Intuit’s Q3 FY26 results delivered a clear message: the company is aggressively shifting upmarket. While a 17% workforce restructuring and low-end DIY tax headwinds created near-term noise (the stock price closed 20% lower the next day), strong double-digit growth in QuickBooks and the TurboTax Assisted category proved that Intuit's core moat remains highly intact.

1. Performance

a. Q3 FY26 Results

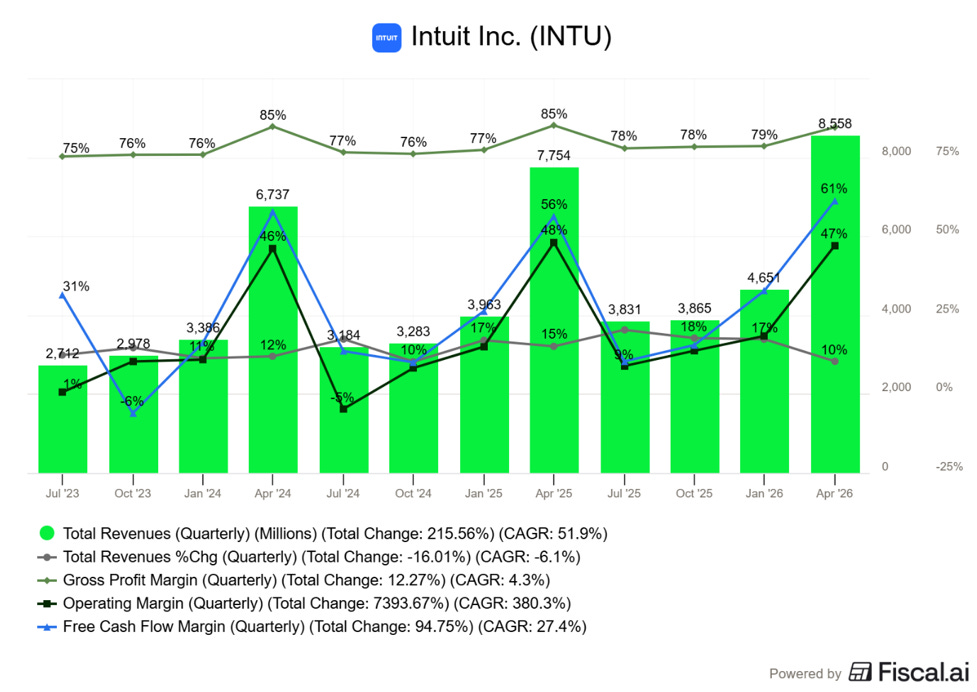

Intuit delivered a strong beat-and-raise quarter, topping Wall Street expectations while absorbing elevated costs from its strategic upmarket pivot. Revenue climbed 10.4% year-over-year to $8.56 billion, edging past the $8.54 billion consensus, driven largely by double-digit growth in the Global Business Solutions segment. On the bottom line, non-GAAP EPS reached $12.80 (up 9.9% YoY), comfortably beating the $12.57 consensus estimate and exceeding internal management guidance.

However, non-GAAP operating income grew at a slower rate of 7.8% to $4.7 billion, compressing operating margins by ~136 basis points to 54.7%. This compression and the 12.5% jump in overall key costs (specifically service costs, R&D, and marketing), were primarily driven by aggressive reinvestments into AI and sales capacity, alongside pricing headwinds in the low-end consumer tax market.

Despite this near-term margin squeeze, management signaled deep conviction in their cash flow trajectory by repurchasing $1.6 billion in stock, hiking the dividend by 15% to $1.20, and announcing a massive new $8 billion share repurchase authorization.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

