Every month we share 2 write-ups on companies we decided to examine as potential additions to our portfolio. Although the companies analyzed may tick most of the boxes, if the margin of safety is not considered sufficient, we will not initiate a position but rather monitor the stock.

Up to now, we clearly stated at the conclusion of each write-up whether we decided to buy the stock or not. This is changing!! The plan is to release each new write-up free from any action at the time of the release so as to allow the reader to draw his/her own conclusions, though, we will still share our concluding remarks on the quality of the business.

Despite this, we are NOT taking away from our subscribers our investment journey. Thus, we are re-introducing the format of “Investment thesis” (see example -> Greggs Plc - Investment thesis) memos. In these short memos we will be sharing our thesis for new positions, address the key risks, state our action and provide a link to the full analysis. This could be dated an hour after the report (if we are too excited in owning the stock), a day, a week, a month or even a year after the report.

For any additions to existing positions we will still use our Quarterly Portfolio Updates to keep you informed.

New Year, new screening. After running the first screening of the year, lululemon Athletica stood out. Scoring high in almost all metrics, demonstrating high growth rates, having best in class operating margins and high returns on capital made it an easy choice for the 1st release of 2023.

1. Key Facts

Description: lululemon Athletica Inc. (“LULU”, “Lulu”, and “Company”) is engaged in the design, distribution, and retail of technical athletic apparel, footwear, and accessories, mainly sold through company-operated stores (“COS”) and direct to consumer (“DTC”) e-commerce. The Company, as of 30 October 2022, operates globally through 623 COS with the majority located in United States (337), China (105 – including Hong Kong and Taiwan), Canada (66), Australia (31) and UK (16).

Key Financials: Over the period FY12 to Q3’FY22, the Company depicted a revenue and operating income Compound Annual Growth Rate (“CAGR”) of 19% and 15.9%, respectively, reaching a Trailing Twelve Month (“TTM”) revenue of c. $7.5B and operating income of $1.6B (margin of 21.4%). LULU has Cash and Short-term investments of $353 million compared to lease liabilities amounting to $1,039 million. Cash position was abnormally low due to the investments in inventory in Q3’FY22 so as to meet demand.

Price & Market Cap (as of 20th January 2023): Its market cap is $39.9 billion with a 52-week high of $410.7 and a 52-week low of $251.51, whereas it currently trades at $312.80.

Valuation: LULU trades at a TTM EV/EBITDA of 21.7 (10 Year average of 22.4) and at a TTM P/E of 33.8 (10 Year average of 40.5).

*Note: Fiscal Year (“FY”) of Lulu ends on the Sunday closest to January 31 of the following year (i.e. FY21, year ended 30 Jan 2022).

The rest of the write-up includes the following sections:

2. Business Overview

3. Management & Culture

4. Industry

5. Financial Analysis

6. Capital Allocation

7. Competitive Advantages, Opportunities and Risks

8. Valuation

9. Concluding Remarks

2. Business Overview

Lululemon in a nutshell

Lulu was founded in 1988 in Vancouver, Canada and its initial public offering took place in July 2007. Since its inception it delivered a total return of 2,134.29% (per Koyfin) translating into a compound annual return of c. 22%.

Although it started as a company offering yoga pants to women, it expanded its offering providing technical athletic apparel, footwear and accessories to both men and women. The versality of its products/offering meets the needs of people who do yoga, run and train and those involved in other activities such as tennis, golf and hiking.

From a single store in Vancouver, Canada in 2000 to 623 company-operated stores across the globe with United States (337 stores) being its largest market as of today. Although, the number of stores expanded considerably brand awareness is still low and the potential for growth seems huge. More on this later.

If interested to read more about the history of LULU you can read the article written by our friend Investment Talk Elastic Growth, Lululemon and more specifically section “The Brief History of Lululemon”.

Reporting segments

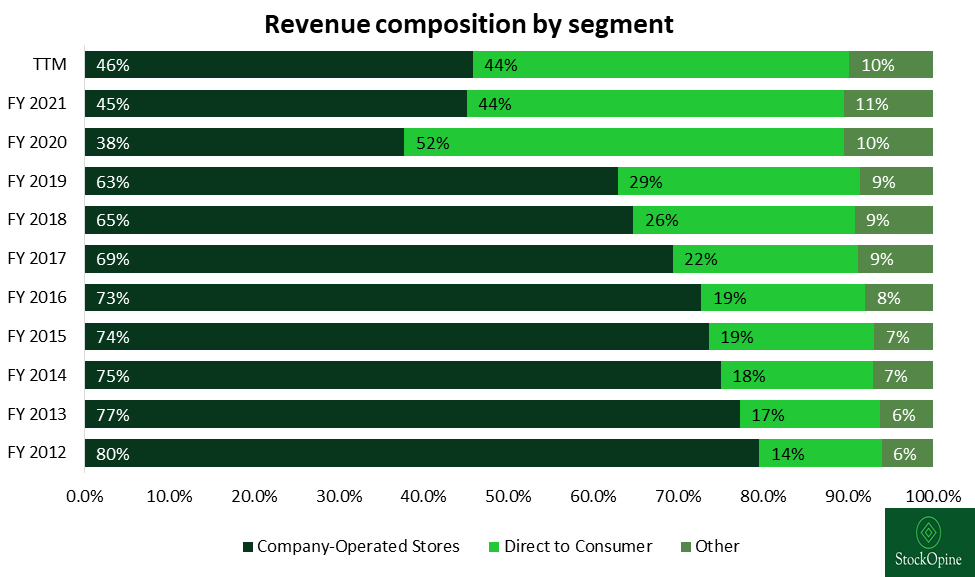

The Company has 3 reporting segments, namely, Company-operated stores, Direct to consumer and Other.

