the trailing twelve months (TTM) ending Q1 2025, IDEXX has delivered impressive growth, posting a revenue CAGR of 10.2% and an operating income CAGR of 15.9%. This has resulted in TTM revenue of $3.9 billion and operating income of $1.2 billion, yielding an operating margin of 30.7%. The company's balance sheet includes cash and short-term investments of $164 million compared total debt and lease liabilities of $1.1 billion.

Market Data (as of July 28, 2025):

Market Cap: $45.6 Billion

Share Price: $566.50

52-Week Range: $356.10 - $570.40 (currently trading near its 52-week high)

Valuation Multiples: IDEXX currently trades at a discount to its historical averages:

TTM EV/EBITDA: 34.6x (vs. a 5-year average of 42.0x)

TTM EV/Sales: 11.8x (vs. a 5-year average of 13.2x)

2. Business Overview

a. The Story of IDEXX

IDEXX Laboratories was founded in 1983 by David Evans Shaw (stepped down in 2002), who identified an untapped niche in animal health diagnostics. Starting with just five employees in Portland, Maine, the Company initially focused on creating reliable diagnostic tests for the livestock and poultry industries. A key strategic advantage in its early years was that veterinary products did not require the same lengthy and expensive FDA approval process as those for human use, allowing for rapid innovation. A major breakthrough was the development of the SNAP family of tests, which provided veterinarians with fast, accurate, in-clinic results.

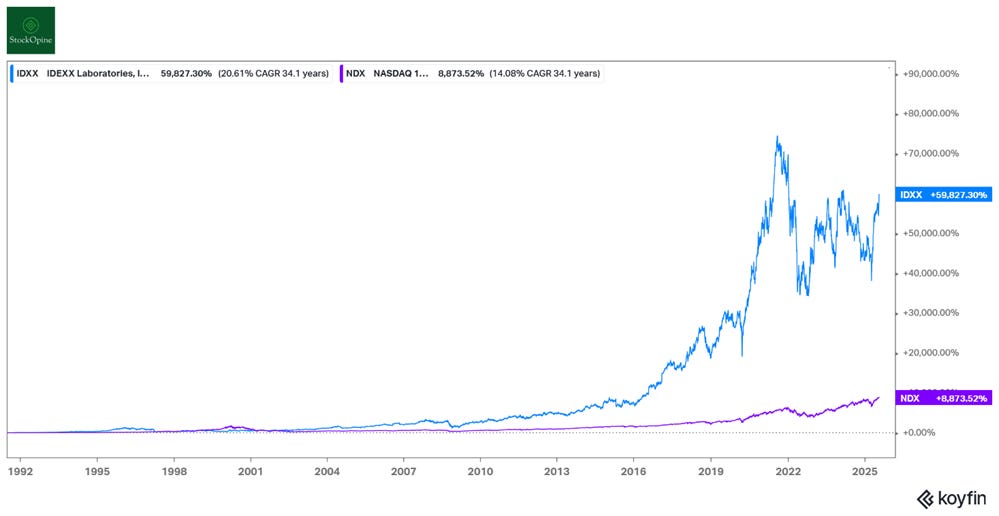

Following a successful IPO on the NASDAQ in 1991, the Company used the infusion of capital to pivot its focus heavily towards the companion animal (pets) market. This strategic shift proved successful, establishing the Companion Animal Group as the core engine of growth and transforming IDEXX into the global leader it is today. Since its IPO, the Company has delivered an impressive annual total shareholder return of 20.6% (translating to 59,827% since inception) compared to 14.1% for Nasdaq 100.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers, premium members can benefit from a 3-month free trial)

a. Business model: The Razor-and-Blade Ecosystem

This model is primarily executed through Customer Commitment Arrangements, such as the IDEXX 360 program. In these multi-year agreements, customers receive free or discounted instruments in exchange for committing to purchase minimum annual amounts of products and services. These are often structured as reagent rental arrangements, where the clinic gets use of the instrument at little to no cost, locking them into the IDEXX ecosystem. To further strengthen these relationships, IDEXX provides incentives like upfront cash-equivalent points and volume-based rebates.

This strategy creates a competitive moat. High switching costs, driven by deep workflow integration and staff training, leading to exceptional customer retention rates, consistently reported in the high 90s. The moat is further deepened by an integrated software suite, including VetConnect PLUS and Vello, which centralizes patient diagnostic history and enhances client engagement, making it increasingly difficult for veterinarians to leave the ecosystem.

IDEXX delivers its Companion Animal Group (CAG) solutions through two modalities:

Point-of-Care Solutions: In-clinic instruments that provide results within minutes while the patient is still in the practice.

Reference Laboratory Services: A global network of labs where veterinarians can send samples for more complex tests, with results typically returned the next day.

Source: March 2025 presentation

The demand for the Company's core companion animal products is primarily driven by three factors: the number of patient visits to veterinary hospitals, the diagnostic protocols recommended by veterinarians, and the rate of pet owner compliance with those recommendations.

While the CAG is the core of the business (accounting for ~92% of sales), IDEXX also operates two other segments:

Water (5% of sales): Provides testing solutions to detect microbiological parameters for government labs and water utilities.

Livestock, Poultry, and Dairy (LPD) (3% of sales): Offers diagnostic tests to manage herd health and ensure milk safety and quality.

IDEXX employs a hybrid go-to-market strategy, primarily using a large, direct sales force to engage veterinarians in North America for its companion animal, reference lab, and imaging products. To expand its global footprint, the Company supplements its direct sales efforts with independent distributors and other resellers in certain international markets.

Regulation

IDEXX operates in a complex regulatory environment, which creates a significant barrier to entry for new competitors. In the US, its products are regulated by several federal agencies:

USDA (U.S. Department of Agriculture): Oversees many of the veterinary diagnostic products.

FDA (Food and Drug Administration): Regulates dairy products used in milk monitoring programs.

EPA (Environmental Protection Agency): Approves test methods for water quality monitoring.

The company maintains licensed manufacturing facilities and must comply with a host of global product regulations, including those in the European Union. This stringent regulatory framework is a clear advantage that strengthens its market position.

R&D

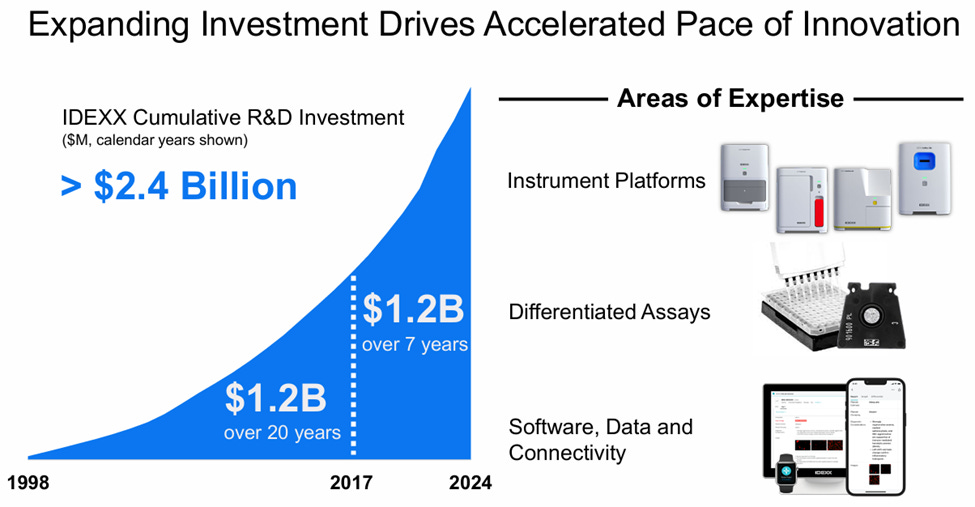

Innovation is the lifeblood of IDEXX’s strategy, enabling the Company to command premium pricing, deepen its moat, and expand its addressable markets. The Company's commitment is evident in its R&D spending, which has significantly accelerated in recent years.

In 2024, IDEXX spent $219.8 million (or 5.6% of revenue) compared to $191.0 million (or 5.2% of revenue) in 2023. The acceleration of this commitment is striking: IDEXX invested $1.2 billion in R&D over the last 7 years (2017-2024), matching the total amount it spent in the previous 20 years combined.

Source: March 2025 IDEXX presentation

While the company holds numerous patents, its strategy relies more on its innovative skills, brand strength, and integrated product offerings rather than any single piece of intellectual property, with the notable exception of key licenses related to its Catalyst platform.

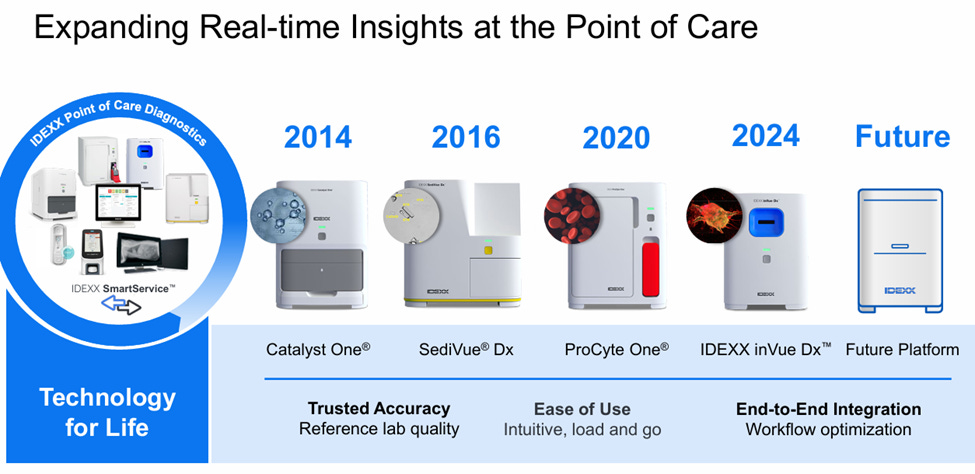

A Timeline of Recent Innovation

IDEXX maintains a rapid pace of product launches and enhancements, consistently delivering new value to its customers.

2021: Successfully launched the ProCyte One Hematology Analyzer, its next-generation point-of-care platform, delivering over 2,500 units globally in its first year.

2022: Released eight new product, service, and software solution enhancements.

2023: Delivered six new enhancements and successfully prepared for the major launch of the IDEXX inVue Dx™ Cellular Analyzer.

2024: Achieved launch readiness for nine new solutions, began shipping the revolutionary IDEXX inVue Dx Cellular Analyzer in Q4’24, and launching the Vello software, a pet owner engagement tool that integrates with its key PIMS platforms and was adopted by nearly 600 practices by year-end (over 700 by Q1’25).

2025: Launched the IDEXX Cancer Dx panel in late March, expanded Catalyst menu with Cortisol test and remains on track to expand the inVue Dx menu with a fine needle aspirate capability for analyzing "lumps and bumps".

The Next Wave of Growth Platforms

Two recent innovations, the IDEXX inVue Dx and IDEXX Cancer Dx, are poised to become major long-term growth drivers.

1. IDEXX inVue Dx: Revolutionizing Point-of-Care Cytology

The IDEXX inVue Dx Cellular Analyzer, which began shipping in late 2024, marks a new era in point-of-care diagnostics.

The Problem It Solves: Traditional cytology (the microscopic analysis of cells) is a laborious, technique-intensive process that requires significant hands-on time from a skilled veterinarian to read a slide.

The Solution: The inVue Dx platform combines advanced optics with an AI model trained on millions of cellular images to deliver a revolutionary, slide-free, "load-and-go" workflow. It analyzes ear cytology and blood morphology samples in minutes, integrating the results seamlessly with the IDEXX VetLab Station and VetConnect PLUS.

Market Opportunity & Traction: Customer interest has been exceptionally strong, with nearly 1,600 pre-orders by the end of 2024. IDEXX is targeting over 4,500 placements in 2025 and 20,000 over the next five years. The platform addresses a huge unmet need, as there are an estimated 19 million ear cytologies performed manually today, and an opportunity to add blood morphology analysis to another 20 million CBC tests annually. This is expected to contribute approximately $50 million in instrument revenue alone in 2025. Furthermore, the upcoming Fine Needle Aspirate menu expansion for inVue Dx will add another 11.5 million annual testing opportunities for evaluating common "lumps and bumps" in veterinary oncology.

With over 900 placements of inVue Dx as of April 2025, including approximately 600 in April alone after gating controls were removed, IDEXX is on track for its full-year target of 4,500 placements. Over a longer horizon, management projects that the inVue installed base will approach a size similar to the ProCyte hematology platform.

Source: March 2025 IDEXX presentation

A quote from Tina Hunt, EVP of Global Strategy and Commercial, to sum it up:

“It is slide-free, load-and-go workflow with very minimal hands-on time. And this is a process. Before inVue, that was very laborious. It took a lot of time, but also it was very technique-intensive. So you really have a doctor coming in and reading the slide.

Now they just add the sample and they get the results. The results are available in the electronic medical record. They're quantifiable, but we provide interpretation information…we're off to a great start. And what we've indicated is 4,500 for the year and 20,000 over the next 5 years.”

