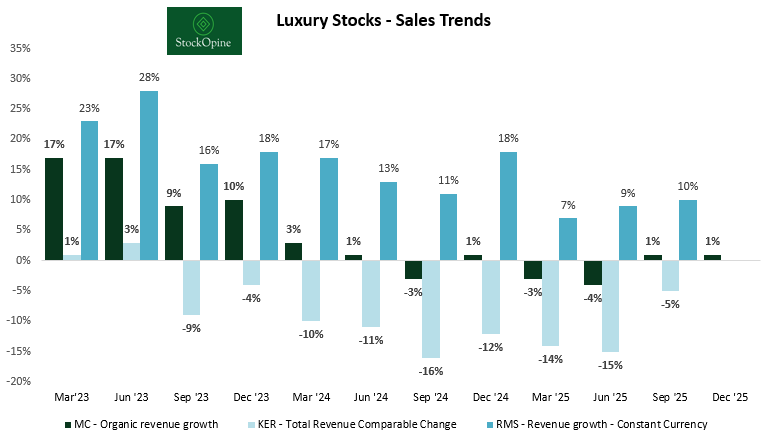

We are now deep into the second year of the fashion luxury industry downcycle, and it feels like a never-ending story. The silver lining? LVMH is not suffering in isolation. The Group performed significantly better than its closest competitor, Kering, confirming that these headwinds are industry-wide rather than company-specific. Of course, we must exclude the ultra-premium outlier, Hermès, from this comparison. Their ability to sustain positive revenue growth serves as a testament to the fact that ultra-premium scarcity is far more recession-resistant than broader luxury.

Source: StockOpine Analysis

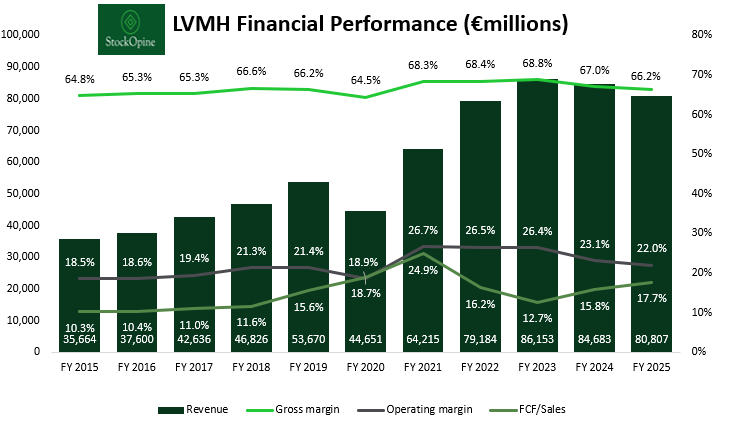

During periods of stagnant growth, operating deleverage kicks in, and this is exactly what we are seeing right now at LVMH. Operating margin has declined from 26.5% in FY23 to 22% in FY25. However, despite the cycle, management has managed to keep operating margins above pre-COVID levels.

What does this tell us? We believe LVMH is currently under-earning. As the cycle turns and the Group returns to organic growth of at least mid-single digits, operating leverage should kick back in, allowing profit margins to expand from here.

Nevertheless, we remain in a stagnant period and have not yet seen definitive signs of the cycle turning, with various external factors still in play (geopolitics, FX, tariffs). Without overwhelming you with macro thoughts, let’s dive into LVMH’s FY25 results.

1. A Closer Look on FY25 Numbers

LVMH reported €80.8B in revenue for FY25 (-5% reported, -1% organic). The year was characterized by what Bernard Arnault described as a “winter” for the industry, driven by three major headwinds:

Currency headwinds: A negative FX impact of -3% on revenue and -€1 billion on operating profit, as the Dollar, Yen, and Renminbi weakened against the Euro.

Geopolitical and Economic uncertainty: Including trade tensions (tariffs on Cognac in China and the US) and tax increases in France.

Cyclical normalization: Following the post-COVID boom, demand has softened, particularly in Wines & Spirits.

Operating profit declined 9% YoY to €17.8B, with operating margins compressing to 22.0% (from 23.1% in FY24). The decline was primarily driven by:

Gross Margin pressure: Down 6% YoY, falling to 66.2% of revenue.

Currency impact: A substantial €1.06 billion negative hit to recurring operations. Almost 60% of the operating profit decline was FX-related.

Strategic Spend: Despite the downturn, management maintained marketing and selling expenses at 37% of revenue to preserve brand desirability rather than slashing costs to boost short-term earnings.

“I believe we can say more seriously that the results of the group are solid in a rather challenging, disrupted climate economically... 2026 won’t be simple either, but one thing at a time.” Bernard Arnault, CEO.

