KLA Corporation - Deep Dive - Part (2/2)

We hope that you enjoyed reading the first part of our $KLAC deep dive report. In this second and last part of our deep dive we will capture Risks, Competitive Positioning, Opportunities, a high level DCF calculation and our Remarks (sections 5-9). If you enjoy it, make sure that you share it to social media to spread the word.

In case you have any questions feel free to reach out either in the comments section below or DM us on Twitter @Stock_Opine.

For transparency reasons, we should also note that KLAC 0.00%↑ accounts for 4% of our portfolio with an average cost price of $336.53.

5. Risks

Recession fears and potentially a reduced consumer and business spending as well as cutting back on CAPEX of key players can delay sales and thus KLA might fail to achieve its targets. Considering KLA’s customer concentration to just few companies like TSM and Samsung Electronics increases this risk. (More details in sections 1&2)

On the positive side, during the Investor Day, the message was that even if a customer gives up a slot that easily gets filled up given the lead times of their products.

>25% of KLA Sales are to China and could be impacted from the US-China tensions (export licensing requirements imposed by the U.S. Department of Commerce, CHIPS Act to reignite manufacturing in US and the recent Nancy Pelosi’s visit to Taiwan).

Although the current licenses have not impacted KLA’s operations significantly as of today such political actions remain a risk. (More details in section 1)

Supply chain shortages, extended lead times and lockdowns in China due to COVID surges (supply disruptions, delay in systems installations, customer acceptance processes etc.).

The mitigating actions disclosed by Bren Higgins on the Investor Day is that they extend their order period, enter into long term purchase commitments, carry the inventory risk (inventory days higher than peers), have decade-long relationships (96% of key suppliers are under contract) and there is an executive level engagement.

Acquisitions: Although the risk is not significant considering Management guidance of allocating only 4% to M&A, the Company is actively engaging in acquisitions (ECI Technology for $431.5M in Feb 2022) and its Goodwill as of 30 June 2022 stood at $2.3B net of accumulated impairments of $534.2M (c.19% of initially acquired goodwill was impaired). The 19% write-off is significant and shows that on certain occasions KLA overpaid.

This does not mean that the acquisitions do not pay off, as Orbotech which was the big deal in 2019 ($3.26B) along with SPTS and ICOS make up the EPC segment which generated in CY21 system revenues of c. $1B and enabled the company to tap the packaging market, a distant target 3.5 years ago.

6. Moat / Competitive Positioning

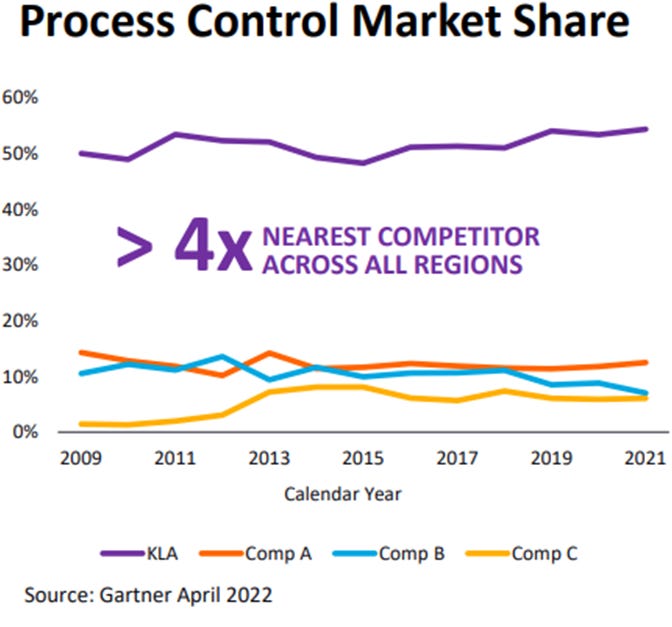

Market share

Dominant market share in semiconductor metrology/inspection equipment of 54.4%, x4 the nearest competitor due to strong specialization and the need of semiconductor metrology/inspection in order to obtain high yields during manufacturing with newer nodes. High and growing market share demonstrates the strength of KLA’s portfolio.

Source: KLA Investor Day 16th June 2022 presentation

Ahmad Khan, Share. Share is a very important metric, 54.4%. Last time when I was here for the last Investor Day, we made a commitment that we believe we can gain 0.5% share year-on-year. This would have resulted a share of 53.5% in 2023. We are happy to inform that we're at 54.4% already.