2. IDEXX Cancer Dx: Tapping the Multi-Billion Dollar Oncology Market

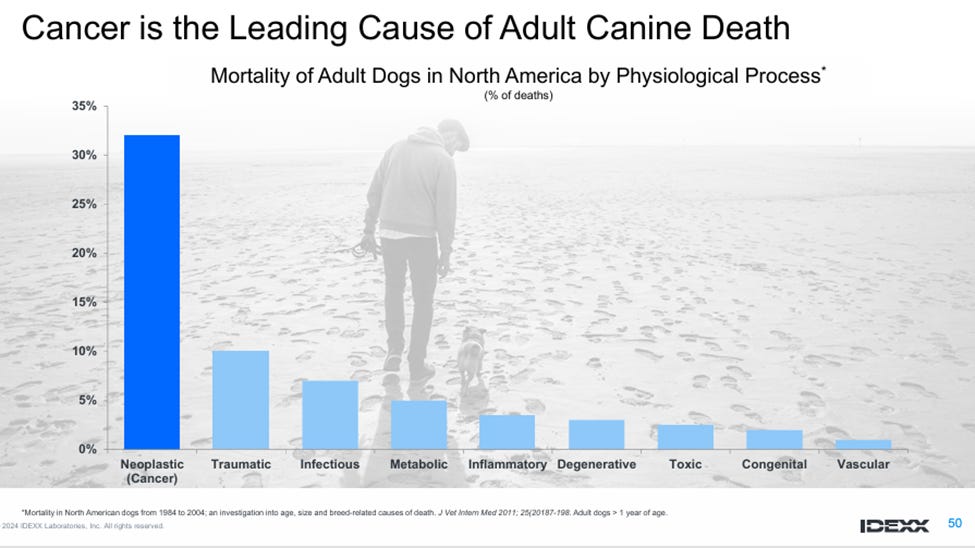

Launched in March 2025, the IDEXX Cancer Dx is a pioneering diagnostic panel for the early detection of cancer, the leading cause of death in dogs.

The Problem It Solves: Cancer in pets is often a "silent" disease that goes undiagnosed until it reaches late stages (Stage 3 or 4), when treatment options are limited and less effective. Demand for early cancer detection is exceptionally high, with 89% of veterinarians likely to add cancer screening to their wellness protocols and 73% of pet owners interested in such a test for their pet.

Source: August 2024 IDEXX investor presentation

The Solution: IDEXX has launched an affordable reference lab panel, starting with lymphoma (which accounts for ~24% of canine cancers and has good therapeutic options if detected early), that can be added to routine wellness screens for as low as $15 (or $60 if it is a standalone test). The panel has a rapid 2-3 day turnaround time and will be expanded over the next three years to cover over 50% of the most prevalent canine cancers.

Market Opportunity & Traction: IDEXX estimates the cancer screening opportunity for at-risk dogs in North America (estimated at 20 million) alone is $1.1 billion, within a broader oncology diagnostics market of ~$2.5 billion. The launch has seen strong initial interest, with over 1,000 unique practices ordering the test within the first month. This innovation not only creates a direct revenue stream but is also expected to help drive more pet owners into clinics for wellness visits (annual exam, routine check-up, vaccination).

Quotes from Tina Hunt, EVP of Global Strategy and Commercial, on the Cancer Dx Opportunity:

“Cancer is a leading cause of mortality in both dogs and cats, and it doesn't get diagnosed early enough…So that early detection is very important. So now to answer your question, Jon, on how we're thinking about it, there are about 13.5 million dogs that we believe have cancer and only about 1/4 of them get diagnosed. And as I mentioned, most of them get diagnosed much later. So that's where the aid in diagnosis is going to be very helpful.”

“There are about 20 million at-risk dogs in just North America alone. So when I say at risk, I'm talking about all dogs above the age of 7, they have a high risk for cancer and certain breeds above the age of 4. So if you put that together, that translates to about $1.1 billion opportunity for us with respect to the cancer screening.”

Production and supply chain

IDEXX employs a hybrid manufacturing model, producing many of its significant products in-house at facilities in the US and Europe, while also relying on third parties for certain instruments and critical components. A key aspect of its strategy involves securing long-term contracts with sole-source suppliers for essential consumables. For example, its agreement with Ortho-Clinical Diagnostics for Catalyst chemistry slides extends through 2044 and includes exclusivity clauses, protecting a critical part of its recurring revenue stream. This strategic management of suppliers, combined with the complexity of manufacturing its own biologic products, creates both a supply chain risk and a significant competitive advantage.

Regarding tariffs, the Company is relatively well-positioned due to its operational structure. With approximately 65% of revenues generated in the US and a largely US-based manufacturing footprint for its core CAG segment, IDEXX has limited exposure, particularly to China, which represents less than 1% of total revenue.

a. Segments

Companion Animal Group (“CAG”)

CAG is the core of IDEXX's business, representing approximately 92% of the Company’s revenue. This segment provides a comprehensive diagnostic and information management ecosystem for veterinarians, operating through two distinct but integrated modalities:

Point-of-Care (POC) Diagnostics: This includes a suite of in-clinic analyzers for chemistry, hematology, and urinalysis, as well as single-use SNAP rapid assay tests. These handheld kits (the rapid assay tests) provide veterinarians with fast, accurate results for various diseases (such as canine heartworm or feline leukemia) in minutes, often without instrumentation.

Reference Laboratory Services: A global network of approximately 80 laboratories where veterinarians can send samples for more complex testing and consultations. While expanding the reference lab network is key to growth, IDEXX notes that new and acquired labs may operate at a loss until they achieve sufficient scale, which can create a temporary drag on operating margins.

These modalities are seamlessly connected through a central hub, the IDEXX VetLab Station (IVLS), which consolidates all in-clinic diagnostic results. The IVLS then sends this data to the cloud-based VetConnect® PLUS software, providing veterinarians with a single, holistic view of a patient’s diagnostic history.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

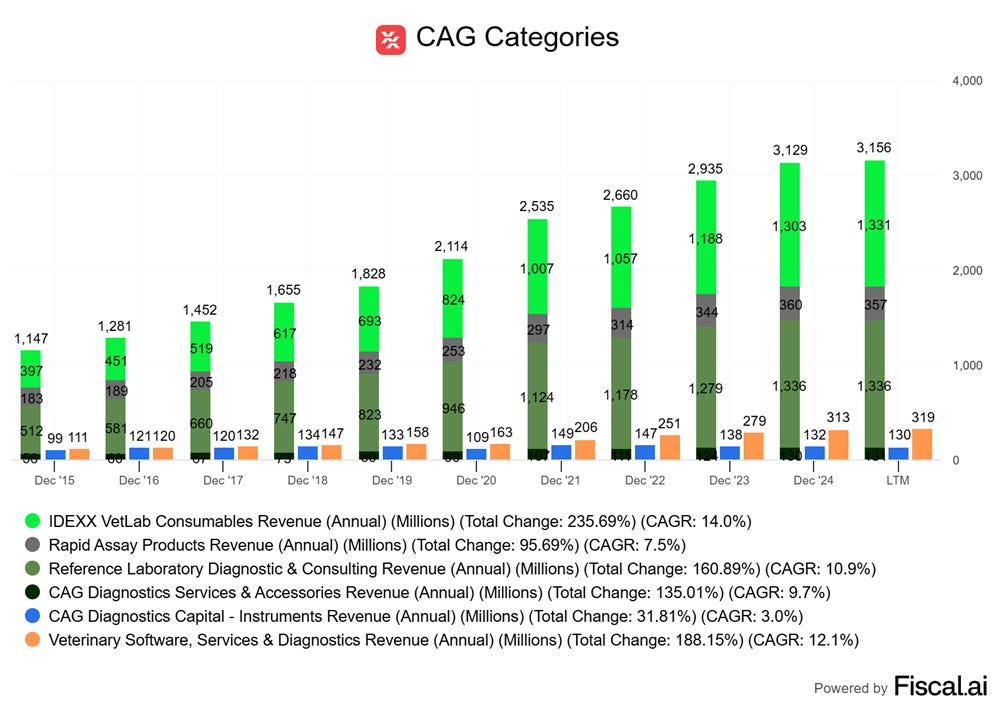

CAG revenue is comprised of six distinct streams as shown in the above chart. The recurring components (defined as items regularly purchased by vets to perform ongoing diagnostic testing), the "blades" of the business model (stacked together in the above chart), are the most significant, with IDEXX VetLab Consumables and Reference Laboratory services being the largest contributors at 34% of sales each.

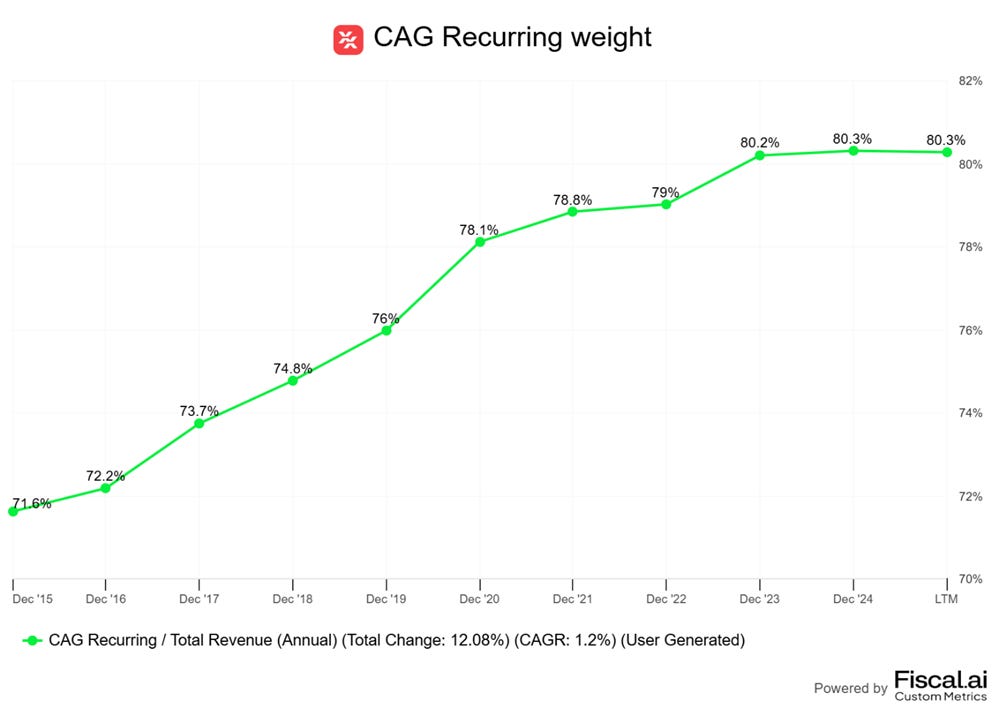

Recurring revenue now accounts for over 80% of total sales compared to 72% in 2015. This was primarily driven by the exceptional growth in high-margin consumables, which delivered a 14% CAGR over the period, reaching $1.3 billion in sales and a share of revenue of 34% Vs 25% in 2015. In contrast, instrument sales, the non-recurring "razors", were the slowest growth driver with just a 3% CAGR, reaching sales of $130 million.

In the most recent quarter, the CAG segment delivered organic growth of 4.4%, led by standout performance from IDEXX VetLab consumables (+10.5%) and the Veterinary Software and Services business (+7.5%).

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

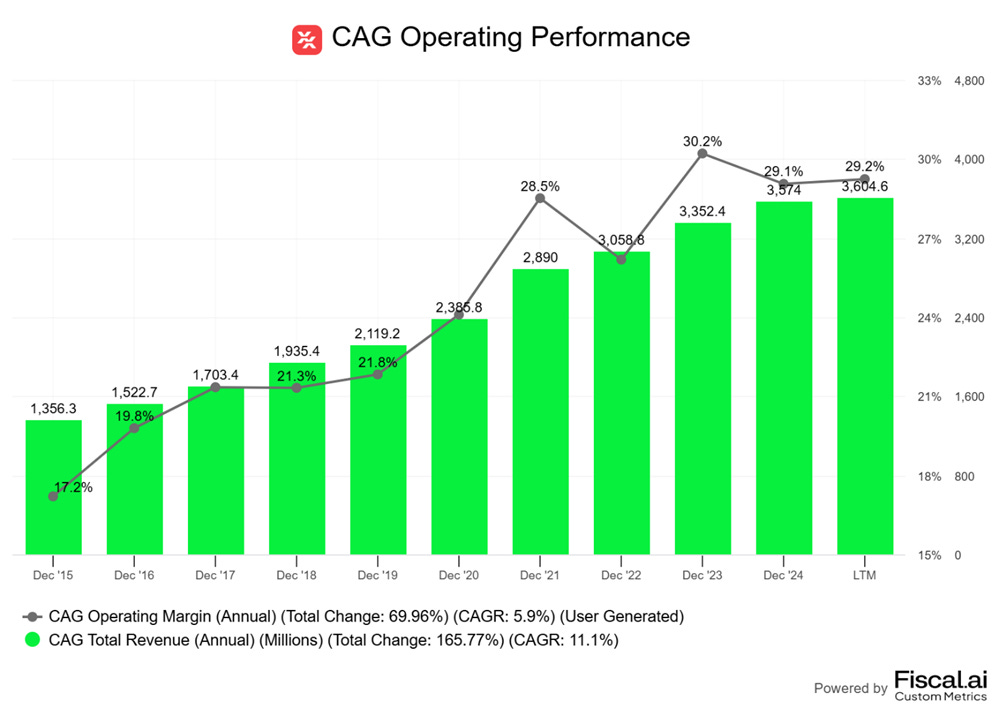

The importance of this mix shift cannot be overlooked. While instrument sales grow slowly, they enable the predictable, high-margin recurring revenue from consumables and services. This favorable shift, boosted by the high-margin Veterinary Software business, has driven a substantial increase in the company's operating profitability, from 17% in 2015 to nearly 31% by 2024 (when adjusted for a one-off litigation accrual – the case is closed now).