Company-Operated stores account for 46% of sales or $3.4B on a TTM basis (45% in FY21) and these are the sales generated through its 623 stores. The operating margin for COS (excludes general corporate expenses) since FY12 until today (excluding FY20) averages at 27%.

Direct to Consumer (e-commerce) account for 44% of sales or $3.3B on a TTM basis (44% in FY21) and these are the sales generated through ecommerce. LULU operating as an Omni-channel allows a guest to shop both in store and online. As per management, when a store-only guest shops online becomes an Omni-guest and spends approximately 30% more. The operating margin for DTC (excludes general corporate expenses) since FY12 until today averages at 42%.

Source: Stratosphere.io, StockOpine analysis

Considering the high margin of DTC business, it’s no coincidence that the initial Power of Three in April 2019 (more on this later) targeted for doubling DTC sales over a 5-year period. COVID pulled forward the demand and helped in smashing this target in FY20. The trend is upwards showing resilience and through the Power of Three x2 in April 2022, management targets for another doubling of DTC sales, i.e. exceeding $5.5B.

The higher margin of DTC is expected since costs like rent, electricity, and wages are minimized relative to COS. The value proposition in growing DTC is further supported by the lower Capital expenditure (“CAPEX”) requirements (average 2% of sales) compared to COS (average 6% of sales). Higher margin, lower CAPEX implies better returns on invested capital.

Other includes the remaining types of distribution to end customers (e.g. outlets, temporary locations – 60 in North America, sales to wholesale accounts, license and supply arrangements – mainly in Mexico and Middle East countries – total 22 stores, and recommerce – sales of repurchased Lulu products) as well as sales to its connected fitness customers through lululemon Studio (formerly known as MIRROR). The operating margin for Other (excludes general corporate expenses) since FY12 until today (excludes FY20) averages at 14%.

We believe that all segments are important to the future success of the Company with each having its own weight. DTC might seem the ideal segment, but without physical stores brand awareness would have been limited (it is already low). License and supply arrangements require less CAPEX but Lulu still gets the exposure to new markets, raising brand awareness, and providing the Company with an opportunity to sell through its e-commerce channel. Pop-ups allow to test the waters in new markets, capture seasonal demand and reach new guests. ‘Like New’ (recommerce of repurchased products) which went live to all US stores in April 2022 allows users to trade-in clothing in good condition and get e-gift credit that they can use on new items. The old items are revived and become available for sale at a lower price. This is a win-win situation for the Company and its customers. Existing users are encouraged to purchase again from Lulu (as they get e-gift cards) while it also attracts new users of lower income classes who want to get quality at price levels which are not restrictive anymore. Does it ring a bell? To us yes, ‘Network Effect’ is calling. On top of this, profits from the program go directly to the sustainability initiatives of Lulu.

Revenue by Category

Since FY17, the Company disaggregates its revenue into Women’s product, Men’s product and Other categories (accessories, lululemon studio and footwear). Women’s product is the chunk of revenue accounting for 65% or $4.9B on a TTM basis (71% back in FY17) while Lulu is also becoming more appealing to Men as revenue grew from $527M in FY17 to $1.8B on TTM basis (or from 20% weight to 25%).

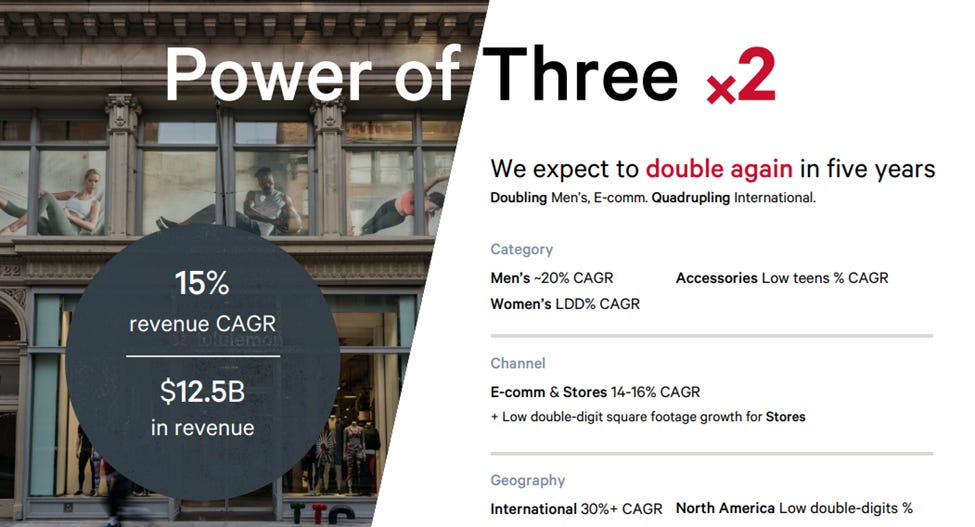

Men’s doubling of revenue was another Power of Three (Apr 2019) target that was achieved earlier than the 5 year horizon. From $691M in FY18 to $1.5B in FY21 and expected to exceed $3B by FY26 (New Target under Power of Three x2 – April 2022).