Source: StockOpine Analysis

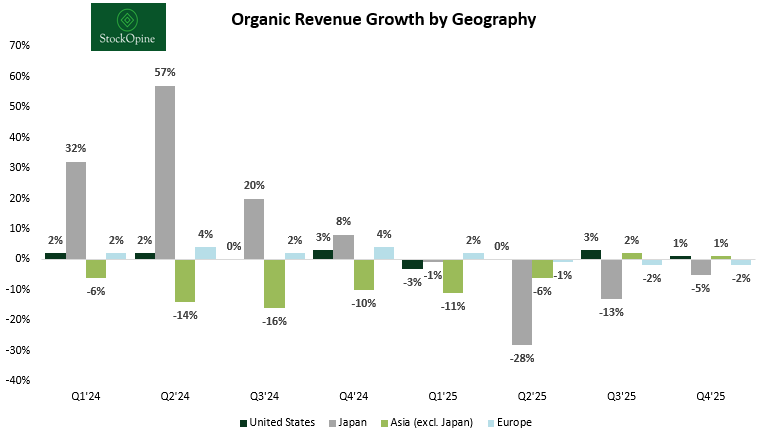

2. Regional Trends

Despite a negative full-year organic print (-1%), momentum shifted positively in the second half of the year. H2 organic growth rebounded to +1%, signaling a potential stabilization.

United States: Growth was flat during the year but accelerated in H2 as the dollar weakened, encouraging domestic spending over tourist spending abroad.

Europe: Saw a reverse trend; growth was stronger in H1 due to tourism but softened in H2. Overall, Europe organic revenue declined by 1% in FY25.

Japan: Revenue declined by 12% as a result of tougher comps.

Asia (ex-Japan): Remained under pressure, declining 4% over the year but returned to growth in the second half of the year after 6 consecutive quarters of decline.

Source: StockOpine Analysis

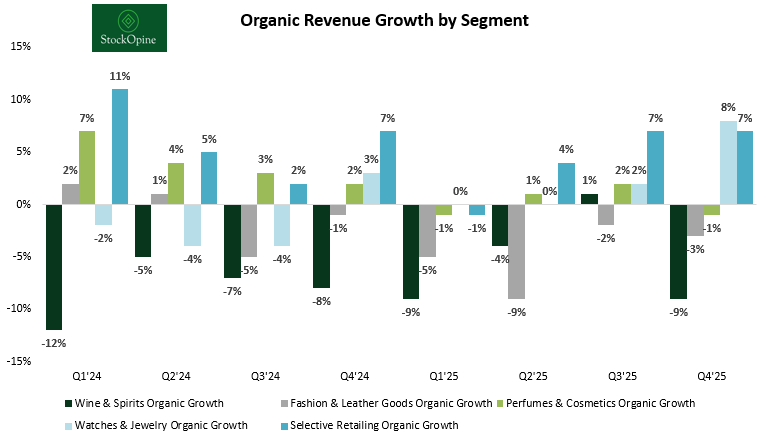

3. Segment Breakdown: Divergent Fortunes

With the exception of Wines & Spirits, all remaining segments showed improvement in the second half of the year. However, only Watches & Jewelry and Selective Retail delivered positive consecutive growth in both Q3 and Q4.

Source: StockOpine Analysis

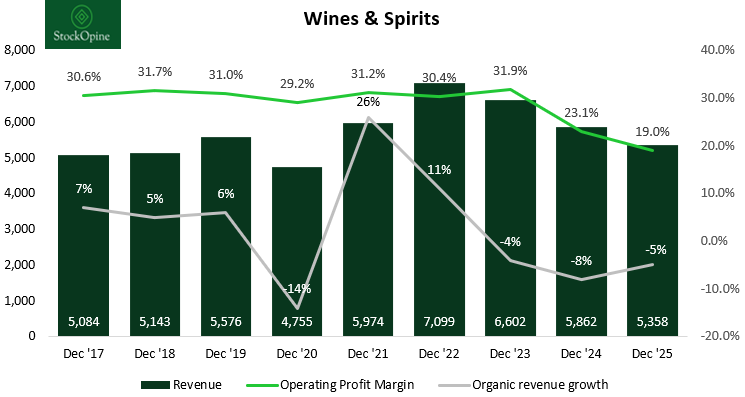

Wines & Spirits

This segment remains the hardest hit, posting a -5% organic revenue decline. This marks the third consecutive year of organic revenue decline. For years, this segment enjoyed a stable 30% operating profit margin with top-line growth in the mid-single digits. Now, a decline in spirits which could potentially prove structural is being supercharged by tariffs.

Cognac: Significantly impacted by trade tariffs and weak demand in China and the US. Organic revenue decline was -12% YoY for the category.

Champagne: Held up better with resilient sales, aided by Moët & Chandon’s renewed Formula 1 partnership. Organic growth for Champagne and Wines was flat YoY.

Profitability: Margins collapsed to 19.0% (vs 23.1% in FY24).