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

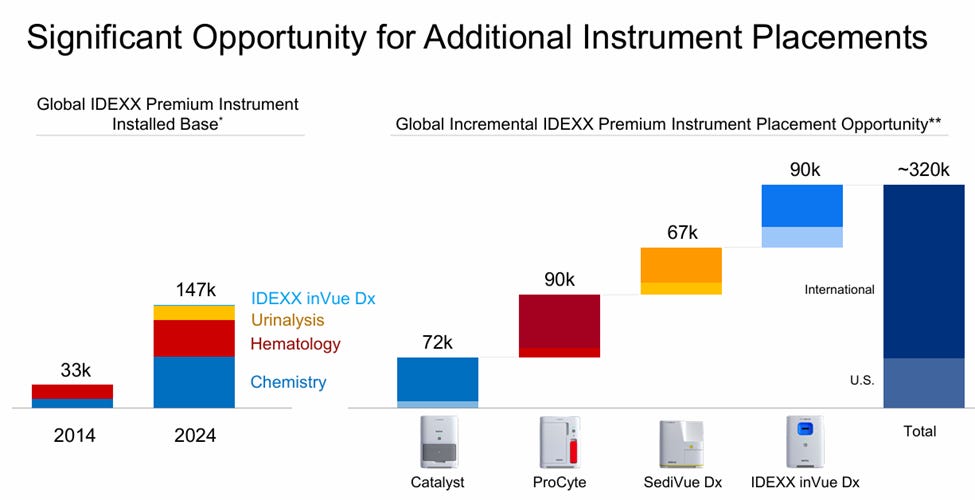

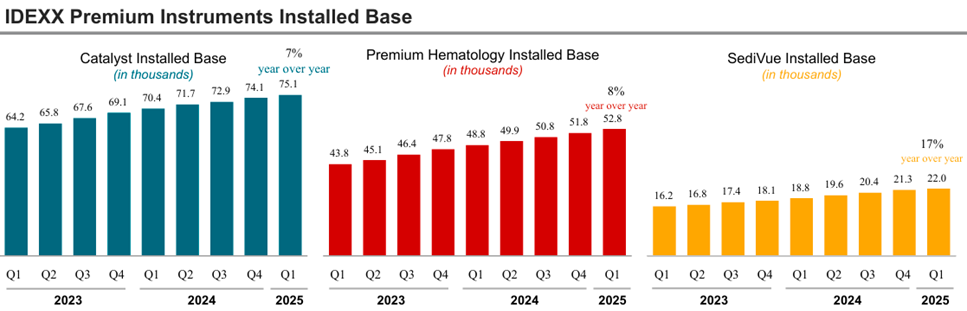

The foundation of this recurring revenue stream is the Company's large and growing premium instrument installed base. The growing premium installed base indicates strong demand from veterinarians for in-house diagnostics that improve patient care and clinical decision-making. As of the first quarter of 2025, this installed base includes:

Catalyst Analyzers: 75,100 units (+7% YoY), which are fundamental to in-clinic blood chemistry analysis.

Premium Hematology Analyzers: Over 52,000 units (+8% YoY), including the ProCyte Dx and ProCyte One, providing crucial information on patient blood cells.

SediVue Dx Analyzers: Over 22,000 units (+17% YoY), showing the most rapid expansion by automating urine sediment analysis.

Source: Q1’25 IDEXX Earnings Snapshot

Source: March 2025 IDEXX presentation

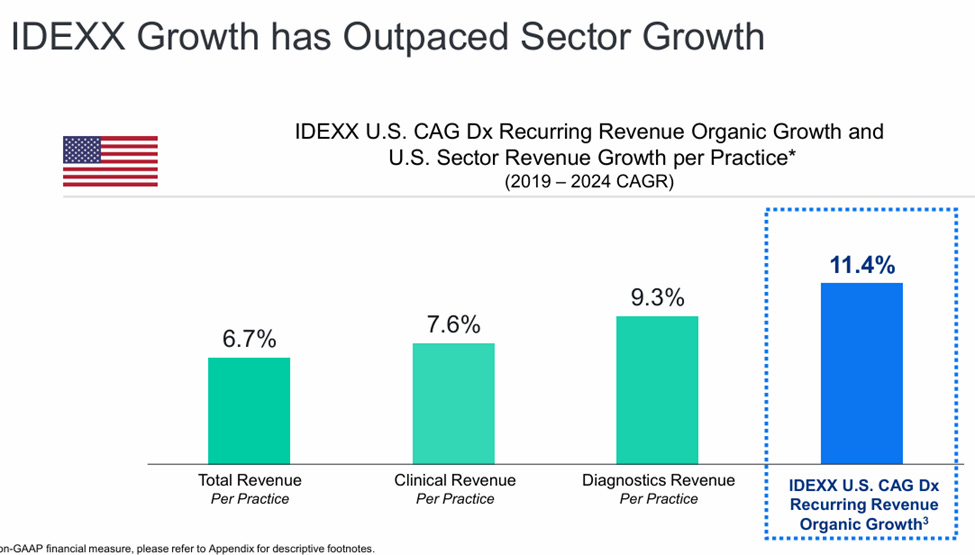

This expansion of its installed base, combined with price realization and increased utilization, allowed IDEXX to outpace the annual growth of the broader veterinary sector by over 200 basis points over the past 5 years. The Company has achieved this despite recent headwinds in US clinic visit numbers, underscoring the value of its differentiated and integrated solutions.

Source: March 2025 IDEXX presentation

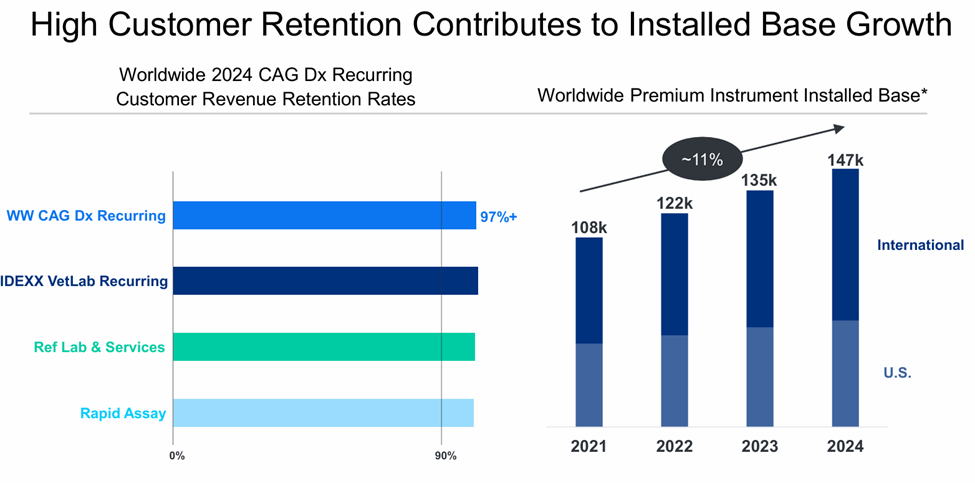

The success and stickiness of this model are supported by an exceptionally high customer retention rate, consistently reported in the 97-99% range. This retention rate, is supported by the Company's operational excellence, including its ability to maintain over 99% product availability and 98% on-time delivery for reference lab results.

Source: March 2025 IDEXX presentation

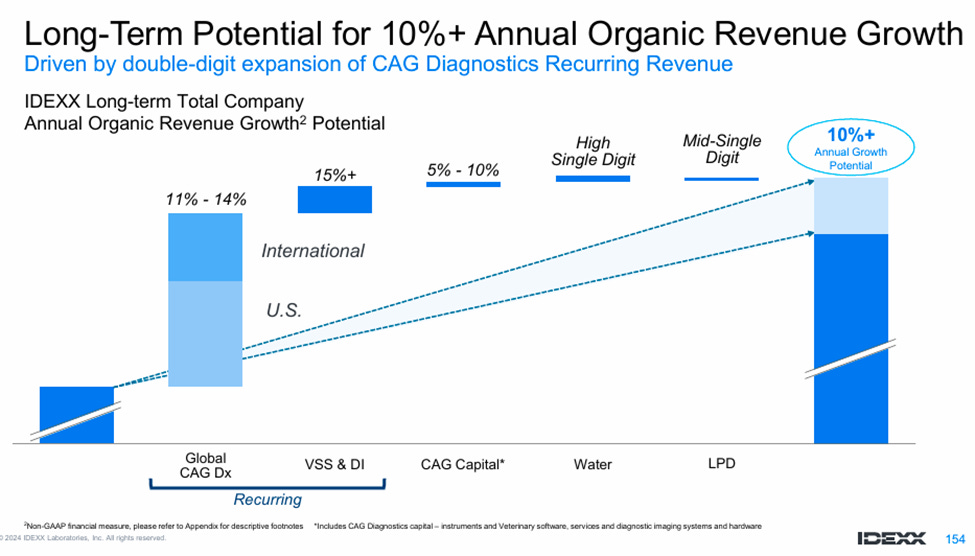

Looking ahead, the outlook for the CAG segment is strong, underpinned by a massive, underserved global addressable market estimated at over $45 billion. To capitalize on this, IDEXX is targeting 10%+ annual organic revenue growth, driven by the double-digit expansion of its recurring CAG Diagnostics revenue. This growth is expected to be fueled by three key drivers: new innovation platforms like inVue Dx and Cancer Dx tapping into multi-billion dollar opportunities; a core strategy to increase test utilization through veterinarian education about best medical practices; and the expected long-term growth in clinical visits driven by favorable pet ownership demographics and the aging of the large post-COVID pet population.

However, the Company must navigate a veterinary industry that is becoming increasingly consolidated. The growing scale of corporate hospital groups gives them greater buying power, which could impact profitability and supplier relationships over the long term.

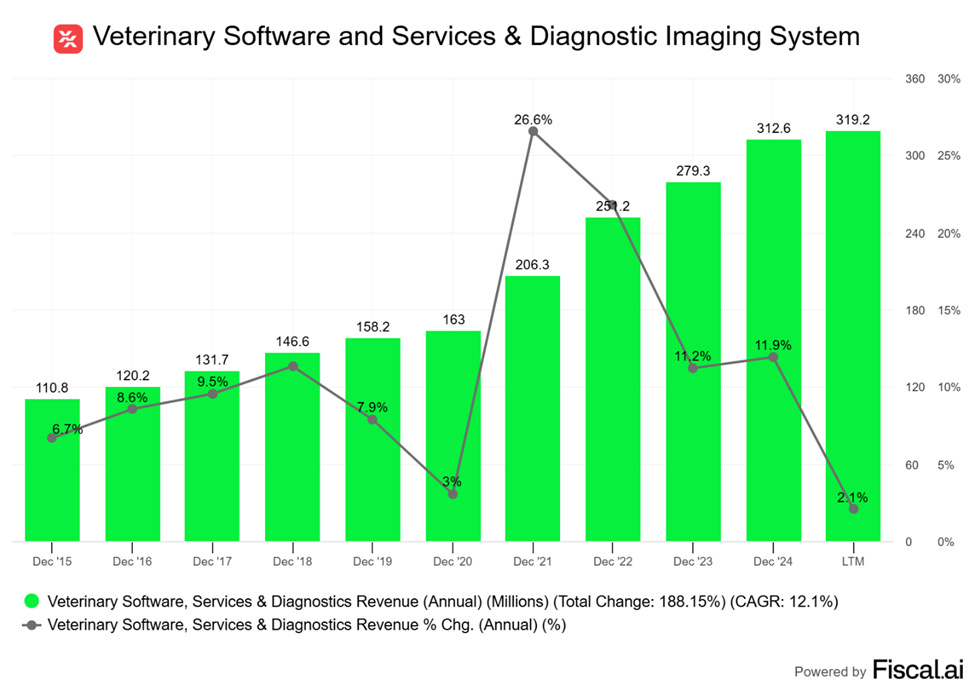

Veterinary Software and Services & Diagnostic Imaging Systems

This is critical and high-growth component of the CAG ecosystem, providing the digital infrastructure that runs the modern veterinary clinic. Its core offerings are Practice Information Management Systems (PIMS), which manage key functions like electronic health records, scheduling, billing, and inventory. The portfolio includes the on-premise, highly customizable Cornerstone software and a suite of cloud-based platforms like the user-friendly ezyVet, Neo and the VetConnect PLUS. These systems are supplemented by a host of integrated tools for client communication (Vello), workflow management (VetRadar), and diagnostic image archiving (IDEXX Web PACS) creating a sticky software suite.