Lastly, other segment (10.5% of sales on TTM) is what completes the offering of Lulu, for which management strives to continuously broaden its merchandise. It grew from $230M in FY17 to $783M on a TTM basis (CAGR of 29.4%).

lululemon studio (included in Other) is the connected fitness segment which does not seem to be performing as expected, yet the expectations are there.

Meghan Frank, CFO “It is important to note that while footwear and our evolved lululemon studio, MIRROR model are exciting long-term opportunities for us, we have taken a conservative approach to how we've contemplated them in this plan. And over the next 5 years, we are forecasting the combined penetration of those 2 pieces to be in the mid-single digits, lower in the near-term years and higher in the outer years.”

With the transition from MIRROR to lululemon studio and the new membership program announced on September 2022, management seems excited with its offering, and is on the right track in achieving the target of signing 80% of their guests to the program (on the free membership). Yet, we consider lululemon studio as an upside, with membership programs providing positive externalities to the rest of the business rather than being a driver of future performance. Needless to say that there is an ongoing litigation for certain infringement of patents in which the Administrative Law Judge issued Initial Determination recommending Exclusion Order and Cease and Desist Order against the Company (Company filed a petition).

Footwear is another step taken by the Company to enhance its offering.

Calvin McDonald, CEO, “it shows the ability to identify unmet needs even in a category like footwear and then how we innovate, how we bring that to market. So I think it's a great example to just demonstrate that there is a lot of opportunity when you focus on innovating behind unmet needs regardless of the category in which you're trying to do it in.”

In March 2022, it announced its official entrance to footwear with four innovative women’s styles and revealed the plan to do the same for men in 2023. Not their core business and not a significant component of the Power of Three x2 equation, however, a milestone towards offering the “head-to-toe” solution to its customers. We presume that margin wise there would be insignificant impact as the Direct-to-Consumer (both own stores and ecommerce) sales of Skechers USA Inc., which primarily sells shoes, has a margin that oscillates around the 65% level (Lulu has 5 year average gross margin of 56%).

Geographic mix

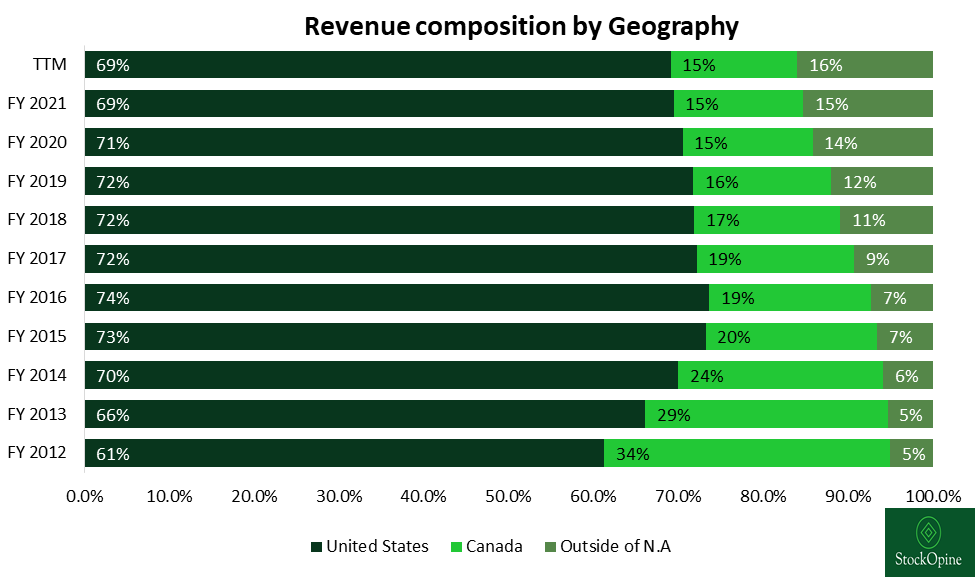

The majority of Lulu’s revenue is generated from the US which is considered along with Canada, the two most mature markets. This by no means translates to a lower expected growth as the expectation is for over $8B in revenues by FY26 compared to $5.3B in FY21. Nevertheless, the opportunities abroad seem massive in relative terms.

US accounts for 69% of its sales on a TTM basis i.e. revenue of $5.2B (CAGR of 20.5% since FY12), whereas Canada and International sales had a similar weight and revenues of $1.1B (CAGR of 9.4% since FY12) and $1.2B (CAGR of 34% since FY12), respectively. While not disclosed explicitly, based on the scale of US and the comments made by management, it appears that this is a more profitable region at this stage.

Source: Stratosphere.io, StockOpine analysis

In its Power of Three (April 2019) the Company targeted to quadruple its international sales from $360M to $1.4B. It is not there yet but it achieved 83% of this target on a TTM basis. If China zero COVID policy was not enforced this target could have been possibly achieved 100%. Per Power of Three x2 the target remains unchanged. Quadruple sales of $957 in FY21 to reach c. $3.8B by FY26 with China expected to be its 2nd largest market, while the number of stores in China is expected to triple.

Opening new stores, increasing sales per store, growing DTC channel, enhancing offering through product innovations and raising brand awareness are the growth drivers for LULU, both in North America and internationally.