Source: StockOpine Analysis, Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Fashion & Leather

The core engine of LVMH saw -5% organic growth. Profitability remained best-in-class with a 35.0% operating margin, which is above pre-covid levels but below last year’s 37.1% (and the ~40% peak levels seen in FY21/FY22). Despite the negative full-year organic figure for the segment, Bernard Arnault noted that Louis Vuitton and Christian Dior both grew “quarter after quarter from Q1 to Q4”

Louis Vuitton: Continued to innovate with unique initiatives like the “Vuitton Ship” in Shanghai and a new high-end makeup line.

Dior: Benefited from a “creative renewal” following successful shows in early 2026.

Source: StockOpine Analysis, Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

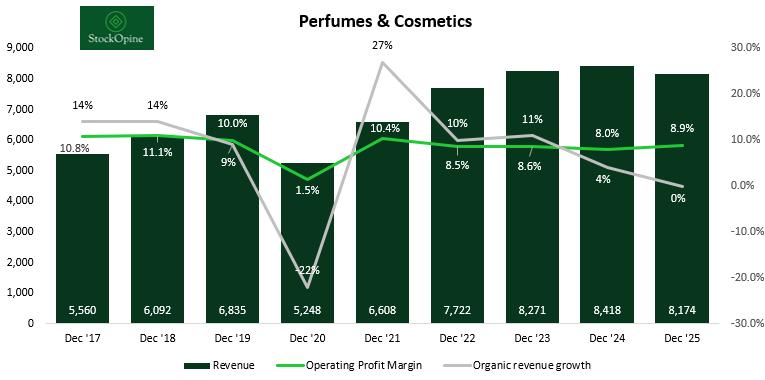

Perfumes & Cosmetics

Organic growth was flat (0%), but the segment outperformed on profitability, with operating profit up 8%.

Dior: Sauvage remains the world’s best-selling men’s fragrance, and Dior lipsticks are sold “every 2 seconds”.

Strategy: The focus on selective distribution helped margins rise to 8.9%.

Source: StockOpine Analysis, Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

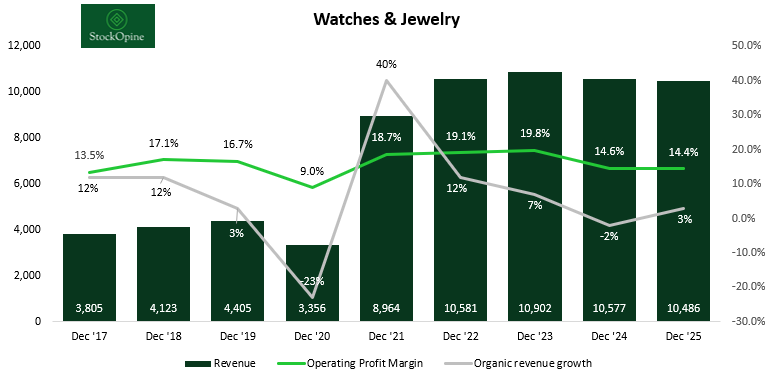

Watches & Jewelry

This segment was a bright spot, flipping to +3% organic growth (vs. declines previously). Notably, organic revenue growth for the segment acceleraed to 8%YoY in Q4’25.

Tiffany & Co.: The elevation strategy is “bearing fruit” with a massive transformation plan involving store renovations and a push into high jewelry (shifting focus from silver to gold).

Bvlgari: A standout performer achieving "another record-breaking year" in 2025.

Source: StockOpine Analysis, Fiscal.ai (affiliate link with a 15% discount for StockOpine readers)

Selective Retailing

The Star Performer Sephora continues to be the “unchallenged world leader” in beauty retail.

Performance: The division delivered +4% organic growth and 28% jump in operating profit.

DFS: LVMH is actively exiting this business, having sold a majority stake to focus on more profitable ventures. DFS accounted for 1.8% of LVMH’s total revenue in FY25.

4. Conclusion

LVMH is navigating a “winter” cycle, but the business remains significantly profitable and cash-generative. Despite lower profitability, they generated €14.3B in free cash flow (+6.8% vs. FY24) by better controlling CAPEX and working capital.

Management offered a “reserved” outlook for the short term in 2026 due to geopolitical headwinds but remains optimistic for the medium term. A key highlight for investors is the Arnault family’s conviction: The family is set to cross the 50% ownership threshold in 2026, reinforcing their long-term commitment.

“A family group isn’t riveted to the quarterly results... We create product for the long term and we’re not mesmerized by what’s going to happen in the coming quarter.” Bernard Arnault.

With H2 organic growth turning positive (+1%), LVMH appears to be forming a bottom. However, this recovery may take longer than expected given the persistent challenges in the external environment.

At current levels, the stock trades at 16.2x NTM EV/EBIT and an FCF/EV yield of 4.9%. These are multi-year low valuations in a downcycle where LVMH is likely under-earning. In that respect, we remain long at these levels and may even consider increasing our position if the stock falls further.