To support these solutions, post-contract support provides customers with access to technical assistance as needed through call centers and online portals. In addition, the segment includes diagnostic imaging systems, like the IDEXX ImageVue DR series, which capture digital radiographs to replace the traditional chemical-based x-ray film process.

Source: IDEXX August 2024 Investor Presentation

This segment accounts for approximately 8% of total Company sales and, with a 12.1% CAGR from 2015-TTM, is the second-fastest growing part of the business behind VetLab consumables. It generates relatively high margins from its subscription-based products, with recurring revenue comprising 80% of the segment's sales (the rest comprises of hardware and digital imaging system).

As CEO, Jay Mazelsky noted: “IDEXX software helps clinics unlock the full potential of their diagnostics, improve client engagement and enhance operational efficiency. This quarter, we saw strong performance across our practice information management system as well as pet owner engagement tools like Vello. Our ezyVet and Neo platforms continue to grow as we deliver double-digit placement growth in our leading cloud-native PIMS during the quarter with accelerated momentum.”

Growth is driven by a dual strategy of organic innovation and strategic acquisitions, as the majority of the Company's M&A activity is in software. Major acquisitions like ezyVet (2021) and Greenline (2024) have been significant contributors to growth. For example, these acquisitions boosted sales by 10.5% in 2021 (out of 26.6% total growth), 7.9% in 2022 (out of 21.8% total growth), and 4.7% in 2024 (out of 11.9% total growth).

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

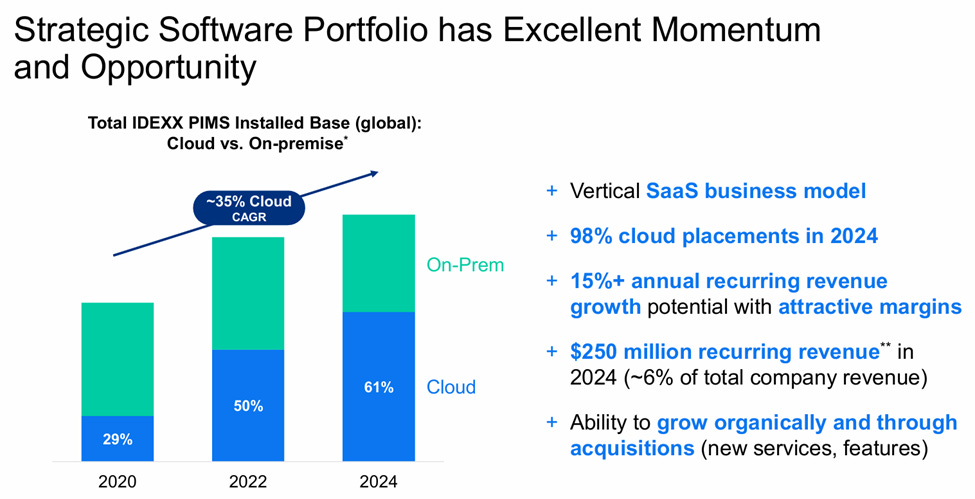

The business has excellent momentum driven by the rapid shift to the cloud, with 61% of the PIMS installed base now being cloud-native (compared to 29% in 2020) and 98% of new placements in 2024 being cloud-based systems. Meanwhile, recent performance has been strong, with double-digit placement growth in leading cloud PIMS and Vello users (introduced in 2024) growing over 20% in Q1 2025 from the prior quarter.

Source: March 2025 IDEXX presentation

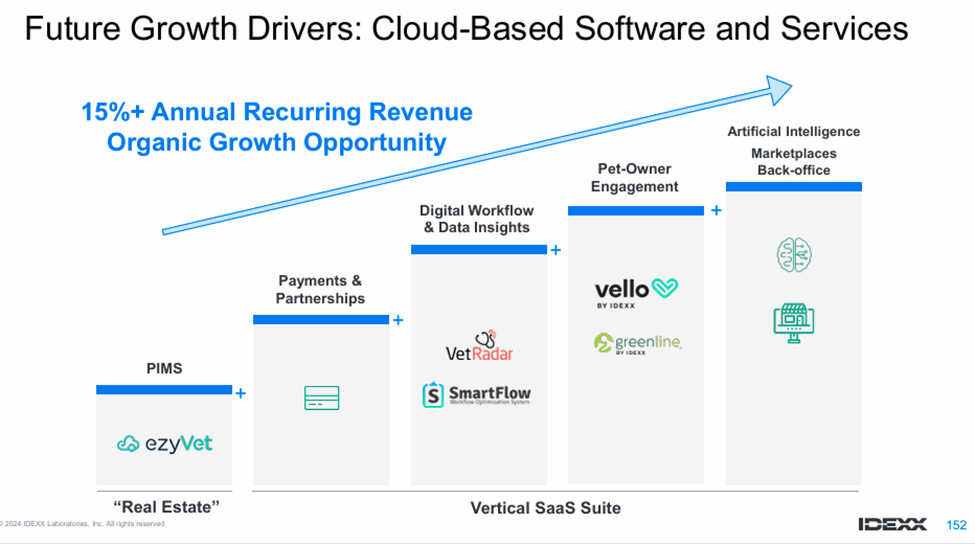

The software portfolio is a key strategic focus and the Company is targeting 15%+ annual recurring revenue growth from this segment. The overarching strategy is to continue driving cloud adoption and leveraging the fully integrated software ecosystem to deepen the competitive moat, making it indispensable to a clinic's daily workflow.

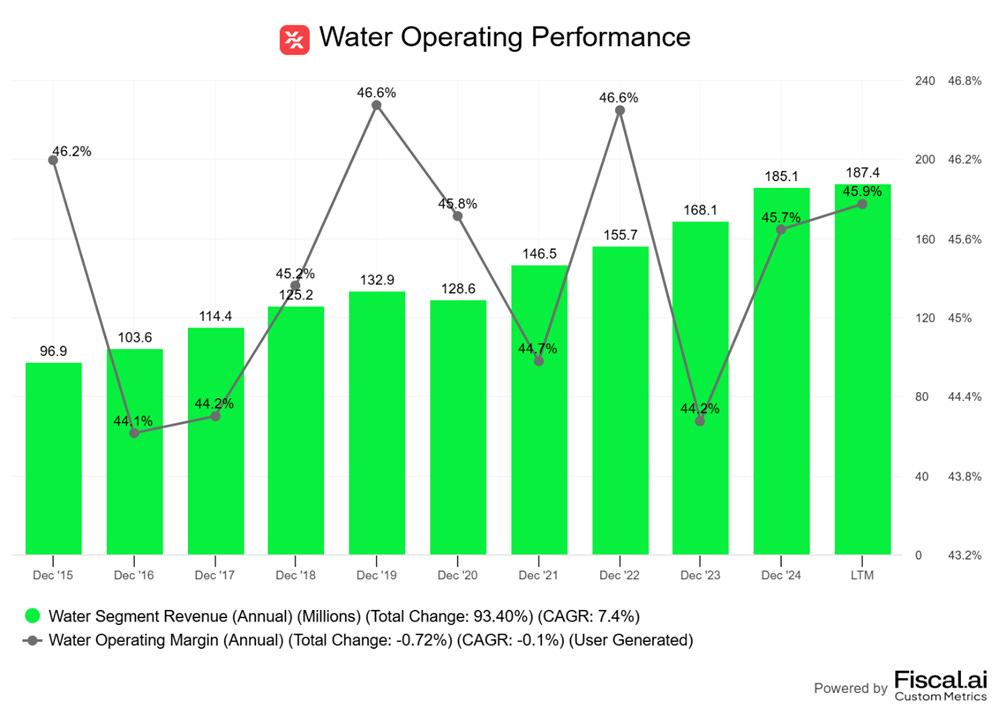

Water quality products (“Water”)

This segment provides innovative testing solutions for the detection and quantification of various microbiological parameters in water. Its principal products, like the Colilert tests, are used by government laboratories, water utilities, and private certified labs to ensure the safety of drinking water, bottled water, and water used in production processes.

The Water segment, which accounts for approximately 5% of total sales, is the Company's most profitable with an operating margin of around 46%, significantly higher than the CAG segment's margin (+30%). It has grown at a 7.4% CAGR since 2015 and continued its strong performance into the most recent quarter, delivering 7% organic revenue growth in Q1 2025 driven by a combination of price increases and higher testing volumes.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

The future growth in the segment is dependent on the Company's ability to increase international sales and broaden its product line. As the market is largely driven by regulation, it provides a stable, albeit smaller, source of revenue and profit for the company.

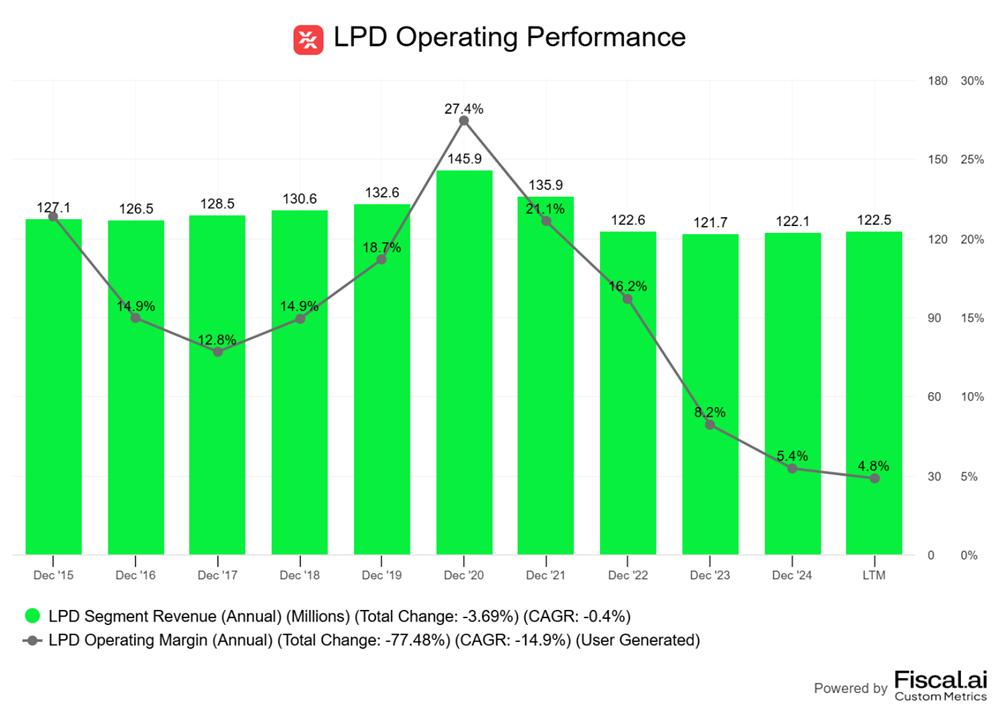

Livestock, Poultry and Dairy (“LPD”)

The LPD segment provides diagnostic tests, services, and related instrumentation used to manage the health of herd animals and to ensure the quality and safety of milk from contaminants like antibiotic residues. Its customers are primarily government and private laboratories that provide testing services to producers and livestock veterinarians.

LPD is the smallest segment, accounting for only 3% of total sales and posting a negative CAGR of -0.4% since 2015. It operates at a near break-even level of profitability, with a 5.7% operating margin, a significant decline from the double-digit levels observed in the past. Demand can be volatile, influenced by specific disease outbreaks or government-funded programs, though the segment did grow 4% organically in Q1 2025.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Given its small scale and low profitability, this segment is not considered a primary long-term growth driver for IDEXX, especially when compared to the significant opportunities within the Companion Animal Group and its software portfolio. This raises questions about its long-term strategic fit within the company.

Geographies

IDEXX's business is centered in the US, which generates 65% of total revenue, while international markets account for the remaining 35%. Outside of the US, the largest markets are Germany (4.5%), Canada (3.9%), and the U.K. (3.5%). The importance of international sales varies significantly by segment, accounting for only 33% of CAG revenue but a substantial 82% of LPD and 48% of Water revenues.

While the US market is more profitable due to higher spending by US pet owners, the international segment grew faster in 2024 (7.5% vs 5.9% for the US) and in Q1 2025, as international CAG recurring revenue grew at a robust 8.5% organically, well ahead of the 3% growth in the US market (affected by the 2.6% drop in clinical visits), driven by strong new business gains and a rapid expansion of its premium instrument installed base.