The below pie chart represents the store composition as of 30 October 2022. As it can be observed, US and China (including Hong Kong, Taiwan and Macao) are the leading regions in terms of stores. From the “All other” category Germany with 10 stores and New Zealand with 8 are the most significant.

Source: Latest 10Q filing, StockOpine analysis

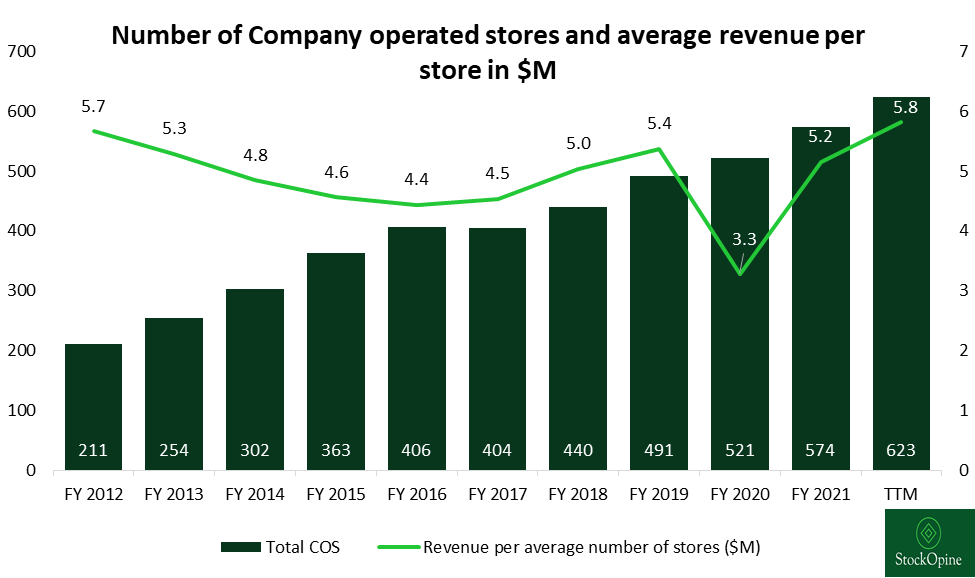

Even though, the number of stores drives revenue growth it does not necessarily mean that each store reaches its full potential from Day 1. For example, Canada has much lower number of stores, yet similar revenues to the rest of the international locations. This disproportionate relationship is further justified by the graph below which shows that when a new region was introduced, revenue per store declined. E.g. in FY14 it entered the UK market, in FY15 the China market, in FY16 the South Korean market while at the same time stores in US (and China after FY15) were growing exponentially.

Source: Stratosphere.io, StockOpine analysis

Going forward, the Company expects to grow stores at double digit rates.

Branding

Almost everyone reading this write-up is aware of Adidas, Nike, Puma etc. As per the Brand Finance in Apparel 50 2022 rankings, LULU’s brand value improved moving up from 25th to 21st, however it’s brand awareness is not there yet. Increasing the number of physical stores does help but the data provided by management suggests that there is still a lot to be done. Entering Spain (Barcelona & Madrid) and the recent opening of a new store in Champs-Elysees, Paris (over 300,000 visitors per day) creates a momentum in Europe for further brand recognition.

On its Investor Day 2022, the below screenshot was shared that shows unaided awareness (percentage of respondents aware of a product, brand, or advertising top-of-mind without assistance) across regions.

Source: Lulu Investor Day April 2022 presentation

In US which is considered LULU’s most mature market, the estimated unaided awareness stands at 25%. In UK in which the Company entered in FY14, it stands at 15% whereas in China (entered in FY15) it stands at 7%. Per management, other peers stand at 85%-90%. This provides a huge opportunity for Lulu both in achieving its target to quadruple international sales but to also double men’s sales (just look at the 11% in US).

Other levers that management is pulling to raise awareness, are new products (see footwear), the standard various marketing methods (a recent approach but no material change is expected in marketing as a % of sales – e.g. earned and paid media, sports marketing and partnership) and through community building. LULU tries to cultivate the community and create connection with guests by having 1,500 ambassadors globally (e.g. Jordan Clarkson an NBA player, Official outfitter of Team Canada, Joe Wicks a well-known UK fitness coach), having 20,000 educators in stores assisting guests, digital educators, running virtual events, organizing 10-K races and most recently introduced its 2-tiered membership program. The essential membership program (free, like a loyalty program) provides benefits to those who sign up and generates better data for the Company to understand guests’ needs, deepen the relationship and optimize the experience.