b. Segmental Analysis

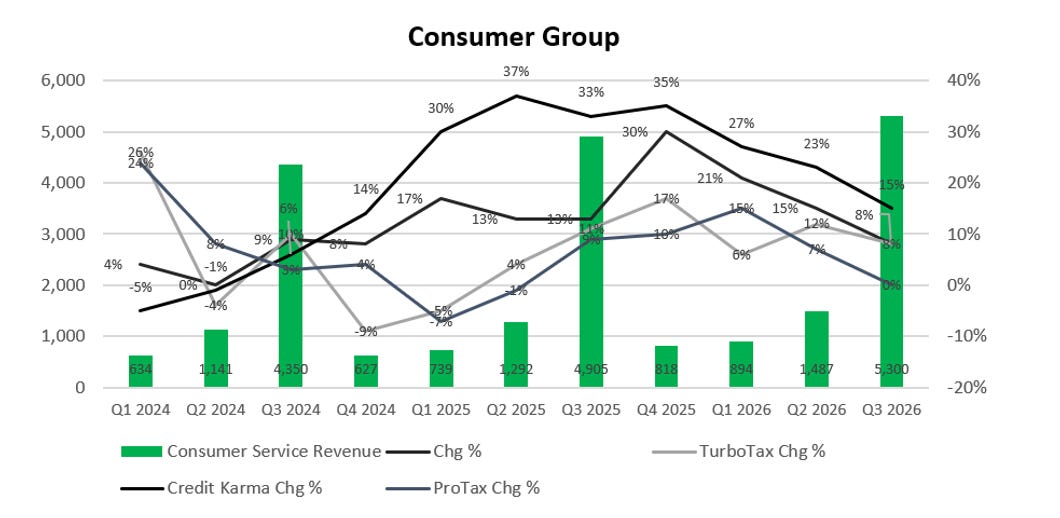

Consumer Group

The Consumer segment reported sales of $5.3 billion, an 8.1% increase year-over-year. This growth was anchored by a 7.9% increase in TurboTax revenue to $4.4 billion alongside a 14.9% year-over-year acceleration in Credit Karma revenue to $631 million, which was heavily driven by broad product strength across personal loans, auto insurance, and home loans. In contrast, the mature ProTax division experienced flat year-over-year growth at $278 million for the quarter.

Source: StockOpine Analysis

However, the headline story is the divergence within the tax business. In an environment where total IRS filers are projected to decline by ~2 million units, the largest contraction since the pandemic, Intuit expanded its presence in the $37 billion assisted tax category. TurboTax Live revenue is projected to increase by 36% to $2.8 billion, accounting for roughly 53% of total TurboTax revenue and driving a 38% growth in TurboTax Live customers. This shift toward assisted offerings and faster refund options led to a projected 11% increase in ARPU. This growth in higher-value filers helped offset a reduction in overall market share, as free, pay-nothing customers decreased from 8 million to approximately 7 million.

Conversely, the DIY segment faced headwinds among price-sensitive filers earning less than $50,000. CEO Sasan Goodarzi noted the company lost on price in this niche but plans to evolve the business model to monetize these users through the broader consumer platform.

“Build on our momentum with TurboTax Live, where we have the largest TAM and a significant ARPU opportunity. Second, evolve our DIY business model to deliver the right value at the right price point for the most price-sensitive filers, and monetize beyond tax with our consumer platform. We’re confident in our platform assets and proof points to deliver on our long-term growth goals.”

To mitigate headwinds in the low-end consumer segment, Intuit utilized its platform network, reporting that ARPU is approximately 30% higher for customers using both TurboTax and Credit Karma compared to those using TurboTax alone. This cross-platform integration allowed Credit Karma members with simple tax situations to have up to 80% of their data pre-filled. Consequently, the number of tax filers beginning their filing process within the Credit Karma interface increased by 54%.

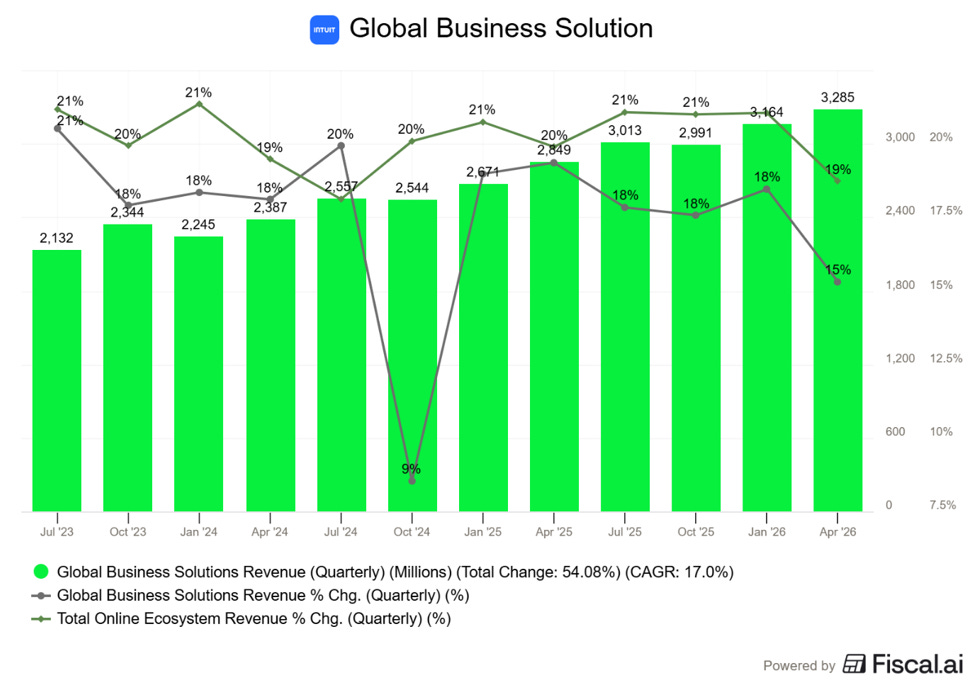

Global Business Solutions (GBS)

GBS revenue grew 15% to $3.3 billion, with the Online Ecosystem revenue increasing 19% year-over-year. Excluding Mailchimp, Online Ecosystem growth was even more robust at 22%. Total international online revenue grew 10% on a constant currency basis.

Source: Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)