3. Management

a. Culture

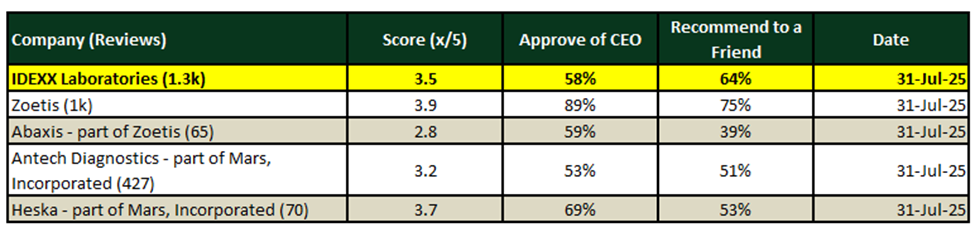

IDEXX's company culture appears to be solid and improving, with no significant warning signs. The Company's Glassdoor rating is 3.5, with 64% of employees recommending it to a friend and 58% approving of the CEO. While these metrics are below competitor Zoetis, they are higher than Antech Diagnostics.

Source: Glassdoor

More importantly, internal metrics point to a strengthening culture. The Company's overall voluntary employee turnover rate has shown a clear downward trend, declining from 13.3% in 2022 to 8.5% in 2024. This improvement may be partially attributed to initiatives like balancing reference lab shifts to reduce employee overtime and burnout.

Perhaps the strongest indicator is that IDEXX achieved an employee Net Promoter Score that was above the 90th percentile for all employers, according to data from its third-party engagement platform.

b. Leadership

IDEXX is led by a stable and experienced management team, with a strong culture of promoting leaders from within the organization.

CEO: Jonathan J. Mazelsky was appointed President and CEO in October 2019, having been with IDEXX since 2012, previously serving as Executive Vice President for the North American CAG business. The transition was unexpected, following a tragic cycling accident that resulted in a paralyzing spinal cord injury to the former long-serving CEO, Jonathan Ayers. However, the Board's well-planned emergency succession protocols enabled a smooth and seamless leadership transition without disrupting the business.

CFO: The Company has also managed a smooth CFO transition in 2025. The retiring CFO, Brian McKeon, was succeeded by Andrew Emerson, effective March 1, 2025. This was another promotion from within, as Mr. Emerson had been with IDEXX since 2015, leading finance for the critical CAG business and overseeing corporate finance functions since 2020.

The broader executive team reflects a culture of commitment and long tenures, with many members having joined IDEXX over a decade ago, including one executive who has been with IDEXX since 1999.

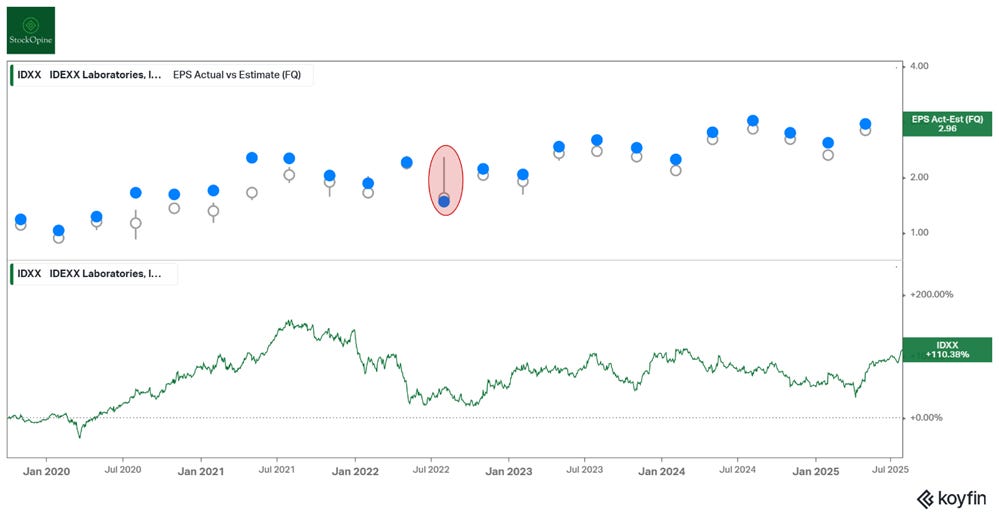

Under the leadership of CEO Jonathan Mazelsky, the Company has executed well, missing earnings consensus just once while delivering a total shareholder return of approximately 110%, translating to a CAGR of around 13.4%.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers, premium members can benefit from a 3-month free trial)

c. Compensation

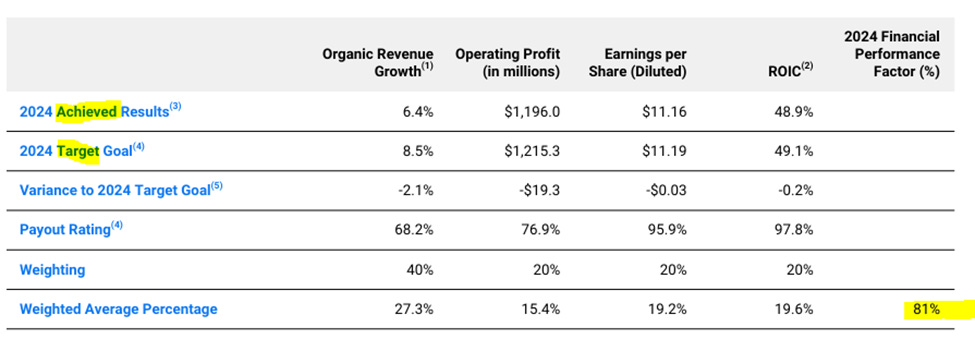

IDEXX’s executive compensation is heavily weighted towards performance, creating alignment with shareholder interests. It consists of a base salary, an annual cash bonus, and long-term equity awards.

The annual bonus is tied to a blend of financial metrics (60% weight), including organic revenue growth, operating profit, EPS, and ROIC, and non-financial goals (40% weight). The Board sets challenging targets that are not "lowballed", as evidenced by the 81% achievement rate against the financial goals in 2024. These targets are dynamic. For instance, following the strong performance in 2023, 2024 targets were raised for key metrics like organic growth (to 8.5% from a 7.8% target in 2023) and ROIC (to 49.1% from 44.5%).

Source: 2024 Proxy Statement

Long-term incentives consist of a mix of stock options and time-based RSUs, both of which vest in equal installments over a four-year period, and Performance-Based Stock Units (PSUs). The PSU vesting is tied to achieving multi-year organic growth and operating profit targets over a three-year performance period, ensuring executives are rewarded for long-term value creation.

In line with other US companies, IDEXX’s compensation program is heavily weighted towards "at-risk" pay to ensure alignment between leadership and shareholder interests. In 2024, 91% of the CEO’s and 84% of other senior executives' target compensation was variable and dependent on performance.

d. Ownership

While directors in aggregate own just 0.98%, leadership’s financial interests are aligned with shareholders through substantial direct holdings relative to their salaries.

The CEO, Jonathan Mazelsky, directly owns shares worth over $45 million, and his total potential ownership, including exercisable options, is valued at approximately $190 million. This represents a value far exceeding the Company's requirement to hold 10 times his base salary of $1.15 million. Additionally, the former long-serving CEO, Jonathan Ayers, maintains a substantial position, holding shares worth over $320 million (approximately 0.7% of the Company).

4. Industry

The companion animal health market is underpinned by powerful and enduring secular trends. These forces are reshaping consumer spending and creating a resilient, high-growth environment for industry leaders like IDEXX.

a. Key Macro & Demographic Trends

The “Humanization” of Pets: Owners increasingly view their pets as integral family members. This emotional bond translates into a higher willingness to spend on premium products. This trend is clearly visible in purchasing habits; after a brief decline in 2023, premium pet food purchases regained momentum in 2024. According to the APPA, 41% of dog owners and 38% of cat owners purchased premium food in 2024, representing a 5% and 9% increase from the previous year, respectively.

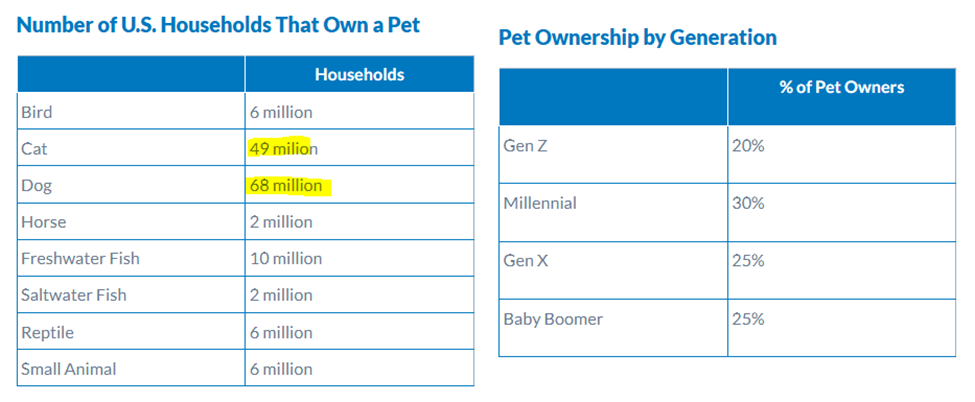

The Pet Population Boom & Generational Shift: The total US pet population is expanding rapidly, with 94 million households now owning at least one pet, a significant increase from 82 million in 2023. This includes 68 million households with a dog and a fast-growing 49 million with a cat. This growth is largely driven by younger generations, with Gen Z and Millennials now the dominant pet-owning cohorts. These younger owners are also more likely to own multiple pets; a remarkable 70% of Gen Z pet owners have two or more pets. The deep integration of pets into daily life is further evidenced by behavioral trends, such as the increasing number of owners traveling with their dogs and a strong desire for dog-friendly workplaces.

Source: The American Pet Products Association (APPA) Releases 2025 State of the Industry Report

The Economics of Companionship: This trend is occurring alongside a consistent decline in US fertility rates, which fell from 2.12 children per woman in 2007 to a low of 1.62 in 2023 (replacement factor is estimated at 2.1). A key factor in this shift is cost as raising a child to age 18 in the US averages over $300,000, while annual pet care is significantly lower at around $1,500-$1,800. For younger generations, pets offer companionship without the same long-term financial commitment, a trend that is reshaping consumer spending patterns.

Pets Are Living Longer: Advances in veterinary care are having a profound impact. The average lifespan of cats has increased by 18% (to 14.4 years) and dogs by 16% (to 13.4 years) since 2010. This is a powerful growth driver, as older pets utilize significantly more healthcare and diagnostics.

Source: IDEXX March 2025 presentation

b. Market Size & Forecasts

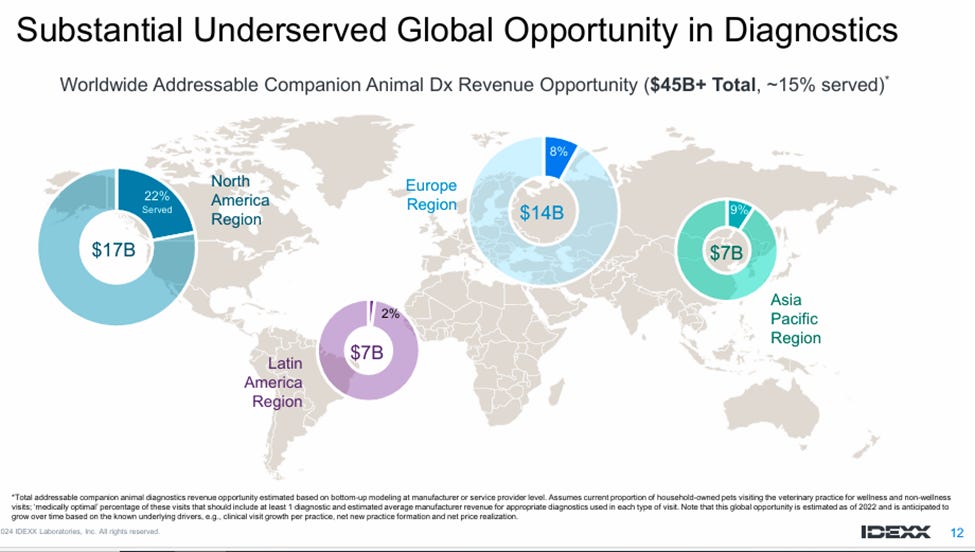

The global addressable market for companion animal diagnostics is massive, estimated by IDEXX at over $45 billion. The most compelling aspect of this market is that it remains significantly underserved, with only ~15% of the total opportunity currently being addressed.

Source: IDEXX August 2024 Investor Day

While the industry has faced a headwind of declining clinical visit numbers over the past three years (down ~2.6% in the latest quarter), this is being offset by an increase in the quality and value per visit, driven by higher diagnostic utilization and a continued willingness from pet owners to invest in innovative care.