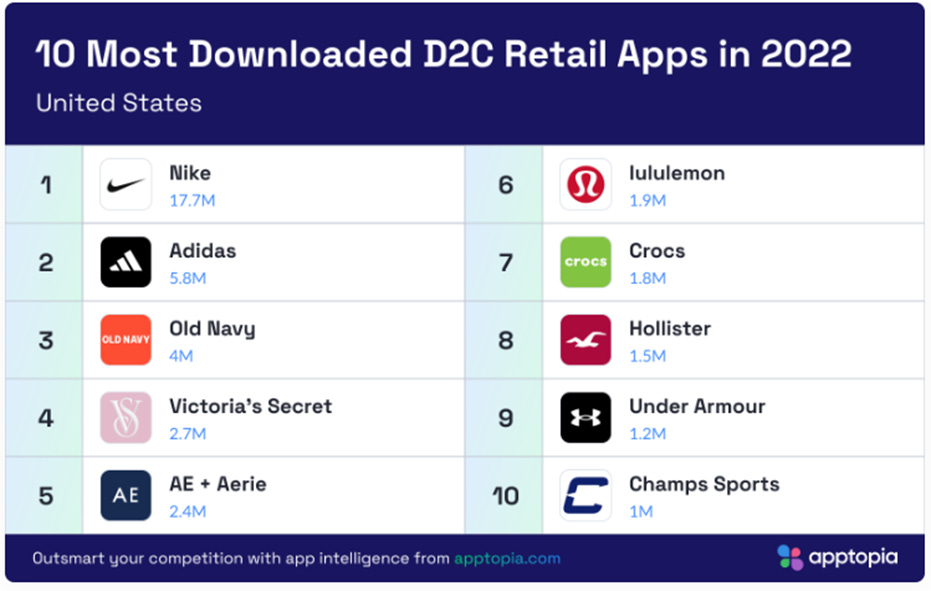

We also examined mobile downloads of Lulu’s app as provided per Apptopia. Making it in the top 10 with 1.9M downloads and regarded as the fastest growing D2C app in Q4, shows that Lulu is on the right track. The spike in Q4 might be also justified by the new lululemon studio membership program announced in September 2022.

Source: Apptopia

Manufacturing

LULU does not operate or own any manufacturing facilities neither has any long-term contracts with its vendors (has long standing relationship though). Per the latest annual filing it relies on 41 vendors that manufacture its products, with the Top 1 accounting for 15% and the Top 5 for 57%. Region wise 40% of its products are manufactured in Vietnam, 17% in Cambodia, 11% in Sri Lanka, 7% in PCR (China) etc.

65 suppliers provide the fabrics for their products with the largest manufacturer producing 27% and the Top 5 56%. Region wise 48% of fabrics are originated from Taiwan, 19% from China, 11% from Sri Lanka, etc. A similar mix was observed in FY20 with slightly higher weight on the largest manufacturer.

Overall, the mix shows that there is reliance to key manufacturers and any supply disruptions, capacity restrictions or even losing any of those key manufacturers could negatively impact sales.

Comparing to Nike and Adidas which also outsource virtually 100% of their production to independent manufacturing partners we observe similar trends. A large number of suppliers, but reliance on few ones and significant reliance on Asian countries.

Source: Adidas and Nike annual filings, StockOpine analysis

Based on the above findings we do not believe that LULU faces any company specific risk relating to manufacturing but rather an industry wide risk. Given LULU’s smaller size relative to peers, a manufacturer may elect to fulfil Nike’s needs rather than LULU’s if capacity constraints persist.

The long-standing relationships with vendors and investments/partnerships made with vendors to deliver best-in-class raw materials considering sustainable future (plant-based nylon, creating yarn and fabric using recycled carbon emissions) somehow mitigate the above risk.

Power of Three x2

Power of Three x2 is the revised strategy / aspiration of Lulu for the next 5 years (released in April 2022) and has 3 key Pillars; a) Double Men’s Product, b) Double DTC and c) Quadruple International by 2026 while at the same time continue to grow Women’s products and North America at double digit rates. On successful implementation and execution of this plan, management expects to generate a revenue CAGR of 15% reaching total sales of c. $12.5B compared to $6.3B in 2021.

We trust that management will execute on the key pillars, if not exceed them. Why? Well, execution to date and the untapped market is what makes us believe that this is achievable. In the last 5 years Lulu missed analysts’ revenue estimates only on two occasions while it missed EBIT estimates just once! Additionally, when the initial Power of Three plan was unveiled in April 2019, the Company set among others the exact same targets, a) Double Men’s Product, b) Double DTC and c) Quadruple International sales by FY23. The result? Smashed Men’s and DTC targets in FY21 and FY20, respectively whereas on a TTM basis the international sales target is 83% achieved. Early achievement of those goals resulted to the revised plan in April 2022.

“We remain early in our growth journey, with our strong product engine, proven ability to create enduring guest relationships, and significant runway in core, existing, and new markets. Following our compelling track record of delivering against our goals, I am excited about taking our growth strategies to the next level to serve more and more guests around the world.” Calvin McDonald, CEO

The remaining financial goals include EPS growth exceeding sales growth, modest annual operating margin expansion, growth of annual square footage in the low double digits (5%), tax rate of 30%, unit inventory growth in line with sales and 7%-9% Capital expenditures.

Source: LULU Investors Day presentation, April 2022

3. Management & Culture

In general we are happy with the existing management and specifically with the CEO, Calvin McDonald. Calvin joined in August 2018 and since then LULU is firing on all cylinders, smashing Power of Three and moving into Power of Three x2.

Compensation

Total compensation of Calvin McDonald grew from $10.6M in FY20 to $13.3M in FY21 driven by higher bonus (cash incentives) and higher stock awards. Considering that revenue grew by 42% and operating income by 69% for the same period we consider the increase of 25% in total compensation as totally acceptable. Per Simply Wall St, CEO’s payroll is about average for similar size companies in the US ($12.72M).

