“It is a testament to the strength of our brand that for the full year 2022, we were able to significantly exceed our annual revenue goal and deliver adjusted operating margin in line with our target.” Calvin McDonald, CEO

On March 28, Lululemon (‘LULU’) reported their Q4 and full-year fiscal 2022 results, which exceeded both consensus and their own revenue guidance. This outstanding performance was reflected in the stock price, with LULU 0.00%↑ opening 14% higher the next day.

It has been one year since LULU laid out its Power of Three x2 plan for FY26, and it already appears that the company is overachieving on its targets. For those who are not familiar with the Power of Three x2, here's a brief overview: In 2019, the company announced the Power of Three plan, which aimed to double its net revenue by 2023. The company achieved this goal ahead of schedule. In 2022, the company launched a new five-year growth plan, the Power of Three ×2, which focuses on the same three key pillars as the previous plan: doubling men's product revenue, doubling DTC (direct-to-consumer) revenue, and quadrupling international revenue by 2026, while continuing to grow women's products and North America at double-digit rates. For more details on this you can visit our in-depth research report on $LULU published in January 2023.

Revenue and Profitability

Source: Koyfin, StockOpine analysis

In FY 2022, LULU's revenue increased by 30% to $8.11B, or 32% on a constant currency basis. This was on top of the impressive 42% growth achieved in FY 2021. The primary drivers of revenue growth were DTC, which increased by 33%, and company-operated store revenue, which grew by 29%. It shall be noted that the Company opened 81 net new company-operated stores (‘COS’) during the year, ending with 655 stores while comparable store sales were up 16%, or 19% on a constant dollar basis.

Despite the strong revenue growth, gross margin decreased by 230 basis points to 55.4% on a GAAP basis. Part of the decrease was due to a provision of $62.9 million recognized against MIRROR hardware inventory, which was incurred as a result of the impairment charge in Q4’22. Adjusting for the obsolescence provision, gross margin for the year would have been 56.2%, i.e. 150 basis points lower than FY 2021, due to higher markdowns, changes in sales mix, higher costs related to product development and distribution centers, and FX headwinds. Nonetheless, we are not overly concerned about gross margin, as management expects to return to FY 2021 levels.

“For the full year, we forecast gross margin to increase between 140 to 160 basis points versus 2022. The expansion relative to last year was driven predominantly by lower air freight expense. For the full year, we expect air freight to be down approximately 150 basis points versus 2022. ” Meghan Frank, CFO

Although GAAP operating income for the year remained flat at $1.328 billion compared to $1.333 billion in FY21, it was significantly impacted by the impairment charges of $471 million related to MIRROR acquisition. Adjusting for the MIRROR impairment charges, operating income increased by 30% to $1.8 billion (adjusted FY21 operating income of $1.38 billion), while adjusted operating margin was stable at 22.1%.

A New Strategy for Lululemon Studio (formerly known as MIRROR)

LULU’s growth was purely driven organically through CAPEX investments with the only acquisition being MIRROR in July 2020 for net cash of $452.6M. Unfortunately the acquisition was unsuccessful as management overestimated the future opportunity of the at-home/connected fitness space in a post-pandemic era. As a result, during the fourth quarter of 2022, LULU recognized post-tax impairment and other charges related to MIRROR totaling $442.7 million.

Back in January, in our LULU report we highlighted:

“We do not believe that the acquisition was successful (future might prove us wrong) given that revenues are declining and considering the ongoing litigation; but at least management is cutting down on marketing expenses relating to lululemon studio showing willingness to adapt. Per the latest impairment assessment, fair value exceeded carrying amount by 4%, thus headroom is minimal and we could easily see an impairment in the near future.”

The impairment was due to revised future expected cash flows as sales of hardware units did not meet Q4 expectations while Customer Acquisition Cost remained higher than expected.

To address this, management decided to pivot away from the hardware-centric business of MIRROR and focus on a more efficient app-based model. The revised strategy involves a two-tier membership program. The Essentials program which was launched in North America in October 2022 and is offered to guests at no cost, had 9 million members enrolling in the first 5 months, significantly exceeding management's expectations. The free membership tier provides benefits such as early access to Lululemon products and select Lululemon studio content.

LULU will also launch a new (3rd tier) paid tier of Lululemon studio this summer. The new app-based model will be offered at a lower monthly subscription rate, and management expects this move to expand their total addressable market for potential members. App-based means to be able to access the digital fitness content via the app rather through hardware. Through these initiatives, management aims to build a community that will drive engagement, incremental purchases, and new guest acquisition.

Power of Three x2

Based on Power of Three x2, management expects to generate a revenue CAGR of 15% reaching total sales of approximately $12.5B in FY 26 compared to $6.25B in FY 21.

Direct to consumer

LULU's direct-to-consumer segment continued to be the top performer, with a 33% revenue increase for the year, or 35% on a constant currency basis. Given this growth, achieving the target of doubling revenue by FY26 seems highly feasible.