That being said, the key long-term growth factors for the industry remain clear:

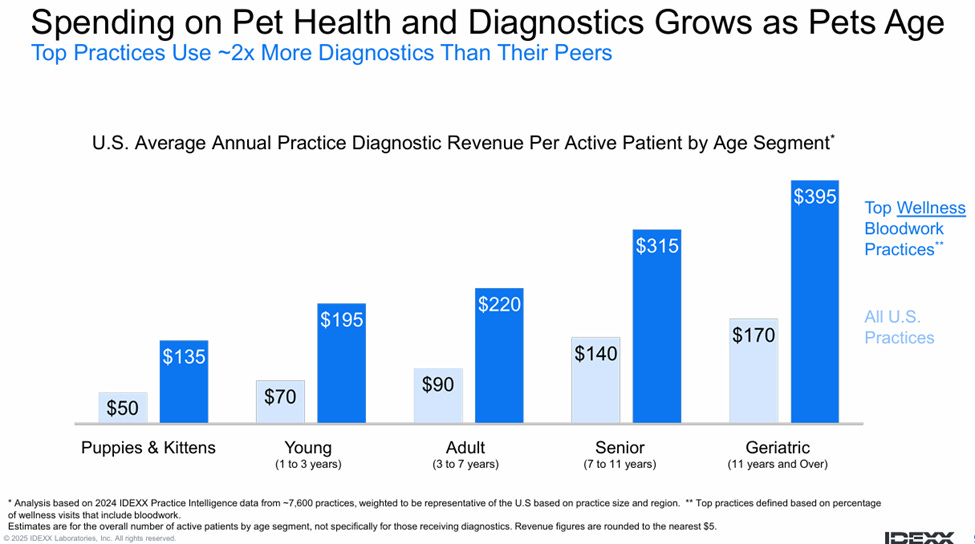

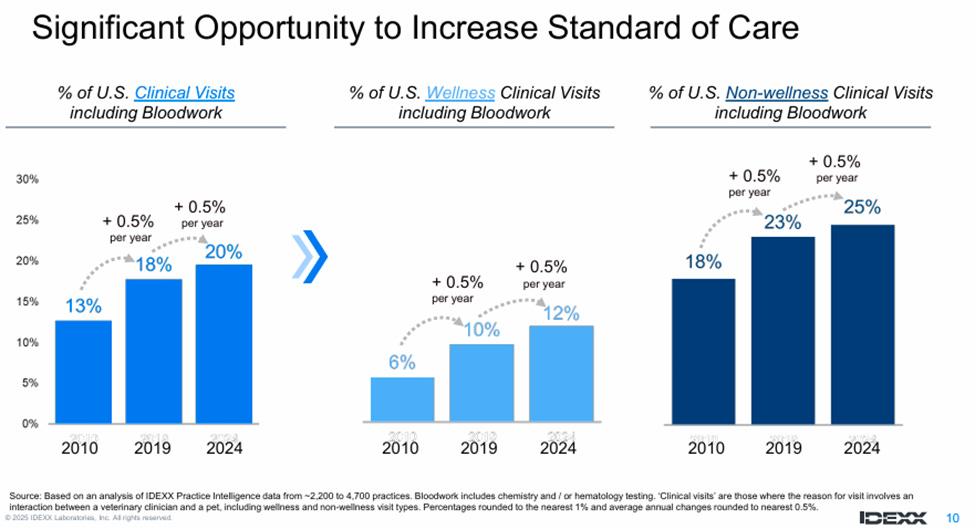

Increasing Diagnostic Utilization: A primary growth lever is educating veterinarians to increase the frequency of diagnostic testing. Currently, only about 12% of US clinical wellness visits include bloodwork, though “top practices” that standardize diagnostics use them more than twice as often as the average practice, uncovering underlying issues in 25-35% of cases.

Source: IDEXX March 2025 investor presentation

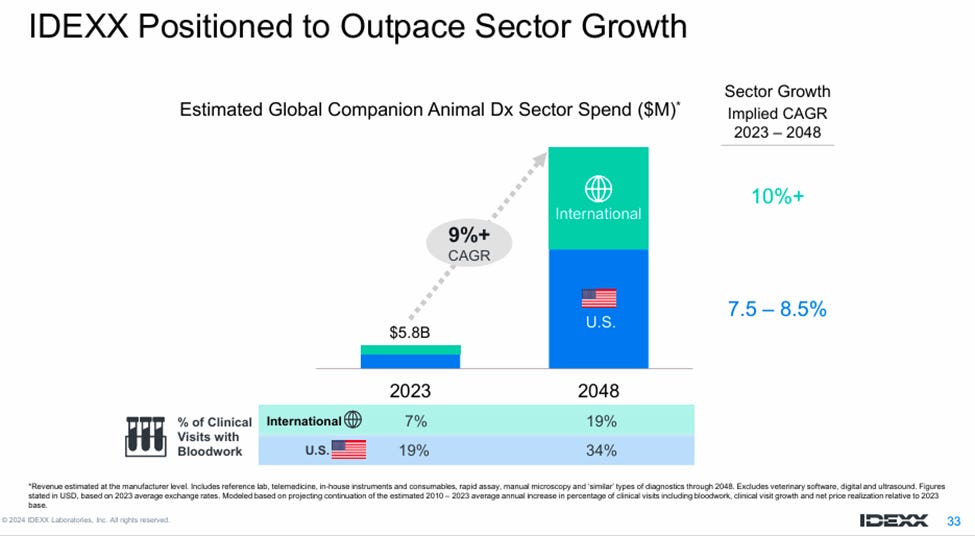

International Expansion: Market penetration is even lower outside of North America (22% served), with Europe at just 8% and Latin America at 2%. This presents a vast runway for growth, with the international market expected to grow at a faster rate (10%+) than the U.S. (8%).

Source: IDEXX March 2025 presentation

Continued Innovation: New testing capabilities and menu expansions, such as those in oncology, create new reasons for testing and drive higher spending per visit, ensuring that the quality and value of each visit continue to improve.

c. Competition Landscape

While many smaller regional players exist or subsidiaries of large conglomerates like Thermo Fisher, the primary competition for the core CAG segment comes from two global companies:

1. Zoetis Inc. (NYSE: ZTS): Zoetis is a dominant force in animal health, but primarily in pharmaceuticals and vaccines. Diagnostics represents a small and less strategic portion of its business, accounting for just 4.2% of its total revenue in 2024.

Scale Comparison: Zoetis's diagnostics revenue was approximately $386 million in 2024, which is minimal compared to IDEXX's CAG revenue of $3.6 billion. This highlights IDEXX's clear leadership and focused expertise in the diagnostics market.

Growth: While Zoetis's diagnostics growth was strong in Q1 2025 at 25.6%, its full-year growth in 2024 and 2023 was 2.7% and 6.5%, respectively, showing a more volatile trajectory compared to IDEXX's consistent expansion of 10% in 2023 and 7% in 2024.

2. Mars, Incorporated (Private): Mars is a strong competitor through its aggressive acquisition strategy, primarily via its Antech Diagnostics and Heska brands. As Mars is a private company, direct financial comparisons are unavailable, but analysis of its components reveals IDEXX's superior scale.

Antech Diagnostics: Antech is a strong competitor, particularly in the reference laboratory space, with a US network of approximately 70 labs, which is larger than IDEXX's. Since Antech's global financials are private, an estimate was derived from its UK subsidiary's reported 2023 sales of £24.7 million (comprised of £3.3M from the UK, £9.9M from the rest of the EU, and £11.6M from the rest of the world). Applying the 3.5% weight of IDEXX's own UK business as a conservative proxy suggests Antech's total global revenue is approximately $932 million (£706 converted to USD), still smaller than IDEXX's CAG segment.

Heska: Prior to its acquisition by Mars, Heska's financials demonstrated the gap between IDEXX and smaller competitors. In 2022, Heska generated $257 million in revenue with just 1.4% growth, compared to IDEXX's CAG revenue of $3 billion with 6% growth in the same year.

While IDEXX faces competition in specific areas, such as from Covetrus in the software market, its primary challengers in the core diagnostics space are Zoetis and the expanding Mars portfolio. However, IDEXX’s scale, higher growth rate, and deeply integrated “razor-and-blade” ecosystem solidify its position as the dominant leader.

5. Financial Analysis

a. Performance

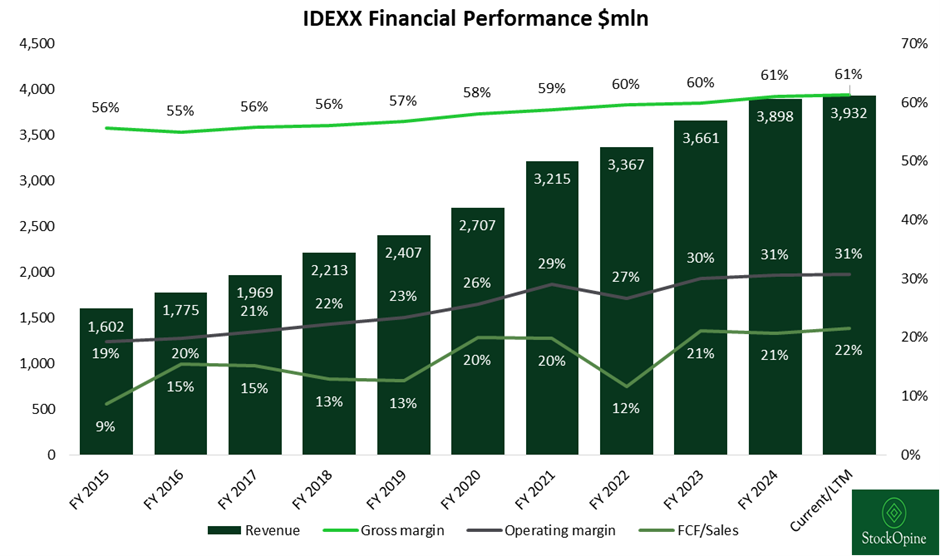

From FY15 to Q1’25 TTM, IDEXX delivered a 10.2% revenue CAGR, reaching $3.9 billion. Gross profit grew at an 11.4% CAGR, with margins improving from 55.6% to 61.3% while operating income rose from $308 million to $1.2 billion, reflecting a 15.9% CAGR and a 30.7% operating margin. Over the past decade, free cash flow margin averaged 15.8%, with FY24 FCF at $808 million or 20.7% of revenue.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers), StockOpine analysis

IDEXX has a track record of delivering strong and profitable growth. While the Company strategically acquires reference labs and software companies, its growth has been primarily organic, driven by the powerful recurring revenue engine of the CAG segment.

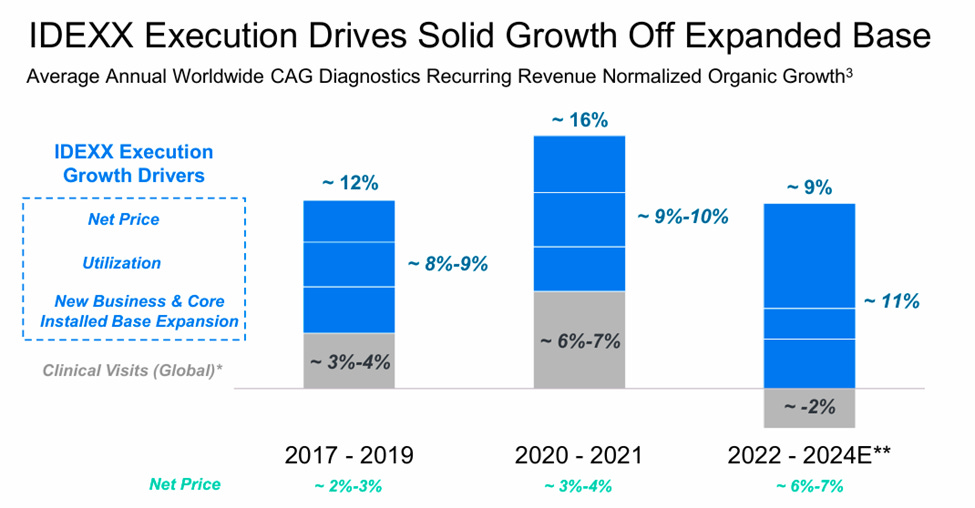

Organic growth has been a dynamic interplay of several key drivers, with their respective importance shifting over different periods:

Pre-COVID (2017-2019): Growth was balanced, with net price increases of 2-3% complemented by a 3-4% growth in clinical visits, alongside benefits from increased test utilization and the expansion of the instrument installed base.

COVID-Era (2020-2021): This period saw an exponential increase in clinical visits (growing 6-7%) as pet ownership surged. This volume growth, combined with continued price increases of 3-4%, had a profound impact on revenue.

Post-COVID (2022-2024): As clinical visit numbers normalized and declined, price realization became the most important driver of growth, contributing 6-7% annually. That being said there is an optimism for a return to growth at 3% for clinical visits (we touch this on the outlook).

In the most recent quarter (Q1 2025), revenue growth was comprised of a 4% contribution from price and a 2% contribution from volume.

Source: IDEXX August 2024 Investor presentation

Gross margins have consistently expanded, rising from 55.6% in FY15 to 61% in FY24, and reaching 62.4% in Q1'25. This improvement is a direct result of the favorable mix shift towards high-margin recurring CAG Diagnostics revenue (especially VetLab consumables) and effective price realization.