Insiders do not have any significant ownership. However, given that only 10% of the total compensation of the CEO is salary and 30% is bonus, whereas 18% is salary and 31% is bonus for other executive officers, and the remaining compensation being Performance Stock Units, Stock Options and Restricted Stock Units (not applicable to CEO), we believe that interests of management are aligned with shareholders.

Culture

Using Glassdoor score which can be used as a proxy for culture it can be concluded that LULU stands out to its peers with the highest score in all categories. As long as people love what they are doing, they are more likely to engage with guests, encourage the community building and assist in developing the brand. Additionally, strong culture helps in retaining the best talents.

Source: Glassdoor, StockOpine analysis

4. Industry

Market size and forecasts

Athleisure market, as per data provided by Grand View Research, is estimated to grow from $330.97B in 2022 to $662.56B by 2030, representing a CAGR of 8.9% and providing a huge opportunity for LULU to maintain its growth trajectory while gaining market share in the process.

In terms of market share, management stated that LULU has an estimated market share of over 5% in US and Canada (company estimates using NPD data - provided on its Analyst Day in April 2022) and at most 1% internationally, whereas the Total Addressable Market (“TAM”) internationally is estimated at $650B. The earnings calls following the Analyst Day show that Lulu is still winning market share across the board.

Calvin McDonald, CEO

April 2022 Investor Day “From a market expansion, we gained more market share than any other brand in the industry since 2019, and that really is growth from all levers.”

Q2’22 “We've definitely seen market share gain according to NPD. We've -- we are the largest share gainer in the quarter at 1.4 points. So we're very pleased with our performance, our performance relative to our peer sets.”

Q3’22 “And our market share gains continue. While the adult active apparel industry decreased its U.S. revenue by 4% in fiscal quarter 3 '22 compared to the same period last year, Lululemon gained 1.5 points of market share in the U.S. over this time, the most of any brand in this market according to the NPD Group's consumer tracking service.”

Competition landscape

The technical athletic apparel industry is highly fragmented. A competitor could be a large, diversified retailer or a wholesaler or even a small retailer focusing on women’s apparel, yoga or other activewear. Companies compete in terms of quality, price, style, use and brand positioning.

The competitors stated in Lulu’s annual report are Adidas, Nike, Athleta brand (of GAP Inc., generated $1.4B revenues in FY21), Under Armour, Urban Outfitters, Columbia Sportswear Company and Victoria’s Secret (sports and lounge offering). But there is more to it. Think of Skechers (footwear), Puma, VF Corporation, Reebok, New Balance, Hanesbrand (owns Champion) or less known firms like Girlfriend Collective (eco-friendly activewear), Alo Yoga (community based, yoga focused) and Sweaty Betty (owned by Wolverine World Wide).

Below we created 3 graphs using Koyfin to evaluate how LULU performs relative to selected peers.

Revenue Growth

Source: Koyfin

LULU is one of the fastest growing firms in the industry while (as it can be seen from the below graph) it managed to do it profitably by having the highest EBIT margin in the industry.

EBIT margins

Source: Koyfin

Looking at the operating profitability, LULU is the clear winner. Other than efficiencies, one of the key reason for the deviation in margins is the wholesale operating model that certain peers apply.

For instance, Skechers generated approximately 63% of its sales in the 9 months 2022 (71% in 2021) through the wholesale channel which as expected has lower margin of c. 37% for the Domestic Wholesale and c. 45% for the International Wholesale compared to over 65% gross margin for its Direct-to-Consumer segment. Nike, Adidas and Under Armour do not disclose gross or operating margin per wholesale and direct to consumer segments, yet wholesale accounted for 58% of Nike’s FY22 (ending 31 May 2022) sales, 62% of Adidas’ FY21 sales and 57% of Under Armour’s FY21 sales.

Let alone the additional credit risk that these firms bear from selling to wholesalers and the higher working capital needs.

Rest assured that LULU can maintain these margins. Per the annual report 2021, “We do not intend wholesale to be a significant contributor to overall sales.”

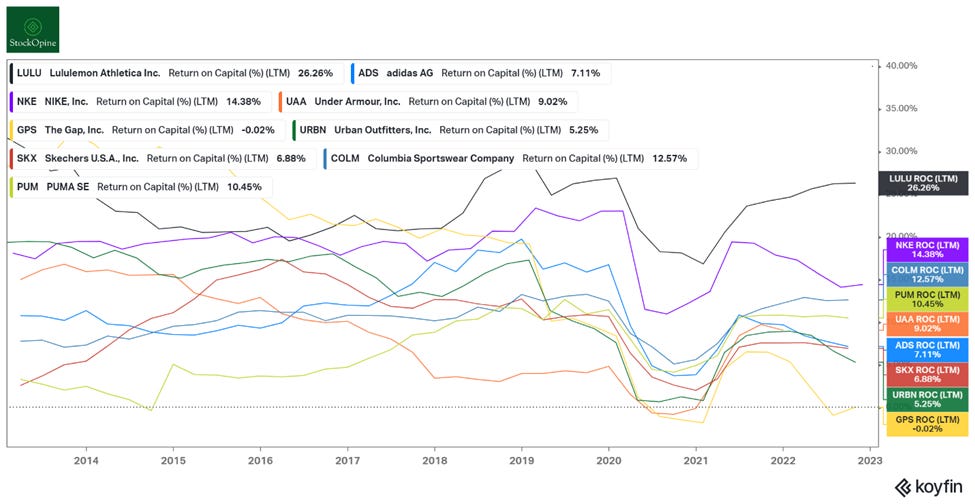

Returns on Capital

Source: Koyfin

LULU grows fast, does it profitably and as it can be seen from the above graph does it efficiently by maintaining the highest Returns on Capital in the industry. You might notice that GAP Inc. (GPS) used to be a high performer, however it was hit by the pandemic driving operating performance down. Additionally, following the implementation of accounting standards that required the capitalization of generally all leases (Right of Use assets), its capital base (due to additional ‘debt’) increased disproportionately as the majority of its business is derived from company operated stores which are leased compared to other peers with a significant portion of their business derived from wholesaling. For example, capital base of GPS increased by c.133% compared to c.20% of Nike.