Ahmad Khan, our plan is very, very simple. Follow the KLA operating model, follow our strategy plan process and build unique systems that solve mission-critical problems for our customers. We build those unique systems that are differentiated that solve mission-critical problems for our customers. Our customers come back, give us share and give us a gross margin. That allows us to reinvest back in the business.

Management claims to have +80% share in optical inspection (a $2.5B market in 2021 as per Management) and its further strengthening its position in overlay metrology and optical metrology.

Ahmad Khan on optical inspection -> “31% CAGR in '18 to '21, far outpacing WFE, far outpacing semi PC. And while we're doing that, we gain share.”

As disclosed on the recent Investor Day, KLAC is the number 1 in 7 out of the 9 markets it serves which shows both the breadth and the importance of its portfolio.

How KLA manages to grow its market share? Deep and long standing relationships with customers and suppliers, innovative & differentiated portfolio and significant R&D investments (Average R&D / Sales for FY12 – FY22 c. 15.6%) so as to drive product differentiation and to consistently meet or exceed commitments to customers.

The importance and magnitude of R&D is somehow explained by a slide that was shared by Management back in June 2021, in which the Process Control R&D of KLA (using 2020 figures) was estimated to be larger than the process control Revenue of Hitachi High-Technology, Onto Innovation, Lasertec and ASML but slightly less than AMAT 0.00%↑ . The same relationship may not hold today (will monitor for future announcements) but R&D expenses increased from c. $750M to $1.1B. Replicating those R&D investments and achieving the scale of KLAC will not be easy for a new entrant in the space.

Margins

Higher gross margins compared to competition and higher operating margins, demonstrate product differentiation and operational productivity/excellence (as per Management). A consistent outperformance shows both cost efficiencies and the value that KLA adds to its customers.

Source: KLA Investor Day 16th June 2022 presentation, Notes: Non-GAAP measures and Semi Cap includes AMAT, ASML and LRCX

Management focus on profitability, by applying the KLA Operating Model, was more than evident on its latest Investor Day. Add to that the targeted 40%-50% incremental operating margin and the relationship of bonus executive compensation to GPM and OPM and you get an insight about the mindset of the people at the wheel.

Rick Wallace, CEO, And I can give you examples of companies we have acquired that were -- would have been on that blue line when we started, and now are on the purple line after we work through both how they run their business, how they price and how they execute.

Source: Koyfin, StockOpine analysis, Notes: * represents the full FY22 for KLAC and LRCX

In terms of cash flows, as it can be observed from the above graph, KLAC managed to generate higher FCF margins than its peers with the exception of FY2021 in which ASML generated considerably higher margin. As per its CFO, Roger Dassen this is exceptional and working capital driven due to the significant order intake in Q4’21 resulting to a FCF to net income conversion of c. 168% compared to a steady state conversion of around +/-100%. Please note that Current/LTM of ASML includes 6M of 2021 (thus Q4’21) and AMAT includes 3M of 2021.

Per our evaluation the difference in FCF margins seems to be operationally driven and not driven by any ‘hidden’ factors such as Stock Based Compensation (“SBC”) (not deducted from FCF but has dilutive effects on shareholders) or lower investments.

Source: Koyfin, StockOpine analysis

Both profit & loss and cash flow metrics demonstrate above average performance and effectively a high quality business.

Switching Costs

The growing installed base and the longevity of its installed base validate the switching cost that KLA systems have. The value added by its systems is proven by the numbers and by the long standing relationships with customers. Additionally, as these systems are highly specialized, once the customer’s employees get acquainted to these systems and manufacturing yield is dependent to its systems makes the switching process costly.

Source: KLA Investor Day 16th June 2022 presentation

It shall be noted that installed base has high longevity with >50% of installed base older than 18 years old as customers utilize tools long after their full depreciation and as a result over the life of a tool, service revenue exceeds initial tool price.

7. Opportunities

Secular growth factors such as evolving Automotives, 5G, IoT, AI, and Data centers smoothing out the cyclical nature of the semiconductor industry.

Oreste Donzella: Automotive is really the secular shift. It's an incredible, incredible inflection that we have perceived the change in the last -- chip shortage in the last couple of years, how electronics, how semiconductors, how boards are becoming absolutely essential to the production of the cars and the vehicles because many, many more components are inside the car and the vehicle, and also because of the complexity of the qualification of semiconductor or electronics inside a car.

