Meta reported its Q4 2024 results on January 29th after the bell, and investors seem to have reacted positively. However, a key concern arises: Are the 2025 CAPEX and OPEX forecasts of $60B-$65B and $114B-$119B, respectively, too high? Let's consider this: 2024 revenues were $164.5B, and assuming a 15% growth, we get to $189.2B, just enough to cover the higher end of the combined OPEX and CAPEX figure of $184B. Is this too concerning? Let’s unpack it.

1. Key Highlights

Q4'24 Revenue: $48.4B, up 21% YoY, surpassing the guidance high of $48B and analysts’ estimate of $47B. Full-year revenue for 2024 reached $164.5B, a 22% increase.

Outlook: Q1’25 revenue guidance is $39.5B-$41.8B, reflecting an 8-15% YoY increase with around a 3% FX headwind.

Operating Income: $23.37B, up 43% YoY, exceeding estimates of $19.8B. Operating margin improved to 48%, up from 41% in Q4'23. Full-year operating income for 2024 rose to $69.4B, a 48% increase compared to $46.8B in 2023.

EPS: $8.02 for Q4'24, up 50% YoY, beating estimates of $6.74. Full-year EPS for 2024 increased to $23.86, a 60% rise compared to $14.87 in 2023.

Source: Finchat.io (15% discount for StockOpine readers) StockOpine analysis

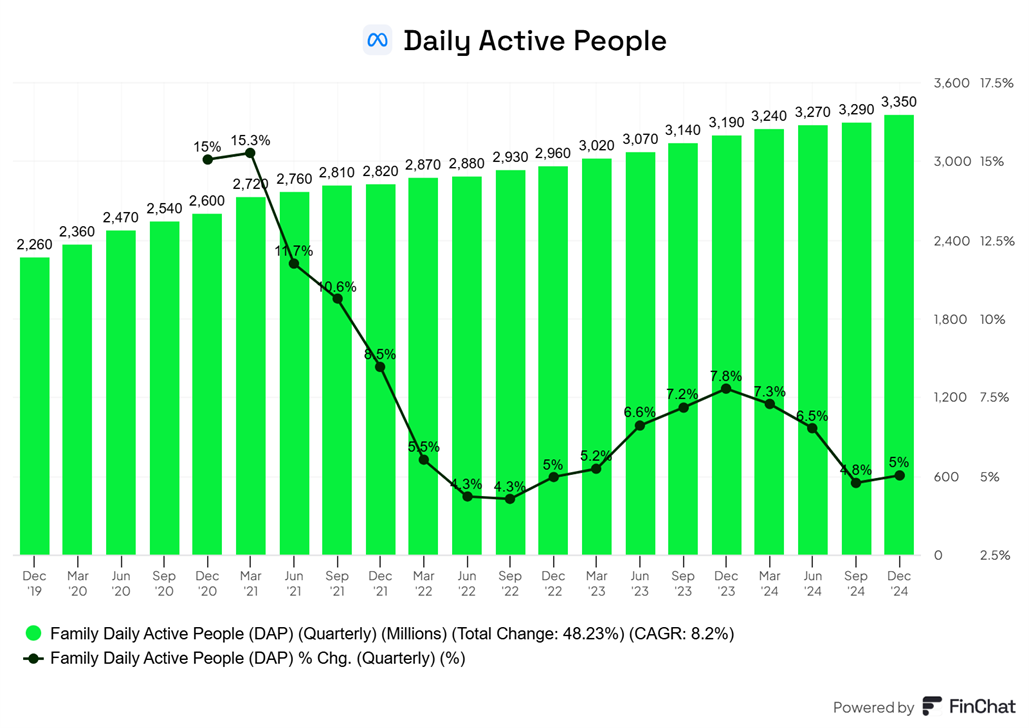

2. Engagement

Core business: Meta's Family of Apps reached 3.35 billion Daily Active People (DAP), a 5% increase, indicating that its apps remain relevant.

Threads: Monthly actives increased to 320 million from 275 million in Q3’24. While unmonetized, Meta is testing ads, but they aren't significant yet.

“We're going to learn what's going to happen with TikTok, and regardless of that I expect Reels on Instagram and Facebook to continue growing. I expect Threads to continue on its trajectory to become the leading discussion platform and eventually reach 1 billion people over the next several years.” Mark Zuckerberg, CEO

Source: Finchat.io (15% discount for StockOpine readers)

WhatsApp continues to gain market share in the US, surpassing 100 million monthly active users. Family of Apps' other revenue grew by 55%, reaching $519 million, driven by business messaging growth (Click-to-WhatsApp Ads, paid messaging) on the WhatsApp Business platform, highlighting strong monetization. Susan Li also mentioned that most of the engagement for Meta AI currently comes from WhatsApp, further positioning the platform as a key driver for future revenue growth.

Source: Finchat.io (15% discount for StockOpine readers)

Other important metrics shared during the call that highlight solid product performance and strong engagement. Susan Li, CFO, noted

“In Q4, global video time grew at double digit percentages year-over-year on Instagram, and we’re seeing particular strength in the US on Facebook, where video time spent was also up double digit rates year-over-year.”

“Reels are already reshared over 4.5 billion times a day, and we’ve been introducing more features that bring together the social and entertainment aspects of Instagram.”

While video is a lower-monetization feature today, Meta follows the strategy of expanding first, then monetizing.

We also noted the launch of a new app ‘Edits’ that provides suite of creative tools allowing creators to create Reels on the phone. That should keep creators engaged within its ecosystem and that should help in retaining users’ attention in the apps (which ultimately drives ad revenue).

Meanwhile, Meta is also supporting advertisers with tools like Andromeda, Advantage+ creative and Advantage+. Advantage+ increases automation for ad campaigns, and Susan Li shared that:

“Adoption of Advantage+ shopping campaigns continues to scale, with revenue surpassing a $20 billion annual run-rate and growing 70% year-over-year in Q4.”

“More than 4 million advertisers are now using at least one of our generative AI ad creative tools, up from one million six months ago.”

All these findings highlight Meta's ongoing focus on enhancing both user and creator experience, while also building out its advertising capabilities to drive sustained growth.

Curious about what Zuck said on AI and CAPEX? Want to see how we factor it into our reverse DCF to estimate the 10-year growth needed to justify today’s price? Become a paid subscriber today!