Luxury stocks have been on a strong run since Richemont’s earnings report on January 16. The key takeaway from Richemont? A significant acceleration in growth across all regions except Asia-Pacific, where sales declines improved from -19% to -7%. Investors took this as a sign that luxury demand may have bottomed after a challenging 2024, sparking renewed confidence in the sector.

Source: Koyfin (affiliate link with a 20% discount for StockOpine readers)

Then came LVMH’s Q4 earnings on January 28. While the results showed broad-based improvements, except in Wines & Spirits - the stock opened down 4%. The likely reason? Expectations were already priced in, and growth wasn’t as exciting as Richemont’s.

However, comparing the two isn’t entirely fair. LVMH has a different revenue mix, and despite more modest growth, the overall takeaway remains positive: Luxury demand appears to have bottomed in Q3’24, setting the stage for a stronger 2025. In Q4’24, LVMH returned to growth even though organic growth stood at the modest of 1% (Vs -3% in Q3).

Source: StockOpine Analysis, FinChat.io (affiliate link with a 15% discount for StockOpine readers)

1. A Closer Look at the Numbers

LVMH reported €84.7B in revenue for FY24 (-1.7% YoY, but +1% organic growth). The company faced three headwinds, all of which were industry-wide, not company-specific:

Weak consumer sentiment in China, which impacted all segments.

Tough post-pandemic comparables, with organic growth soaring 21.6% CAGR from FY20-FY23, far above the pre-COVID average of 9%.

Ongoing struggles in Wines & Spirits, which weighed on revenue and profitability.

Source: StockOpine Analysis, Koyfin (affiliate link with a 20% discount for StockOpine readers)

Operating profit declined 14% YoY, with operating margins falling to 23.1% in FY24 (from 26.5% in FY23), mainly due to:

Lower gross margins (-1.8pp) as LVMH absorbed higher costs of labour, FX and one-off accounting adjustments, without price increases.

Higher marketing & G&A expenses (-1.7pp impact).

However, management was clear: The margin decline isn’t structural as they chose not to cut costs aggressively to preserve long-term growth. This suggests margin recovery as revenue growth accelerates in 2025.

“So from a management point of view, that was a bit of a dilemma insofar as we could have been more active on taking costs down, and that would have meant that we were saying that the crisis was structural. But it isn't, it is circumstantial and we have to be able to react and we wouldn't want to damage our potential budget or marketing budgets for later. So we have to strike a balance. I think we sort of managed. We have contained cost increase, not quite to the same tune as the drop in revenue, which has led to some profit drops in some businesses but it's not that bad overall.” Jean-Jacques Guiony

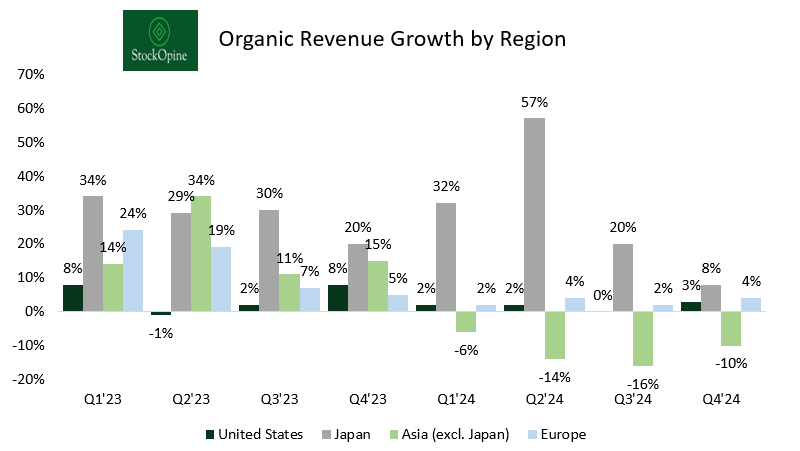

2. Regional Trends

Momentum picked up across most regions in Q4:

US growth accelerated to +3% in Q4’24 (vs. 0% in Q3), with strength in Fashion, Jewelry, and Sephora.

Europe rebounded to +4%, led by Fashion & Leather.