Capex of KLA customers (more details in section 2) -> Rick Wallace, CEO “scaling has returned and the economics of advanced nodes has returned to the industry in a way that is driving new investment by our customer.”

CHIPS Act, a $52 billion package that could benefit KLAC in future periods but the benefits will be more evident to companies like INTC 0.00%↑ . The new plants will require KLAC systems which will drive growth for KLA. We also published our thoughts on How does CHIPS Act affect KLAC and other semi companies?

Opportunities in optical inspection: Increasing process control intensity in logic due to EUV introduction and smaller process designs which makes process margins smaller thus, optical inspection growing significantly (Ahmad Khan).

As addressed by Rick Wallace, Moore’s law resumption due to EUV and going from 10nm->2nm, the rapid growth of design starts of the 7nm, and the expectation of Hyperscalers designing their own silicon fuels growth as process control becomes growingly relevant.

Rick Wallace, CEO, more and more players are going to be designing their own silicon as they recognize the importance of having their own capability. Hyperscalers are already doing it. There's one car company that's been doing it. I'm quite confident there will be more, right? Because as they move into EV, there's going to be more.

Service revenue (mainly service and brake fix maintenance) is sustainable and growing and with 75% subscription like contracts and more than 95% (from 90% in 2019) renewals provide stability and predictability to cash flows. In addition, as indicated by Brian Lorig, EVP, Services, the length of service contracts is extending (average >3 years, increase of 40%). It shall be noted, that Management specified that Service revenue grows 4.5x faster than installed base.

8. Valuation

The stock price as of 6th of September 2022 stands at $330.58 and is down by 23.14% YTD. The market cap of the Company stands at $46.88B and trades at an EV/EBITDA Trailing Twelve Months (“TTM”) multiple of 12.9x compared to its 5 year average of 14.6x. Based on our DCF valuation the estimated price of KLAC stands at $400, 21.0% higher than its current price level with a resulting IRR over a 5-year period of 14.9%.

Source: StockOpine analysis

To estimate the fair value of KLAC we assumed a revenue CAGR of 7.9% based on both analysts’ consensus and Management expectations. The resulting revenue for FY26 (c. $11.9B) and FY27 (c. $13.5B) is at the lower end of Management’s target of $14B +/-$500M of CY26. We consider this assumption to be fair given the estimated WFE CAGR of 7.5% for the period 2021 – 2026.

In terms of profitability, we used an average projected EBITDA margin and terminal EBITDA margin of 43.6% which is higher than the 5 year historic average of 39.1% and similar to the FY22 EBITDA margin of 43.6%. The basis of the margin improvement is the targeted Non-GAAP incremental operating margin of (40% to 50%) and the leverage that the Company expects to have on its SG&A expenses.

To derive the free cash flows to the firm we deducted projected Capex requirements based on the historic average and adjusted upwards by 0.5% to be closer to the 3%-4% range disclosed at the Investor Day.

In respect to the terminal EV/EBITDA multiple, it is assumed to be around 12.5x which is lower than its current multiple of 12.9x and its 5-year average 14.6x. Despite this, the terminal multiple is higher than the median 10.7x multiple of the selected peers in the semiconductor equipment industry but lower than their 5-year median of 14.3x. The quality of its business justifies a higher multiple than the median of its peers, although we tried not to be aggressive in our estimates.

To calculate the value per share we used the minimum required return that we aim to obtain from our investments (i.e., 10%) under the current environment, adjusted for net debt and non-operating assets / liabilities identified and thereafter divided the resulting value by the number of shares.

Based on the above calculations and assumptions used (which of course may not materialise at all), we reach a value per share of $400 with a potential upside of 21.0% and a resulting IRR over a 5-year period of 14.9%.

Sensitivity analysis

The below table gives an indication of the potential upside/downside %age compared to the current price ($330.58 as of 6th of September) when the terminal multiple and the discount rate are changed.

Source: StockOpine analysis

9. Concluding Remarks

KLA has a quality business model which cannot be easily replicated by its competitors or new entrants and this is justified by its high and increasing semiconductor process control (metrology/inspection equipment) market shares, by its high GPM, OPM and FCF margins as well as its long dividend history.

Its specialization in process control, its commitment to R&D and its strong and lasting customer relationships place KLA as a strong candidate in capitalizing on the Semiconductor secular growth factors.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.

We have a long position in the shares of KLAC.

Hi, is it possible you can you update KLA valuation to see where it stands today after 1yr? Thanks