META – Can it go lower, or did we hit a bottom?

Meta reported its Q3 results on 26 October 2022, and the stock had a 1-day reaction of -24.5% (fell from c. $130 to c. $98). Since then, the share price of META 0.00%↑ has recovered some of its losses and stands at $114.22 (14th of November 2022) and trades at a Trailing Twelve Months (“TTM”) EV/EBITDA of 6.3x and P/E of 10.9x compared to 5-year averages of 16.9x and 28.0x, respectively.

In this memo we will briefly discuss the Q3’2022 earnings and would subsequently run 3 stress scenarios to evaluate whether the value assigned to $META by the market is reasonable. These scenarios do not predict the future but rather stress (in our opinion) the downside.

1. Key Highlights

Firstly, we will share what happened in the latest quarter and give some context on the outlook provided by management.

Revenue for Q3’22 of $27.7B (down 4% compared to Q3’21) beating estimates by $314M and mid-point guidance provided by $460M. It is worth noting that Q3’22 had an FX impact of negative $1.79B which would translate into $29.5B (or 1.7% higher than Q3’21). Despite this, competitors did better than META on relative terms.

GOOGL 0.00%↑ advertising revenue for the same quarter grew by 2.5% (including unfavorable FX impact).

SNAP 0.00%↑ revenue increased by 6%.

PINS 0.00%↑ revenue increased by 8% (10% on constant currency).

GAAP EPS for Q3’22 of $1.64 (down 49% compared to Q3’21) missing estimates by $0.22.

Operating income $5.66B, down 46% compared to Q3’21, missing estimates by $412M. Operating margin was 20% compared to 36% in Q3’21.

Source: META Earnings presentations, StockOpine analysis

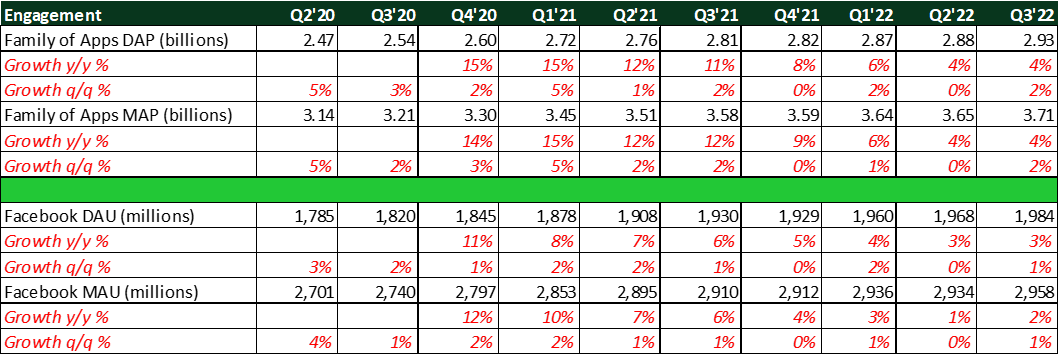

Core business is doing fine with increased engagement (Family of Apps DAP & MAP, and Facebook DAU & MAU).

Source: META Earnings presentations, StockOpine analysis

Its profitability in Q3’22 as well as the guidance for total expenses (from $85B-$87B in FY’22 to $96B-$101B in FY’23, driven by $2B charges in consolidating office facilities and accelerated cost of revenue expenses – mainly infrastructure related) and CAPEX outlook (from $32B-$33B in FY’22 to $34B-$39B in FY’23, driven by investments in data centers, servers and network infrastructure) for FY’23 frustrated investors as the capital allocation seems suboptimal. For completeness Q4’22 Revenue guidance is $30-$32.5B or a 7.2% decline y/y with a c. 7% FX headwind.

Headcount: On Q3’22 earnings call it was noted that “We expect hiring to slow dramatically going forward and to hold headcount roughly flat next year relative to current levels”, and “We are holding some teams flat in terms of headcount, shrinking others and investing headcount growth only in our highest priorities.” Dave Wehner, CFO.