The strength at the gross profit level has translated directly into higher operating margins, which grew steadily from 19% in 2015 to 30.5% in 2024. The most recent quarter's operating margin stood at 31.7% (or 30.8% when adjusted for a one-off litigation accrual reversal), demonstrating a clear and sustainable trend of profitable growth.

Free cash flow margins have generally moved in line with the growing operating profitability, expanding from 8.7% of sales in 2015 to 20.7% in 2024. The only recent exception was in 2022, which saw a temporary negative impact from inventory management that was quickly resolved the following year.

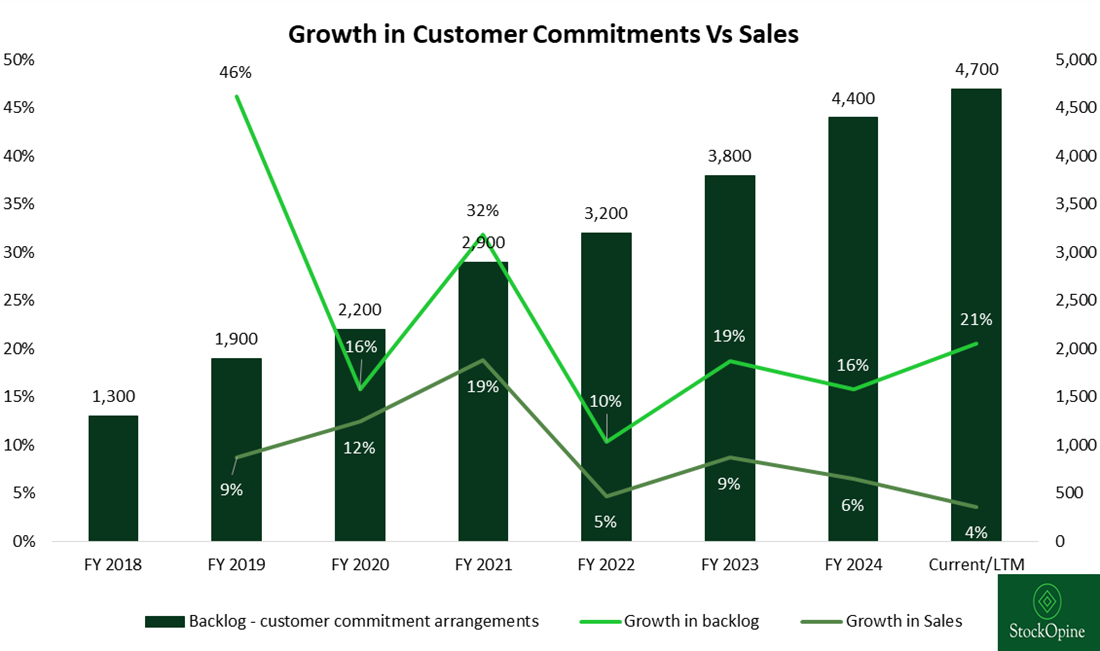

Backlog: A Leading Indicator of Future Growth

A key metric for understanding IDEXX's future growth is its backlog of committed future revenue from multi-year customer arrangements. As of Q1 2025, the Company estimated this backlog to be approximately $4.7 billion.

This backlog has been growing faster than current sales, which is a strong positive indicator of the accelerating momentum. This is because a multi-year contract is added to the backlog in its entirety upfront, while revenue is only recognized annually. The rapid growth of this figure compared to current sales is driven by several factors:

Successful placement of new instruments into clinics coming with a new multiyear agreement.

High rates of customer contract renewals and extensions, often at higher values and possibly at longer terms.

A shift towards more advanced instruments that carry higher minimum purchase commitments.

As CFO Andrew Emerson confirmed, recent large corporate contracts were both “expansions and extensions”, increasing the duration of relationships and the breadth of services used.

The fact that this backlog is growing faster than recognized sales indicates that future revenue is becoming more predictable and secure, the instrument installed base is expanding successfully, and customer loyalty is exceptionally high.

Source: IDEXX financials, StockOpine analysis

b. Financial position

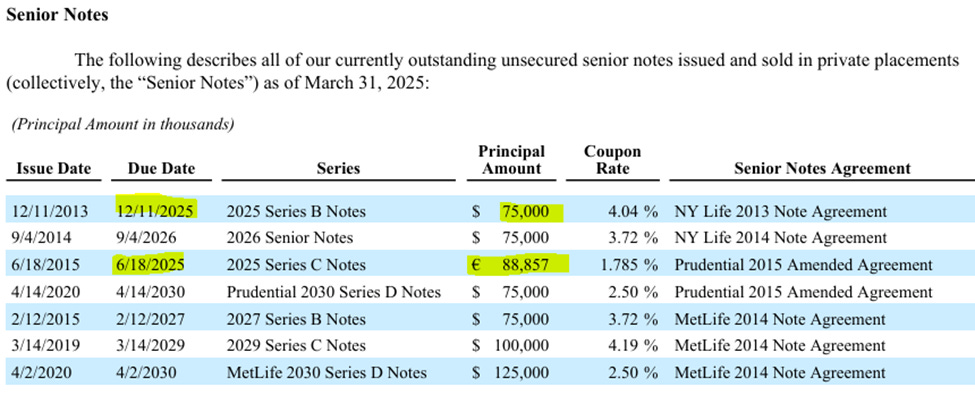

IDEXX maintains a flexible financial position. As of Q1 2025, the Company's balance sheet included $164 million in cash and short-term investments against approximately $1.1 billion in total debt and lease liabilities. While IDEXX operates with a net debt position, its leverage is very manageable.

The debt is well within its covenant requirements as its debt to adjusted EBITDA ratio stood at a safe 0.58x in Q1 2025, far below the 3.5x maximum. Furthermore, IDEXX has significant liquidity, with over $928 million in remaining borrowing availability under its credit facility. The Company’s strong free cash flow, which reached $808 million in 2024, provides ample capacity to easily cover all debt maturities falling due over the next three years, and management retains the flexibility to reduce its share buyback program if needed to prioritize deleveraging.

Source: Q1’25 10Q

c. Capital allocation

IDEXX has a clear and shareholder-friendly capital allocation strategy. Between fiscal years 2015 and 2024, it generated approximately $5.6 billion in operating cash flow. Of that, it allocated $1.1 billion (20%) to net capital expenditures, $363 million (6.5%) to acquisitions, and the vast majority of $4.4 billion (79%) to share repurchases. This approach emphasizes reinvestment in the business while delivering consistent shareholder returns, primarily via buybacks, which have reduced the total share count by 10.3% since 2015.

The Company has been particularly active and opportunistic with its buyback program. For example, it accelerated repurchases in Q1 2025, spending $400.9 million at an average price of ~$439.7 per share. In hindsight, this proved to be a timely decision, as the share price increased by 25% in the months that followed. After a slowdown in 2023 to prioritize debt repayment, IDEXX guided for approximately $1.5 billion in share repurchases for 2025 with 5.2 million shares available as of 31 March 2025.

Acquisitions represent a smaller but important part of IDEXX's capital allocation strategy. These are bolt-on acquisitions designed to enhance existing business lines, particularly in software. The vast majority of M&A spending has been focused on bolstering the technology portfolio, with key examples including the acquisitions of ezyVet (2021) and Greenline (2024). IDEXX has a good track record of integrating these purchases, with no goodwill impairments recorded in recent years.

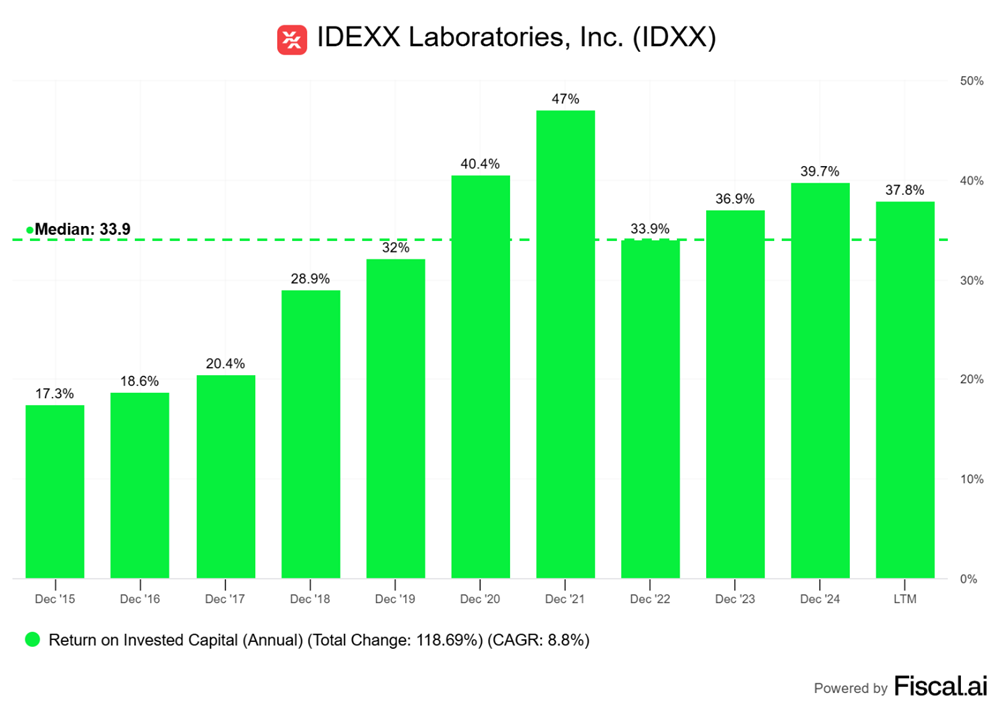

The effectiveness of this capital efficient strategy is demonstrated by IDEXX’s impressive returns. Return on Invested Capital (ROIC) has expanded significantly, rising from 17.3% in 2015 to 39.7% in 2024.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

d. Outlook

IDEXX, in Q1’25, has revised its outlook for 2025, adjusting reported revenue and operating margin due to favorable foreign exchange rates and a litigation accrual adjustment. The guidance is based on the assumption that the recent trend of a ~2% decline in US clinical visits will persist for the full year.

Key updated targets for 2025 include:

Revenue: $4.095 billion - $4.210 billion, representing 6% - 9% organic growth (5-8% reported).

CAG Diagnostics Recurring Revenue: 5% - 8% organic growth (4-7% reported), supported by an anticipated full-year price realization of 4% to 4.5%.

Operating Margin: 31.1% - 31.6%, maintaining its outlook for 30 - 80 basis points of comparable operating profit margin expansion, even after absorbing headwinds from tariffs and lower-margin inVue Dx placements.

Earnings Per Share (EPS): $11.93 - $12.43, representing 8% - 12% growth on a comparable basis.

Capital Expenditures: Estimated to be approximately $160 million.

Long-Term Multi-Year Goals

IDEXX's long-term growth is driven by a massive and underserved instrument placement opportunity, representing a runway of over 320,000 potential new units. Consequently, it has established multi-year financial goals that reflect its confidence in its durable business model:

Organic Revenue Growth: 10%+ annually

Annual Operating Margin Gains: 50 - 100 basis points, driven by software, price realization and growing mix of CAG recurring revenue

Annual EPS Growth: 15% - 20%

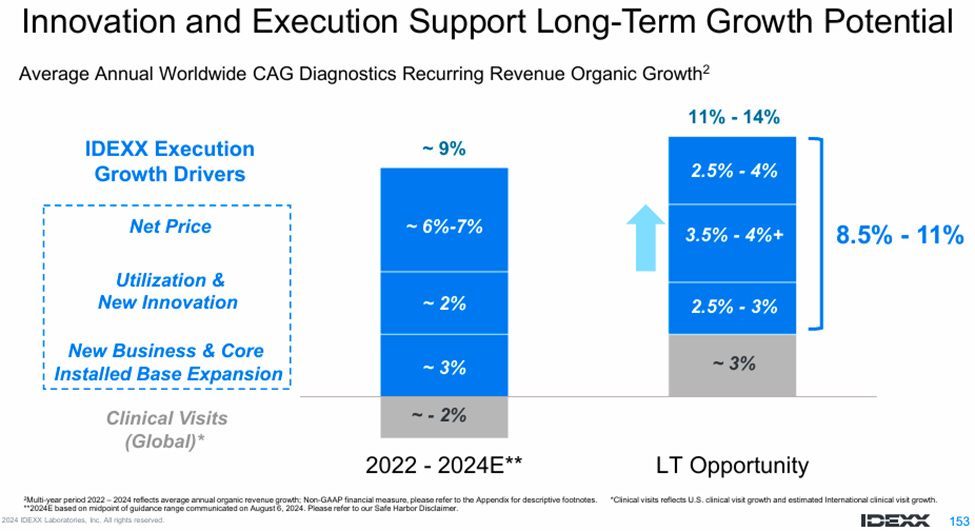

This growth is expected to be driven by software and services 15% annual growth, a double-digit expansion in CAG recurring revenue (11-14%), which management believes will be achieved through a combination of net price increases, new business from installed base expansion, and a reversal of the recent trend in clinical visits. As EVP Tina Hunt explained, IDEXX has confidence in a return to 3%+ annual clinical visit growth over the long term, driven by powerful tailwinds, including pets living longer, rising adoption by younger generations, and the large "bolus" of pets adopted during the COVID pandemic now aging into a life stage that requires more intensive diagnostic care.