5. Financial Analysis

Over the period FY12 to Q3 FY22, Lulu achieved a revenue CAGR of 19%. During this time, gross profits grew at similar pace maintain a TTM margin of 56%. During the period FY12 to FY15, operating and Free Cash Flow (“FCF”) margins declined in line with gross margins but since then there is a clear improvement. In FY21, LULU reached an operating margin of 22% and a free cash flow margin of 16%. On a TTM basis, FCF margin was negatively affected by the increase in inventory by 85%, a result of a strategic decision to build inventories and meet demand in Q4 as the business is seasonal towards the back half of the year.

In the trailing twelve months ending in Q3 2022, revenue reached $7.5B, while gross profit, operating income and free cash flow reached $4.2B, $1.6B and $92M, respectively.

Source: Lululemon Annual Reports, Koyfin, StockOpine Analysis

As explained elsewhere in the report revenue growth is driven by the increase in number of stores, revenue per store which is impacted by traffic and dollar transaction size, DTC and other offerings or channels of distribution.

The Company does not portray significant operating leverage. While sales are increasing margins slightly improved since FY15. It is worth noting that the trend is upward demonstrating product quality and differentiation. We are presuming this as we do not see any material deviation in margins that would indicate an abnormally high markdown (i.e. reduction in selling price to sell less popular apparel). With the current increase in inventory of 85% such risk does exist. Please note, that we do not imply that the Company has no markdowns as its outlets and warehouse sales are used to sell slow moving inventory and inventory from prior seasons at discounted prices.

Per the Power of Three x2 plan, management expects moderate improvements in operating margins due to the North America business, e-commerce, scale and cost efficiencies as well as moderation on airfreight costs which were affected by the supply chain disruptions.

On average, LULU generated 12% FCF margin and spent 6.6% of its revenue on CAPEX to drive growth. Going forward it expects its investment requirements to increase at 7%-9% levels to support its new growth plan (investments in distribution centers, digital, stores, technology).

LULU has Cash and Short-term investments of $353 million compared to lease liabilities amounting to $1,039 million. Cash position was abnormally low due to the investments in inventory in Q3’FY22 so as to meet demand. However, it shall also be noted that the Company has over $400M available facilities. Additionally, the company reached a high cash position of $1.26 billion at the end of January 2022.

6. Capital Allocation

LULU’s growth is purely driven organically through CAPEX investments (digital, new stores, remodel existing ones, distribution, technology etc.) with the only acquisition being MIRROR in July 2020 for net cash of $452.6M.

We do not believe that the acquisition was successful (future might prove us wrong) given that revenues are declining and considering the ongoing litigation; but at least management is cutting down on marketing expenses relating to lululemon studio showing willingness to adapt. Per the latest impairment assessment, fair value exceeded carrying amount by 4%, thus headroom is minimal and we could easily see an impairment in the near future.

LULU does not distribute dividends, however since 2012, LULU returned over $2.5 billion to shareholders through share repurchases. As of 30 October 2022, available value of shares for repurchases is $812.5M. Share repurchases are done opportunistically based on available programs approved by the Board. The Company does not seem to be the best allocator in terms of repurchases as in FY21 they repurchased the largest amount of shares (2.2M) with an average cost price of $369 whereas the purchase of 844k shares in Q4’ FY21 at an average cost of $381 stands out.

Source: Koyfin, StockOpine analysis

Despite the weaknesses identified above, LULU still generates the highest Returns on Capital in the industry and generates Returns on Equity of over 30% since FY18.

7. Competitive advantages, Opportunities and Risks

Competitive advantages

Other than quality and product innovation which brings guests to LULU, a differentiating factor is the connection with its guests. The 1,500 ambassadors around the globe create a sense of community, the 20,000 educators across the globe assisting guests when they interact with products create a unique experience and using DTC to understand customers while receiving direct feedback creates a deep relationship with customers. Having the Sweat collective program (fitness instructors, gym owners, personal trainers, athletes, coaches etc. are eligible to participate) also helps the Company to get feedback on how to improve designs which leads to product innovation. The strength of such relationships and the ability to innovate was demonstrated during the pandemic.

Opportunities

In a nutshell, the opportunities of Lulu are presented across the board, i.e. North America, DTC channel, Men’s Products and International sales. Improving brand awareness can boost sales. As shown earlier (under Branding), the unaided brand awareness for LULU is low (US only 25% whereas it is 11% for Men, China only 7%, France and Germany <5%) leaving a significant room for expansion.