Although from the above we could not interpret the massive layoffs, Meta announced on 9th of November 2022, that is letting 11,000 (or 13%) employees go (total in Q3’22 were 87,314) with Mark Zuckerberg acknowledging “I got this wrong, and I take responsibility for that. In this new environment, we need to become more capital efficient.”

Outlook changes -> Total expenses from $96B-$101B in FY’23 to $94B-$100B due to the plan of adding fewer employees than previously expected and CAPEX from $34B-$39B in FY’23 to $34-$37B.

Reality labs is ‘burning’ money, $12.8B operating losses on a TTM basis with CFO noting “We expect Reality Labs expenses will increase meaningfully again in 2023” however from 2023 onwards the plan seems less aggressive “More broadly, beyond 2023, we expect to pace Reality Labs investments to ensure that we can achieve our goal of growing overall company operating income.”

Whether this is a fad or not it cannot be predicted with certainty, but Zuckerberg is not alone.

"This quarter we took action to further focus our business on our three strategic priorities: growing our community and deepening their engagement with our products, reaccelerating and diversifying our revenue growth, and investing in augmented reality," said Evan Spiegel, Snap Inc. CEO.

Reels

“This of course includes Reels, which continues to grow quickly across our apps -- both in production and consumption. There are now more than 140 billion Reels plays across Facebook and Instagram each day. That's a 50% increase from six months ago. Reels is incremental to time spent on our apps. The trends look good here, and we believe that we're gaining time spent share on competitors like TikTok.” & “On Instagram alone, people already reshare Reels 1 billion times a day through DMs.” Mark Zuckerberg, CEO

In terms of advertising revenue: Per last quarter Instagram Reels crossed $1B run rate. Per current quarter Instagram and Facebook combined reached $3B run rate.

WhatsApp

Relating to Click-to-messaging ads “Click-to-WhatsApp just passed a $1.5 billion run rate, growing more than 80% year-over-year.” Mark Zuckerberg, CEO. META also started tapping into paid messaging (they see a big opportunity here) and launched JioMart on WhatsApp in India (chat-based commerce).

2. Stress scenarios

In this section we run 3 rather bear case scenarios to assess how much Meta can go down and what inputs will result to such unfavorable outcomes.

FY’23 Inputs

The input for Revenue of FY’23 was $115.4B in line with FY’22 estimated revenue, provided Meta generates $31B in Q4’22 (guidance of $30B-$32.5B). This figure is well below the $123.4B FY’23 estimate of analysts provided by Koyfin.

Advertising /FoA revenue FY’23 of $113.5B with an operating margin of 37%, the lowest margin achieved in latest years and c. 100bps lower than our estimate for FY’22 (average margin for 2019-2021 stood at 46%).

Given that Reality Labs expenses will increase meaningfully in 2023 we applied a 30% mark-up on the projected loss of FY’22 (assumed at $13.1B), resulting to an operating loss of $17.0B.

Taxes were assumed at 21% of operating profits, in line with guidance provided.

We added back to those figures a non-cash depreciation & amortization of 9%. This is higher than the historic figures (2019-2021 -> 7.6% & 9M 2022 7.5%) but considering the increasing CAPEX as a percentage of revenue we consider this adjustment fair.

CAPEX for FY’23 was estimated at $35.5B (guidance mid-point).

It shall be noted that we did not add back Stock Based Compensation as one way or another, this has a cost to existing shareholders (dilution).

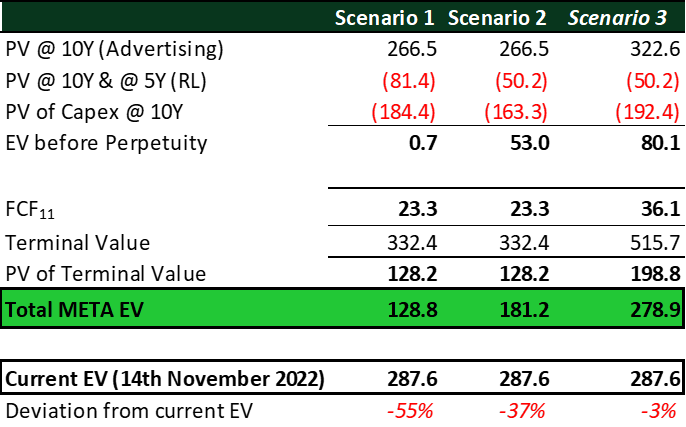

Scenario 1

We assumed that FY’23 figures will prevail for the next 10 years for both FoA and Reality Labs (“RL”), while in the process the Company’s CAPEX will decline gradually from 31.3% of revenue to 18.3% (average of 2012-2021).