Japan slowed to +8%, due to tough comps.

Asia (ex. Japan) declined -10% YoY (vs. -16% in Q3). Gradual improvement but still weak.

Source: StockOpine Analysis, FinChat.io (affiliate link with a 15% discount for StockOpine readers)

Is China improving? While uncertainty remains, early signals are encouraging:

Richemont’s sales decline in Asia improved from -19% (Q3) to -7% (Q4), which shows improvement in this market.

LVMH’s Asia (ex. Japan) revenue decline also improved from -16% to -10%.

China stimulus measures could help restore consumer confidence.

Bernard Arnault acknowledged the challenges but remained optimistic:

“As for China, I believe that the Chinese government is now aware of the fact that they need to kickstart the economy. The economy needs to recover and therefore, a few plans have been announced to just help the economy. That's the first thing. The second thing, our high-quality products are still extremely desirable in China. People still want to buy our products. The environment was severely impacted by COVID. Then there was a strong recovery followed by another crisis, the real estate crisis. So it's going to take some time.”

3. Segment Breakdown: Where’s the Growth?

Wines & Spirits

LVMH’s Wines & Spirits division continued to struggle, posting an -8% organic revenue decline as weak demand in China and the US weighed on results. Cognac sales were particularly weak, while champagne and wines held up slightly better. These challenges are not unique to LVMH, as competitors like Diageo and Brown-Forman have reported similar headwinds. Looking ahead, LVMH’s CFO Jean-Jacques Guiony will now personally oversee Moët Hennessy, signaling a strong internal push to turn the segment around.

Fashion & Leather

In contrast, Fashion & Leather Goods, LVMH’s largest and most profitable segment, showed signs of stabilization. After posting a -5% organic revenue decline in Q3, the negative growth decelerated to -1%. Growth in Europe and the US helped offset continued softness in Asia.

Perfumes & Cosmetics

Perfumes & Cosmetics had +2% organic growth in Q4, slightly slowing from +3% in the previous quarter. Despite the modest deceleration, Dior’s Sauvage and Miss Dior remain the world’s best-selling fragrances, reinforcing the segment’s strong brand equity.

Watches & Jewelry

Watches & Jewelry returned to +3% organic growth after a -4% decline in Q3. In Q4, Tiffany delivered 9% organic growth, with profits doubling compared to pre-acquisition levels. Meanwhile, TAG Heuer signed a 10-year deal as the official timekeeper of Formula 1, alongside Moët & Chandon and Louis Vuitton.

Selective Retailing

Finally, Selective Retailing, which includes Sephora and DFS, was the best-performing division. Organic revenue growth accelerated to +7% in Q4, up from +2% in Q3. Sephora, in particular, continued its exceptional run, delivering double-digit revenue and profit growth.

“We are the first perfume and cosmetics retailer in the U.S. for Selective Retailing in the U.S. and in many countries.”

“In 1998, it was about EUR 100 million of revenue, something close to that. And now Sephora revenues stand at more than 10x that. Let me count. Yes, a lot more. I can't give you all the figures because you would not believe them.” Bernard Arnauld

DFS still faces challenges especially in Hong Kong and Macau which makes considerable business of the segment. In those regions the Chinese consumer remains weak, largely impacted by the weakening of CNY.

4. Has Luxury Officially Bottomed?

This quarter suggests luxury demand has stabilized, with improvement across most segments except Wines & Spirits. However, Chinese consumer demand remains fragile.

Looking ahead to 2025, LVMH does not provide financial guidance, but Bernard Arnault’s comments were notably bullish, stating:

“And as I said earlier, in 2025 -- well, 2025 is starting rather well with quite a few companies -- well, I mean, it is January, end of January so let's not anticipate too much, but we have quite a few companies that reported double-digit growth. Louis Vuitton, since you're here, or Tiffany, which both reported a double-digit growth since the beginning of the year.”

5. Conclusion

We’re pleased with the latest quarter's results and industry signals indicating stabilization and potential acceleration, which should help LVMH's margins recover. Regarding China, we believe stimulus measures will eventually support the consumer. The main concern remains the alcohol segment, which has yet to recover.