“In stores, traffic increased over 30%; and in our digital business, traffic to our e-commerce sites and apps globally increased over 45%. On a 3-year CAGR basis, traffic is up 7% in stores and 40% in e-commerce. This speaks to the strength of our omni-operating model as we engage with our guests in ways most convenient to them.” Meghan Frank, CFO

Source: Stratosphere.io, StockOpine analysis

Men’s products

Men's revenue growth remained strong, increasing by 27% and keeping the company on track to double revenue by FY26. However, in Q4'22, growth decelerated to 22% compared 28% in Q3'22.

Source: Stratosphere.io, StockOpine analysis

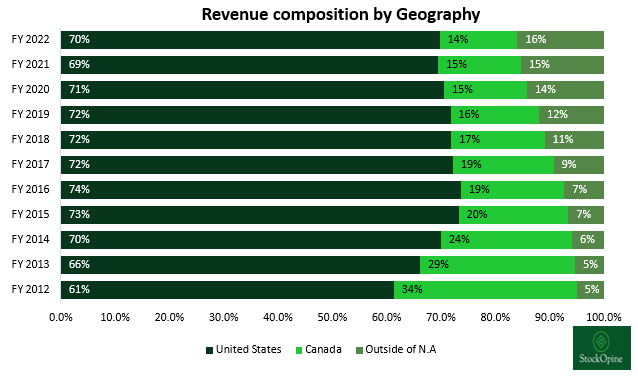

International

LULU's international segment saw a 35% revenue growth in both Q4'22 and FY 22, while North America recorded a 29% revenue increase during the same period.

Management sees a significant opportunity in China with momentum picking up despite COVID-19 impacts. Even though COVID-19 affected revenue in December, revenue in China grew over 30% year-over-year in Q4’22 and over 50% on a 3-year CAGR basis. To reinforce LULU’s commitment to the market, the company recently opened its largest store in Asia Pacific, in Shanghai, bringing its store count in China to 99, compared to 70 stores in January 2021.

With a 35% annual growth rate, LULU is on track to achieve the target of quadrupling international sales by FY26.

Source: Stratosphere.io, StockOpine analysis

Market Share Gains

LULU’s CEO, Calvin McDonald, highlighted that despite a 5% decrease in the U.S. adult active apparel industry revenue compared to the same period last year, LULU gained 2.3 points of market share, the highest among all brands in the market, according to NPD Group's consumer tracking service.

Additionally, brand awareness around the world continues to improve.

“We added 5 points to our unaided awareness in Australia from 19% to 24%, 2 points in China from 7% to 9% and 2 points in the U.K., taking us to 16% in the market.”

If you recall from our write-up in January, raising brand awareness is a key opportunity for LULU and we are satisfied to see this progress.

Cash Position, Inventories and Share Repurchases

CASH: With $1.155 billion in cash and cash equivalents compared to nil debt (other than $1.1B lease liabilities), as well as almost $400 million of available liquidity under its revolving credit facility, the company has sufficient resources to fund its growth.

INVENTORY: LULU's inventory balance was $1.4 billion, which is a 50% increase from the previous fiscal year and below management expectations. The rate of growth decelerated from the 85% increase seen in Q3'22, though, inventory growth is expected to exceed revenue growth in the first half of 2023. Management anticipates that the growth rate will align with revenue growth in the second half of the year indicating that inventory levels are on track to normalize.

SHARE REPURCHASES: During the year, the Company repurchased 1.4 million shares at a total cost of $444 million, implying an average price of $317. This compares to 2.2 million shares repurchased in FY 21 at a total cost of $812.6 million, implying an average price of $369. Even though share repurchases may not always be an accurate reflection of a company's ability to allocate capital, the fact that the Company repurchased larger amount of shares at higher prices in FY 21 is a negative sign.

Outlook

For 2023, LULU's management expects revenue to be within the range of $9.3 billion to $9.41 billion, surpassing the $9.2 billion we had initially estimated in our valuation model in January. This range represents a growth rate of 15% to 16% compared to 2022.

Operating margin for FY’23 is expected to increase by 20 to 40 basis points compared to 2022, indicating an operating margin of 22.3% to 22.5%.

Concluding Remarks

After reviewing LULU’s Q4 and full-year fiscal 2022 results, it is clear that the company has executed while it continued to gain market share and enhance its brand awareness. Despite the impairment charge on lululemon studio, the achievement of the Power of Three x2 plan appears to be highly probable.

There may be potential challenges in the macro environment and competition, yet, we maintain a positive outlook on LULU's future prospects.

If you enjoyed this memo, spread the word. It helps.

In April, we will also release detailed write-ups on FERG 0.00%↑ and WSO 0.00%↑ as well as our Quarterly Portfolio Update. If you are interested to receive the full analysis consider joining the premium tier.

You can also find us at Commonstock and on Twitter @StockOpine.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward-looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

This post may contain affiliate links, which means that we might get a commission if you decide to sign-up using any of these links. No extra cost is charged to you.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.