In December’s first article, we dive into Leslie’s, the largest pool supply retailer in the US. The boom and bust of the pool industry brought this niche retailer to its knees, with its stock price collapsing by 90% since its IPO in 2020.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

1. Key Facts

Description: Leslie’s (the “Company”) is the largest direct-to-consumer pool and spa care brand in the United States. They market and sell supplies and services for pools and spas, including chemicals, equipment, parts, cleaning accessories, and safety and recreational products. Leslie’s serves both residential and professional clients and sells its products through more than 1,000 physical locations as well as e-commerce platforms.

Key Financials: From FY18 to FY24, the company achieved a revenue Compound Annual Growth Rate (CAGR) of 6.9% while its operating income declined from $116 million (13% operating margin) to $67 million (operating margin of 5%). Leslie’s has debt and lease liabilities of $1.05 billion compared to cash and short-term investments of $109 million.

Price & Market Cap (as of 13 December 2024): Its market cap is $451 million with a 52-week low of $2.20 and a 52-week high of $8.21, whereas it currently trades at $2.44.

Valuation: It trades at a NTM EV/EBITDA of 11.1x (5 Year average of 15.3x) and a NTM EV/Sales of 1.0x (5 Year average of 2.6x).

2. Business Overview

a. Leslie’s history and reputation

Leslie’s was founded in 1963 by Phil Leslie, in a single location in Los Angeles. The Company quickly expanded to more locations to cater the growing demand for pool and spa care products, establishing itself as a trusted retailer in pool care. By the time it went public in 2020, Leslie’s managed to grow to a 1000 store chain across 37 states, making it the largest retailer in the pool care industry, capturing 15% market share in the lucrative aftermarket spend of the pool industry.

Why we like this industry? Pool aftermarket spend benefits from the growing installed base of pools and the recurring nature of maintenance and repair revenues, which contribute to consistent industry growth. Leslie’s estimates that more than 80% of Leslie's product sales are non-discretionary. Leslie’s history underscores the resilience of this business model. Throughout its history and up to its IPO in 2020, Leslie’s achieved 57 consecutive years of sales growth, a testament to the enduring demand for pool care products and services.

b. The IPO and the pandemic boom

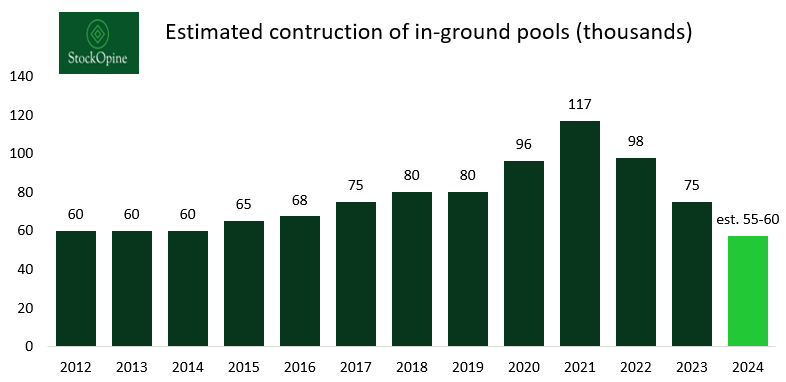

Leslie’s went public in October 2020 at an IPO price of $17 per share, raising $510 million and debuting with a valuation of $3.84 billion. The timing couldn’t have been better as the pool market was thriving during the pandemic. With pandemic-related restrictions and lockdowns, people were spending significantly more time at home while also receiving government stimulus checks. This led to a rise in pool usage (more $ spent on pool care) and home improvement projects, including the installation of new pools and the renovation of existing ones. This drove increased demand for pool equipment, chemicals and hot tubs. In fact, construction of new pools during the pandemic, spiked to levels not seen before.

Source: Pool Corporation 10K filings, Pool Corporation Q3’24 Earnings call, StockOpine Analysis

On hindsight, this was the perfect time of a pool business IPO. Heavily burdened with $1.2 billion in debt at the time, Leslie’s used part of its net proceeds to repay $390 million in floating rate notes due in 2024, which carried a high interest rate of 9.5%. This reduced financial pressure, but as of October 2024, the company’s debt remains at $833 million - almost unchanged from its post-IPO levels (we’ll discuss this further in the financial analysis section).