Mental wellness: Pandemic had material impact on the mental wellness of people (feeling lonely and find it hard to communicate, stress too much etc.). Per LULU’s 2021 wellbeing report, physical activity has a positive impact on mental health (70% of respondents) thus people who run, train or engage in other activities are very likely to need LULU’s products.

Active and healthy lifestyle trends drive demand for comfortable, fashionable and versatile clothing which translates to more demand for LULU’s products.

Risks

Uncertainty in macroeconomic environment, rising interest rates, inflation etc. affect both the supply side and demand side of the business. On the supply side, inflationary pressures affect among others freight and wages, impacting margins whereas on the demand side rising interest rates can reduce disposable income of customers which may cause a cut in their discretionary expenses.

Majority of its products are manufactured in Asia and the majority of fabric is sourced from Taiwan. Tensions between China and Taiwan, sporadic impositions of lockdowns due to COVID, economic instability in Sri Lanka create uncertainties that can disrupt the supply chain (as well as the demand in physical stores).

China is also a key driver of the expansion strategy as it is expected to be LULU’s second largest market. Local policies and regulations similar to zero COVID policy and tensions with US can materially distort these plans.

The abnormally high inventory to strategically position LULU in meeting future demand might be subject to markdowns (or even write-offs) if apparel becomes out of fashion/season or if customers face income disruptions due to the macro environment.

8. Valuation

The stock price as of 20th of January 2023 stands at $312.8 with a negative one-year return of 3%. The Company's market capitalization is $39.9B and it trades at an EV/EBITDA TTM multiple of 21.7x. Based on our DCF valuation, the estimated price of Lululemon is $322, slightly higher than its current price by 2.9%, with an expected IRR over a 5-year period of 10.8%.

Source: StockOpine analysis

To estimate the fair value of Lulu, we assumed a revenue CAGR of 15.3% in line with analysts’ expectations. This results to a revenue of $12.7B which is slightly higher than the $12.5B set under the Power of Three x2 plan. We do not think that this is aggressive, since under the reigns of the same CEO, LULU managed to beat its prior 5-year plan earlier than expected (except for international sales, though it’s on track). The potential expansion is further supported by the sizable untapped market (i.e. $650B internationally) and the athleisure industry expectations of 8.9% CAGR until 2030.

In terms of profitability, we used an average and terminal projected EBITDA margin of 25.1% and 24%, respectively. The average EBITDA margin is in line with the 5-year average EBITDA margin of 25%. Although management expects an annual moderate expansion in operating margin, which makes sense given its expected increase in scale and the potential normalization of headwinds such as FX or supply chain disruptions, we decided to take a slightly more conservative stance as we expect the use of traditional marketing approaches to add some pressure on margins.

To derive the free cash flows to the firm we deducted projected Capex requirements of 7.9% of revenue in line with the mid-point of management expectation under Power of Three x2 plan (7%-9%) which is slightly higher than its 5 year average of 6.6%.

In terms of the terminal EV/EBITDA multiple, we assumed a value of 18.4x which although equals to a 15% haircut from its current multiple of 21.7x (and lower than its 5-year average of 26.2x) it is slightly higher than the average of 17.9x of selected peers (Nike, Adidas, Skechers, Under Armour, Puma). The Company deserves a premium but as the competition in the athleisure place gets more intense it is likely to see multiples declining. Given that this assumption is critical to the valuation, the sensitivity analysis below provides a more holistic picture of possible outcomes.

To calculate the value per share we used the minimum required return that we aim to obtain from our investments (i.e., 10%) under the current environment, adjusted for net debt and non-operating assets / liabilities identified and thereafter divided the resulting value by the number of shares.

Based on these calculations and assumptions (which may not materialize), we estimate a value per share of $322, which is higher than the current price of $312.8, resulting to an IRR over a 5-year period of 10.8%.

Sensitivity analysis

The below table gives an indication of the potential upside/(downside) %age compared to the current price ($312.8 as of 20th January 2023) when the terminal multiple and the discount rate are changed.

Source: StockOpine analysis

9. Concluding Remarks

LULU operates in a highly fragmented market, though, we believe that its first mover advantage in the athleisure space, the quality of its products and its approach on reaching the customer directly and blending in/cultivating the community (rather than pure wholesaling), allow the firm to build strong relationships with guests and strengthen its brand positioning. Considering its debt-free capital structure, the Company has ample space to fund its growth plans and its product innovation processes therefore fulfilling customer unmet needs.

Under the reigns of Calvin McDonald, LULU can exceed the targets set under the Power of Three x2 plan and can capitalize on the untapped international market opportunity of $650B; outgrowing its peers, maintaining the best in class margins and generating outstanding returns for its shareholders.

You can find us at Commonstock and on Twitter @StockOpine.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward-looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

This post may contain affiliate links, which means that we might get a commission if you decide to sign-up using any of these links. No extra cost is charged to you.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.

Also, given the revenue per store trend, and given that the company projects 15% revenue with similar square footage growth - are they not implicitly assuming that revenue per sq ft will remain constant? May DTC pick that up a bit. What is your 5 year out store count? And any thoughts on capex per store?

Also, what are your thoughts about the declining revenue per sq ft?

“However, in recent years, revenue per square foot in the retail space has declined. From $1,595 in 2018, this metric declined to $1,425 in 2019 and it further dropped down to only $755 in 2020. However, this figure increased to $1086 in 2021, due to increased economic activity after a long period of stores shutdown during the onset of pandemic.”