Furthermore, CFO Andrew Emerson has highlighted the role of innovation in this algorithm, noting that new innovations are expected to contribute approximately 2% to the long-term annual growth rate.

Source: IDEXX August 2024 investor day

6. Competitive Advantages, Opportunities and Risks

Competitive Advantages

Integrated “Razor-and-Blade” Ecosystem: IDEXX's primary advantage is its business model. By placing a massive installed base of diagnostic instruments ("razors"), the Company locks in a highly predictable, multi-year stream of high-margin recurring revenue from the sale of proprietary consumables ("blades"). This model is difficult to replicate at scale and is the foundation of its financial strength.

High Switching Costs & Sticky Customer Base: The deep integration of IDEXX's instruments (via the IVLS) and software (PIMS, VetConnect PLUS) into a clinic's daily workflow creates extremely high switching costs. This ecosystem effect, combined with the Company's operational excellence (e.g., 99%+ product availability), results in exceptionally high customer retention rates, consistently in the 97-99% range.

Scale and Regulatory Barriers: As the clear market leader with a revenue scale in diagnostics, IDEXX benefits from significant operational leverage. Furthermore, the Company operates in a complex and stringent global regulatory environment (overseen by the USDA, FDA, and EPA in the US), which creates a barrier to entry for new and smaller competitors.

Continuous Innovation Engine: The Company’s moat is built on a continuous R&D engine that consistently delivers a broad, integrated portfolio of best-in-class products. This relentless pace of innovation, rather than patent protection alone, is a key competitive advantage that is difficult for competitors to replicate.

Opportunities

New Innovation Platforms: The Company’s growth will be fueled by its next wave of innovation. The IDEXX inVue Dx Cellular Analyzer and the IDEXX Cancer Dx panel are tapping into new, multi-billion dollar addressable markets in cytology and oncology, respectively, where there is immense unmet demand from both veterinarians and pet owners.

Increasing Diagnostic Utilization: The global companion animal diagnostics market, estimated at over $45 billion, remains massively underserved (only ~15% penetrated). A core opportunity for IDEXX is to increase the frequency of testing per clinical visit by educating veterinarians on the medical and financial benefits of a higher standard of care.

International Expansion: The international market represents a substantial long-term growth opportunity. With diagnostic penetration in key regions like Europe at just 8% (compared to 22% in North America), there is a long runway to place instruments and drive recurring revenue growth.

Expansion of the Software Ecosystem: With a target of 15%+ annual recurring revenue growth, IDEXX is capitalizing on the industry's shift to cloud-based software. By growing this high-margin business through both organic innovation and strategic acquisitions, it deepens its competitive moat and increases its share of clinic spending.

Risks

Veterinary Industry Consolidation: An increasing percentage of veterinary hospitals are being acquired by large corporate groups and buying consortiums. These entities have significant buying power and often seek favorable pricing from suppliers. Furthermore, some of these corporate owners operate their own competing reference laboratories, creating a risk that they could shift testing away from IDEXX after acquiring a clinic.

Economic Slowdown: Demand for companion animal care is sensitive to the broader economy, as pet owners generally pay for services out-of-pocket. A significant economic slowdown could lead to a reduction in pet-owner spending on diagnostics. It could also cause veterinarians to defer purchasing or upgrading capital items like IDEXX's in-clinic analyzers.

Key Supplier Reliance: IDEXX depends on sole-source suppliers for critical components, most notably the Catalyst consumables, which are secured through an exclusive agreement with Ortho-Clinical Diagnostics extending to 2044. While this long-term contract provides supply security, any disruption would significantly impact production as finding and qualifying a replacement would be a difficult and lengthy process.

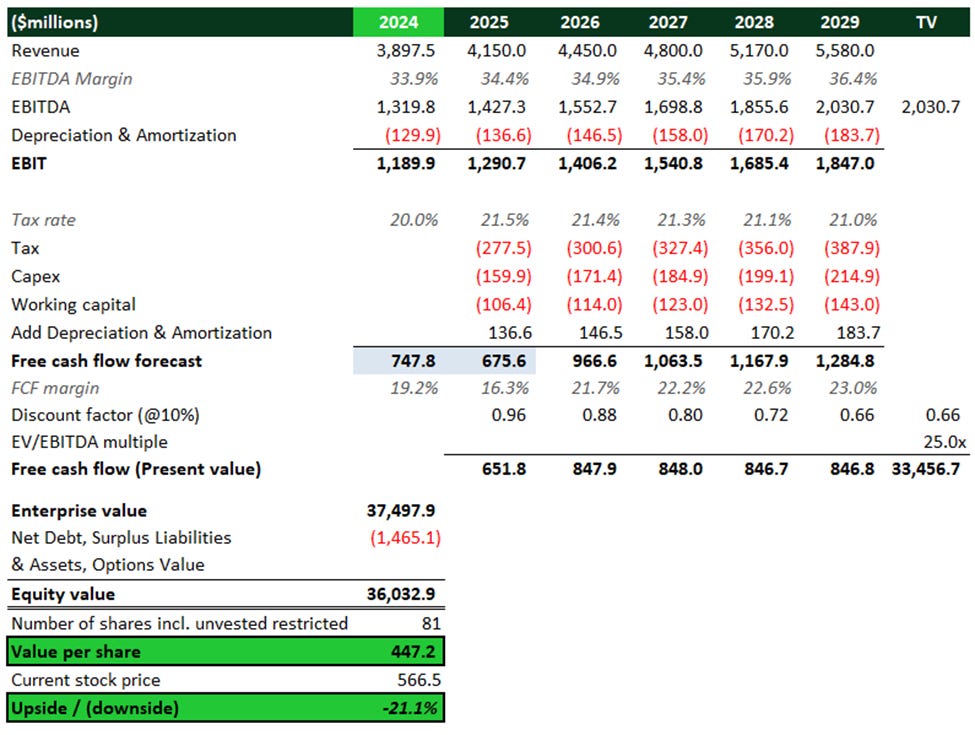

7. Valuation

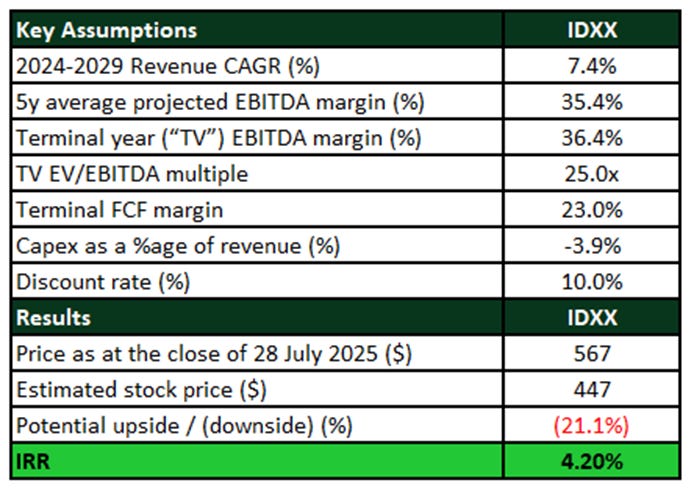

The stock price as of 28th of July 2025 stands at $566.5 with a year to date return of 37%. The Company's market capitalization is $45.6 billion and it trades at an EV/EBITDA TTM multiple of 34.6x. Based on our DCF valuation, the estimated price of IDEXX is $447, ~21% lower than its current price, and an expected IRR over the projected period of 4.5%.

Source: StockOpine analysis

Revenue Assumptions

To estimate IDEXX’s fair value, we assume a revenue CAGR of 7.4% through fiscal year 2029, reaching approximately $5.6 billion. While our revenue growth assumption is below management's long-term organic growth target of 10%+, we believe it is a prudent forecast, as the Company's actual growth in 2024 (6.5%) was below that target. Our model is underpinned by the following key segment growth assumptions:

IDEXX VetLab Consumables: 11.6% CAGR (vs. a historical CAGR of 14%)

Reference Laboratory Diagnostics: 4.5% CAGR (vs. a historical CAGR of 10.9%)

Veterinary Software: 11.4% CAGR (vs. a historical CAGR of 12.1%)

Profitability Assumptions

We forecast the EBITDA margin to average 35.4%, expanding to a terminal margin of 36.4%. This is above both the 5-year historical average of 31.7% and the 33.9% margin achieved in fiscal year 2024.

Our forecast is built by starting with the 2024 margin of 33.9% which is expanded by an average annual margin of 50 basis points. This assumption is aligned with the lower end of management's long-term guidance for 50-100 basis points of annual operating margin expansion and is consistent with their 2025 guidance for 30-80 basis points.

Free Cash Flow and Capital Expenditures

We assume capital expenditures will be 3.9% of revenue, aligned with IDEXX’s FY25 guidance of $160 million and is also consistent with the Company's 5-year historical average. After accounting for taxes and working capital, we estimate a terminal FCF margin of 22.8%. This is above the 5-year historical average of 17.3% (adjusted for stock-based compensation) and reflects our expectation of sustained high profitability.

Terminal Value

For the terminal value, we applied a 25.0x EV/EBITDA multiple. This is well below IDEXX’s current TTM multiple of 34.6x and its 5-year historical average of 42.0x.

In a peer context, our chosen multiple is in line with the 5-year average for Zoetis (25.8x) but represents a premium to its current multiple of 18.0x. We believe this premium is justified by IDEXX’s superior capital efficiency, as demonstrated by its ROIC of over 35% compared to approximately 24% for Zoetis.

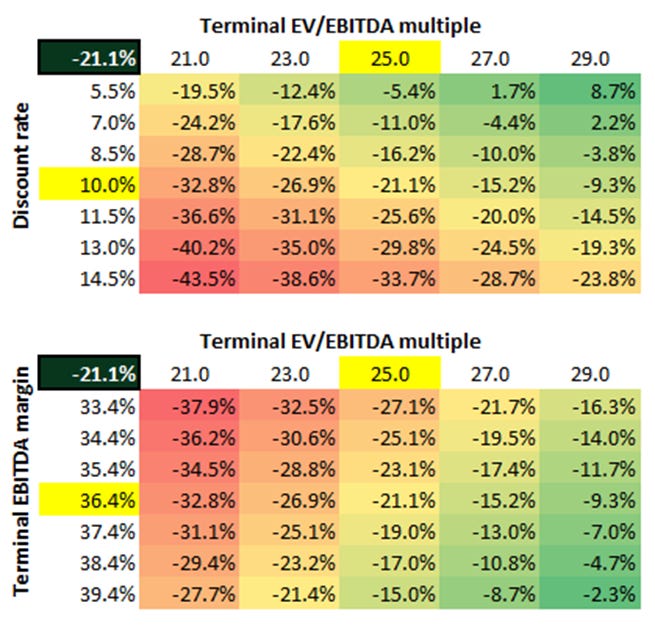

While we view 25.0x as an appropriate multiple, the accompanying sensitivity analysis illustrates a range of outcomes. Based on this analysis, even with a higher terminal multiple, IDEXX appears to be richly valued at its current price.

Valuation summary

To calculate intrinsic value, we apply a 10% discount rate, adjust for net debt and non-operating assets/liabilities, and then divide by the total number of shares outstanding.

Based on our model, the fair value per share is $447, which is 21% lower than the current market price, implying an IRR of 4.2% over the forecast period.

a. The Valuation model

Here’s the full year-by-year financial projections from our model.

Source: StockOpine analysis, Note: The reported FCF for 2024 was $808M. The $747.8M figure used in our analysis is a normalized FCF that has been adjusted to deduct SBC. For the purpose of this analysis, we treat SBC as a cash expense. The 2025 FCF figure reflects a manual deduction of the FCF generated in Q1.

b. Sensitivity analysis

The tables below illustrate the sensitivity of our valuation to key assumptions, showing the potential upside or downside relative to the current share price of $566.5 (as of July 28, 2025).

The first analysis varies the terminal EV/EBITDA multiple and the discount rate, while the second varies the terminal EV/EBITDA multiple and the terminal EBITDA margin. As shown, the valuation appears rich across a range of scenarios, suggesting limited upside potential from the current price.

Source: StockOpine analysis

8. Conclusion

IDEXX Laboratories is the undisputed global leader in veterinary diagnostics, built upon a masterfully executed “razor-and-blade” model that has created a durable competitive moat. This strategic excellence is reflected in its stellar financial performance, characterized by consistent organic growth, steadily expanding margins, and an impressive Return on Invested Capital.

Looking ahead, the Company has clear runways for future growth from its innovation pipeline, increasing test utilization, and international expansion. However, this operational excellence appears to be fully reflected in the stock's current rich valuation. While IDEXX is a high-quality business we would be proud to own, the current share price does not offer a sufficient margin of safety. A significant pullback to the levels seen near its 52-week low of approximately $360 would present a compelling entry point.