It shall be noted that our stress model assumes that the investments in RL for the next 10 years, i.e., c. $189B in operating expenses and increased CAPEX requirements will not generate any meaningful benefit to META. An unlikely scenario as the company has a real option to abandon it earlier or downsize its investments in RL. Additionally, the stress model assumes that FoA margins will remain at current levels, implying that among others Reels and WhatsApp will remain under-monetized (again unlikely).

Using a ten-year period and a discount rate of 10% (the minimum required return that we aim to obtain from our investments under the current environment) we reach an Enterprise Value of almost 0.

For the terminal year we assume that RL will be abandoned and applied a terminal growth rate of 3% to FoA cash flows.

Based on these calculations, we reach an Enterprise Value (“EV”) of $128.8B or 55% lower than the current EV of $287.6B (14th November 2022).

Scenario 2

The differences compared to Scenario 1 are that RL is abandoned earlier (i.e., after year 5) and CAPEX is assumed to reach the 18.3% as a percentage of revenue by Year 6.

Based on these calculations, we reach an EV of $181.2B or 37% lower than the current EV of $287.6B.

Scenario 3

The difference compared to Scenario 2 is that Advertising/FoA Revenue is assumed to grow by 5% per annum (so CAPEX figures increase as well) whereas in the terminal year the growth remains at 3%. It shall be noted, that per Statista, digital advertising spend is expected to grow from $602.25B in 2022 to $876.1B in 2026 or 9.8% compound annual growth rate.

Based on these calculations, we reach an EV of $278.9B or 3% lower than the current EV of $287.6B.

Source: StockOpine analysis

In neither scenario we assumed that margins would expand, nor that RL would ever have a positive contribution to META and thus will be just abandoned.

Sensitivity analysis

These scenarios are rather extreme and in no case represent our best estimate. Therefore, we run sensitivity on Scenario 2 and Scenario 3 by changing FoA operating margin and the Discount rate demonstrating where the value of META can go if margins improve but without any additional revenue growth than what is included in these scenarios.

Source: StockOpine analysis

3. Concluding remarks

Meta core business is doing fine with engagement being intact and rather improving. Reels and WhatsApp could prove to be big winners if their monetization is successful (currently on right track) whereas the recent layoffs show that Zuckerberg cares for the company’s profitability and investments in RL are not at all costs. We remain bullish on META despite the outrageous expense and CAPEX forecasts for FY’23 and we believe that none of the above stress scenarios will materialize (we could be wrong).

You can find us at Commonstock and on Twitter @StockOpine.

Disclaimer: The team does not guarantee the accuracy or completeness of the information provided in the newsletter. All statements express personal opinions based on own financial and business analysis. Any estimates or forward-looking statements made are inherently unreliable. No statement of opinion is an offer or solicitation to buy or sell the financial instruments mentioned.

The content of our newsletter is not a trading or investment advice and we do not provide any personal investment advice tailored to the needs of any recipient. The information provided should not be considered as a specific advice on the merits of any investment decision. Securities trading involve risk and you might lose your capital and/or incur other damages. Investors should make their own research and consult their registered investment advisor or financial advisor before taking any investment decision.

Neither the team nor any of its affiliates accept any liability whatsoever for any direct or indirect loss however arising, from any use of the information contained herein. Any unauthorized copy of this newsletter or its contents is illegal.

This post may contain affiliate links, which means that we might get a commission if you decide to sign-up using any of these links. No extra cost is charged to you.

By subscribing / reading our newsletter or any affiliated social media accounts, you indicate your unconditional acceptance to the above and your unconditional acceptance to our terms and conditions.